Chart of the Day – UnitedHealth (UNH) On Life Support

Q1 2025 Earnings Conference Call Recaps: Cisco (CSCO)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Cisco’s (CSCO) Q3 2025 earnings call.

![]()

Cisco Systems (CSCO) is a global technology leader that designs and sells networking hardware, software, security solutions, and cloud-based services that power the backbone of the internet and enterprise IT infrastructure. Best known for its switches and routers, Cisco also offers advanced products in cybersecurity, observability, collaboration (like Webex), and now AI infrastructure. The company serves a wide range of customers, from hyperscalers and telecom providers to governments and small businesses, offering the tools to build, secure, and automate digital networks. CSCO beat expectations and surpassed its full-year AI order target a quarter early, hitting over $1B in AI infrastructure orders, including $600M+ in Q3 alone. Orders from webscale customers rose 32%, and enterprise orders grew 22%, driven by demand for Ethernet-based AI systems, Wi-Fi 7, and refreshed routing. Security was another standout, with high double-digit order growth and Splunk landing its largest deal ever. CSCO emphasized momentum in sovereign AI projects like Saudi Arabia’s Humain and capacity constraints, not demand, limiting AI revenue ramp. Tariff impacts are expected to weigh on Q4 margins, but CSCO reported no signs of pull-forward demand. The stock was up about 6% on 5/15 after the triple play report…

Continue reading our Conference Call Recap for CSCO by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q1 2025 Earnings Conference Call Recaps: Walmart (WMT)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Walmart’s (WMT) Q1 2026 earnings call.

![]()

Walmart (WMT) is the world’s largest retailer, operating a global network of hypermarkets, discount department stores, Sam’s Clubs, and e-commerce platforms. With over 10,500 stores in more than 20 countries, Walmart serves a broad consumer base across income levels. The company also runs a rapidly expanding advertising business (Walmart Connect), a membership program (Walmart+), and global marketplaces, providing a unique lens into consumer behavior at scale. WMT delivered a strong quarter despite an increasingly volatile backdrop. Sales grew 4% (constant currency), with e-commerce up 22% and e-commerce operations turning profitable for the first time globally. Membership income rose nearly 15% and advertising revenue jumped 50%. Tariff pressures, especially from China, were a major focus, as the company warned of rising costs on general merchandise while working to shield food prices. On mixed results, the stock fell as much as 3.5% on 5/15, but it made a quicky recovery…

Continue reading our Conference Call Recap for WMT by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Bespoke’s Morning Lineup – 5/15/25 – Eco Data Deluge

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“How you begin life is not nearly as important as how you end up.” – Emmitt Smith

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

To view last night’s segment on CNN’s OutFront with Erin Burnett, click on the image below.

After some positive days of market performance, the euphoria surrounding the US-China trade talks has faded a bit as investors focus again on rising rates, with the 10-year treasury yield back above 4.5%. Walmart (WMT) marked the unofficial end to earnings season with better-than-expected earnings on inline revenues, and the stock is up fractionally. The morning is much worse for UnitedHealth (UNH) as that company’s terrible year continues with reports that the company is under criminal investigation related to billing practices in its Medicare Advantage plans. Based on where the stock is trading in the pre-market, shares have lost more than half of their value since April 11th!

While the pace of earnings reports is slowing down, today is one of the busier days in recent memory for economic data with Empire and Philly Fed Manufacturing reports for May, Retail Sales for April, PPI for April, jobless claims, Industrial Production, Capacity Utilization, and Business Inventories. As if that’s not enough, Powell will also be speaking at 8:40 eastern.

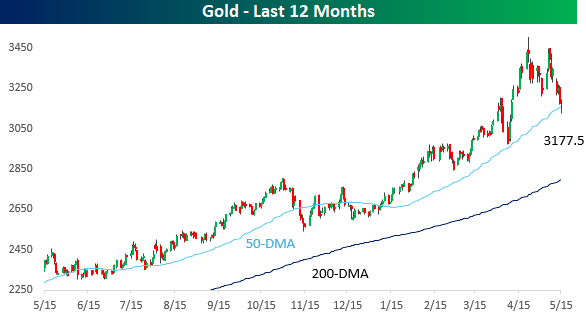

As tensions in global trade pushed economic uncertainty to levels rarely seen before, investors couldn’t get their hands on enough gold. At its high for the year on 4/22, front-month gold prices were up over 30% YTD, and Costco (COST) even had to place a one-ounce limit on the amount of gold that its customers could purchase as sales of the yellow metal on its website exceeded $200 million per month.

With the US and China dialing back on trade tensions, markets and investors have let out a giant exhale of relief, and while it has been good for risk assets, gold prices have taken a hit. Overnight, prices dropped as low $3,123 per ounce, representing a decline of 11% from the recent record high. While prices recovered a bit since the lows, gold briefly traded below its 50-day moving average for the first time since early January.

As gold corrects, its price has become increasingly volatile, and large daily moves have become increasingly common. While it traded more than 2% lower on an intraday basis yesterday, it finished the day down just 1.8%. Even though it didn’t have a daily move of 2%, 11 of the last 25 trading days have seen moves of more than 2%, and just recently, the rolling 25-day total was 12. As shown below, 2%+ daily moves haven’t been that clustered together since 2011, and before that, the Financial Crisis.

