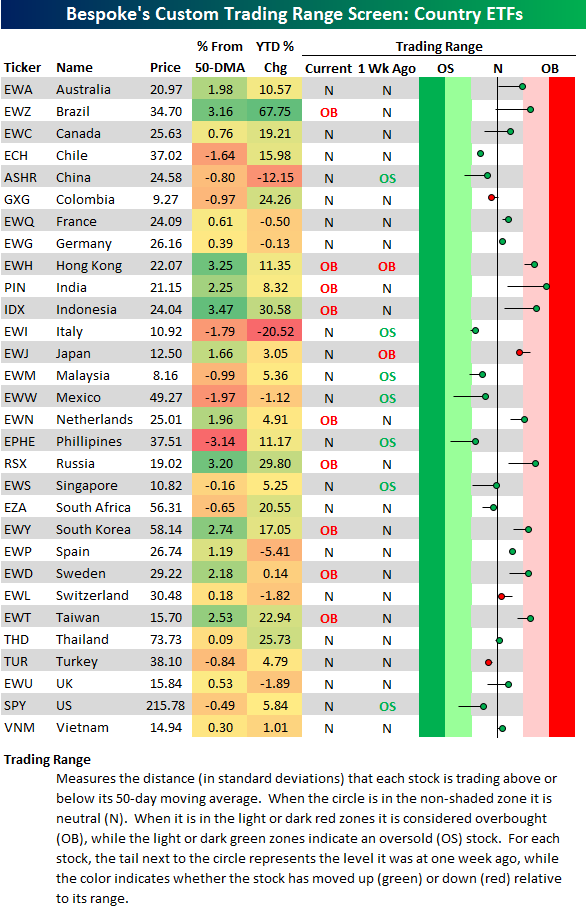

Bespoke’s Country Trading Range Screen

Below is an updated look at our country trading range screen using key ETFs traded on US exchanges. For each ETF, the dot represents where it’s currently trading, while the tail end represents where it was trading one week ago. The black vertical “N” line represents each ETF’s 50-day moving average, and moves into the red or green zones are considered overbought or oversold.

Last week at this time, most ETFs were in neutral territory, but there were more oversold areas than overbought. As of the close today, not one country ETF is oversold, while nine of thirty are overbought. The US (SPY) is one of the few countries still trading below its 50-day moving average.

India (PIN), Indonesia (IDX), Russia (RSX), Brazil (EWZ), and Australia (EWA) are a few areas of the world that have seen big upside momentum over the last week. India is the most overbought country in the screen, while Indonesia, Russia and Brazil aren’t far behind.

The average country in the screen is now up 10% year-to-date, and 22 of 30 are in the black for the year versus 8 that are in the red. Italy (EWI) remains the biggest loser with a drop of 20.52% YTD, while Brazil (EWZ) is by far the biggest winner with a gain of 67.75%.

Chart of the Day – October Intra-Month Performance

What Worked, What Didn’t in Q3: Bespoke’s Quarterly Outlook

On Friday, September 30th, we held our Q4 Outlook call for clients. This is the third quarter in a row we’ve held an outlook call, which has proven to be a very popular feature among Bespoke clients. The quarterly outlooks are an outgrowth of Bespoke’s widely read and quoted annual outlook piece, The Bespoke Report, which is released at the end of December each year. A recording of Friday’s call and the 26-page presentation are available with any paid membership to Bespoke. Review our subscription options and choose any plan to listen to the call and view the presentation. In the call, we discussed:

- Why we think valuations are excessive but are not likely to be the spark for a sell-off.

- Why from a seasonality perspective, we were not surprised at all by the uptick in volatility in September.

- Why weak sentiment among individual investors and the analyst community are key contrarian support indicators heading into Q4.

- Why technicals, seasonality and history support a positive outlook for stocks in Q4.

- Why elections matter for Q4 performance.

