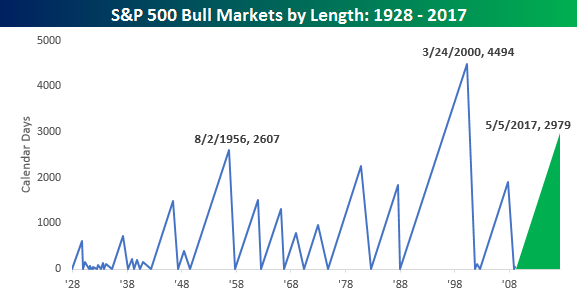

Bull Market Officially Turns Eight

While the eight-year anniversary of the financial crisis low was on March 9th, the bull market didn’t officially turn eight until last Friday when the S&P 500 closed at its first new all-time high since March 1st (eight days before the eight-year anniversary). Below we have updated our bull market charts which compare the current bull market in the context of prior bulls in terms of length and strength. Remember, we define bull and bear markets as rallies (declines) of 20% of more on a closing basis that were preceded by a 20%+ decline (rally). At 2,979 calendar days and counting, the current bull market ranks as the second longest of all time, ahead of the early to mid-1950s bull market by about a year but way behind the granddaddy of them all which spanned from 1987 through 2000.

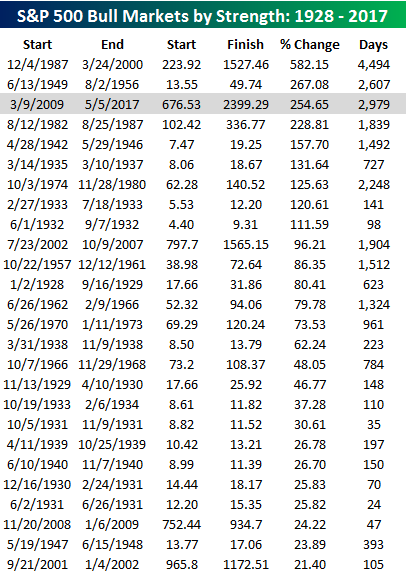

In terms of strength, the current bull market ranks as the third strongest of all time. The table below lists all S&P 500 bull markets since 1928 sorted by strength. The only two that were stronger than the current one were the 1987 – 2000 run and the 1949 – 1956 rally. At current levels, though, the S&P 500 is right on the heels of the bull that ended in 1956. In fact, to move into second strongest of all time, the S&P 500 would have to rally just 3.4% to 2,483.44. A move into first place, however, is a bit more of a longshot. In order to move into the top spot, the S&P 500 would have to rally an additional 92% to 4,614 without a 20% decline in between. It’s a ways off, but we wonder if even that would be enough to move the AAII Bullish sentiment reading above 50%.

Bespoke Brunch Reads: 5/7/17

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Policy Pros & Cons

Minutes of the Meeting of the Treasury Borrowing Advisory Committee of the Securities Industry and Financial Markets Association May 2nd (US Department of the Treasury)

A summary of the TBAC meeting assessing the need for ultra-long-term bonds with maturities out to 50 or 100 years. While their decision isn’t final, it does make it less likely the Treasury will adopt coupon debt that long. We should note the TBAC does suggest a 50 year zero coupon bond might receive lots of interest. [Link]

Corporate Tax Cut as Growth Elixir? Foreign Experience Suggests Caution by Greg Ip (Wall Street Journal)

Evidence suggests that regardless of other potential upsides or downsides to changing the corporate tax rate (there are many arguments on both sides), large corporate tax cuts will not create rapid economic growth. [Link; paywall]

Germany

Why Germany Still Has So Many Middle-Class Manufacturing Jobs by Hermann Simon (Harvard Business Review)

An analysis of what makes Germany’s famed mittelstand so good at producing “Hidden Champions”: companies that excel within their industry, have revenues below 5bn EUR, and are unheralded by the general public. [Link]

