The Bespoke Report – 6/2/17 – Baby Step

Just when you think the market has run out of catalysts to push stocks to new highs, they break out and rally. With earnings season in the rearview mirror and President Trump coming back from an overseas trip, the possible positive catalysts for equities were hard to come by. In the market, though, has there ever been a rally based on a positive catalyst that everyone was expecting? Of course not. If that was the case, it would have already been priced in!

While the S&P 500 actually took out its bull market highs on an intraday basis in early May, it didn’t make a convincing breakout to new highs until this week, when the index cleared its two-plus month period of consolidation. As shown in the chart below, the stair step pattern we have been highlighting endlessly for months now remains intact, although, at this point, the most recent run still looks like a baby step compared to prior legs higher. Will it continue? Only time will tell, but in this week’s report, we provide updates to both the pros and cons for further gains down the road.

If you’d like to read our thoughts on recent performance plus the rest of this week’s Bespoke Report newsletter, take advantage of our one-month Bespoke Premium free trial offer. Sign up now at this page.

Have a great weekend!

The Closer 6/2/17 – End of Week Charts

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. This week, we’ve added a section that helps break down momentum in developed market foreign exchange crosses.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

Click here to start your no-obligation two-week free Bespoke research trial now!

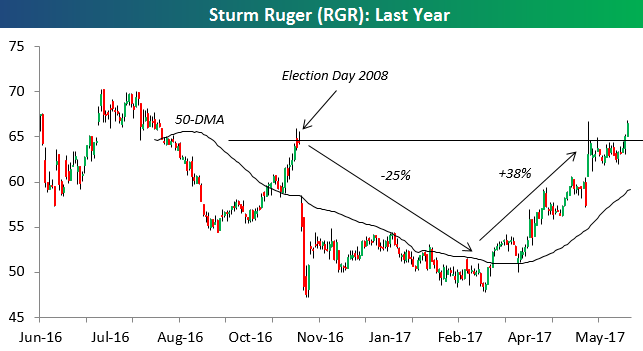

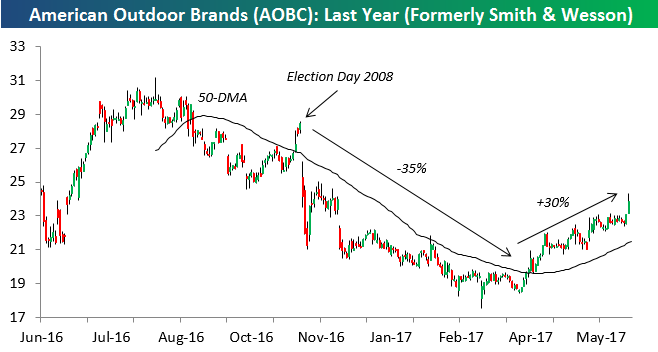

Gun Makers Reload

The two most widely followed gun makers are Sturm Ruger (RGR) and American Outdoor Brands (AOBC), which was formerly Smith & Wesson. Through much of President Obama’s two terms, these stocks went gang-busters. Anytime there was talk about limiting or outlawing gun ownership, a certain percentage of Americans would rush out and buy more of them. Investors realized this as well, and the stocks were bid higher.

Leading up to the 2016 Presidential Election, both RGR and AOBC were rallying because the stock market was giving Clinton a much higher chance of victory than Trump. When Trump shocked the world and won on November 8th, the gun-makers tanked the following day. With the GOP guaranteed to hold the White House for the next four years, investors quickly realized there would be no Second Amendment threats for the foreseeable future. You can see the sharp drops following the 2016 Election in the charts of RGR and AOBC below.

In the first few months following last year’s Election, RGR and AOBC continued to trend lower. At their lows in early March, RGR was down 25%, and AOBC was down 35%.

We’re highlighting the two names today because recently they’ve been on a tear. AOBC has rallied 30% off its lows, while RGR has rallied 38% and just this week moved above where it was trading prior to the Election.

Over the last few weeks there have been a lot of data points highlighting the “Trump fade,” where asset classes that moved sharply higher immediately following the Election have given it all back. In the case of the gun-makers, it’s the same story only in the opposite direction.

S&P 500 P/E Contraction?

