Bespoke’s Sector Snapshot — 1/18/18

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a two-week free trial to Bespoke Premium now.

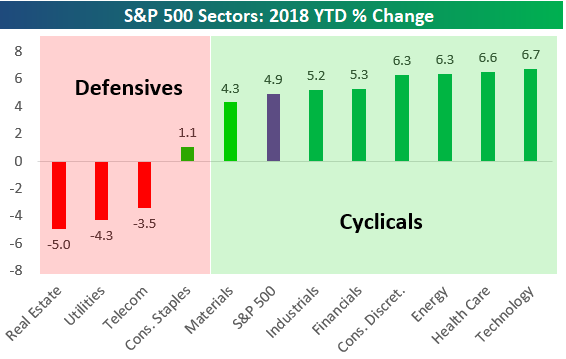

Below is one of the many charts included in this week’s Sector Snapshot, which highlights the year-to-date percentage change for the S&P 500 and its eleven sectors. As you can see, defensive sectors are underperforming while cyclicals have been very strong. That’s the type of underlying action investors want to see.

To see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

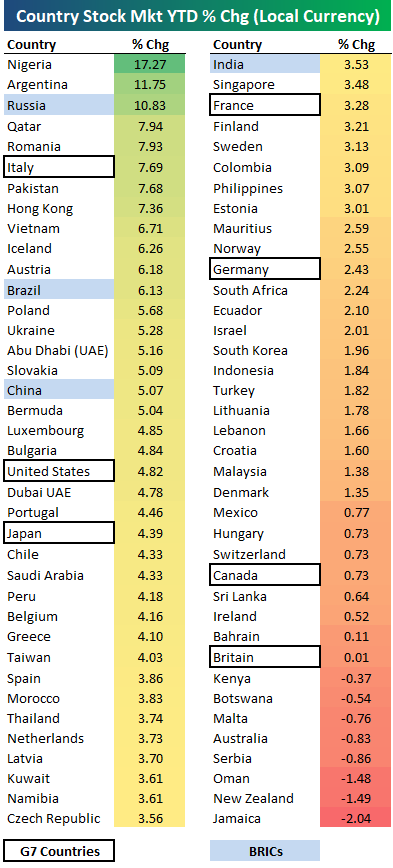

2018 Stock Market Performance of 76 Countries

We’re just 18 days into 2018, but the average country’s stock market (in local currency) is already up 3.51% year-to-date based on the 76 indices highlighted in the table below. Sixty-eight of the 76 countries are “in the black” for the year while just 8 are down.

As shown, Nigeria is off to the best start with a gain of 17.27%, followed by Argentina (+11.75%) and Russia (+10.83%). Italy has been the best G7 country so far, followed by the US and then Japan. Canada and the UK have been the weakest of the G7 with gains of less than 1%.

In terms of declines, Jamaica is down the most, but the drop has been just 2%.

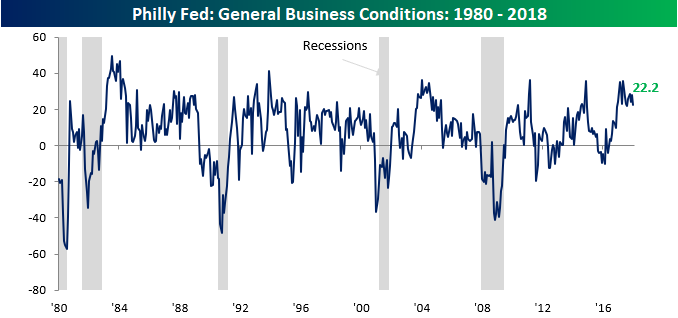

Unlike the Eagles, the Philly Fed Disappoints

Although it was still solid, the January report on Manufacturing from the Philadelphia Fed came in slightly weaker than expected. Think about it like the current Eagles without Carson Wentz; not quite as strong but respectable nonetheless. While economists were forecasting the headline reading in this month’s report to come in at a level of 25.0 versus last month’s reading of 27.9, the actual print came in at 22.2. This may not sound like an important level, but keep in mind that it is the 14th straight monthly reading above +20. That has only happened one other time in the history of the survey dating back to 1980!

