Bespoke Brunch Reads: 10/16/16

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Fixed Income

Banks deflect attempts to bring sunlight to bond dealing by Robin Wigglesworth (FT)

An overview of the debate between market participants over whether more information would improve or hurt liquidity for the world’s largest financial market. [Link; paywall]

Procrastination as a strategy in the global reach for yield by Alexandra Scaggs (FT Alphaville)

An overview of where money markets stood on the brink of reforms whose deadline passed last week. Very worthwhile for those not yet up to speed on this market. [Link; registration required]

Nobel Prize Winner Wants You to Stop Treating Bonds Like Stocks by Isobel Finkel (Bloomberg)

A summary of the most recent Nobel Prize laureate’s views on the difference between stock and bond markets; definitely an obscure approach, but one worth understanding. [Link]

Profiles

Brad Katsuyama Q&A: ‘I Don’t Think We Would Have Survived If It Was Just Hype’ by Matt Levine (Bloomberg)

The text version of Levine’s podcast interview with Katsuyma, who was featured in Michael Lewis’ most recent book Flash Boys. An interesting read for the market structure details, the business discussion, and the personal story. [Link]

Bob Diamond’s Misadventures in Africa by Renee Bonorchis, Donal Griffin, and Paul Wallace (Bloomberg)

A long read over the most recent exploits of the former CEO of Barclays, who departed following the 2012 LIBOR manipulation scandal. [Link]

Economic Data

Jordà-Schularick-Taylor Macrohistory Database by Òscar Jordà, Moritz Schularick, and Alan M. Taylor (Macrohistory.net)

This one was is less of a read and more of a data dump. The database contains a massive chunk of information about national economies dating back well into the 19th century and is an invaluable research tool. [Link]

Politics

Where Do Clinton And Trump Have The Most Upside? by David Wasserman, Reuben Fischer-Baum and Ritchie King (538)

A county-by-county analysis of where each party stands to gain or lose the most based purely on demographic shifts amongst non-college whites, college-educated whites, and non-white voters. [Link]

GOP Pollster Frank Luntz Reveals Replicas of the Oval Office, Monica Lewinsky’s Blue Dress in His L.A. Home (Photos) by Peter Kiefer (The Hollywood Reporter)

It takes all kinds to make the world go ‘round, and in the case of veteran GOP pollster Luntz he makes the world go ‘round with an impressive ode to patriotism in his Los Angeles home. [Link]

ETF Launches

ETF Watch: Whiskey Fund Launches (ETF.com)

Fans of strong brown water can now add that particular asset to their portfolios with shares in this fund which owns publicly traded manufacturers of alcohol. [Link]

How a Blogger Started His Own ETF by Simon Constable (WSJ)

We’ve followed Eddy Elfenbein for a long time and like his straightforward, data-driven approach to markets. Best of luck to him with his new actively-managed ETF which includes the interesting feature of higher fees for outperformance and lower fees for underperformance. [Link]

Academic Efforts

What Is the New Normal for U.S. Growth? by John Fernald (FRBSF Economic Letter)

Why has GDP grown slower post-recession and been decelerating overall for many years? This letter does a good job unpacking the various factors and their outlook in the future. [Link]

Turning Over Accepted Wisdom with Turnover by Cliff Asness (AQR Cliff’s Perspectives)

An expansion of a recent paper by AQR partner Lasse Pedersen which investigates the proposition that all active managers are fighting over one pie of performance and therefore anyone outperforming must have a corresponding underperformer as well. AQR maintains this isn’t the case. [Link]

Real Estate

Bleak Times at the Mall by Justin Lahart (WSJ)

The ongoing decline of the mall thanks to shifts in consumption and other factors is something we’ve noted previously, but this post does a solid job recapping the issue. [Link; paywall]

The Weak Outlook for Residential Investment by Jordan Rappport (FRB KC Macro Bulletin)

This quick summary makes the case that the current slowdown in US construction spending is a function of the supply-side, not weak demand, a view we at Bespoke have held over the last few quarters. [Link; 4 page PDF]

Are Backyard Apartments Helping Austin’s Affordability? by Syeda Hasan (NPR KUT)

A fascinating case study on the microeconomics of housing supply and regulation, which isn’t necessarily amenable to common-sense solutions which look good on paper. [Link]

Report: $272 Billion Tied Up In Accumulated Private Sector Vacation Time (Project: Time Off)

Unused vacation time sits on corporate balance sheets as a liability, a fact that Project: Time Off used to their advantage by analyzing corporate disclosures to gauge just how much time off American workers have left unclaimed. [Link]

The Obama Legacy

PHH wins landmark victory: CFPB ruled unconstitutional by Ben Lane (Housingwire)

The Court of Appeals for the DC Circuit has handed down a remarkable defeat for the Dodd-Frank Act’s new regulator, the Consumer Financial Protection Bureau. The court has ruled the CFPB unconstitutional, due to its unique governance structure. We’re reasonably sure this will head to the SCOTUS at some point. [Link]

Energy-related CO2 emissions for first six months of 2016 are lowest since 1991 (EIA Today In Energy)

