ETF Trends: US Sectors & Groups – 5/11/17

Gold and oil have finally popped on a trailing 5 day performance basis with gold miners and oil-related companies leading the charge on our best performers list. Brazil, South Korea, South Africa, and Russia have also popped on strong emerging markets price action. On the losing side of the slate, Spain, Biotech, banks, and “safe haven” currencies have sold off with Swiss franc and Japanese yen down notably.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Chart of the Day: One Breadth Measure Fails to Keep Up

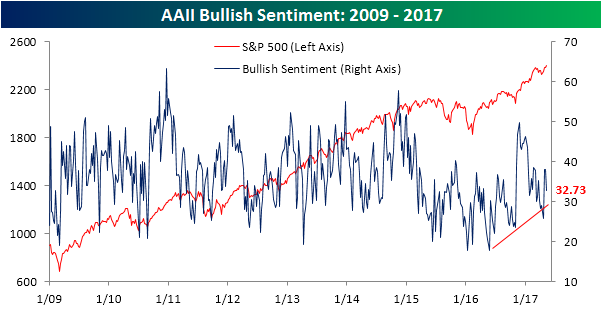

Bulls Retreat…Again

After a pretty large uptick in positive sentiment last week, individual investors reined in their horns this week, even as the S&P 500 hit new all-time highs. According to AAII’s weekly survey, bullish sentiment dropped from 38.07% down to 32.73% for the largest weekly decline since March 9th. This week’s reading also extends the streak of sub-50% readings to a record 123 straight weeks.

For full access to our market analysis that is second to none, start a 14-day free trial to our Bespoke Institutional research platform.

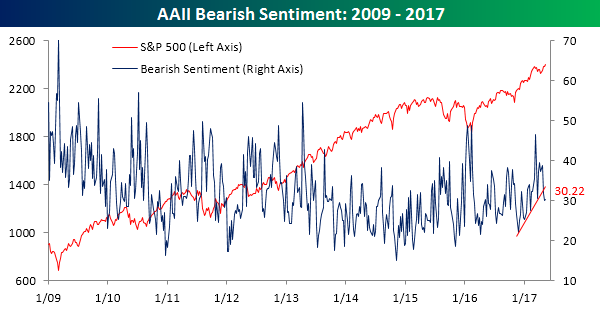

While bulls retreated, bears saw only a slight uptick this week as bearish sentiment increased from 29.95% up to 30.22% keeping it below the uptrend line that was broken to the downside last week.

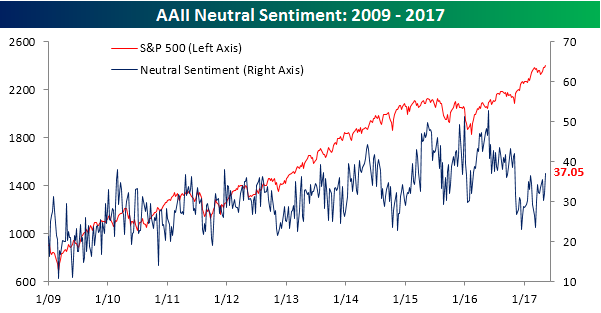

With little uptick in bearish sentiment, all the bulls that were shaken out this week found themselves in the neutral camp as this measure increased to 37.05% from last week’s reading of just under 32%. That’s the largest weekly increase since mid-March and the highest reading since before the election. Perhaps it was this week’s abrupt firing of FBI Director James Comey or just a general feeling of unease at record highs, but individual investors definitely took on a more cautious attitude in the last few days.