The global decline in the labour income share: is capital the answer to Germany’s current account surplus? by Bennet Berger and Guntram Wolff (Bruegel)

The authors argue that Germany’s large and persistent current account surplus is a different macroeconomic response to the same problems which result in high unemployment in other Eurozone members. We agree. [Link; 17 page PDF]

Sports

The Future of Football by Spencer Hall (SBNation)

A long piece but one filled with interesting thoughts about the future of the most popular sport in America: rules changes, coaching, and equipment all get attention. [Link]

How Ueli Steck Met Mountaineering’s Oldest Companion: Tragedy by Michael Wejchert (NYT)

The story of a Swiss mountain climber’s daring career and an investigation of the sport of mountaineering. [Link; soft paywall]

Moar Fyre

Comcast Rejected Funding Days Before Doomed Fyre Festival by Polly Mosendz and Kim Bhasin (Bloomberg)

Last week’s horrific failure, the Fyre Festival, was a (massively mistaken) branding exercise for Fyre Media Inc, a company that Comcast’s venture capital arm (yeah, we had no idea either) declined to fund just before the debacle. [Link]

“Let’s just do it and be legends man” by Gabreille Bluestone (Vice)

More on the massive squandering of resources and general ineptitude of the Fyre Festival organizers. False advertising class action lawsuits against models, “disaster pricing” for basic equipment like toilets and showers, customs snafus, and everything else you can imagine. [Link]

Hunger

Shameful Lunch Shaming by Billy Shore (Medium)

A passionate argument in favor of giving hungry kids the food they need, without stigma. [Link]

Venezuela Is Starving by Juan Forero (WSJ)

The catastrophic results of nationalization and economic collapse: the most basic resources to sustain life are no longer available in Venezuela. [Link; paywall]

Decline & Fall

Tyler Cowen and the Fallacy of American Laziness by Laurence B. Siegel (Advisor Perspectives)

Savage pushback against the idea George Mason economist Tyler Cowen has trumpeted: that American society is in decline and it’s all thanks to a “complacent class”. [Link]

Brexit dinner: live leaking from the second sitting by Robert Shrimsley (FT)

A satirical imagining of another round of last week’s disastrous Brexit dinner, presented in the format of angered live-tweeting from both sides of the table. [Link; paywall]

Bankruptcy

Amid Brick-and-Mortar Travails, a Tipping Point for Amazon in Apparel by Nick Wingfield (NYT)

As retailers reel, Amazon is looking for ways to up the pressure on apparel retailers with custom clothing options and private-label manufacturing. [Link, soft paywall]

U.S. Courts: Bankruptcy Filings Drop 6 Percent in 2016, Lowest since 2006 by Bill McBride (Calculated Risk)

As consumers and businesses continue to see improved income and activity in the wake of the last recession, bankruptcy filings have made new lows. [Link]

New Products

Elon Musk teases future plans at TED talk by Glenn Chapman (AFP/Yahoo)

At a TED talk in Vancouver, Musk talked about tunnel boring and mass transit. [Link]

U.S. SEC approves request to list quadruple-leveraged ETFs (Reuters/Yahoo)

The good news is that you’ll soon be able to buy a 4x leveraged long or short version of the S&P 500. The bad news is that you’ll soon be able to buy a 4x leveraged long or short version of the S&P 500. [Link; auto-playing video]

Have a great Sunday!

