B.I.G. Tips – April 2017 Seasonality

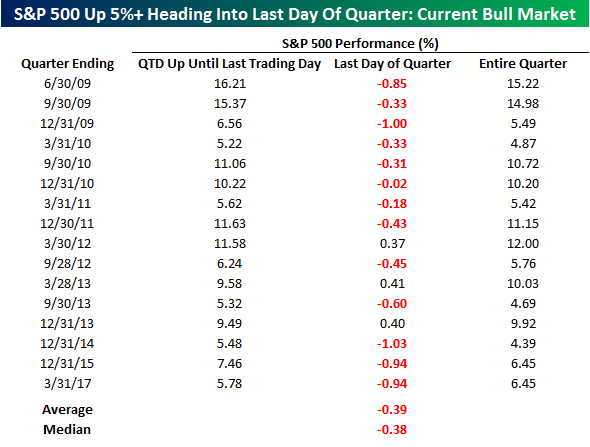

Up 5% Heading into Quarter End

With a gain of 5.78% so far in the quarter and just one trading day left in it, the S&P 500 is on pace for a pretty solid Q1. Given the gains we have seen, it’s ironic that all quarter long investors have been bombarded on a near daily basis with headlines proclaiming an end to the rally. A 5%+ gain is a 5% gain. Looking ahead to the final day of the quarter, we wondered how the market tends to close out the quarter following a strong run. Do investors keep buying or do they take profits?

To shed some light on that question, we looked at every quarter during the current bull market where the S&P 500 was up 5% or more heading into the last trading day to see how the S&P performed on the final day. Even though we only looked at the current bull market, we found plenty of quarters that met the criteria. During the 32 quarters so far in this bull market, the S&P 500 was up over 5% QTD heading into the last day of the quarter half of the time (16 quarters). Looking at the results, there’s a pretty convincing case to be made that traders don’t continue piling into the market. Of the fifteen prior quarters we looked at, the S&P 500 was down on the final trading day of the quarter 12 times for an average decline of 0.39%. Perhaps it’s due to investors re-balancing out of some of their winning asset classes and into losing asset classes, but during the current bull market at least, there hasn’t been a lot of buying to be found on the last day of a quarter where the S&P 500 was already up 5%.

The Closer — Productivity Puzzling — 3/30/17

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke Institutional clients, we update charts on multifactor productivity using BLS data updated today. We also discuss the low investment problem those charts reveal and take a look at some EM currency charts.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

The Closer is one of our most popular reports, and you can see it and everything else Bespoke publishes by starting a no-obligation 14-day free trial to our research!

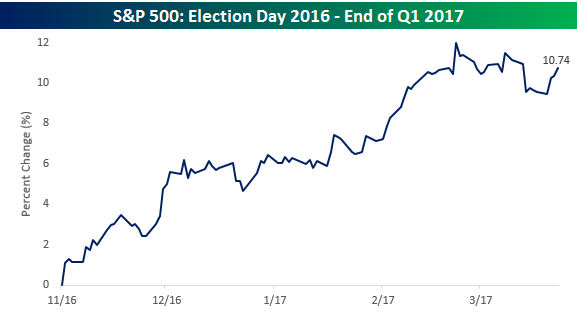

Guess The Chart: Election Edition

With Q1 winding down in the next two days, we thought it would be a good time to review the performance of the S&P 500 since Donald Trump was elected last November and play a quick game of “Guess the Chart.” As shown in the chart below, the S&P 500 rallied hard following the election, traded sideways for several weeks, and then rallied into early March before backing off the rest of the month. Even after the pullback, though, the S&P 500 is still up just under 11% and not far from its bull market highs.

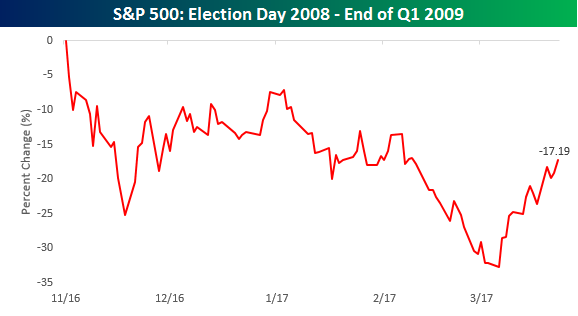

The next chart also shows performance from Election Day through the end of Q1. This mystery chart has seen a similar but much more volatile pattern than the one of the S&P 500 above. Like the S&P 500, it rallied following the election, traded sideways for several weeks, and then spiked higher into early March before backing off its highs towards the end of March. Can you guess the chart?