After the last recession, vehicle miles travelled recovered slowly, and are still well below peaks on a per-capita basis. That, combined with much stronger fuel efficiency standards, a huge decline in coal’s share of power generation, and the rise of cleaner burning natural gas have all helped push down CO2 emissions dramatically despite a return to growth. [Link]

Healthcare

Tracking your steps might not help: New study shows Fitbits do not improve health by Jamie Cohen (Duke Chronicle)

A new paper from a professor at Duke has shown that adding Fitbits (or other fitness trackers) does not necessarily improve health care outcomes. [Link]

More Than 1 Million to Lose Obamacare Plans as Insurers Quit by Zachary Tracer, Tatiana Darie, and Katherine Doherty (Bloomberg)

As Aetna, UnitedHealth, and other state or regional insurers have pulled out of state or federally run healthcare exchanges, 1.4 million people in 32 states will be forced to buy insurance elsewhere – often with higher premiums. [Link; auto-playing video]

Law & Order

Facebook, Twitter, and Instagram surveillance tool was used to arrest Baltimore protestors by Russell Brandom (The Verge)

The ACLU recently published a report showing that police used social media surveillance provider Geofeedia to identify protestors and arrest them. Facebook, Instagram, and Twitter have all revoked access to their APIs for the company following the report. [Link]

Gadgets

Curta calculator: The mechanical marvel born in a Nazi death camp by David Szondy (New Atlas)

A grim origin, obviously, but this is a fascinating bit of mechanical engineering: a hand-cranked calculator that can be built at home. [Link]

Food

The Missionary by Dana Goodyear (The New Yorker)

A fascinating longform effort at recounting the culinary history of San Diego’s southern neighbor and a profile of a chef working to return it to its former glory. Note: this story dates back to 2012, but is still a great read! [Link]

Brexit

Brexit: Some lessons from Greece by Duncan Weldon (Medium)

Applying the political and game theoretical (as well as economic) lessons of the Greek debacle to the current issue of Brexit negotiations; very thoughtful and well done. [Link]

Models

Aswath Damodaran doesn’t *quite* agree with Bernstein’s bashing of DCF models under zero rates by David Keohane (FT Alphaville)

A thorough debunking of the idea that low rates make discounted cashflow models unworkable. [Link; registration required]

Miscellaneous

30 for 30 Shorts: The High Five (ESPN)

Not a read, but this ten minute oral history on the origins of the high five is more than worth your time to watch. We were amazed at what a recent development the high five really is. [Link; auto-playing video]

The Bespoke Report — Small-caps, Biotech Struggle as Election Nears

US equity markets finished the week solidly in the red, led lower by small-caps and biotechs. The Russell 2,000 small-cap ETF (IWM) fell 1.95% on the week, putting it down 3% for the quarter already. Even still, IWM is up 6.93% year-to-date, which is more than 200 basis points better than the S&P 500’s (SPY) change.

You can view the recent performance of all asset classes in our key ETF matrix below.

We analyze this week’s action, the Fed, economic indicators, sentiment and more in this week’s Bespoke Report newsletter. You can read the entire report by starting a 14-day free trial to our paid content.

Have a great weekend!

The Closer 10/14/16 – End of Week Charts

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model.

The Closer is one of our most popular reports, and you can sign up for a trial below to see it and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!

Bespoke Weekly Chart Book – 10/14/16

ETF Trends: International – 10/14/16

Natural gas has lost out to coffee as the top performer of the past week. Mortgage-related stocks, Mexico, Brazil, and Utilities have also taken off. On the losing side of the equation, XBI and IBB were the worst performers on the weak with Metals, Semis, a number of country ETFs, and Pharma also underperforming.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Dynamic Upgrades/Downgrades: 10/14/16

The Closer 10/13/16 – Crude Read On Prices

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we summarize today’s EIA report on the US petroleum market. We also take a look at the solid rebound in import prices.

The Closer is one of our most popular reports, and you can sign up for a trial below to see it and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!