In addition to looking forward to Q4, we also looked back to see what worked in Q3. As you can see in the preview below of one page from the presentation, Q3 was all about “rotation.” The biggest winners from the first half of 2016 were the big losers in Q3, while the weakest stocks in the first half out-performed dramatically in Q3. That probably doesn’t bode well for active managers like hedge funds, unless they managed to rotate their books appropriately!

ETF Trends: Fixed Income, Currencies, and Commodities – 10/3/16

Oil-related ETFs continue to outperform dramatically, with drilling services names leading the charge higher in the wake of last week’s announcement by OPEC that some production is likely to be shuttered. Norway, Mexico, and Brazil have benefited. Over the last week some of the worst performers have been natural gas, utilities, and REITs as dividend plays have come under pressure. Biotech and gold have also underperformed somewhat.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Bespoke Stock Seasonality Report: 10/3/16

B.I.G. Tips – October 2016 Seasonality and Calendar

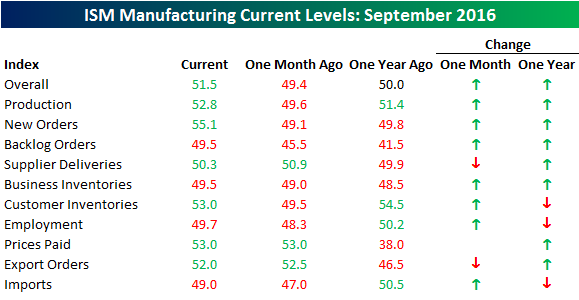

ISM Manufacturing Leads a September Rebound

While it’s still premature to categorize the weak economic data of the last month as nothing more than a late summer lull, today’s ISM Manufacturing report provides good evidence for people who subscribe to that narrative. In September’s report, economists were expecting a headline reading of 50.4 versus last month’s reading of 49.4. The actual reading, however, came in at 51.5, which erased half of the decline from August. Even with this month’s rebound, the headline index remains well off of its summer high of 53.2.

The internals of this month’s report also looked positive. While four of the index’s components slipped into contraction territory in August, three moved back into expansion territory in September. The biggest increases this month came in New Orders (+6.0) and Backlog Orders (+4.0), while the only declines came in Supplier Deliveries (-0.6) and Export Orders (-0.5). Relative to a year ago, breadth was even stronger as the headline index and seven out of ten subcomponents all increased y/y.

Early Readings Pointing To A Solid Month For Auto Sales In September

Auto sales for the month of September are being reported throughout the day today, and we’ll be tracking them as they’re released here on the blog. Make sure to check The Closer tonight (sent to our Institutional clients) for a full recap of the day’s reports and what it means for the broader economy. This month, the seasonal adjustment factor for the auto market as a whole is about 0.97; headlines sales numbers NSA will be annualized and then boosted by about 3% as the market enters the slower fall selling season.

Auto sales for the month of September are being reported throughout the day today, and we’ll be tracking them as they’re released here on the blog. Make sure to check The Closer tonight (sent to our Institutional clients) for a full recap of the day’s reports and what it means for the broader economy. This month, the seasonal adjustment factor for the auto market as a whole is about 0.97; headlines sales numbers NSA will be annualized and then boosted by about 3% as the market enters the slower fall selling season.

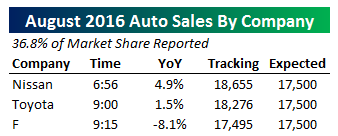

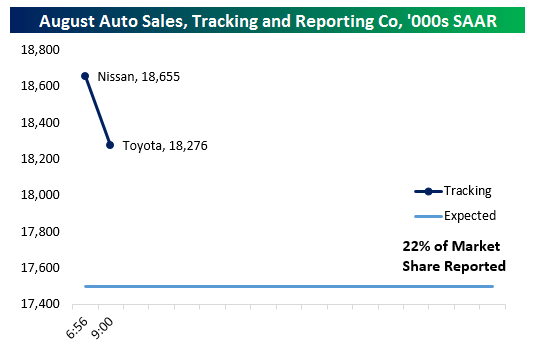

Early releases from Nissan and Toyota were solid, with Nissan announcing a 4.9% YoY sales gain. Toyota missed expectations for a 2% YoY gain with a 1.5% figure but its report kept tracking well above the 17.5mm SAAR estimate. Ford was weak, as expected, with sales falling 8.1% YoY versus 8% estimated, but even with that huge drop, the market is tracking in-line versus estimates with about a third of the industry having reported. We will continue to update these figures throughout the day.

