Traders Betting on “Death By Amazon” in the Retail Space

Earlier today, we published an update to our “Death By Amazon” index of stocks, which tracks the performance of stocks in companies whose sales are the most Amazon-able. In the update, we mentioned how the “Death By Amazon” index just recently made a four-year low. On a related note, short interest figures for the end of March were released earlier this week, and looking at the data, Death By Amazon is a trade that hasn’t gone on unnoticed.

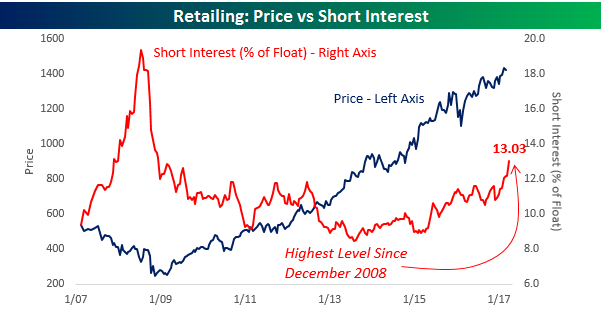

The chart below compares the price of the S&P 1500 Retailing Group and the average short interest as a percentage of float (SIPF) for stocks in the group going back to 2007. For the last several months now, average short interest levels have been rising steadily for the group and currently stand at over 13%, which is the highest reading for the group since December 2008. Not since the depths of the financial crisis have traders been more negative on the group, although we would note that they were a lot more negative back then compared to now. One thing to note in this chart is that even though it looks as though the Retailing Group has performed well over the last few years, practically all of the gains in the sector are the result of Amazon.com (AMZN), Home Depot (HD), and Priceline.com (PCLN). Outside of these three stocks, the vast majority of the group’s members have been trending the other way.

In terms of individual stocks, the table below shows the sixteen stocks in the group that have more than 20% of their float sold short. Looking at the list, all but three stocks are down so far this year. Ironically, the stock with the highest short interest, RH (formerly Restoration Hardware), is up sharply YTD. That’s more of a special situation, though, as RH is coming off hard times from prior years and is still down more than 50% from its highs in late 2015. Lumber Liquidators (LL) is another example. Although it is up 37% this year, it’s trading at a fifth of its level from late 2013. For just about every other stock shown, 2017 has already been a year to forget, especially when you consider the fact that the broader market is up about 5% on the year.

While the outlook for many of the names in the retail space is bleak, there will undoubtedly be some companies that buck the trend and turn things around. In our earlier update to the Death By Amazon index, we actually highlighted one of the names in the list below as a turnaround candidate. So if you haven’t already, sign up for a free trial and check out the report!

the Bespoke 50 — 4/13/17

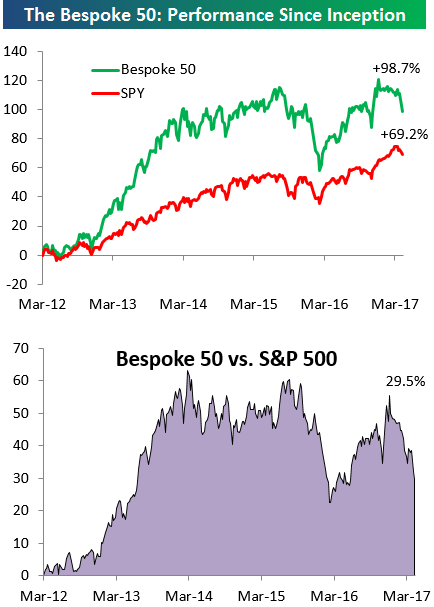

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 30 percentage points. Through today, the “Bespoke 50” is up 98.7% since inception versus the S&P 500’s gain of 69.2%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, sign up for Bespoke Premium ($99/month) at this checkout page and get your first month free. This is a great deal!

Bespoke’s “Death By Amazon” Index Makes 4-Year Low

Bespoke created its “Death By Amazon” index back in 2014 as a way to track the retail companies most affected by the rise of Amazon. Companies included must be direct retailers with a limited online presence (or core business based on physical retailing locations), a member of either the Retail Industry of the S&P 1500 or the S&P Retail Select index, and rely primarily on third party brands. We view these attributes as the best expression of AMZN’s threat to traditional retail.