The Bespoke Report – The Death of Volatility

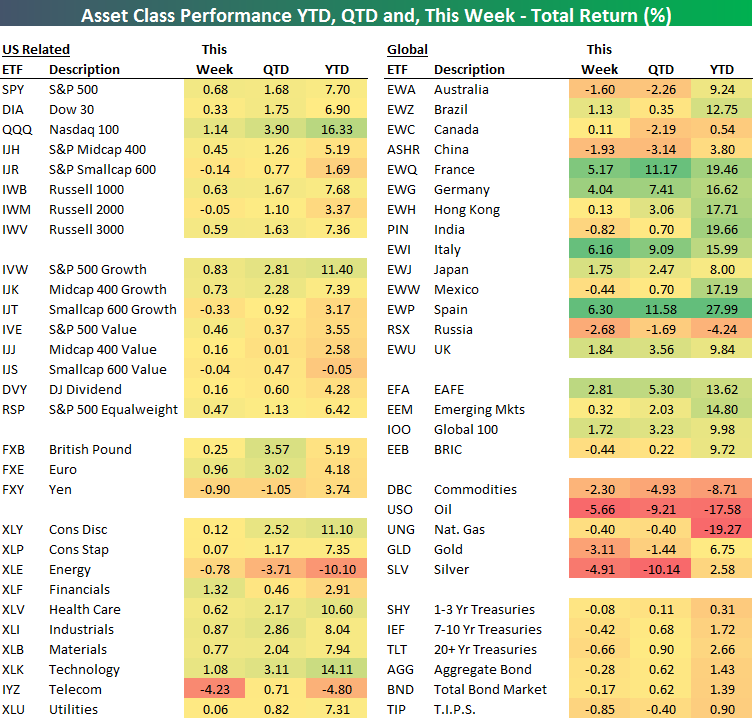

Bespoke’s Asset Class Performance Matrix — Cinco de Mayo Edition

Below is a look at Bespoke’s asset class performance matrix using key ETFs that we track on a regular basis. For each ETF, we highlight its total return over the last week, quarter-to-date, and year-to-date.

US equity ETFs posted modest gains this week, with the S&P 500 rising 0.68%. The real star of the week, and for that matter, quarter and YTD has been the Nasdaq 100 (QQQ), which is up over 16% on the year! Just two sectors (Energy and Telecom Services) were down on the week, while Financials, Technology, and Industrials led the way higher.

Although US equities were up, international markets continued their trend of outperformance with Europe up sharply, although Asia was a bit weak. The YTD returns for some of these countries have been incredible with gains in excess of 15% not out of the norm.

Have a great weekend!

Start a 14-day free trial to our Bespoke Institutional research platform to view our famous Bespoke Report newsletter.

The Closer 5/5/17 – End of Week Charts

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

Click here to start your no-obligation two-week free Bespoke research trial now!