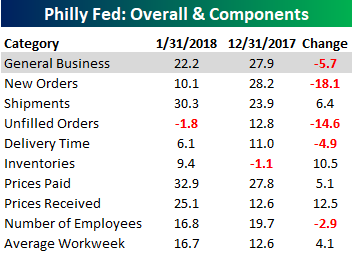

As far as the internals of this month’s report were concerned, there wasn’t a whole lot of strength to mention. Of the report’s nine sub-indices, just five saw m/m gains. Of those, the biggest increases were Prices Received and Inventories. To the downside, the weakness was centered in Orders as both the indices of New and Unfilled Orders saw double-digit declines.

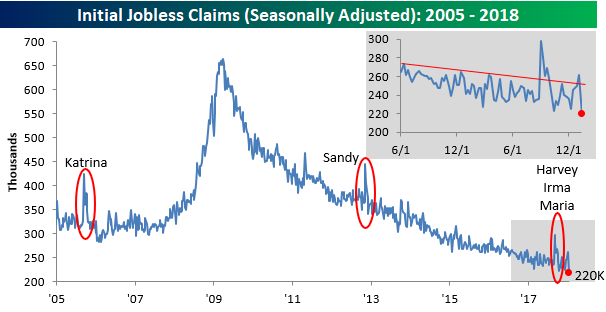

Jobless Claims Back in “Amazing” Mode

After a disappointing report last week, jobless claims plunged this week, falling from 261K down to 220K compared to expectations for a level of 249K. Relative to expectations, this week’s report was the strongest since September 2017. It was also only the 8th weekly print that came in lower than expected by 29K or more since 2001. Even more amazing is the fact that the 220K print is the lowest reading we have seen since February 1973. That’s 45 years ago, folks! And remember, these stats don’t adjust for massive population growth since the 70s either.

The four-week moving average also saw a pretty big decline this week, falling from 250.75K down to 244.5K. That’s still more than 13K above the cycle low of 231.25K back in early November, but it does break a streak of four straight weeks where the reading increased.

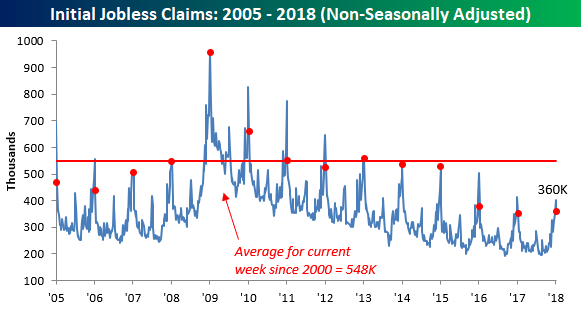

On a non-seasonally adjusted (NSA) basis, jobless claims fell from 403.6K down to 360K. While NSA claims were actually slightly lower at the same time this year, they are still more than 188.1K below the average of 548.1K for the current week of the year dating back to 2000. All in all, it was a very strong report.

Chart of the Day: Senior Living Stabilizes

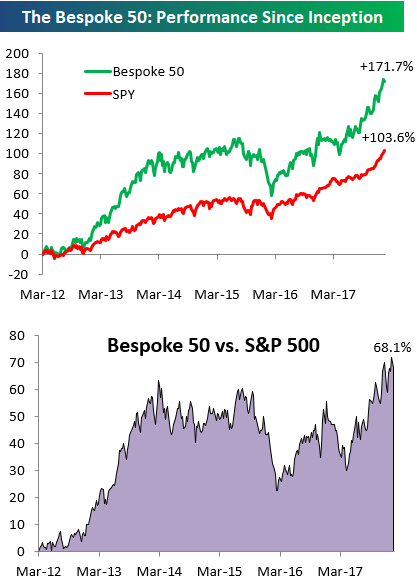

the Bespoke 50 — 1/18/18

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 68.1 percentage points. Through today, the “Bespoke 50” is up 171.7% since inception versus the S&P 500’s gain of 103.6%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