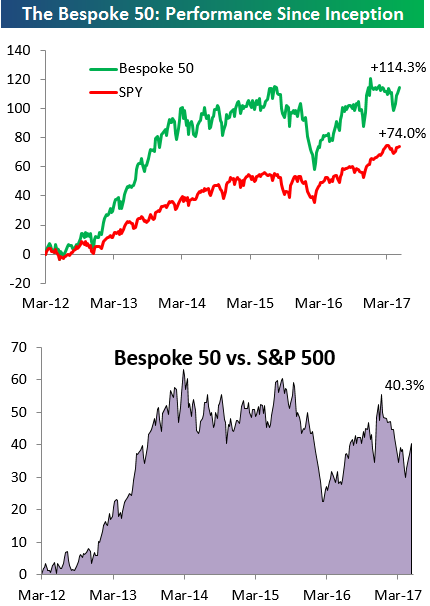

the Bespoke 50 — 5/11/17

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 40 percentage points. Through today, the “Bespoke 50” is up 114.3% since inception versus the S&P 500’s gain of 74.0%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, sign up for Bespoke Premium ($99/month) at this checkout page and get your first month free. This is a great deal!

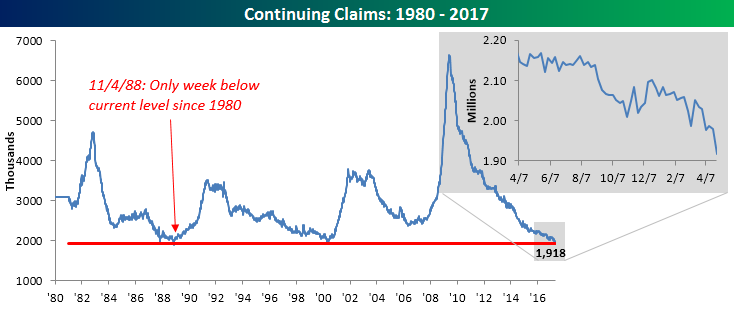

Continuing Claims Make Another Multi Year Milestone

In addition to this week’s lower than expected print in jobless claims, continuing claims were even more impressive. In this week’s report, continuing claims came in at 1.918 million, which was not only well below the consensus expectation of 1.980 million, but it was also the lowest weekly reading in this indicator of the current economic expansion. In fact, the only other time since 1973 where continuing claims were lower was in the first week of November 1988. Someday, both initial and continuing claims will start trending higher again, but until they do, it is a bullish sign for the market and economy.

For full access to our market analysis that is second to none, start a 14-day free trial to our Bespoke Institutional research platform.

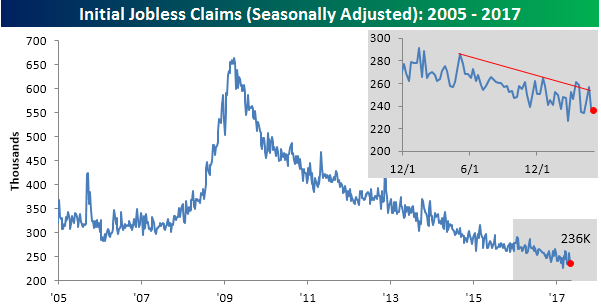

Jobless Claims Lower Than Expected

Jobless claims came in lower than expected this week, falling from 238K down to 236K and 9K below the consensus expectation for an increase to 245K. Once again, after bouncing higher two weeks ago, jobless claims are moving back down to the lower end of their range and are within 10K of the multi-decade low of 227K. This week’s print also marked the 114th straight week where claims have been below 300K.

For full access to our market analysis that is second to none, start a 14-day free trial to our Bespoke Institutional research platform.

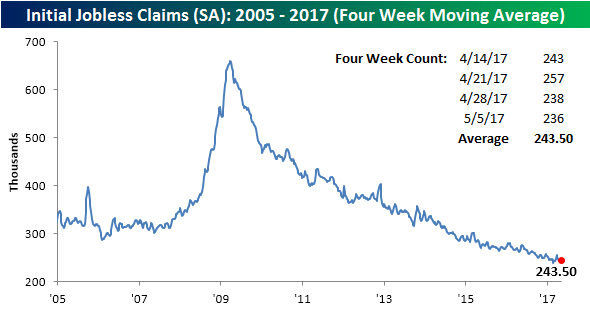

Looking at the four-week moving average, jobless claims ticked up slightly, rising from 243K up to 243.5K. Despite the slight increase, the four-week moving average is still within 4K of its multi-decade low.