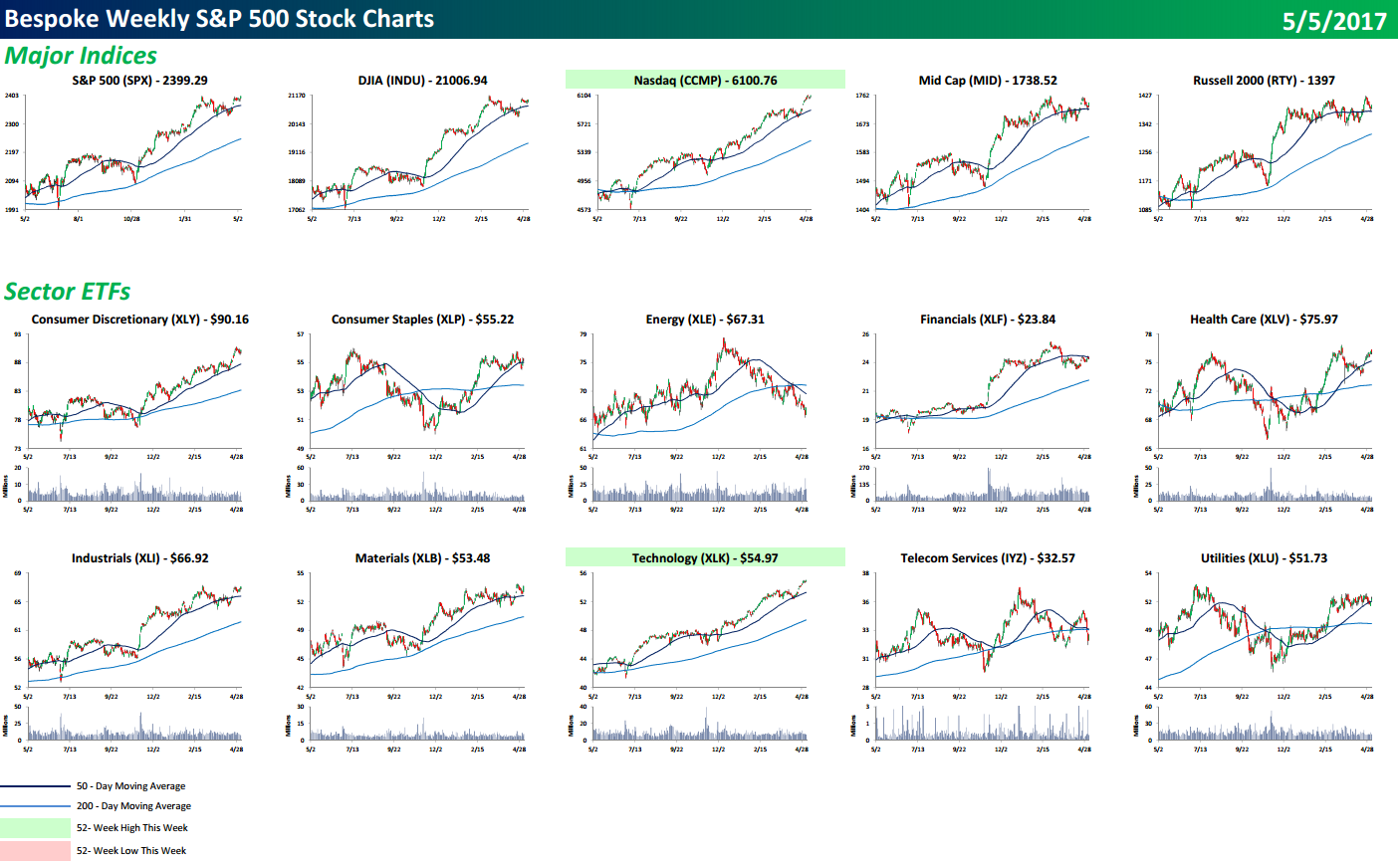

S&P 500 Quick-View Chart Book — 5/5/17

Each weekend as part of our Bespoke Premium and Institutional research service, clients receive our S&P 500 Quick-View Chart Book which includes one-year price charts of every stock in the S&P 500. You can literally scan through this report in a matter of minutes or hours, but either way, you will come out ahead knowing which stocks, or groups of stocks, are leading and lagging the market. The report is a great resource for both traders and investors alike. Below, we show the front page of this week’s report which contains price charts of the major averages and ten major sectors.

To see this week’s entire S&P 500 Chart Book, sign up for a 14-day free trial to our Bespoke Premium research service.

ETF Trends: Fixed Income, Currencies, and Commodities – 5/5/17

European ETFs have resumed their trend of dramatic 5 day outperformance as equities on the continent have spiked ahead of a likely defeat for Marine Le Pen in the second round of French elections. Virtually every ETF in the top 20 is related in some way to Europe. Underperformance is all about commodities with Telecoms the only ETF in the ten worst performers that isn’t either directly exposed to commodities or commodity producers.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Bespoke Consumer Pulse Data Bounces Back, But…

Each month, Bespoke runs a survey of 1,500 US consumers balanced to census. In the survey, we cover everything you can think of regarding the economy, personal finances, and consumer spending habits. We’ve now been running the monthly survey for more than two years, so we have historical trend data that is extremely valuable, and it only gets more valuable as time passes. All of this data gets packaged into our monthly Bespoke Consumer Pulse Report, which is included as part of our Pulse subscription package that is available for either $39/month or $365/year. We highly recommend trying out the service, as it includes access to model portfolios and additional consumer reports as well. If you’re not yet a Pulse member, click here to start a 30-day free trial now!