Below is a chart of the S&P 500’s price versus its trailing 12-month P/E ratio. As you can see, up until the March 1st high for the S&P, its P/E ratio was trending right along with it. Since then, however, we’ve seen P/E contraction, even though the index has gone on to make a new high. This means that earnings (the E in P/E) have outpaced price (the P in P/E) over the last couple of months. That’s a good thing, especially for anyone who was worried about valuations.

S&P 500 Quick-View Chart Book — 6/2/17

B.I.G. Tips – What Are Millennial Investors Up To?

ETF Trends: US Sectors & Groups – 6/2/17

Treasuries got a bump today following a weaker than expected NFP print and some soft details in the guts of the report. We’ll have a full recap in The Bespoke Report tonight. Other strong performances over the last week come from international equities (Turkey, Japan, and Germany all have improving Manufacturing PMIs per the May data from Markit this week). Energy names continue to grind lower on a trailing 5 day basis with natural gas, oil exploration & production, and Energy all much weaker.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

ETF Trends: Hedge – 6/1/17

Energy commodity-related ETFs continue to underperform dramatically although natural gas has taken the dubious top spot for worst performing ETFs over the past five days. Best performers are varied: retail ETFs, consumer plays, and Chinese equities are some of the biggest gainers over the past week.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

The Closer — Gearing Down, Global & Domestic — 6/1/17

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke Institutional clients, we review global manufacturing PMIs, US auto sales, Brazilian growth, and Mexican IMEF PMIs released today.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

The Closer is one of our most popular reports, and you can see it and everything else Bespoke publishes by starting a no-obligation 14-day free trial to our research!

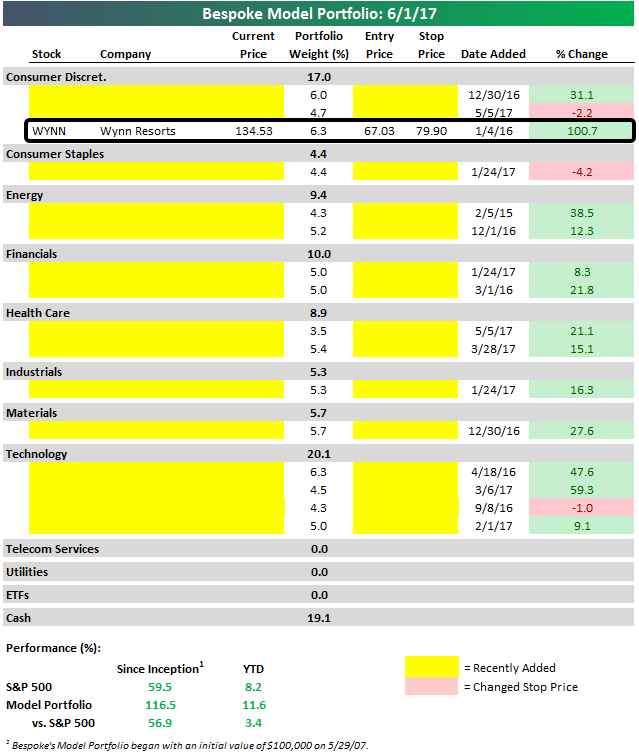

Bespoke Model Portfolio: WYNNing!

In early 2014, luxury casino company Wynn Resorts (WYNN) traded up near $250/share, but by early 2016 the stock had fallen more than 75% to trade as low as $57.74. When the stock dipped into the $60s, founder and CEO Steve Wynn began buying up a massive amount of shares. Between December 2015 and January 2016, Wynn purchased roughly $95 million worth of his company’s shares for an average price of $60.70. In less than a year and a half, Wynn has turned that $95 million purchase into $212 million as shares have jumped 120% to $134.

In early 2016, Bespoke also thought WYNN shares looked attractive. On January 4th, 2016, we added the name to our Bespoke Model Portfolio at $67.03. That trade is up over 100% as of today.

The Bespoke Model Portfolio is included with all three of our research packages for investors, and it’s a portfolio of our best growth stock ideas. Since inception in May 2007, the portfolio is up 116% versus a gain of 59.5% for the S&P 500. (As always, past performance is not a guarantee of future results.) Below is a snapshot of the portfolio as it’s presented to our members, but only the WYNN position is shown. We’ve redacted the remaining holdings — you have to be a member to see them! Start a 14-day free trial to Bespoke Premium to become a member and see the Bespoke Model Portfolio now. You’ll also get a 20% lifetime discount when you sign up today.