Dynamic Upgrades/Downgrades: 10/18/16

CPI Ticking Higher

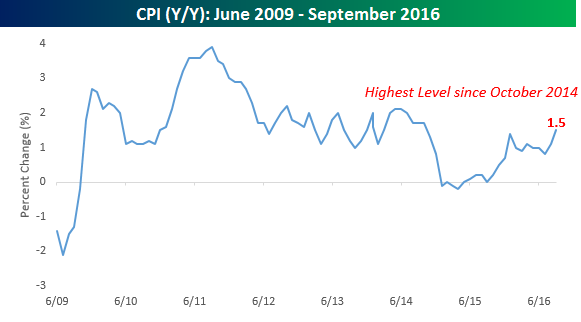

Today’s CPI for the month of September came in mixed relative to expectations as the headline m/m change was inline with expectations (0.3%), while the core print was light (0.1% vs 0.2%). On a y/y basis, inflation (as measured by the CPI) is running at 1.5% on the headline and 2.2% on a core basis. Looking at the chart below, September’s headline y/y print was the highest monthly reading since October 2014 and is beginning to show signs of an established trend higher.

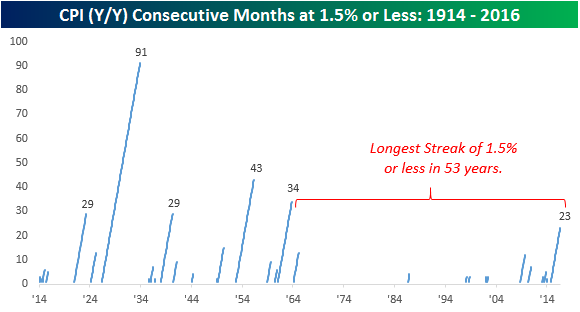

While inflation may be trending higher, remember that it remains in what has been an extraordinarily low range. The chart below shows prior streaks where the headline y/y print was at or below 1.5%. At 23 months and counting, the current streak is the longest since 1963 and the sixth longest in the last 100 years. When economists mention the fact that the FOMC would probably tolerate inflation running hot for a period of time before becoming overly concerned, one reason is that over the last two years, it has been exceptionally cold.

The Closer 10/17/16 – Sub-Industrial Production

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we summarize today’s Industrial Production report from the Federal Reserve, and take a look at how 124 different sub-industries within the S&P 500 have performed YTD.

The Closer is one of our most popular reports, and you can sign up for a trial below to see it and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!

ETF Trends: Fixed Income, Currencies, and Commodities – 10/17/16

Biotechs continue to slide, as does South Africa where confidence in the current government continues to slide. Interestingly, DBV is one of the best performing ETFs we track over the past five days. The ETF takes long and short positions in FX futures based on interest rate differentials, and typically doesn’t have much volatility. The USD has also performed well, while Utilities have outperformed despite mixed returns in the bond market recently.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Chart of the Day: Two Infrastructure Plays Look Bullish

Bespoke Briefs — Federal Reserve Policy — October 2016

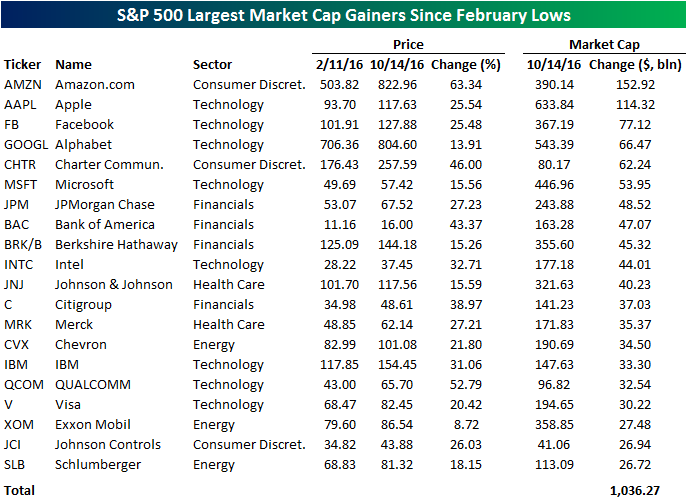

Biggest Market Cap Gainers Since February Lows

An article on Amazon.com (AMZN) in Barron’s this weekend had a really eye-popping statistic in it, and that was that since its low earlier this year, AMZN’s stock is up over 70%. A 70% gain in eight months is impressive enough, but when you take the market cap of the company into account, Amazon.com has increased its market cap by more than $150,000,000,000; that’s billion with a b! The table below lists the 20 companies in the S&P 500 that have seen the largest increase in their market cap since the S&P 500’s closing low for the year on 2/11. As shown, AMZN tops the list with a 63% rally in the stock and a $153 billion increase in its market cap. In addition to AMZN, Apple (AAPL) is the only other stock in the S&P 500 that has seen its market cap increase by more than $100 billion. Looking at the list, a lot of the names should come as no surprise given their already large market caps. There’s also a heavy presence of Technology stocks on the list (8) who have benefited from the strength of that sector. In total, these 20 stocks have accounted for an increase of $1.04 trillion in market cap, or 38% of the total $2.7 trillion increase in market cap for the entire index since the February lows.