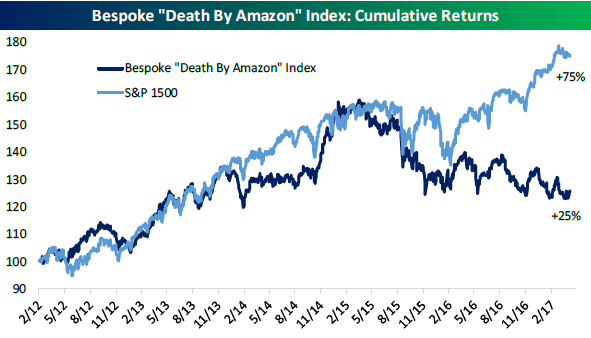

Below is a look at the performance of Bespoke’s “Death By Amazon” index versus the S&P 1500 since the start of 2012. As shown, the index has underperformed the market significantly over this 5-year period. The DBA is up 25% versus the S&P 1500’s gain of 75%. And how has Amazon.com (AMZN) performed since early 2012? It’s up more than 300%.

Each month we provide an update of our “Death By Amazon” index along with a look at the performance of the index’s individual members. In this month’s report, we also feature one long idea from the department store group and one short idea from the “off-price” retailer group.

To see this month’s Death By Amazon report, sign up for a 14-day free trial to our Bespoke Premium research service.

Post-Election Winners Down the Most

The average stock in the S&P 1500 (contains large, mid, and small caps) is down 3.35% since the index peaked on March 1st. We broke the S&P 1500 into deciles (10 groups of 150 stocks each) based on stock performance from election day 2016 (11/8/16) through the March 1st equity market peak to see how the biggest post-election winners and losers have been doing during the current pullback. As shown, the decile of stocks that did the best during the post-election rally from 11/8/16 through 3/1/17 are down an average of 8.45%. Clearly investors have been selling the biggest “Trump Trade” winners since the beginning of March.

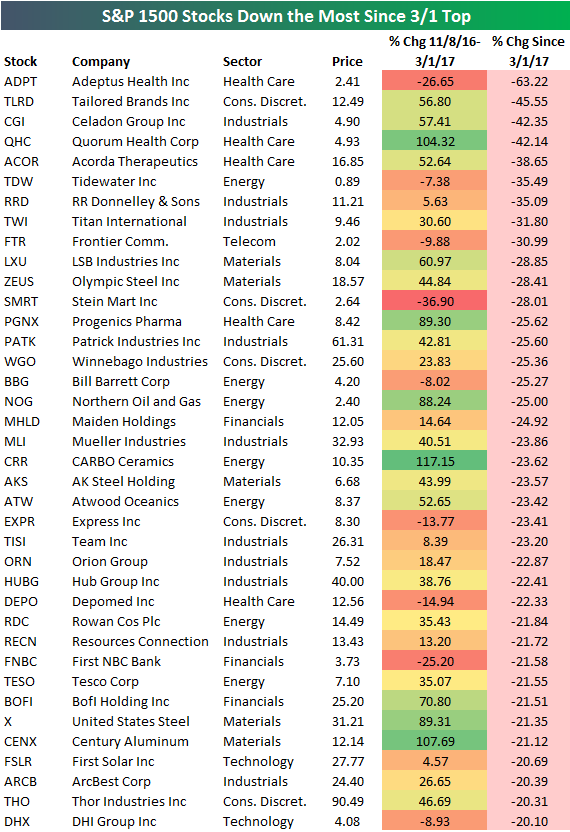

Below is a list of the worst performing stocks in the S&P 1500 since the March 1st equity market peak. All of the names listed are down 20%+. Notables include Frontier Communication (FTR), AK Steel (AKS), Winnebago (WGO), US Steel (X), and First Solar (FSLR). It’s been just a brutal few weeks for these names.

