The Closer 8/10/16 – Crude Crunch, Beveridge Bunched

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we chart the release of weekly EIA data on the petroleum market. We also discuss the evolution of the relationship between the job openings rate, the quit rate, and the unemployment rate.

The Closer is one of our most popular reports, and you can sign up for a trial below to see it and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!

ETF Trends: US Sectors & Groups – 8/10/16

Below is our daily list of the twenty best and twenty worst performing ETFs over the last five trading days. Every single one of our top twenty performers is a foreign country based or region based exposure, as the weakening USD allowed for gains in other areas. Turkey led the way, followed by Emerging Middle East and Asia, then by Japan JPY Hedged and Mexico. Natural gas and related stocks were the worst performers on the week. After performing very while last week, the biotech exposures joined the worst performers. Gold and healthcare related stocks also turned in poor performances.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

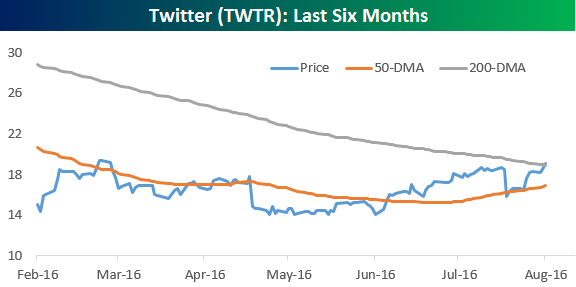

Twitter (TWTR) Finally Back Above Its 200-Day Moving Average

After a streak of 469 days below, Twitter (TWTR) finally traded back above its 200-day moving average today.

As you can see in the chart below, shares of Twitter (TWTR) have spent the large majority of time below the 200-DMA since the stock has been public. Will today’s positive cross-over mark a significant turning point?

High Season for Dividends

We’ve just published our August 2016 Dividend Screen for Premium and Institutional subscribers, which provides a list of all Russell 3,000 stocks going ex-dividend over the next two months. If you’re not yet a subscriber, you can start a free two-week trial at this link.

The second month of the quarter is typically high season for stocks going ex-dividend. For example, tomorrow there are a whopping 71 stocks in the Russell 3,000 going ex! (Remember, you have to own shares at the close on the trading day before the ex-dividend date to capture a stock’s dividend.)

Below is a list of S&P 500 companies yielding more than 2.5% that go ex-dividend through the end of August. Large-cap stocks like LyondellBasell (LYB), Chevron (CVX), Pitney Bowes (PBI), Mattell (MAT), and Navient (NAVI) are all included on the list, and they all have yields above the 4% mark. That’s at least 2.5 percentage points above the current yield of the 10-Year Treasury Note!

B.I.G. Tips – August 2016 Dividend Screen

B.I.G. Tips – New 52-Week Low For High Yield Spreads

Fixed Income Weekly – 8/10/16

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

This week, we spend some more time talking about rapidly rising LIBOR and what it means for other markets.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!

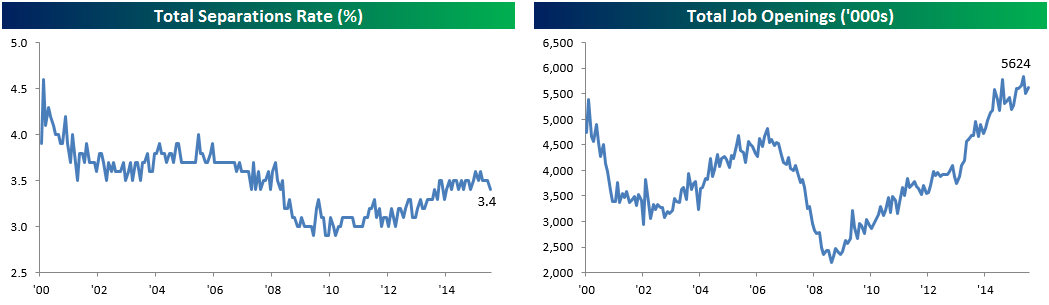

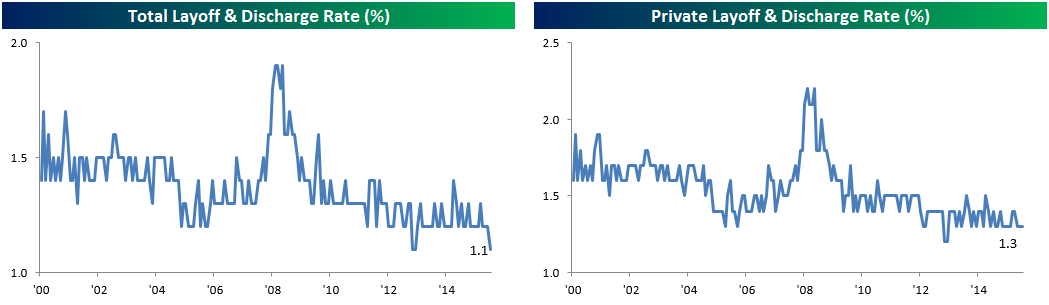

Layoffs Hit Lowest Recorded As Openings Rise Slightly

There were slight upward revisions to last month’s large sequential drop in job openings and June saw a slight MoM gain in openings, but total openings are below the all-time high set in the month of April. The total separations rate which includes all departures from a given job regardless of cause ticked down to the bottom of its two-year range.

