Fog Lifting For Individual Investors

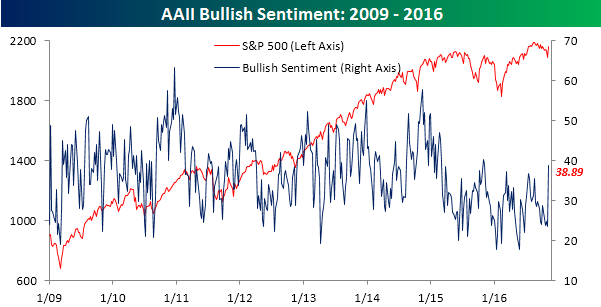

Did Donald Trump just do what record highs in the S&P 500 couldn’t? For several months now, consumer and investment sentiment has been anchored by the uncertainty regarding the election and especially over the possibility of what a Trump Presidency would mean for the markets and, more importantly, the economy. One of the best examples of this is the weekly sentiment poll from the American Association of Individual Investors (AAII). Even though the S&P 500 has essentially been at or near all-time highs for much of 2016, bullish sentiment on the part of individual investors has been stuck below 40% for a record 54 straight weeks and 88 of the last 89 weeks.

This week, AAII’s bullish sentiment reading still came in below 40%, but it has came closer to that level than any other point in the last year. According to this week’s survey, bullish sentiment increased surged from 23.64% up to 38.89%, representing the largest one-week increase since July 2010. That’s six years! To be fair, AAII’s weekly poll is conducted from Thursday through Wednesday, so the bulk of this week’s responses were more than likely tabulated prior to the election, and even prior to the Comey letter saying that nothing had changed in the FBI’s decision not to recommend indicting Clinton. That being said, in a year where the so-called establishment has been proven to be so disconnected with the views and opinions of the overall population, it is only fitting that a survey of bullish sentiment among individual investors surged the most in six years at the same time as the biggest US political upset in at least a generation, if not history. It will be really interesting to see where this reading stands next week.

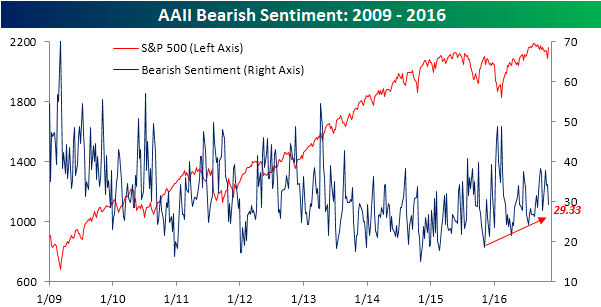

While bullish sentiment surged, bearish sentiment declined but not nearly by as much as the magnitude of bullish sentiment. It still fell below 30%, which is the lowest level in five weeks.

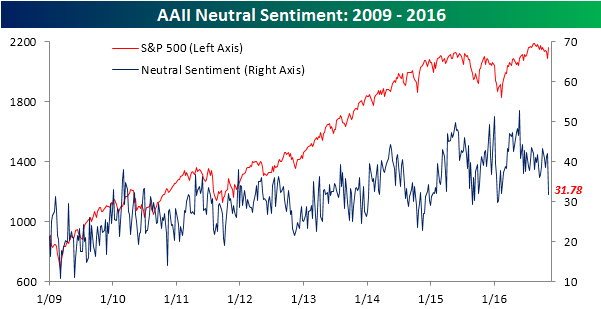

Neutral sentiment was also of note this week, and illustrated the fact that the passing of uncertainty regarding the election really impacted sentiment. In this week’s survey, neutral sentiment declined from 42.05% down to 31.78%, which is the lowest level since January.

The Closer 11/9/16 – First Day After

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke Institutional clients, we detail the current stance of global equity indices in our Global Index Screen, discuss the varied impact of the Trump election on the Health Care sector, update the quieting in volatility markets, and discuss the massive move in interest rates over the last 24 hours.

The Closer is one of our most popular reports, and you can see it and everything else Bespoke publishes by starting a no-obligation 14-day free trial to our research!

ETF Trends: Hedge – 11/9/16

In the wake of the Presidential election, anything related to commodities, the industrial cycle, banks, or Energy has exploded higher in price. Defense stocks have also done well. All an extrapolation of the likely policy path for President Trump. On the losing side of the equation, Treasuries have gotten absolutely demolished, as have solar stocks (concerns over subsidies for clean energy being cut). The Japanese yen has plunged, as has the Swedish krona and the euro.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Election Unwind

The general consensus heading into Election Day 2016 was that a Trump victory would spell doom for stocks. The nine-day losing streak experienced by the S&P 500 as Trump’s odds were rising and then two days of gains just before Election Day as his odds fell again served to reinforce then thinking. Even further, as actual vote counts that started to project a Trump victory came in on election night, Dow futures nose-dived 800 points!

So with the S&P 500 up more than a percent on the day with a little over an hour left of trading, why have the negative sentiments towards a Trump Presidency seemingly been flipped on their head so quickly? It appears that investors didn’t factor in the gains that pro-GOP sectors would experience with a Trump win and a Republican sweep in Congress. So far today, gains for stocks and sectors that stand to benefit from typical GOP positions have more than made up for any Trump fear selling.