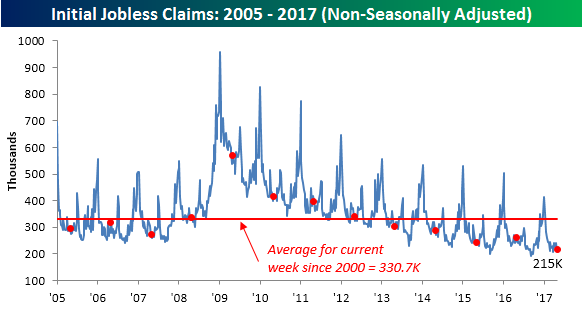

On a non-seasonally adjusted basis, claims ticked up slightly rising from 211.3K up to 215K. For the current week of the year, that’s the lowest reading since 1973 and more than 115K below the average for the current week of the year dating back to 2000. No matter what metric you use, jobless claims were positive this week.

Chart of the Day: Credit Markets Confirming Rally

Bespoke Short Interest Report: 5/10/17

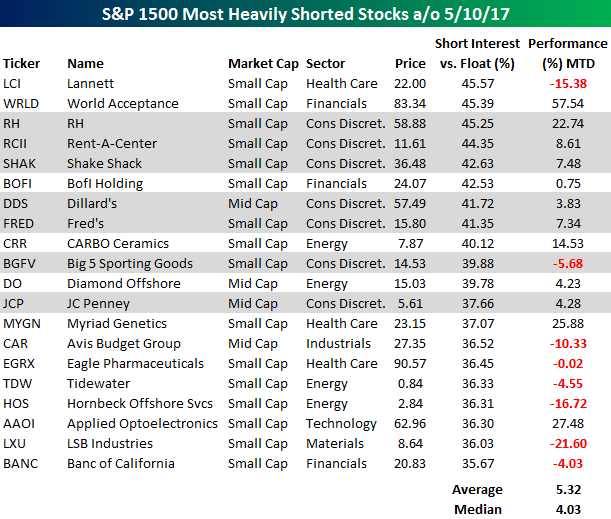

S&P 1500 Most Heavily Shorted Stocks

The major exchanges released short interest figures for the end of April after the close on Tuesday, and while overall levels of short interest didn’t see much in the way of major changes, the number of heavily shorted stocks continues to expand as 61 stocks in the S&P 1500 now have more than a quarter of their float sold short. In the interest of space, the table below lists the 20 stocks in the S&P 1500 with the highest levels of short interest as a percentage of float. As shown in the table, these stocks have been performing admirably so far in May with an average gain of 5.32% and a median gain of 4.03%. The big winner on the list has been World Acceptance (WRLD) which has rallied over 57%, helped in large part by a positive earnings report on Tuesday.

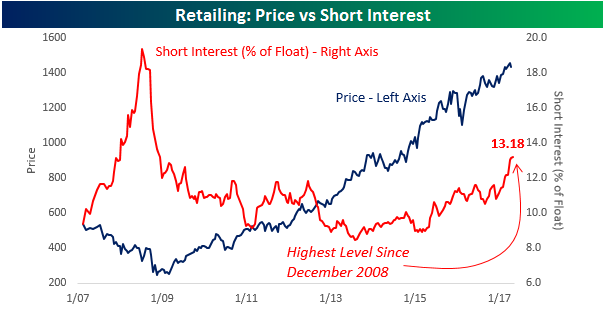

Another trend in the semi-monthly short interest figures over the last few months has been the strong presence of retail-related stocks. As shown in the chart, short interest as a percentage of float for the group is currently over 13% and at its highest level since the Financial Crisis. Obviously, with Death By Amazon, sentiment towards the retail sector is tilted to the negative side, and while our longer term view towards brick and mortar retail is negative, nothing moves in a straight line. There will be times when sentiment gets too extreme and the sector will rally.

