Brunch Reads – 3/8/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

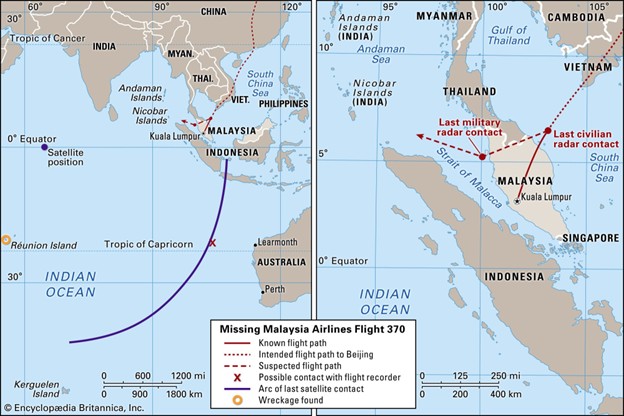

Malaysian Mystery: In the early hours of March 8, 2014, Malaysia Airlines Flight 370 departed Kuala Lumpur for Beijing with 239 people on board. Less than an hour into the flight, the Boeing 777 vanished from radar. Military radar later revealed that the plane had unexpectedly turned back across the Malay Peninsula and continued flying west before vanishing again. Satellite communication data later showed the aircraft continued transmitting automated signals for several hours, indicating it flew far off course along a remote arc over the southern Indian Ocean until it likely ran out of fuel.

The disappearance triggered the largest aviation search effort in history, involving more than two dozen countries and the scanning of roughly 120,000 square kilometers of ocean floor. Early search operations focused on the South China Sea before satellite analysis moved the search thousands of miles southwest into one of the most remote stretches of ocean on Earth. Despite years of underwater searches using advanced sonar equipment and deep-sea drones, the aircraft’s main wreckage has never been found.

Investigators explored numerous explanations for the disappearance, including mechanical failure, onboard fire, hijacking, or deliberate action by someone in the cockpit. Evidence that the aircraft’s communication systems were manually disabled and that it executed a controlled course change led many investigators to conclude the diversion was likely intentional, though the official investigation could not determine who was responsible or why. In 2015, a confirmed piece of MH370 debris, a wing component known as a flaperon, washed ashore on Réunion Island in the Indian Ocean, with additional fragments later discovered along the coasts of Africa and nearby islands. These findings strongly support the conclusion that the aircraft ultimately crashed into the southern Indian Ocean after flying for hours on autopilot. More than a decade later, the disappearance of MH370 remains one of aviation’s greatest mysteries.

AI & Technology

Jack Dorsey Blamed AI for Block’s Massive Layoffs. Skeptics Aren’t Buying It. (WSJ)

Block held a $60 million company celebration in California just months before announcing plans to cut roughly 40% of its workforce, with CEO Jack Dorsey pointing to rapid advances in artificial intelligence as a key reason for the restructuring. Some analysts and former employees argue the layoffs reflect years of overhiring and sprawling expansion into new ventures rather than an immediate AI-driven change in how the company operates. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

The Bespoke Report – Iran War

This Week’s Bespoke Report: Oil’s Record Week, Software’s Comeback, and the Iran Fallout

It was one of the wildest weeks in recent market history. Here’s a look at what we’re covering in this week’s Bespoke Report.

Oil Just Had Its Biggest Week Ever

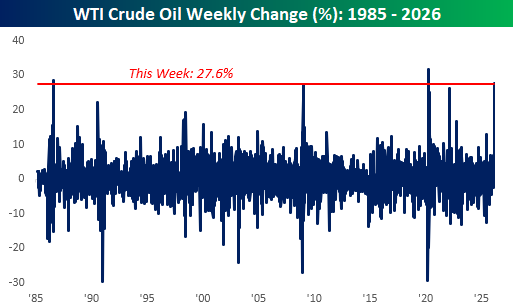

Crude oil surged 36% this week, the largest weekly gain since at least 1985, after US/Israeli strikes on Iran effectively shut down tanker traffic through the Strait of Hormuz. By Friday afternoon, oil was trading above $91/barrel at its most overbought level in history. In the report, we look at what has historically happened to both oil and equities after spikes like this, and how quickly the pain is likely to show up at the gas pump.