Update 1 9:39 AM: GM reported sales about in-line with expectations, selling 0.6% fewer cars than September of 2015, versus -0.5% estimate. Despite the slight miss, after seasonal adjustment our tracker for auto sales ticked up slightly and with 54% of the market reported we are now showing a seasonally adjusted sales pace of about 17.55mm vehicles.

Update 2 9:51 AM: Fiat-Chrysler was expected to see sales declines of over 5% but the final member of the “Big Four” US auto sellers reported volumes only the smallest margin lower than a year ago, bringing our tracker for industry-wide sales up to 17.59mm SAAR. Two-thirds of the market is now reported and we are tracking a modest beat versus the 17.5mm SAAR estimate.

Update 3 10:16 AM: Honda was expected to report a 1.6% YoY gain in US vehicle sales for September but came in a -0.1% growth. Despite that miss, our tracker now stands at 17.6mm SAAR with almost 80% of the auto market reported; unless remaining companies report very, very large misses, it’s unlikely total sales will miss analyst estimates for September at this stage.

Update 4 2:33 PM: A number of minor automakers reported over the last few hours, totaling about 16% of market share. Results were varied, with Subaru, Hyundai, and Mercedes all posting solid gains but big declines at BMW and a relatively weak month at Kia. The net impact on our tracker has been slightly positive, and we’re on pace for a beat of about 0.1mm SAAR with over 92% of the industry reported. All major auto brands have now reported. We will update the chart below with the final numbers from Ward’s Auto when they are released but by our calculations auto sales came in at 17.62mm SAAR in the month of September.

Bespoke Brunch Reads: 10/2/16

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Business of Finance

Blackstone’s Top Dealmaker Says Now Is The Most Difficult Period He’s Ever Experienced by Devin Banerjee (Bloomberg)

High prices for everything with a cash flow have made the life of long-term purchaser of businesses very, very painful. [Link]

A quick Deutsche ‘splainer by Dan Davies (Medium)

Published ahead of the 14% rally in DB shares to end the week, Davies provides an excellent overview of the situation DB finds itself in. [Link]

Food

When Restaurants Ditch the Dining Room by Serena Dai (NY Eater)

There’s an increasing trend towards getting rid of the front of house entirely with the surging popularity of online platforms for food delivery. [Link]

Turning Breakfast Waste into Food for Commerce by Michele Wucker (strategy+business)

A dizzying array of food waste is being turned to alternative uses, running the gamut of the breakfast menu. [Link]

Real Estate

Pinching Pennies in the Hedge-Fund Capital of America by Oshrat Carmiel and Katia Porzecanski (Bloomberg)

Brutal returns for hedge funds are having spillovers in the local economy where they are most geographically concentrated, from car dearlerships to home prices. [Link]

Housing Highlights From The 2015 ACS by Jed Kolko (Terner Center For Housing Innovation)

An excellent summary of the data contained in the most recent release of the US Census American Community Survey for the year of 2015. [Link; 29 page PDF]

26 crazy pictures of micro-apartments around the world by Chris Weller (Business Insider)

Urban living at its smallest, from Kips Bay 300 square-footers running over $2,000/month to some of the most crowded city slums in the world. [Link]

Sports

Who Actually Won the Moneyball Revolution? by Josh Levin (Slate)

A retrospective on the statisticization of baseball, a process that began in earnest with the success of Billy Beane in Oakland but has continued to this day. [Link]

