Bespoke Short Interest Report: 6/13/16

Bespoke Stock Seasonality Report: 6/13/16

Bespoke Brunch Reads: 6/12/16

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Series Premiers

Inside O.J.: Made In America, ESPN’s best-ever 30 for 30 film by Richard Deitsch (Sports Illustrated)

The first of a five-part documentary under ESPN’s 30 for 30 franchise premiered last night, and the series has big potential. [Link, auto-playing video]

Why We Binge by Carl Quintanilla (Medium)

CNBC unleased a new effort to understand both the media business and the cultural phenomenon of binge watching; Carl introduces it with this essay. [Link]

Retail

Are We in a Mattress-Store Bubble? by Stephen J. Dubner (Freakonomics)

Mattress stores are ubiquitous and clustered, but why? And can the industry survive an influx of highly valued online competitors? [Link]

Cadillac Bets on Virtual Dealerships by Christina Rogers, John D. Stoll, and Gautham Nagesh (WSJ)

A huge dealer footprint and excessive inventories have led Cadillac to take an experimental approach to the business of selling cars. [Link, paywall]

Markets Business

The Alchemist Who Turned Toxic Assets Into Gold at Citigroup by Dakin Campbell and Donal Griffin (Bloomberg)

The story of a Citigroup desk that took big bets on CDOs which have paid off, making proprietary bets despite new regulations which are designed to prevent that kind of activity. [Link; auto-playing video]

Credit Suisse Boss Faces Revolt From Bankers Over Strategy Shift by Landon Thomas Jr (NYT Dealbook)

Efforts to revamp Credit Suisse by pulling away from investment banking businesses are not going well, either internally or in the firm’s stock price. [Link]

Kerviel Wins $517,000 as Judge Attacks SocGen Over Firing by Fabio Benedetti Valentini and Gaspard Sebag (Bloomberg)

Former rogue trader Jerome Kerviel has been awarded compensation by a Paris judge after he caused a $5.6 billion (yes, billion) trading loss. [Link]

Cultural Questions

The Strange, True, Tragicomic Story of EGOT by Sophie Gilbert (The Atlantic)

There isn’t a good summary for this off-the-wall story about winning an Emmy, Grammy, Oscar, and Tony, but it’s a fun diversion through the looking glass that is our popular imagination. [Link]

McDonald’s: you can sneer, but it’s the glue that holds communities together by Chris Arnade (The Guardian)

For much of the country, the humble McDonalds is not just a place to get decent, cheap coffee: it’s also a community hub that plays an important social role. [Link]

Rise of the Machines

How a Supercomputer Is Ready to Mint Money Out of Mexico’s Stock Market by Benjamin Bain and Patricia Laya (Bloomberg)

Emerging markets aren’t just emerging in terms of economic growth and development; in the case of Mexico, algorithmic trading is a decade behind the US and that means opportunity. [Link]

Jobs Threatened by Machines: A Once ‘Stupid’ Concern Gains Respect by Eduardo Porter (NYT)

An overview of universal basic income, a proposal designed to ameliorate the impact of technology stealing existing jobs; that’s all assuming, of course, that this time actually is different. [Link, soft paywall]

Byzantine Bonds

Trail of Defaults Leads to Dark Corner of Tax-Exempt Bond Market by Martin Z. Braun (Bloomberg)

Some municipal lenders use their tax exempt status to borrow on behalf of specific projects which wouldn’t otherwise classify as municipal deals. This article is a good overview of the details and drawbacks of the process. [Link]

The Hardest Part of the ECB’s Bond Buying Could Be Actually Buying the Bonds by Alastair Marsh (Bloomberg)

A summary of the operational details behind the ECB’s Corporate Sector Purchase Program (CSPP); while the nuts and bolts of the bond buying program may not be interesting to everyone, but we aren’t everyone! [Link]

Real Estate

Manhattan Landlords Boost Renter Incentives in Apartment Glut by Oshrat Carmiel (Bloomberg)

As new supply comes online, the typically rabid apartment rental market in Manhattan is showing some cracks for landlords. [Link]

REIT Surprise: How Real Estate Crushed the Stock Pickers by Ken Brown (WSJ)

A short history of one area of the market which has not only outperformed impressively but has largely been ignored by equity investors of all kinds. [Link, paywall]

Silicon Valley

Welcome to Larry Page’s Secret Flying-Car Factories by Ashlee Vance and Brad Stone (Bloomberg)

The co-founder of Google isn’t only focused on moonshots through Alphabet’s “Other Bets” division. He’s also ploughing tens of millions into an effort to build a flying car. [Link]

Traffic-weary homeowners and Waze are at war, again. Guess who’s winning? by Steve Hendrix (WaPo)