Since the election last November, pretty much all of the economic indicators we’re able to track in our monthly survey turned more bullish. In our survey prior to this month, however, things dipped slightly. Coming into this month, we were very interested to see if this dip continued or if it was just a blip. Once we got the survey data back, we were happy to see that it was more of a blip than the start of a dip.

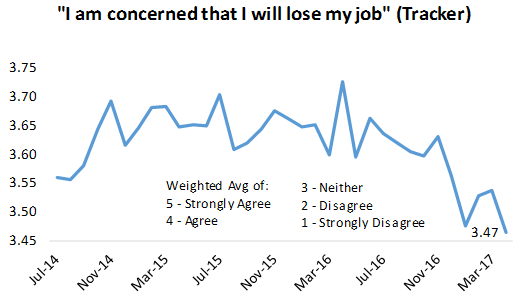

Below we highlight three charts from our Pulse survey this month that show the bounce back. The first chart is our “job loss concern” tracker. We ask consumers how concerned they are that they will lose their jobs. A high reading is bad for the economy because when people are concerned that they’ll lose their job, they’re much less likely to spend money, especially on discretionary items. As shown in the chart, our tracker actually made a new low in our survey series going back to 2014, meaning consumers are the least worried they’ve been about losing their jobs in quite some time.

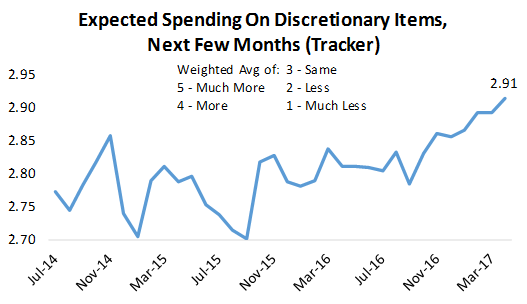

The second chart we’re featuring from this month’s Pulse report is expected spending on discretionary items. We mentioned above that employment concerns have a big impact on discretionary spending. And with employment concerns at new lows, it’s no surprise that our expected discretionary spending tracker hit a new high in our survey. Plans for spending “over the next few months” have been ticking higher now for more than six months.

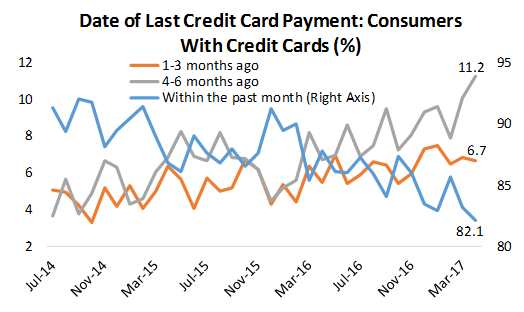

While employment is healthy and spending is expected to increase, not all was rosy in this month’s Pulse report. One thing we’re seeing is that late payments on credit cards are starting to increase. We provide more analysis of why this might be happening in our monthly Pulse report, but this is definitely something we’ll be monitoring in the months ahead.

To track additional consumer sentiment trends, click here to start a 30-day free trial to our Pulse service now!

Shanghai Composite Breaking Down

Since double-bottoming at the same time as oil did in early 2016, China’s Shanghai Composite has trended steadily higher over the past 15 months. But after making a broad double top between November and April, the index has now broken its uptrend off Q1 2016 lows. There’s a more recent trend that’s been in place since July 2016 which has been tested three times previously. The close today brought the Shanghai Composite below that trend as well. This is a bearish technical set-up.

The Closer — AHCA Passage And What’s Next, Productivity, Global Services PMIs — 5/4/17

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at what’s required for the AHCA (passed by the Republicans in the House today) to become law. We also update tracking of productivity in the US and global whole-economy and services sector PMIs.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

The Closer is one of our most popular reports, and you can see it and everything else Bespoke publishes by starting a no-obligation 14-day free trial to our research!