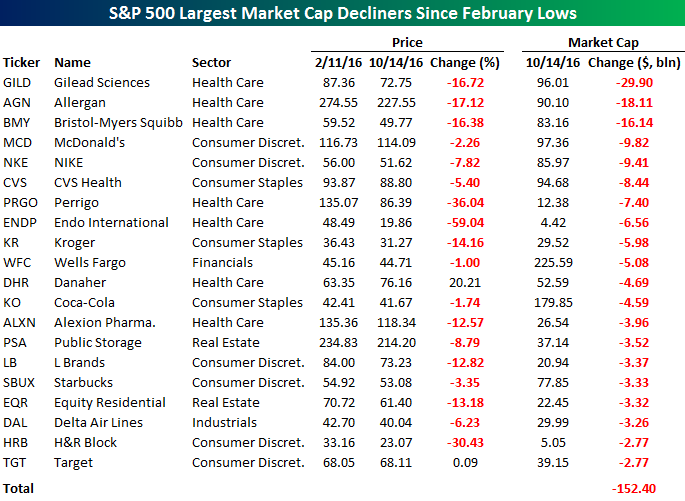

While Technology has accounted for a large portion of the gains in market cap off the February lows, Health Care has been a drag. In the table of the 20 biggest losers in market cap since February, seven are from the Health Care sector, including each of the top three. Topping the list of losers, Gilead (GILD) has seen its market cap shrink by $30 billion since February. Here, though, we would point out that not all of the decline in GILD’s market cap is due to share price declines. Yes, the stock is down, but the company has also repurchased a good chunk of stock during this period, which shrinks market cap. Along those lines, there are actually two stocks that are up during this period that have seen their market caps decline. Danaher (DHR) is actually up over 20%, but its market cap declined following the spin-off of Fortive (FTV). Likewise, Target (TGT) has seen a marginal gain since the S&P 500’s closing low in February, but its market cap has declined by nearly $3 billion.

Bespoke Stock Seasonality: 10/17/16

Dynamic Upgrades/Downgrades: 10/17/16

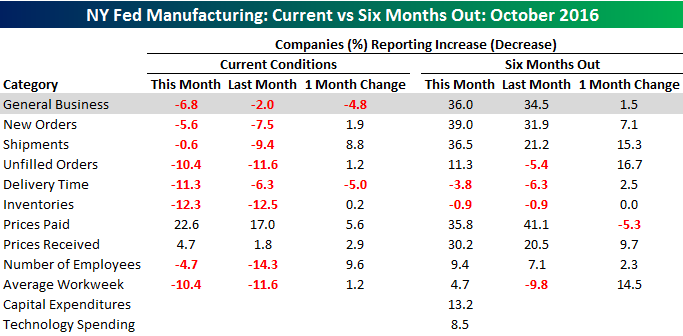

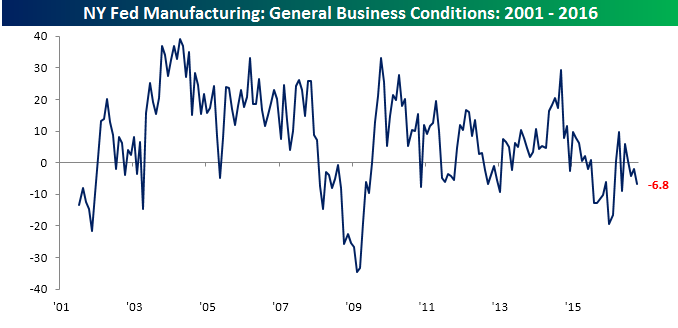

Weak Manufacturing in the New York Region

October’s report on Manufacturing in the New York region took another turn for the worse this morning. While economists were expecting the headline reading of the Empire Manufacturing report to rebound back into positive territory from last month’s reading of -2.0, the actual reading declined to -6.8. This was the third straight monthly reading below zero, the fourth straight weaker than expected reading, and the weakest overall report since May.

Not everything was bad about the October report, though. The internals of the report were actually more positive than the headline. As shown in the table below, besides the headline reading, Delivery Time was the only component of the current conditions part of the report which deteriorated in October. As far as expectations are concerned, manufacturers’ expectations for General Business conditions were more positive in October than September with Prices Paid showing the only decline. Additionally, plans for CapEx rose to their highest level since April.