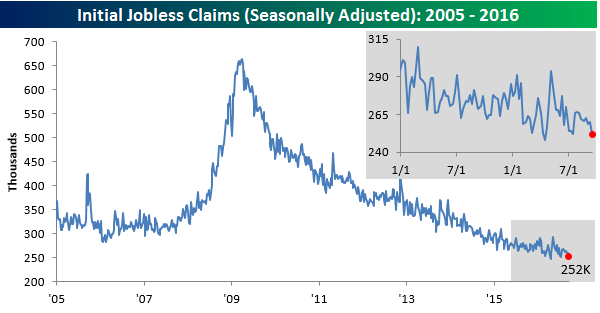

Jobless Claims Fall Further

This week was the first time in eight weeks where economists’ consensus expectations for jobless claims was not 265K, and while they finally lowered their consensus forecast to 261K, the decline wasn’t enough as first time claims dropped to 252K, which was the lowest weekly reading since mid-July. At the risk of sounding like a broken record, this week’s report represents the 81st straight week that claims have been below 300K, which is the longest streak in over 40 years.

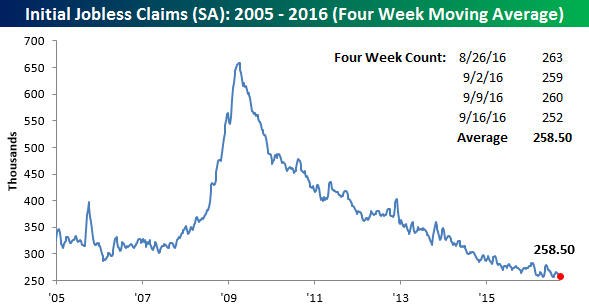

With this week’s decline, the four-week moving average dropped from 260.75K down to 258.5K. That’s the lowest level since late July and just 2.5K above the cycle low of 256K from April. We had a hard time believing that we would ever get back down near the cycle lows, but another week like this week’s print and the four-week moving average will be right there.

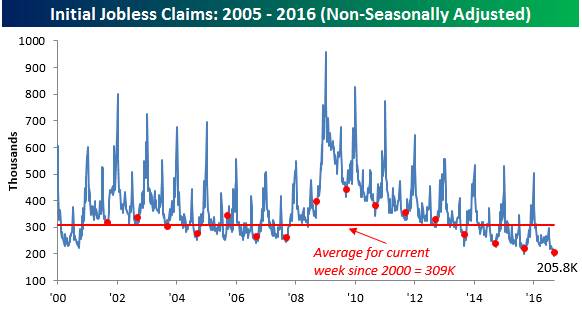

On a non-seasonally adjusted basis (NSA), jobless claims rose from 193.3K up to 205.8K. Despite the increase, this week’s reading is more than 100K below the average for the current week of the year since 2000 and the lowest reading since 1973. Judging by the standards of jobless claims at least, the labor market remains in pretty good shape.

Bears Rule the Roost

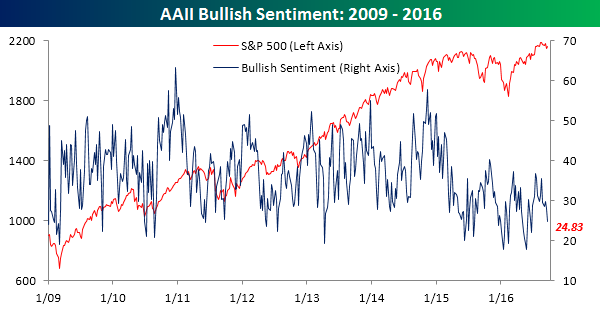

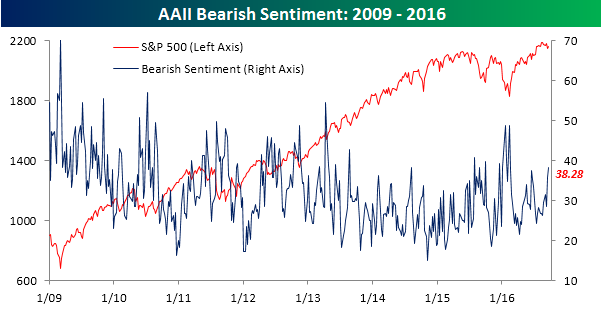

The S&P 500 closed Wednesday less than 1.5% from an all-time closing high, but looking at the most recent sentiment figures from AAII, you would think that equities are in a bear market. According to this week’s sentiment survey, bullish sentiment fell to 24.83% down from 27.94%. That’s the lowest weekly reading since late June, the 47th straight week that bullish sentiment was below 40%, and the 81st time in the last 82 weeks that we have seen sub-40% readings. Based on this survey at least, it is hard to say that investors are complacent.

While the bullish camp increasingly shrinks, bears are showing up all over the place. It wasn’t just the recent Delivering Alpha conference from CNBC where bears were everywhere, but individual investors are increasingly bearish. According to this week’s survey, bearish sentiment increased from 35.92% up to 38.28%. This is the first week that bearish sentiment has been higher than both bullish and neutral sentiment as well as the highest weekly reading since the February market lows.

The Closer 9/21/16 – …And Miles To Go Before I Hike

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we review the FOMC decision, giving a complete recap of price action around the decision for more than 30 different assets. We also discuss the RBNZ decision that took place this evening.

The Closer is one of our most popular reports, and you can sign up for a trial below to see it and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!