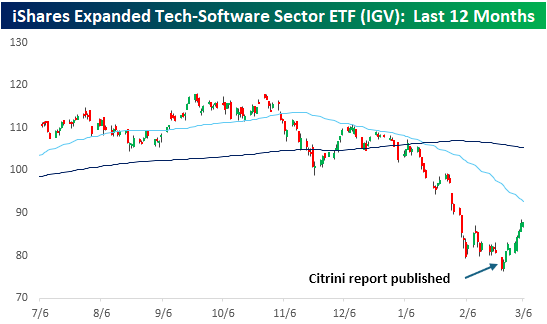

Software Bounces Back

After falling more than 22% in the first two months of 2026, the iShares Expanded Tech-Software ETF (IGV) has rallied nearly 14% in just nine trading days with remarkably steady intraday buying pressure. The Citrini essay that terrified the sector on 2/22 may have marked the clearing-out event. It’s always easier to see in hindsight, but underneath all the snow on 2/23, there was plenty of blood on the software streets. We chart the bounce and put the current streak in historical context.

A Historic Reversal in Positioning

The Iran conflict triggered what looks like a broad deleveraging across institutional portfolios. Everything that worked in January and February stopped working this week, and everything that didn’t work started working. International equities that had been trouncing the US for months got hit the hardest, while the most beaten-down US stocks rallied sharply. We break down the reversal by asset class, country, and individual stock, and we explain why the US held up better than the rest of the world.

The Three-Headed Monster Awakens

Oil, Treasury yields, and the dollar. Our “three-headed monster” indicator just surged to its highest combined level in nearly a year. Two weeks ago, the monster was still asleep. We show where current readings sit relative to 40 years of history and what it has meant for forward equity returns.

Payrolls Go Negative

Friday’s jobs report showed a loss of 92,000 nonfarm payrolls, badly missing the +55K estimate. But the headline number is misleading. A big chunk of the weakness came from a single line item that will almost certainly reverse. We walk through what’s really going on beneath the surface, including what the data says about AI’s impact on younger workers.

The S&P 500 Keeps Bouncing

The S&P 500 opened down 1% or more on three separate days this week and managed to claw back each time. That’s only happened 13 times in SPY’s history since 1993. We look at where those prior weeks fell on the chart and what happened next.

That’s just a recap of some of the topics covered in this week’s Bespoke Report, our flagship weekly newsletter. This week’s edition is 29 pages of charts, tables, and in-depth analysis. If you’d like to dive in further, you can start a Bespoke trial to read the full report and get access to all of our daily research.

Daily Sector Snapshot — 3/6/26

The Triple Play Report: 3/5/26

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report covers what each company does, what this quarter’s results say about their growth outlooks, and their histories of delivering triple plays. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read today’s Triple Play Report. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

“Software is Dead, Long Live Software”

The first two months of the year were a year to forget for the software sector. In just two months, the iShares Expanded Tech-Software Sector ETF (IGV) fell more than 22%, taking its total decline from its peak to over 30%. In the early weeks of 2026, it seemed as though every weekend a new negative article about the sector was published, allowing nervous investors to worry all weekend about the death of software stocks at the hands of AI.

The most notable of these reports, so far, was the Citrini essay titled “The 2028 Global Intelligence Crisis”. Published on 2/22, it also coincided with a weekend blizzard in the northeast. When the markets opened for trading the following Monday on 2/23, the magnitude of the decline was likely exaggerated given the lower market liquidity. Looking back at that report, though, in the short-term at least, its publication appears to have been a clearing-out event for the market, as IGV has rallied 13.9% since the close on 2/23.

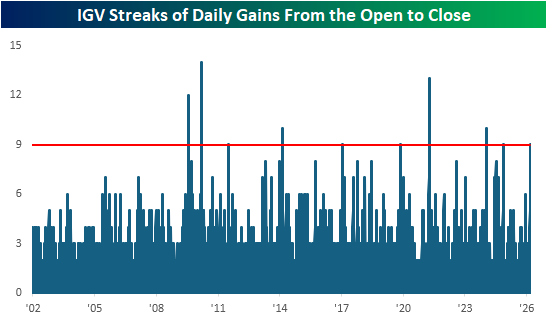

Over the course of that 13% rally, IGV has traded higher in eight of the last nine trading days, including today’s fractional gain as of midday. Not only has IGV traded consistently higher, but there has also been steady buying throughout the trading day. In each of those nine days, even on the one day it traded lower, IGV traded higher from the open to close. While there have been five other streaks where IGV had more consecutive days of gains from the open to close, the current streak is tied with four other periods for the sixth-longest streak in the ETF’s history. It’s always easier to see in hindsight, but underneath all the snow on 2/23, there was plenty of blood on the software streets.