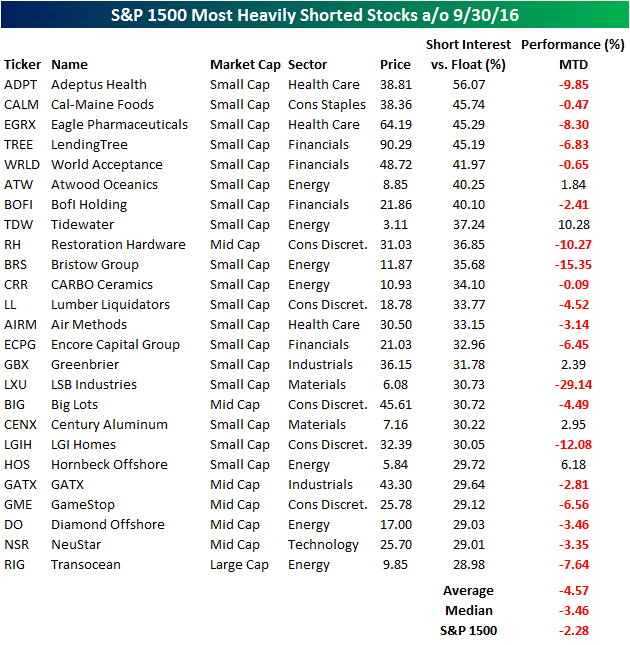

“Uncle!” S&P 1500 Most Heavily Shorted Stocks

Short interest figures for the end of September were released after the close on Tuesday, and while overall levels of short interest remain relatively low by historical standards, a number of stocks are still heavily shorted. Within the S&P 1500, 38 stocks have more than one-quarter of their free-floating shares sold short, and below we list the 25 most heavily shorted names. For each stock listed, we have also included their performance so far in October. Looking at the list, one trend remains clear; the shorts are killing it this month. Of the 25 stocks listed, just five are up in October, while the remaining 20 are down. Overall, the 25 stocks listed are down an average of 4.57% (median: 3.46%), which is more than twice the decline of the S&P 1500 as a whole. Four of the stocks are down over 10%, including former hedge fund darling Restoration Hardware (RH). While the stock was in the triple-digits last year at this time, today it’s barely hanging on to $30.

Underperformance of heavily shorted stocks typically indicates a risk-off market. However, when these stocks start to show signs of outperformance, it usually indicates that a rally is at hand, so watch these stocks closely. Better yet, sign up for a free trial below and let us do it for you!

Bespoke’s Sector Snapshot — 10/13/16

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a 14-day trial to Bespoke Premium now.

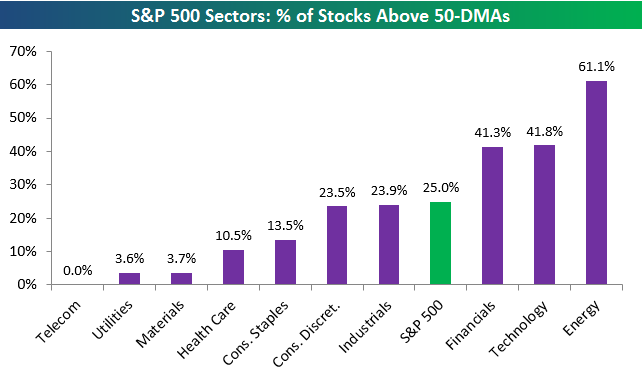

Below is one of the many charts included in this week’s Sector Snapshot, which shows the percentage of stocks in each sector trading above their 50-day moving averages. As shown, just 25% of stocks in the S&P are currently above their 50-days, which is a weak breadth reading. The only sector with a reading above 50% is Energy, while Telecom, Utilities, and Materials all have readings below 10%.

To see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a 14-day free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

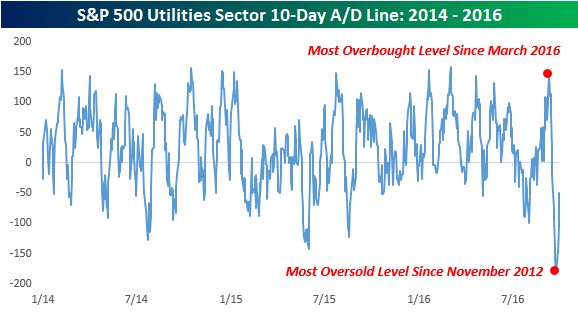

Utilities Go Haywire

When it comes to different sectors of the market, it doesn’t get more ‘boring’ than Utilities. In fact, the sector is known for its lack of action, which is one reason why investors in the sector like it so much. You simply aren’t going to wake up one morning and see stocks in the sector up or down 5% on no news. In the last couple of weeks, though, the sector’s volatility has been increasing as sentiment on the sector has gone from extremely positive to downright apocalyptic. The chart below shows the 10-day advance/decline (a/d) line of the S&P 500 Utilities sector going back to the start of 2014. If you aren’t familiar with the 10-day A/D line, it is simply a breadth measure that adds up the daily number of advancing issues minus the daily number of declining issues on a rolling ten trading day basis.

Just over two weeks ago, on 9/23, the sector’s 10-day A/D line rose to its highest level since March. As if a light switch suddenly went on, though, the next ten trading days saw extremely negative breadth as the 10-day A/D line cratered to its most oversold level since November 2012 and one of the most oversold readings for the sector on record. Given their relatively high dividend yields, utility stocks tend to be interest rate sensitive, so when interest rates rise, stocks in the sector decline. While interest rates did rise during this period where sentiment shifted, they didn’t go up by that much. We can only imagine how rough things for the sector could get if rates really started to rise.

Our weekly Sector Snapshot report provides detailed charts of important trends and indicators for the ten major S&P 500 sectors. For each sector we provide the following charts: overbought/oversold level, 10-day advance/decline line, % of stocks above 50-day moving average, P/E ratio, and relative strength vs. the S&P 500. Along with the charts, we also provide insightful commentary on current market trends so that subscribers can stay on top of our views.

The Sector Snapshot report is published on a weekly basis every Thursday after the close. The report is available to Bespoke Premium and Bespoke Institutional members. Sign up for a free-trial below.