Apps like Waze are great for shaving a few minutes off a commute or errand run, but they’re increasingly exposing low-traffic thoroughfares to high traffic volumes, drawing the ire of residents. [Link]

Mathematics

An Ivy League professor explains chaos theory, the prisoner’s dilemma, and why math isn’t really boring by Elena Holodny (Business Insider)

A long but digestible interview of Steven Strogatz, a Cornell Professor of Applied Mathematics, including an overview of our favorite application of game theory, the Prisoner’s Dilemma. [Link]

Food

Why Is Chick-fil-A’s App Number One in the App Store? by Adam Chandler (The Atlantic)

The popular regional chicken chain (which we are fond of ourselves) is known for its simple sandwiches, but managed to teach the tech world a lesson about app popularity this week. [Link]

Orange Juice Costs Most in Four Years as Storm Threatens Florida by Marvin G. Perez (Bloomberg)

Brazilian citrus has already been damaged by rain, and it’s now the turn of the Florida crop, sending OJ futures to the highest in years. [Link]

Dogs

Firefighters gave a final, farewell salute to this old golden retriever, the last 9/11 rescue dog by Katie Mettler (WaPo)

This was a tear-jerker, no other way to describe it, as the nation has lost its last canine veteran of Ground Zero. [Link]

Mulligans

Islamic State Members From the West Seek Help Getting Home by Maria Abi-Habib (WSJ)

The war isn’t going so well for the Islamic State in eastern Syria and northern Iraq, and that’s leading a number of Western citizens to rescind on their pledge to join the caliphate. [Link, paywall]

Investing

Calculating the Return on Incremental Capital Investments by John Huber (Base Hit Investing)

A conceptual overview of incremental return on invested capital, an important concept for understanding forthcoming returns from a business rather than the total return on existing capital. [Link]

The BESPOKE REPORT — 6/10/16

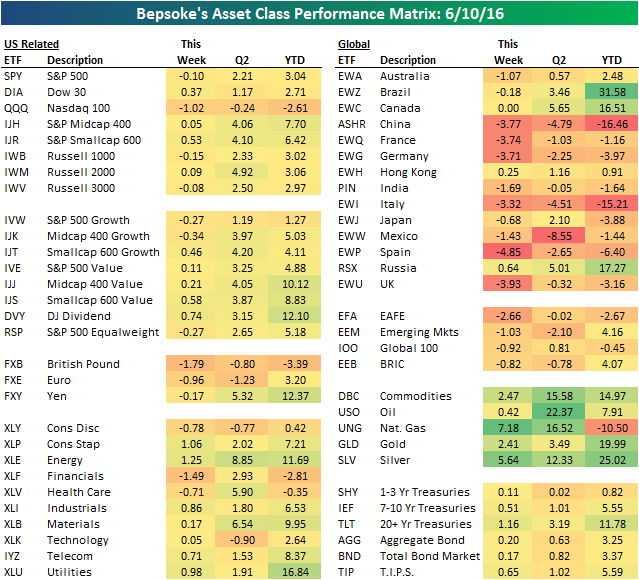

Below is a look at the recent performance of various asset classes using key ETFs tracked by Bespoke on a daily basis. The left side of the matrix is made up mostly of US equity ETFs, while the right side is made up of foreign equity market ETFs, commodity ETFs, and Treasury ETFs. As you’ll notice, there’s a lot more action going on outside of US equities, with big moves lower recently in foreign markets and big moves higher in commodities. France (EWQ), Germany (EWG), Spain (EWP), Italy (EWI), and the UK (EWU) all got crushed this week on Brexit fears, while natural gas (UNG) and silver (SLV) saw the biggest gains of any asset class.

Each week, Bespoke sends clients across all of its subscription levels the Bespoke Report newsletter. If you’re looking for Bespoke’s analysis of current market internals, economic data, earnings beats and misses, individual stock ideas, and more, the Bespoke Report has it all.

Continue reading this week’s Bespoke Report by starting a 14-day free trial to our paid content below.

Have a great weekend!

The Closer 6/10/16 – “End of Week Charts”

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we break down weekly Commitment of Traders data from the CFTC, recap weekly price action, and update economic surprise indices for world economies.

The Closer is one of our most popular reports, and you can sign up for a trial below to see it and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!

Bespoke’s Weekly Chart Book: 6/10/16

While none of the major averages got there this week, three sectors in the S&P 500 and nearly 20% of all stocks in the index traded to a 52-week high below. The three sectors (Consumer Staples, Industrials, and Utilities) are highlighted below. For updated charts of all the stocks in the S&P 500, check out our S&P 500 Weekly Chart Book.