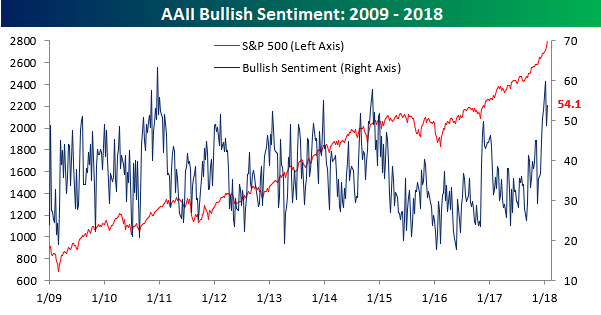

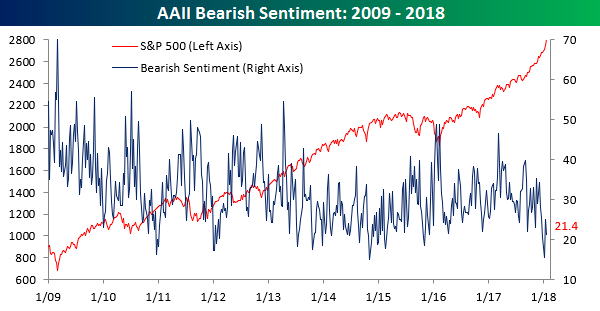

Bulls Back in the Majority

After a one-week dip back below 50%, bulls are back in the majority in the weekly survey of individual investors from AAII. In this week’s survey, bullish sentiment increased from 48.7% up to 54.1%. Outside of the 59.8% print two weeks ago, this week’s level of bullish sentiment is the highest since November 2014.

As bullish sentiment ticked back above 50%, bearish sentiment declined but still held above 20%, falling from 25.1% down to 21.4%.

The Closer — Capplex, IP Trends Stronger, VIX Versus Stocks, BoC Recap — 1/17/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review Apple’s capex plans, US industrial output, the disconnect between stocks and the VIX, and the BoC decision today.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Chart of the Day: Heed the Gap

B.I.G. Tips – One Way Markets

Looking back on the last six months of the S&P 500’s performance, it’s hard to overstate just how remarkable of a run it has been. There have definitely been periods where the S&P 500 rallied more (and many cases a lot more), but the nearly complete lack of downside pressure has been extraordinary. Just look at the chart below. There have only been two periods where the S&P 500 saw more than a 1% drawdown on a closing basis from a closing high, and the largest drawdown was just 2.2%!

There’s hardly been any downside pressure at all. In the chart below we calculated the cumulative amount of downside pressure in the S&P 500 on a rolling six-month basis going back to 1928. To do this, we simply added up the magnitude of the daily declines (measured in basis points where every 100 bps equals 1 percentage point) in the S&P 500 over a six-month rolling window. Heading into today, the cumulative impact of all the S&P 500’s down days over the last six months was a total of 1,230 bps.

How does that stack up relative to other periods? Let’s put it this way; since 1928, there have only been three other periods, which all spanned from 1964 through 1966, where the cumulative impact of down days over a six month period was less than the last six months. The most extreme of these periods was in May 1964, when the cumulative six-month downside impact was less than 1,000 bps. We often hear from people who are amazed at how sanguine the market can be in the midst of all the headlines surrounding Washington and the state of geopolitical affairs, but in the 1960s, the US saw more than a little bit of geopolitical and political turmoil as well! And just like today, in the 60s we saw long periods where the market did nothing but go up. This is a reason we always note that politics and investing don’t mix!

So what can we expect from the market after such an extended rally without much in the way of pullbacks? To help answer this question, we just published a report looking at 18 prior periods where the S&P 500 was closely correlated to the current period and analyzed the returns going forward.

For anyone interested in the trends we uncovered, this report is a must-read. To see it, sign up for a Bespoke Premium membership now!