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up:

Bespoke’s Morning Lineup – 3/6/26 – Boiling a Frog

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I never worry about the problem. I worry about the solution.” – Shaquille O’Neal

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Did you know that there’s an employment report today? With geo-politics in the forefront, economic data has largely taken a back seat this week, but the data will keep coming (unless there’s a shutdown, of course!), and heading into this morning’s report, the S&P 500 and Nasdaq are indicated to open down by between 0.75% and 1.0%, continuing a week of lousy market action. Treasury yields are higher, crude oil is surging, and gold is fractionally higher.

In Asia, most major indices were flat to lower, but still finished the week sharply lower, with the Nikkei down 5.5%, China down 2.1%, and South Korea down more than 10%. In Europe, the losses are even larger, with the STOXX 600 down over 1%, taking its decline for the week to over 5%. Across the continent, every major benchmark is down over 5% this week.

Besides the Employment report, Retail Sales also hit the tape at 8:30. The employment report was a disappointment across the board as Non Farm Payrolls fell 92K versus forecasts for an increase of 55K, and the Unemployment Rate increased to 4.4% versus forecasts for 4.3%. Average hourly earnings were slightly higher than expected, rising 0.4% versus forecasts for an increase of 0.3%. As bad as that report was, it will be interesting to see if there were any weather-related impacts. While the jobs picture was weaker, Retail Sales came in better than expected.

When markets opened for trading on Monday, and crude oil prices rallied a bit over 5%, it was viewed as a surprisingly muted reaction to a monumental event in the Middle East. It looked like we got off easy. As the days have gone on and the conflict has continued, crude oil prices rose every day this week with a 4.7% gain on Tuesday, a 0.1% gain on Wednesday, an 8.5% gain on Thursday, and what’s shaping up to be a 6.5% gain today. The frogs in the market pot had no idea what was coming.

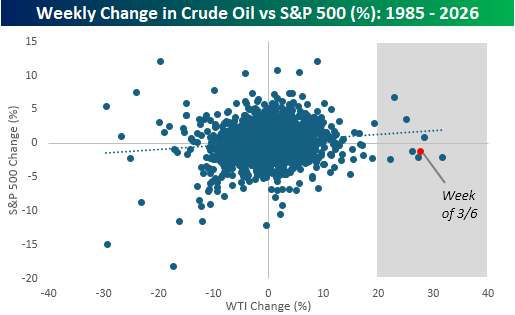

Adding them all together, WTI is on pace for a 27.6% gain this week, which would rank as the third-largest weekly gain since at least 1985. The only two larger gains were 31% in early April 2020 during Covid and 28.4% in August 1986 when OPEC announced a surprise production cut. One-week rallies of this magnitude aren’t very common.

With oil prices up so sharply, it’s not surprising that equities have been under pressure, but looking at past moves shows that the inverse relationship isn’t as strong as you would think. The chart below compares the weekly change in crude oil to the S&P 500 going back to 1985, and there’s little correlation between the weekly direction of crude oil prices and the S&P 500. If anything, the correlation is slightly positive.

The shaded area includes each of the prior weeks when crude oil prices were up 20%, and of the seven occurrences, the S&P 500 was up three times and down four. For all seven weeks, the S&P 500’s median decline was 1.2%. Based on where futures are trading right now, guess how much the S&P 500 is down this week? 1.2%!

The Closer – Crude Golden Cross, Skew, Productivity – 3/5/26

Log-in here if you’re a member with access to the Closer.

- Front month crude oil is setting up for a golden cross; a technical pattern that has historically played out to be less bullish than its reputation implies.

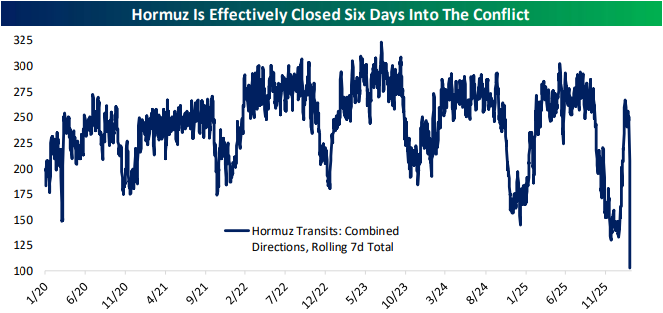

- The closure of Hormuz has resulted in extreme upside skew in options markets for crude oil.

- Labor productivity received material upward revisions for the past six quarters.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

The Triple Play Report: 3/2/26 – 3/4/26

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report covers what each company does, what this quarter’s results say about their growth outlooks, and their histories of delivering triple plays. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read today’s Triple Play Report. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.