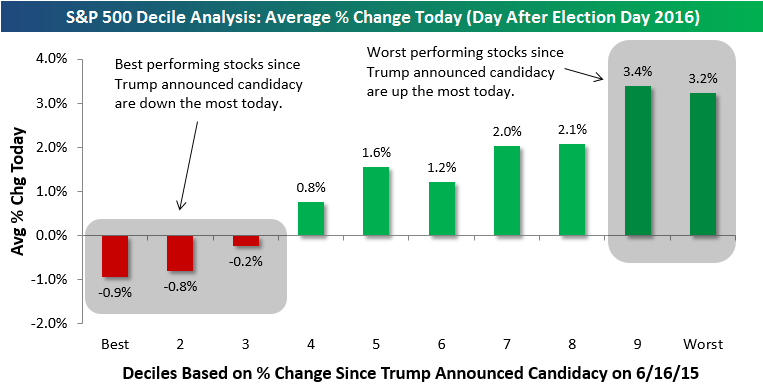

We show how it’s playing out in the chart below. We took a snapshot of the stocks that made up the S&P 500 on the day Trump announced his candidacy back on June 16th, 2015. We then calculated each stock’s price change from that date through the close yesterday and grouped them into deciles (10 groups of 50 stocks each) based on performance. We then calculated the average price change of the stocks in each group today now that Trump has been declared the winner.

As shown below, the three deciles of the best-performing stocks (top 150 stocks) from the day Trump announced through yesterday are all averaging declines today. The two deciles of the worst performing stocks (bottom 100 stocks) from the day Trump announced through yesterday are all averaging big gains. Clearly, we’re seeing a Trump/GOP reversal. Throughout the campaign, stocks were pricing in better odds for Clinton to win than Trump, and now that Trump has won, the trade is coming unwound.

Below is a look at the average performance of stocks in each sector today compared to the average performance of stocks in each sector from the time Trump announced (6/16/15) through yesterday’s close. As shown, sectors like Energy, Health Care, Materials, Financials, and Industrials are seeing their stocks rally today, while sectors like Consumer Staples, Technology, and Utilities that saw big gains from 6/16/15 through yesterday are averaging declines today.

The early trade for Trump plus an all-GOP Congress is moving money into Health Care (no price caps), Financials (Dodd Frank repeal and higher rates), Materials (infrastructure), Energy (pro-oil), and Industrials (defense, infrastructure).

Chart of the Day – “Yuuuge” Jump in Rates

Fixed Income Weekly – 11/9/16

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

This week we take a look at changes in the deficit depending on who controls the White House and Congress, with an eye towards expectations the Trump administration is likely to widen the deficit.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here to start your no-obligation free Bespoke research trial now!

Republican Sweeps

With Republicans set to take control of the Oval Office, Senate, and House come January, we wanted to provide an update and a little more detail to our B.I.G. Tips report from yesterday highlighting market performance under different political compositions in Washington. Since 1900, there have been thirteen prior sessions of Congress where the GOP had full control of the Oval Office, Senate, and House, and in today’s report, we highlight the how the DJIA performed during each of these periods as well as how sectors performed in the periods post WWII.

If you are interested in seeing our latest B.I.G. Tips report, Republican Sweeps, sign up for a monthly Bespoke Premium membership and get 10% off for life ($89/month). There is no financial obligation whatsoever, and you can cancel at any time.

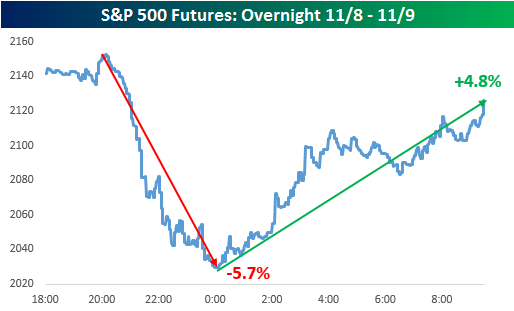

The Best Advice of All: Sleep On it

The best advice anyone could ever receive in their formative years is that whenever an important and emotional decision needs to be made, it often helps to “sleep on it.” Or at the very least, pause for a few minutes to think about the ramifications of your decision. If someone wrongs you on Twitter, the first reaction may be to fire off a nasty response, but if you stop to think about it, more often than not, your better judgment prevails and you choose to ignore the trolls rather than ratcheting things up. Just this week, Gmail introduced a new feature that allows users to retrieve embarrassing emails sent in the heat of the moment, so if you hit send and then have second thoughts, you can try and undo what you have just done.

So, what does all of this have to do with the financial markets? You can probably guess, but we’ll show you anyways. Last night, when it first became apparent that Donald Trump was staging one of the biggest political upsets in a generation at least, global financial markets went haywire, with US equity futures plummeting. After initially rallying following some positive exit poll data for Clinton, things turned south as results in Florida suggested a win in that state for Donald Trump. As shown in the chart below, at one point just after midnight when it became clear that Trump would win the election and news anchors were gasping and some outright getting choked up, S&P 500 futures were down close to 6% from their earlier highs.

With that in mind, someone listening to the news and staring at their screens last night seeing a market down more than 5% may have been tempted to act brashly and sell. It may have felt good at the time, but if you decided to sleep on it for a few hours, you would be looking at a whole different picture this morning, when the futures and then cash trading erased nearly all of their declines. You would have also probably come to the realization that while the President is still the most powerful person in the world, no one person is bigger than nor has the power to control the US economy or the stock market. So even if you think Trump’s policies are bad for the economy (which half of America obviously didn’t believe), the US government still has a number of checks and balances in place to counter any possibility of destructive policies, even if one party controls the Oval Office, Senate, and House. The action overnight also reminds us of another piece of advice we have heard over time – nothing ever good happens in after-hours trading.

The Closer 11/8/16 – Short Update Before An Evening Of Vote Counting

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke Institutional clients, we update our tracking of the Fed’s Senior Loan Officers’ Survey. We also discuss consumer credit growth for the month of September, and discuss volatility markets ahead of election day.

The Closer is one of our most popular reports, and you can see it and everything else Bespoke publishes by starting a no-obligation 14-day free trial to our research!