Bespoke Short Interest Report: 4/13/17

Chart of the Day: Heavy Metal Technicals

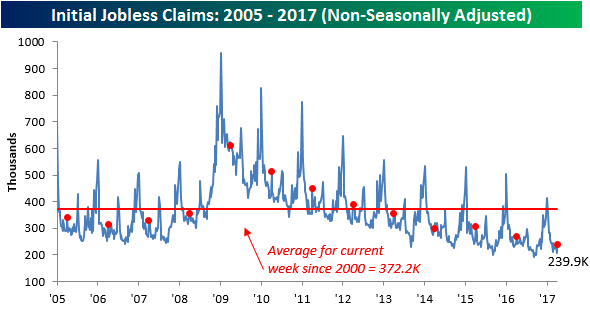

Jobless Claims Back Down Near Cycle Lows

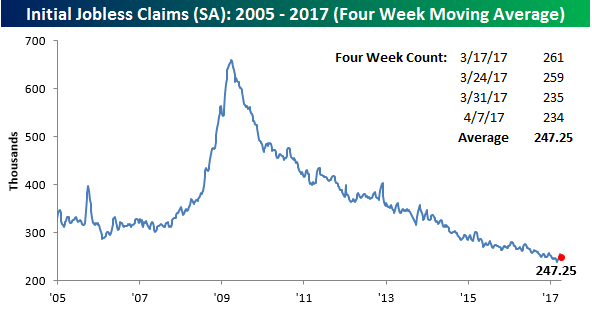

Remember back a couple of weeks ago when weekly jobless claims “spiked” up above 250K for two weeks? After those two weeks of elevated readings back in mid-March, jobless claims have dropped back down near their cycle lows. In this week’s report, claims came in at 234K, which was down 1K from last week’s revised reading and 11K below consensus estimates. Claims have now been below 300K for 110 straight weeks, and any concerns that the labor force was weakening following those two relatively elevated prints last month should be alleviated as it looks increasingly likely that they were more weather related than anything else.

With this week’s decline, the four-week moving average has now dropped 3K down to 247.25K. That puts this reading back within 10K of the cycle low of 239.75K that we saw seven weeks ago.

On a non-seasonally adjusted basis, claims were equally as strong. With a print of 239.9K, NSA claims were more than 130K below their historical average of 372.2K for the current week of the year going back to 2000. It is also the lowest print for the current week of the year dating back to 1969.

The Closer — Double Tops, Oil Data, Eurodollar Shorts — 4/12/17

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke Institutional clients, we chart out some possible double tops in global equity indices, summarize weekly EIA petroleum market data, and analyze positioning in the Eurodollar futures market.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

The Closer is one of our most popular reports, and you can see it and everything else Bespoke publishes by starting a no-obligation 14-day free trial to our research!

B.I.G. Tips – S&P 500 50-DMA Finally Broken

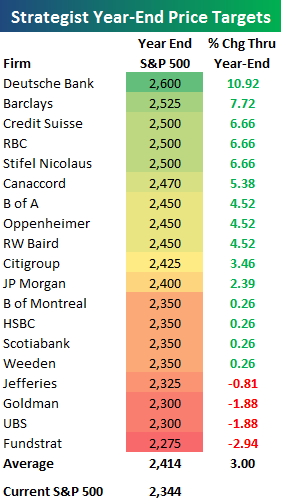

Wall Street Strategists Not Enthusiastic From Here

At the end of 2016, we published this post on year-end price targets for Wall Street strategists. For 2017, the average strategist projected the S&P 500 to post a gain of 5.5%. That’s actually bearish relative to the average annual projection going back to 2000. As shown below, on average, Wall Street strategists collectively project a gain of 9.6% each year. In 2016, strategists predicted the S&P would gain 8.4%, which ended up being just 1.1 percentage points away from the actual gain of 9.5% seen last year. That was the closest they’ve ever gotten to hitting the mark. Normally, they’re about 5.5 percentage points above the actual year-end change.

Bloomberg tabulates these year-end estimates from strategists throughout the year. As mentioned above, at the start of 2017, the average year-end price target for the S&P 500 was 2,362. That would have translated into a gain of 5.5% based on where the index began the year. So where do strategists stand now that we’re already into the second quarter? They’ve gotten slightly more bullish, but they’re still looking for hardly any gains. As shown below, the average Wall Street strategist currently sees the S&P 500 ending 2017 at a level of 2,414. That’s an additional gain of 3% from the S&P’s current level. Normally a sanguine bunch, strategists are currently rather apathetic.