Fantasy Football Season Is Starting. Here’s How the Phenomenon Began by Ashley Ross (Time)

Nearly one-sixth of the country plays fantasy football, a pastime that is also tied to Oakland (see link above). Raiders fans, not known for their pocket protectors, appear to have spawned the couch-bound GMing so prevalent today. [Link]

Art

What Happened to Bob Ross’ Paintings by Lucas Reilly (Mental Floss)

The veteran host of The Joy of Painting has not only soothed the nation with his calm commentary on each oily creation he spawned, but also helped out hundreds of PBS stations with his work. [Link]

6 Photographers Shot the Same Person and the Results are Astonishing by Joel Comm (World Village)

Perspective isn’t just an optical phenomenon – it also perpetuates a fallibility of the human condition. Photographers told different stories about a subject produced almost shockingly different portraits of the same man. [Link]

Innovation

Aetna to Transform Members’ Consumer Health Experience Using iPhone, iPad and Apple Watch (Business Wire/Aetna)

One of the nation’s largest insurers is offering to subsidize the consumers’ purchase of Apple Watches, and effort to improve monitoring and health awareness. [Link]

Startup Cargo Cults: What They Are and How to Avoid Them by Leo Polovets (Coding VC)

An excellent read on the mistakes that start-ups often make in emulating organizations which have found success in the past. [Link]

Implementation Guidance for Executive Order 13707: Using Behavioral Science Insights to Better Serve the American People by John P. Holdren (Executive Office Of The President – Office Of Science And Technology Policy)

The White House has decided to emphasize a focus on behavioral science by executive agencies as a way to improve uptake of government programs and reduce hurdles to policy implementation. [Link; 12 page PDF]

How Actual Nuts and Bolts Are Bringing Down Oil Prices by Tracy Alloway (Bloomberg)

Some of the largest innovative leaps are conducted under the greatest pressure – in this case, mass efficiency in the oil industry, catalyzed by the price declines of the last few years. [Link]

Age & Economics

U.S. Real Wage Growth: Fast Out of the Starting Blocks by Robert Rich, Joseph Tracy, and Ellen Fu (NY Fed Liberty Street Economics)

Quantitative analysis of the path of wage growth throughout a worker’s career. Growth is slowest at the start of careers, accelerates into middle age, then trails off towards retirement. [Link]

Older Americans Are Jeopardizing Their Retirement With Divorce by Carol Hymowitz (Bloomberg)

It turns out that the end of a marriage is not just the end of a romance, but also a devastating blow to financial wellbeing. Separate households cost more, not to mention the tax consequences and legal costs of a divorce. [Link]

Substance Abuse

For Small-Town Cops, Opioid Scourge Hits Close to Home by Jeanne Whalen (WSJ)

A distressing dispatch from the front lines of the fight against powerful new opiods which are ravaging communities across the United States. [Link; paywall]

Retailing

The H&M Sandwich by Shelly Banjo & Andrea Felsted (Bloomberg)

Stuck with higher prices than new entrants and less cache than alternatives, H&M is in a very painful place; sales are down to their lowest growth rates in recent memory. [Link]

Global Concerns

The ECB on the Slowdown in Global Trade by Brad Setser (Council on Foreign Relations)

A summary and analysis of the ECB’s recent effort to understand the slowdown in global trade; China is the primary culprit. [Link]

Key facts about the world’s refugees by Phillip Connor and Jens Manuel Krogstad (Pew Research Center)

10 bullet points (with accompanying charts, of course) on the demographics and displacement of the world’s 60 million refugees. [Link]

Volatility

The relationship between VIX futures term structure and S&P 500 returns by Athanasios P. Fassas (University of Sheffield)

An empirical analysis of the VIX term structure’s predictive power for the path of equity prices in the underlying index. [Link; 19 page PDF]

The Closer 9/30/16 – End of Week Charts

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model.

The Closer is one of our most popular reports, and you can sign up for a trial below to see it and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!