Relative to employment as a whole, the openings rate ticked up MoM but still sits comfortably below May’s high water mark. As is typical, the private openings rate remains above the total rate due to lower government openings, but both remain in their solid upward trend as labor markets tighten.

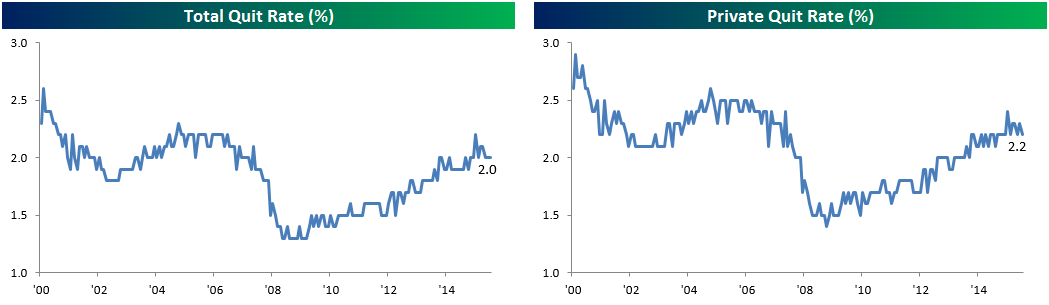

Despite wage growth acceleration in average hourly earnings, the employment cost index, the Atlanta Fed Wage growth tracker, and other measures, the quits rate remains much lower than would be predicted by the openings rate.

The best news from the June JOLTS report was a series low for the layoff and discharge rate, which matched its lowest levels recorded from back in 2013. Private layoffs and discharges are above that level, but sitting comfortably in the bottom end of their all-time range at 1.3%.

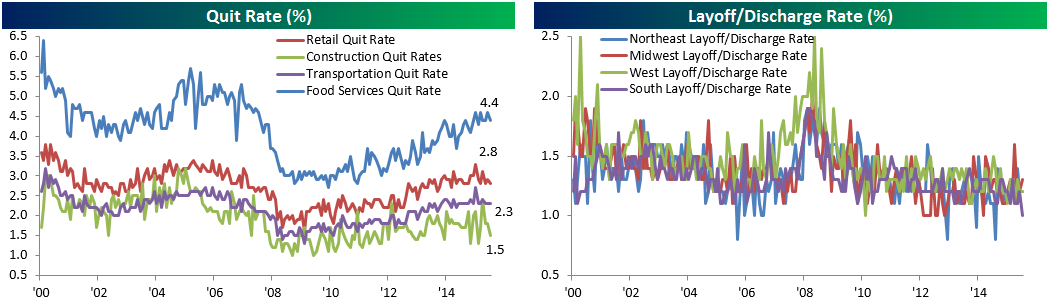

The South Census region recorded a new all-time low in its layoff rate, while other regions saw similarly low levels. Finally, we note that despite continued employment growth, wage growth, and steady labor demand the quit rate by industry has mostly flat-lined among low pre-requisite industries. As shown below, only the Food Services quit rate continues to trend higher.

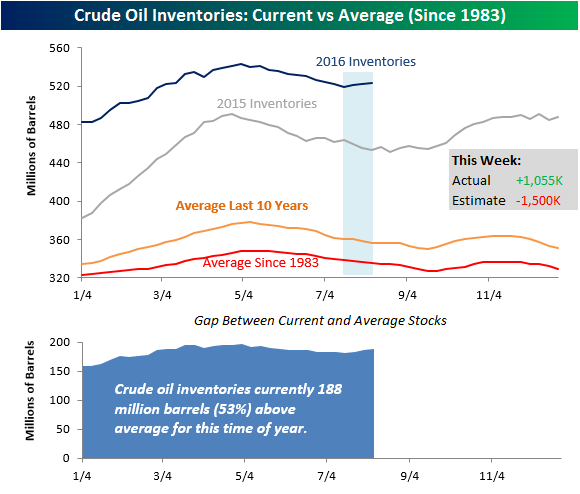

Crude Oil Inventories Continue to Rise; Gasoline Stocks Decline

After declining for a record nine straight weeks, crude oil inventories have now risen for three straight weeks. According to the DoE, crude oil stockpiles increased by 1.055 million barrels compared to expectations for a decline of 1.5 million barrels. As shown in the shaded box in the top chart, crude inventories have been rising for the last three weeks, at a time of year when they are typically declining. With the increases over the last three weeks, crude oil inventories are currently 188 million (53%) above average for this time of year and within 20 million barrels of their multi-decade peak.