Bespoke provides Bespoke Premium and Bespoke Institutional members with the S&P 500 Weekly Chart Book, which contains one year charts of every stock in the S&P 500 grouped according to sector. Whether you have five minutes or an hour, if you follow the charts, there is no faster way to get a read on which areas of the market are working and which are not.

See Bespoke’s S&P 500 Weekly Chart Book by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

ETF Trends: US Indices & Styles – 6/10/16

Your morning cup got a bit more expensive this past week with an ETF tracking coffee bean futures the best performer. Natural gas was also a good return, along with Silver, Gold, and much of the Energy complex. European ETFs were the worst performers across the board as EURUSD rolled over again and global equity markets were weakest in the Eurozone. Solar stocks have also been grim over the past week.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Sector Chart Attack: 6/10/16

As we head into the weekend, we wanted to provide a quick snapshot of where the charts of the ten S&P 500 sectors currently stand. Below we show one-year charts for each of the ten sectors and provide some discussion regarding trends of interest. We have also included the ETF that tracks each sector in parentheses.

One of the most ominous looking charts of the ten is the Consumer Discretionary sector (XLY). As shown below, the sector broke below its 50-DMA on Friday for the first time since the Memorial Day Weekend, and the pattern of a lower high that is forming looks eerily similar to patterns we saw last August and December. While the Consumer Discretionary sector has been under pressure, the Consumer Staples sector (XLP) keeps on trucking higher and actually traded to a new high just today. The Energy sector has been steadily trending higher off the lows earlier this year. This week, the sector took out its April highs but has sold off over the last two days. The sector is overbought and running into resistance from its highs last fall, so some back and forth churning here wouldn’t be a surprise.

One sector that just can’t catch a break these days is Financials (XLF). The sector has been in a pronounced downtrend for the last year now, as it still faces immense regulatory pressure and a dovish Fed keeping rates low. Zero interest rate environments don’t work for banks. The prognosis for the Health Care sector (XLV) is much more positive. Weakness among the biotechs (IBB) aside, the Health Care sector broke its downtrend in April, then pulled back and successfully tested that level and has now rallied again. What was once a downtrend of lower highs is now an uptrend of higher lows.

The chart of the Industrials sector (XLI) is also looking positive. After trading in a sideways range (with some steep sell-offs in between) for the better part of a year, Industrials broke upside resistance in April, and now looks to be establishing a range at higher levels. Like the Industrials sector, the Materials (XLB) sector also broke above upside resistance in April and has been establishing a range at higher levels. The Technology sector (XLK) has been doing a whole lot of nothing over the last year. In the process, it looks to have formed a long-term head and shoulders pattern, which would be a negative. That being said, these types of patterns, especially for indices or sectors, tend to look a lot better with the benefit of hindsight than in real-time.

Finally, as investors continue to reach for yield anywhere they can find it, Telecom Services (XTL) and Utilities (XLU) have been big winners. While the Telecom Services sector is just shy of 52-week highs, the Utilities sector is already there.

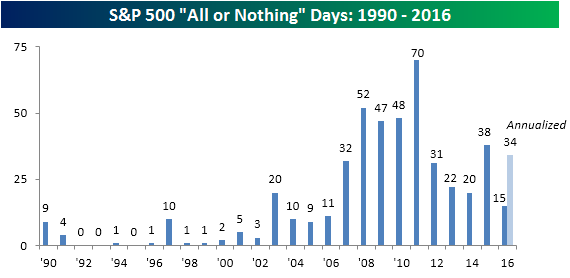

Weakest Breadth Since January

While buyers have been quick to step in on any weakness in the last several days, it is beginning to look more and more like they have headed out early to the beach this Friday. The S&P 500 is down nearly 80 basis points (bps) on the day, which doesn’t sound like a whole lot, but breadth has been abysmal. The S&P 500’s net Advance/Decline reading on the day is -413, meaning that there are 413 more stocks that are down today than up. That’s the weakest single day breadth reading for the S&P 500 since January 13th!

Today’s negative breadth reading also qualifies as an ‘all or nothing day’ for the S&P 500. If you are a long-time reader of our site, you are probably familiar with the term all or nothing day. For those that aren’t, we define an all or nothing day as one where the net number of advancing issues in the S&P 500 for a given day is either above +400 or below -400. While the year started out with a lot of all or nothing days, ever since the February lows, they have been few and far between, so today’s reading is a change of pace. As shown in the chart below, today’s reading (provided it holds) will be the 15th all or nothing day for the S&P 500 this year. At this rate, 2016 is on pace for 34 all or nothing days, which would actually be fewer than last year’s total of 38, but would still qualify as the sixth most for a year dating back to 1990.