Give up yet? The “Mystery Chart” above isn’t from Election Day 2016 through now, but instead from Election Day 2008 through the end of Q1 2009. We also forgot to mention that it is upside down. Can you guess it now? It’s actually the inverse of the S&P 500. It’s not a surprise that the market has seen such different reactions between late 2008/early 2009 and now. Circumstances couldn’t have been more different on just about every measure, but if you are a bull, going forward you have to hope that the differences in performance end here. Below is the real (non-inverse) version of the S&P from Election Day 2008 through Q1 2009.

Bespoke’s Sector Snapshot — 3/30/17

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a 14-day trial to Bespoke Premium now.

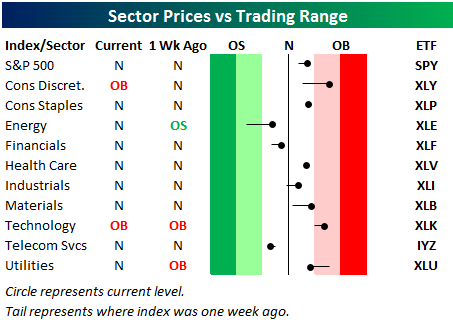

Below is one of the many charts included in this week’s Sector Snapshot, which highlights our trading range screen for the S&P 500 and ten sectors. The black vertical “N” line represents each sector’s 50-day moving average, and as shown, three sectors — Energy, Financials, and Telecom — are currently below their 50-days. Only two sectors — Consumer Discretionary and Technology — remain overbought. (The red zone is considered overbought territory, while the green zone is considered oversold territory.)

To see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a 14-day free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

Chart of the Day: Rupee Ripping

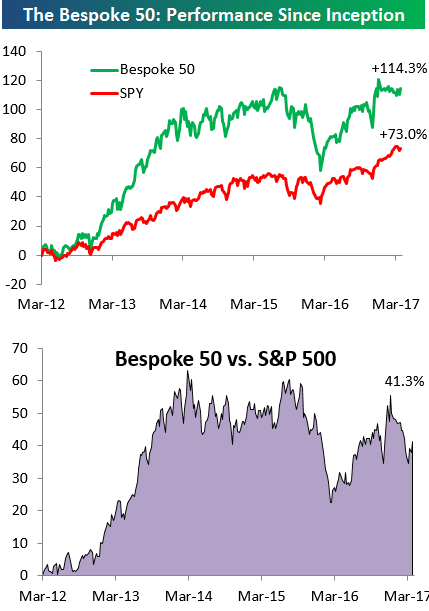

the Bespoke 50 — 3/30/17

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 41 percentage points. Through today, the “Bespoke 50” is up 114.3% since inception versus the S&P 500’s gain of 73.0%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, sign up for Bespoke Premium ($99/month) at this checkout page and get your first month free. This is a great deal!

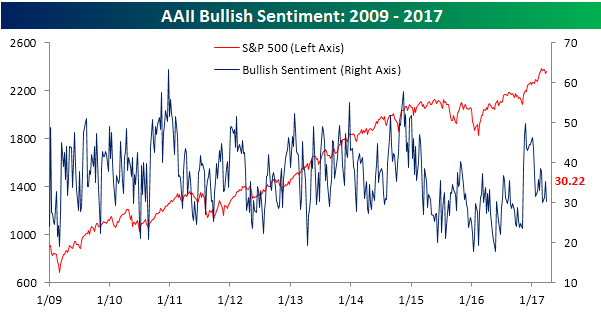

Individual Investors Turn Sour Again

After two straight weeks where individual investor sentiment saw some improvement, this week’s survey from AAII showed that individual investors returned to their bearish ways. In last week’s survey, bullish sentiment reached as high as 35.28% (which is still low by historical norms), but this week nearly all of the last two weeks of improved sentiment was erased as bullish sentiment barely held on to 30%, falling just over five percentage points to 30.22%. For those keeping score at home, it has now been 117 weeks since more than half of individual investors were in the bullish camp.

