Chart of the Day – Crude Oil Bear Market

B.I.G. Tips – CAT Sales Start to Purr

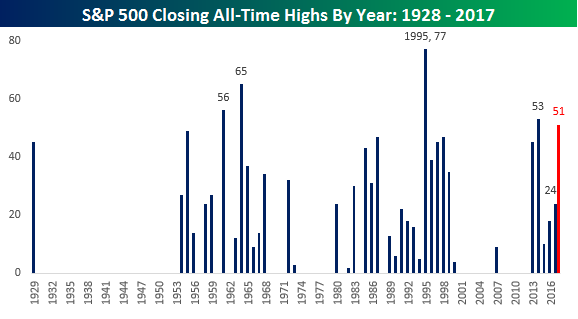

S&P 500 New Closing All-Time Highs By Year

Yesterday’s rally in US equities took the S&P 500 to yet another new all-time closing high, which was the 24th such all-time closing high in 2017. With the year not quite half over, if the pace of the first six months keeps up in the second half, the S&P 500 would be poised for 51 all-time closing highs this year. Obviously a lot can change in the second half, and even a moderate pullback could halt the accumulation of new highs. Conversely, there was a two-month period of consolidation already this year where there were no new highs for the market, so if we see a slow steady grind higher in the second half, the number of new highs could really start to pile up.

The chart below shows the annual number of new all-time closing highs for the S&P 500 going back to 1929. Here, you can really see how a sharp pullback can really halt the frequency of new highs right in its track. After there were 45 new highs in 1929, it took 24 years until 1954 before the S&P 500 did it again. From that point on, the pace of new highs went in waves with many occurrences from the mid-1950s to mid-1960s and again in the 1980s and 1990s, while the pace slowed in the 1970s and 2000s. Since 2013 when the S&P 500 finally took out its pre-financial crisis highs, the pace has picked back up again. If the current pace of highs in the S&P 500 continues, and the S&P 500 closes at 50 or more all-time highs this year, it would rank in the top five of all years. In order to crack 1995’s all-time record of 77 for a single year, though, we would have to see one heck of a rally in the second half.

Bespoke Stock Scores: 6/20/17

ETF Trends: International – 6/20/17

Biotech and long-term Treasuries continue to top our list of the best performers, each up about 3% and with equal-weight outperforming cap-weighted biotech. Underperformers came from the oil sector and related equities as WTI made new lows today. Miners, MLPs, and Russia are also notable underperformers.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Bespoke CNBC Appearance (6/20/17)

Bespoke co-founder Paul Hickey appeared on CNBC’s Power Lunch on Monday (6/20) to talk about Bespoke’s Death By Amazon Index. To view the segment, please click on the image below.

The Closer — Loan Growth Update, Central Banking Preview — 6/19/17

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke Institutional clients, we review bouncing US loan growth data and preview upcoming central bank decisions this week.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

The Closer is one of our most popular reports, and you can see it and everything else Bespoke publishes by starting a no-obligation 14-day free trial to our research!

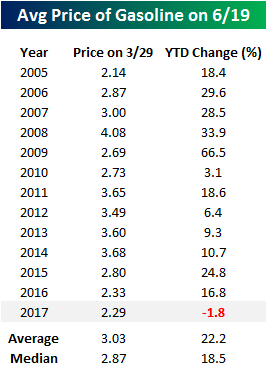

Historically Weak Gas Prices

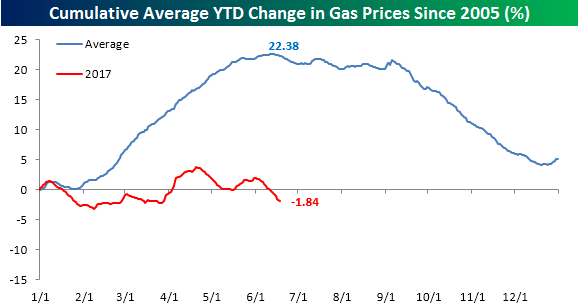

Summer driving season is in full swing, but prices at the pump this year continue to show little in the way of excess demand for gas to fill up the tank. According to AAA, the national average price of a gallon of gas stands at $2.29, and so far in June alone, the average price is down over 3%. Year to date, prices are down nearly 2%. Going back to 2005, there has never been a year where the national average price of gasoline was down on a year to date basis at this point in the year, and there have only been three other years where prices were up less than 10%. With an average YTD gain of 22.2% (median: 18.5%), prices in 2017 have been considerably weaker than they have been in prior years.

What makes this year’s weakness even more noteworthy for this point in the year is that we are currently at the time of year when prices have historically been at their highs for the year. The chart below compares the average price of gasoline so far in 2017 to a composite showing the average YTD change for each point in the year going back to 2005. Based on the historical pattern of gasoline, if prices couldn’t get a lift in the first half of 2017, they could be in for tough sledding in the second half of the year.

On a year/year basis, after an eight-month stretch where gas prices were showing increases, they just moved back into negative territory again in June with a decline of 1.8% y/y. As recently as February, however, the y/y change was well in excess of 30%. Back then everyone seemed to be worrying about a pickup in inflation, but today as low base effects of commodity prices wears off on y/y readings, those fears seem like a distant memory.

ETF Trends: US Sectors & Groups – 6/19/17

As shown below it’s a bit of a mixed bag at the top of the best performers list among the ETF universe we track. Biotech (the equal weight version in the XBI and cap weighted in IBB), mortgage real estate, New Zealand, Vietnam, Australia, long-term Treasuries, and home building stocks are all outperforming. On the worst performers list: miners, steel producers, oil, and Russia.

Bespoke provides Bespoke Premium and Bespoke Institutional members with a daily ETF Trends report that highlights proprietary trend and timing scores for more than 200 widely followed ETFs across all asset classes. If you’re an ETF investor, this daily report is perfect. Sign up below to access today’s ETF Trends report.

See Bespoke’s full daily ETF Trends report by starting a no-obligation free trial to our premium research. Click here to sign up with just your name and email address.

Economic Data Surprisingly Negative

US economic data has been coming in drastically below economists’ estimates of late. Last week we noted that the string of weak readings has been extra painful for housing, with a truly weak residential construction report and a slower than expected homebuilder confidence reading. It hasn’t been all bad news for US data of course; the Atlanta Fed is currently tracking 2.9% GDP in Q2, while the St. Louis Fed model sees 2.32% and the NY Fed is tracking 1.86%. With trend growth around 2%, none of those are terrible. Relative to estimates, however, the data has been much weaker.

As shown below, the Citi Economic Surprise Index, which measures the pace at which indicators are beating estimates, has hit its lowest levels since the summer of 2011, when the economy hit an air pocket at the same time Washington debated raising the debt ceiling and created unnecessary uncertainty (eventually leading to a downgrade from S&P). While recent activity hasn’t been terrible, it’s extremely underwhelming due to the high expectations of economists. That doesn’t mean the economy is crashing; instead, economists will likely cut estimates, data will be stable or possibly tick up a bit, and suddenly the surprise index will rebound. To illustrate the process, below we’ve charted the Citi Economic surprise index and a good old fashioned sin function (remember those from middle school trigonometry?). You can’t use a sin function to predict when or how high the Citi Economic surprise index will bounce, but they are both cyclical, rising and falling back and forth over time. With economic surprises currently coming in worse than all but 5 prior periods of weak data in the history of the Citi index, it’s likely that chastened economists will start underestimating economic performance soon, at least at the margin, restarting the whole cycle to the upside.