Most Loved and Hated Stocks in the Russell 3,000

Yesterday, we highlighted a list of the Russell 3,000’s most heavily shorted stocks. This afternoon, we’re looking at the most loved stocks by analysts in the index. To make the list, the stock has to be covered by at least 10 analysts. The 35 stocks below have at least 92% “Buy” ratings by analysts. For this analysis, ratings like “Overweight” or “Outperform” are considered “Buy” ratings as well. In the Russell 3,000, there are 12 stocks that have 100% “Buy” ratings. These include Norwegian Cruise Line (NCLH), Planet Fitness (PLNT), Paycom (PAYC), LendingTree (TREE), Vonage (VG), and Affiliated Managers (AMG). Other notables on the list of most loved stocks include Broadcom (AVGO), salesforce.com (CRM), AMC Entertainment (AMC), and Sabre (SABR).

While it’s nice to be loved by analysts, this type of bullishness in the Wall Street community doesn’t leave much room for improvement. If a stock already has 100% “Buy” ratings, it can’t benefit from any upgrade calls! Contrarians can use this list to find potential names that may be too loved at the moment. Next to each stock on the list, we’ve included its short interest levels as a percentage of float (SIPF) and year-to-date percentage change. Stocks with low short interest that have had big runs this year already may be names to avoid. If the stock has high short interest levels, it means the analyst community has quite a different take on the company than actual investors. In this regards, names like LendingTree (TREE), Paycom (PAYC), Carrizo Oil & Gas (CRZO), Cempra (CEMP), and Amsurg (AMSG) stand out.

We’ll be back tomorrow with a list of the Russell 3,000’s most hated stocks by analysts.

Chart of the Day: Are We Still Seeing Late-Day Buying?

B.I.G. Tips – Caterpillar Sales Rebound

Fixed Income Weekly – 9/21/16

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

This week, we take a look at what’s driven performance YTD in the municipal market. We also give a trade idea based on last night’s BoJ meeting.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!

ETF Trends: Hedge – 9/21/16

Mexico continues to be pounded lower as market participants use it as a proxy for a Trump Presidency. Homebuilders, Italy, GBP, and EUR have also underperformed over the last few days. On the green side of the slate, Indonesia, Taiwan, and Biotech continue to rally while steel and iron ore-related names get something of a bounce. Natural gas has also broken out and is trending higher.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

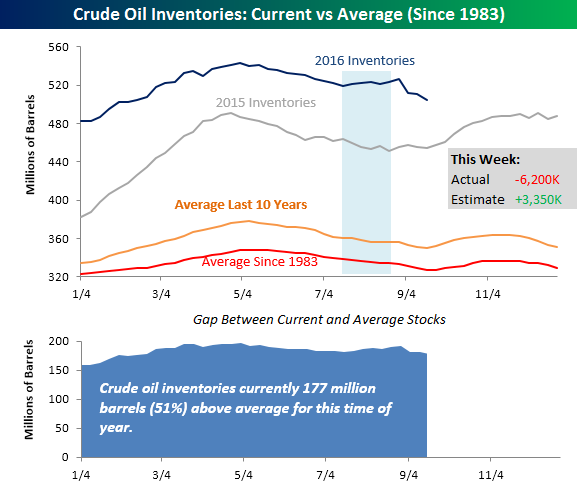

Energy Inventories Continue to Decline

Following on the heels of yesterday’s report from the API, today’s release of weekly crude oil and gasoline inventories showed notable declines. In the case of crude oil, inventories declined by 6.2 million barrels, compared to expectations for a gain of 3.35 million barrels. You may recall two weeks ago that a much larger than expected drawdown in crude oil inventories was attributed to weather impacts from Tropical Storm Hermine. Because of that inventories were expected to rebound in the coming weeks. So far, though, those increases have yet to materialize as the last two weeks have continued to see declines. With this week’s decline, US crude oil inventories are still 177 million barrels above their historical average dating back to 1984, but that is the lowest ‘surplus’ and lowest total level since February.

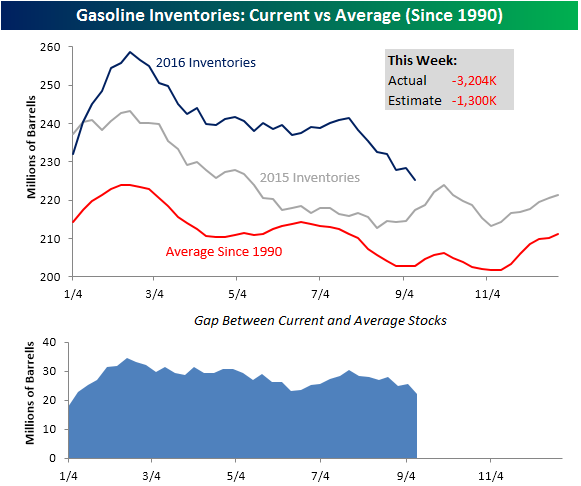

Gasoline stockpiles were expected to decline by 1.3 million barrels this week, but the actual decline was about 2.5 times that at -3.2 million barrels. As shown in the chart, the recent declines in gasoline stockpiles have come at a time of year when they are typically starting to level off or even rise. As a result, gasoline stocks are not far from levels where they were at this time last year.

Bespoke CNBC Appearance (9/21)

Bespoke’s Paul Hickey appeared on CNBC’s Fast Money on Tuesday evening to discuss the Fed and elections. To view the segment please click on the image below.