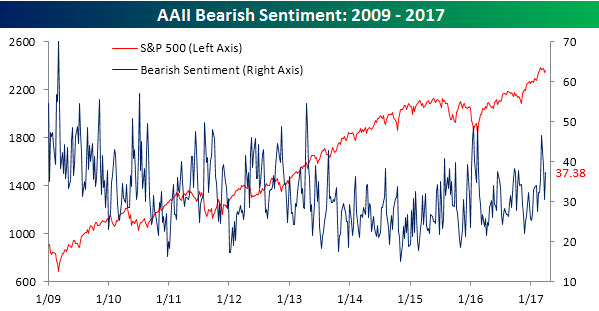

On the other side of the ledger, bearish sentiment ticked higher this week, rising from 30.5% up to 37.4%. In the last two weeks, we had seen some moderating in the bearish tone of individual investors, but it looks like they are getting right back to their bearish ways.

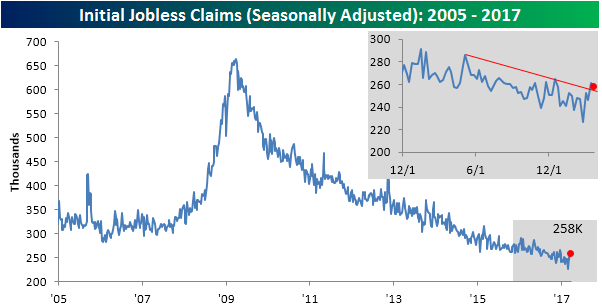

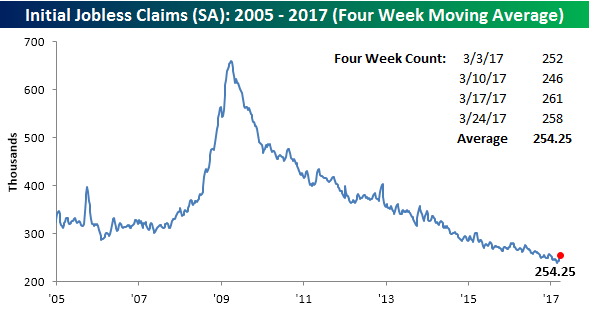

Another Disappointing Jobless Claims Report

When it comes to economic indicators, it used to be that weekly jobless claims were one of the most reliable to deliver a positive report. In recent weeks, though, that hasn’t been the case as claims have come in higher than expected in each of the last four weeks. In this week’s report, economists were expecting the headline reading to come in at a level of 247K from last week’s reading of 261K, but the actual decline was smaller at just 3K to 258K. The last time jobless claims have been higher than expected four weeks in a row was back in January of last year, and to find the last time claims exceeded forecasts for five straight weeks, you have to go all the way back to November 2013. Despite the weaker than expected readings, however, we would still note that claims remain very low, coming in below 300K for the last 108 weeks.

The four-week moving average also saw quite an increase this week, rising from 246.5K up to 254.25K. That 7.75K increase is the largest one-week jump in the four-week moving average since February 2015.

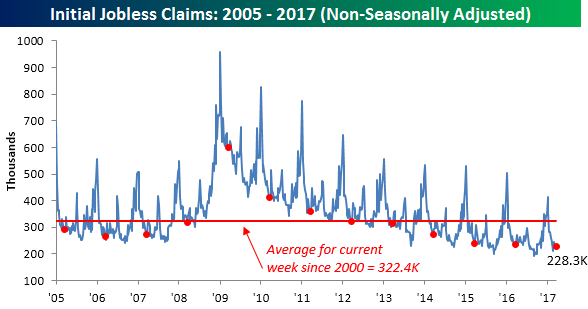

On a non-seasonally adjusted basis, jobless claims still remain encouraging. This week’s print came in at 228.3K, which was the lowest level for the current week of the year since 1973 and 94K below the average level of 322.4K for the current week of the year dating back to 2000.

The Closer — Negative NIIP — 3/29/17

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke Institutional clients, we dive into the quarterly net international investment position data from the BEA. We also take a look at oil inventory data and S&P 500 Energy valuation.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

The Closer is one of our most popular reports, and you can see it and everything else Bespoke publishes by starting a no-obligation 14-day free trial to our research!