Another trend in the semi-monthly short interest figures over the last few months has been the strong presence of retail-related stocks. As shown in the chart, short interest as a percentage of float for the group is currently over 13% and at its highest level since the Financial Crisis. Obviously, with Death By Amazon, sentiment towards the retail sector is tilted to the negative side, and while our longer term view towards brick and mortar retail is negative, nothing moves in a straight line. There will be times when sentiment gets too extreme and the sector will rally.

One example of this shows up in the most recent short interest data. As shown, seven of the twenty stocks highlighted are retailers, ranging from RH with over 45% of its float sold short to JC Penney (JCP) which has close to 38% of its float sold short. In terms of performance, though, six of the seven stocks highlighted are up so far in May with an average gain of 7%. With some of these companies starting to report results that weren’t quite as bad as the market expected, the group is catching a break.

For full access to our market analysis that is second to none, start a 14-day free trial to our Bespoke Institutional research platform.

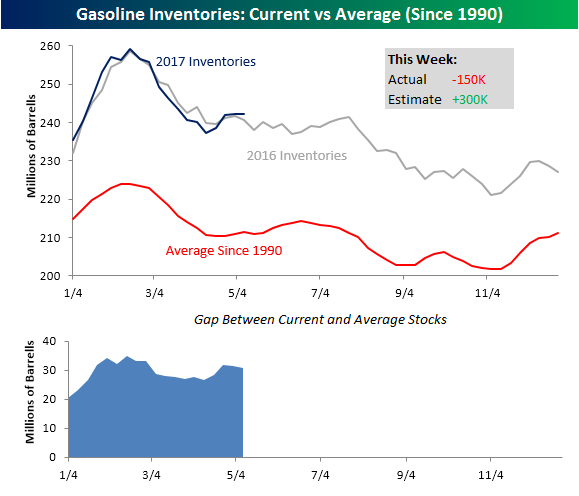

Larger Than Expected Declines in Crude and Gasoline Stockpiles

For full access to our market analysis that is second to none, start a 14-day free trial to our Bespoke Institutional research platform.

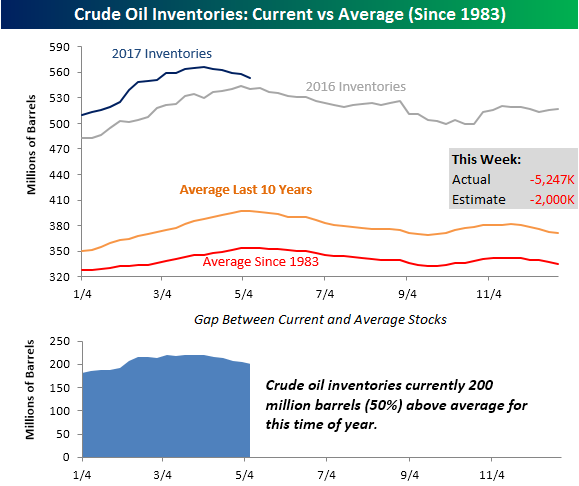

Today’s weekly inventory reports from the Department of Energy (DoE) showed larger than expected declines in both crude oil and gasoline stockpiles. Since it’s been awhile since we last updated our charts of current inventories relative to expectations, we wanted to update them below. In the case of crude oil, stockpiles declined by 5.247 million barrels versus expectations for a decline of just 2 million barrels. This week’s decline was also the largest weekly decline of the year. Looking at how inventories stack up relative to historical averages, current levels are still well above average and even above where they were at this time last year. What is important to note, though, is that inventory levels peaked at the end of March when they normally don’t peak until right about now. If the seasonal decline in stockpiles that normally begins in early May started a month early this year, that could help to support prices going forward.

In terms of gasoline stockpiles, this week’s report showed a modest drawdown of 150K barrels compared to expectations for an increase of 300K. As shown in the chart, current inventory levels are pretty much right in line with where they were a year ago at this time and have been following the pattern of last year pretty closely. Relative to the long-term average going back to 1990, this year’s pattern has also been following the seasonal script, albeit from a much higher base.