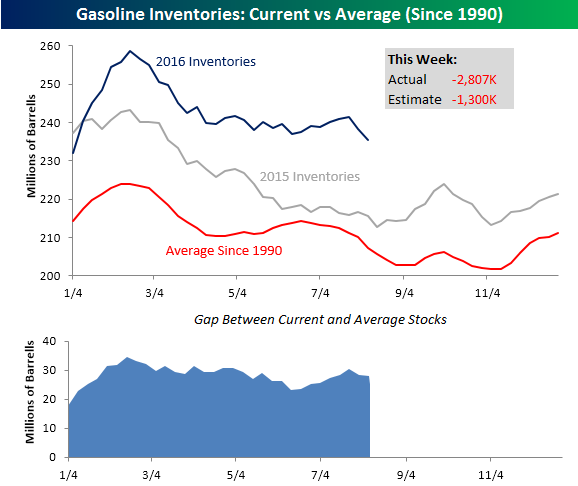

While crude oil inventories unexpectedly increased, gasoline stocks saw a larger than expected decline for the second straight week. As shown in the top chart below, stockpiles were expected to decline by 1.3 million barrels this week, but the actual decline was more than twice that at 2.8 million barrels, making the two-week decline more than 6 million barrels.

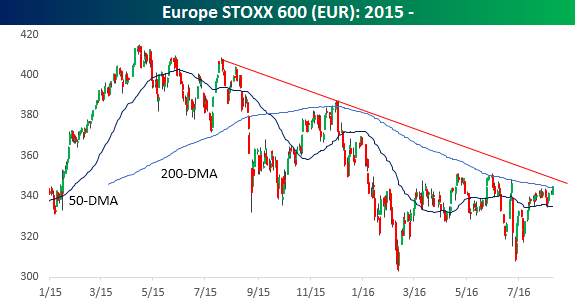

STOXX 600 Peeks Above 200-DMA

The STOXX 600 index contains 600 large, mid, and small cap European equities from 18 different countries and is widely considered a benchmark index for the stock market in Europe. Yesterday, the index achieved somewhat of a milestone as it closed above its 200-DMA for the first time in 2016. As shown in the chart below, many attempts have been made and on multiple occasions the index traded above the 200-DMA on an intraday basis, but yesterday was the first time since last November that the index actually traded and closed above that level. Even after the break above the 200-DMA, though, the STOXX 600 remains in a trend of lower highs that has been in place since the middle of 2015.

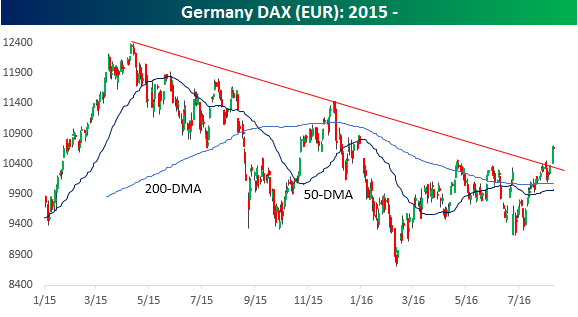

While the STOXX 600 is not out of the woods yet, German equities have been quite strong lately. In the last couple of days, Germany’s benchmark index (DAX) broke above its downtrend from last Spring.

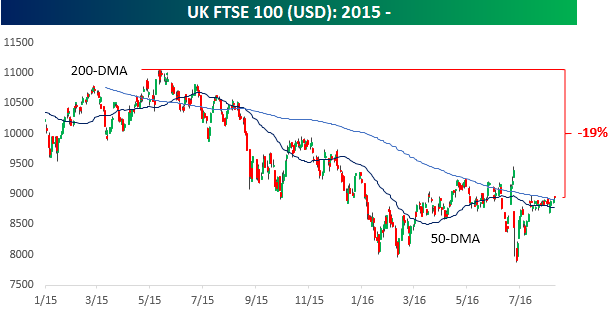

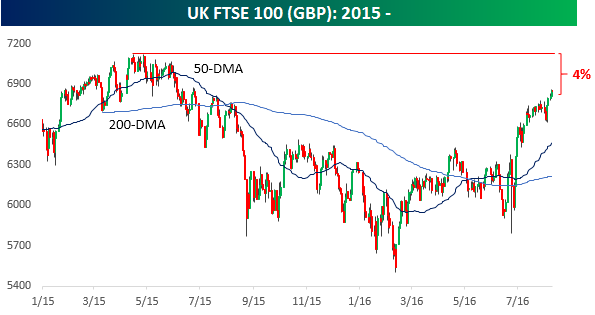

On the subject of Europe, the FTSE 100 has absolutely been on fire over the last several weeks. Not only did the index break its downtrend, but it is currently within 4% of taking out its 2015 high.

The chart above of the FTSE 100, however, is a bit misleading because it doesn’t take into account the big decline in the British Pound since the Brexit vote in June. In the chart below, we show the performance of the FTSE 100 in dollar adjusted terms since the start of 2015. After accounting for the large decline in the pound, the FTSE 100 is still close to 20% from its 2015 highs. Keep this in mind when you hear people talking about the performance of the UK stocks in the post-Brexit environment. It seems as if every day we either hear or read a story pointing to the chart above as an example of how the Brexit vote has been good for the UK stock market, but the reality, which is closer to the chart below, is much different.