The Closer – USD, Mega Cap Impact, Best of Breed – 5/14/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we start out with a dive into options markets’ extremely bearish bets on the dollar (pages 1 and 2). We then check in on the stagnation in earnings estimates and what that means for valuations (page 3). After a look into how the mega caps have impacted recent price action (page 4), we close out with the latest update on our Best of Breed basket (pages 5 and 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 5/14/25

The Triple Play Report — 5/14/25

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 26 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

Evertec (EVTC) is an example of a company that recently reported an earnings triple play after the close on 5/7. The following day, shares rallied 2.5% on the news, extending its streak to four straight share-price gains in reaction to earnings.

Here’s how AI describes the company: Evertec (EVTC) is a financial technology and transaction processing company headquartered in San Juan, Puerto Rico, with operations spanning 26 countries across Latin America and the Caribbean. The company operates through three core segments: Merchant Acquiring, which supports businesses in accepting electronic payments through point-of-sale infrastructure and transaction processing; Payment Processing, where Evertec owns and operates the ATH® debit network and provides ATM, POS, and card network services; and Business Solutions, offering technology outsourcing, core banking platforms, cash processing, and fulfillment services to financial institutions, corporations, and government entities. Processing roughly six billion transactions annually, Evertec plays a vital role in the region’s financial ecosystem. Evertec is well-positioned to benefit from the growing demand for integrated, electronic financial services throughout Latin America and the Caribbean.

EVTC delivered a strong Q1, with revenue rising 11% YoY to $228.8 million. Merchant Acquiring revenue grew 13% to $38.3 million, benefiting from continued growth in Puerto Rico’s consumer spend and higher transaction volumes. The Payment Processing segment posted $78.4 million in revenue, up 10%, and Business Solutions revenue grew 5% on stable demand for core banking and outsourcing services. EVTC discussed strength in Puerto Rico’s consumer economy, supported by low unemployment, wage growth, and government stimulus tailwinds that have proven more resilient than expected. The company emphasized ATH Móvil’s growing ubiquity in Puerto Rico, with expanding use among small and mid-sized businesses and increased relevance in peer-to-peer and government disbursement channels. In Latin America, EVTC is scaling its payment and core banking solutions with a mix of on-premise and SaaS deployments, while its footprint in Colombia and Chile continues to deepen.

Looking at the snapshot below from our Earnings Explorer, Evertec (EVTC) has been a stronger player against analyst estimates fairly consistently. The company has beaten EPS estimates 67% of the time and revenue estimates 87% of the time, and it now has 34 straight revenue beats going all the way back to 2017.

You can read more about EVTC and the 24 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Chart of the Day: Tech Stocks Quickly Reclaim 50-DMAs

Bespoke’s Morning Lineup – 5/14/25 – Mid Week Rest

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“The only strategy that is guaranteed to fail is not taking risks.” – Mark Zuckerberg

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Meta Platforms (META) founder Mark Zuckerberg turns 41 years old today, and love him or hate him, the man has certainly taken some risks in building META into what it is. That’s also why he has a net worth of over $200 billion, making him one of the richest people in the world!

This week, the market has taken a risk on persona, continuing into the pre-market futures. S&P 500 futures indicate a 27-bps point gain at the open while the Nasdaq is 0.40% higher. There’s not much in the way of earnings-related news to contend with today, the economic calendar is empty, and even the geo-political picture has experienced a bit of a lull. Just what you would expect as we all try to get through the middle of the week.

For the S&P 500, the first two trading days of the week have been notable for two big reasons. First, on Monday, the S&P 500 surged above its 200-DMA for the first time in over a month, as the S&P 500 rallied over 3%. The rally of 3.26% was the largest daily gain on a day when the S&P 500 crossed above its 200-DMA since March 2020. Second, it’s hard to see in the chart, but if you squint hard, you can see that yesterday was the first time in over two months that the S&P 500’s 50 and 200-DMA had an upward slope.

Yesterday’s upward shift in the slope of the 50 and 200-DMAs ended a streak of 56 trading days where both moving averages were sloping downwards. As shown in the chart, the length of that streak was far from extraordinary relative to history. During the 2022 bear market, we went nearly a year where at least one of the moving averages was sloping downwards, and during the financial crisis, the market had a stretch of over 19 months where at least one moving average was downward sloping. While the most recent period may not have been the longest streak with at least one moving average sloping downward, the fact that they are both now sloping upward is positive from a psychological standpoint.

The Closer – Whiplash, Nasdaq’s New Bull, Debt Data Deluge – 5/13/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin by evaluating the market’s whiplash so far year to date (page 1) followed by a look at the Nasdaq establishing a new bull market (page 2). Moving on to economic data, we review the latest CPI release (page 3) followed by a deep dive into the latest credit releases including the SLOOS (pages 4 and 5) and the New York Fed’s report on Household Debt & Credit (pages 6-8).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!