Bespoke Short Interest Report: 2/28/18

Short interest figures for the middle of February were released after the close on Tuesday, so we have just updated our regular report on short interest trends for the market, sectors, and individual stocks for clients. Below we wanted to quickly highlight S&P 1500 stocks that have more than a third of their float sold short.

Through the middle of February, 17 stocks in the S&P 500 had more than a third of their float sold short, while six of those names had more than half of their float shorted. Sentiment can’t get much more negative than it is for Applied Optoelectronics (AAOI), which has nearly two-thirds of its float sold short. The negative bet has been paying off for traders again this month as the stock is down over 15%. Right behind AAOI, Big 5 Sporting Goods (BGFV) has over 61% of its float sold short, but this trade has gone against traders as the stock is up over 6% MTD. As is often the case when looking at a list of most shorted stocks, names from the Consumer Discretionary sector dominate the list with over half of the names. Of the remaining eight stocks on the list, no sector accounts for more than two names.

In terms of overall performance, the seventeen stocks listed have seen an average decline of 3.58% this month (median: -9.13%) compared to a decline of 2.39% for the S&P 1500. The fact that these stocks are underperforming even when one of them is up nearly 70% (FOSL) illustrates just how weak the rest of the stocks have been. It also doesn’t help the cause for the most shorted stocks that MiMedx (MDXG) has declined more than 55%!

For a more detailed look at short interest data on a regular basis, sign up for a monthly Bespoke Premium membership now!

Fixed Income Weekly – 2/28/18

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s note, we compare return profiles for synthetic investment grade or high yield credit and the equity market.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

Chart of the Day: Tech Sector Weighting Eclipses 25% — First Time Since 2000

Watching S&P 500 Breadth

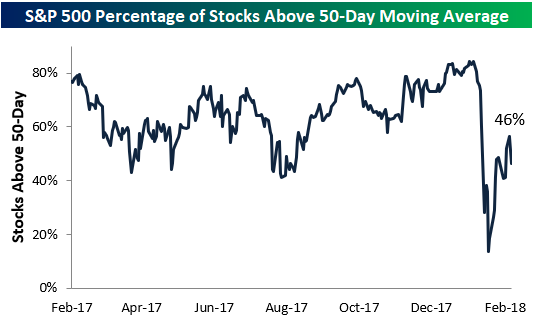

As shown in the chart below pulled from our interactive Chart Tool (available to anyone), the S&P 500 remains just above its 50-day moving average.

The percentage of stocks in the S&P 500 that are trading above their 50-day moving averages remains below the 50% mark, however, which is a sign of weak breadth relative to where the broad index is trading.

The Technology and Financial sectors — which account for roughly 40% of the S&P 500 — are keeping breadth levels for the broad market afloat. As shown below, 78% of Tech stocks are above their 50-DMAs, while 64% of Financial stocks are above their 50-DMAs. There are seven sectors that currently have weaker breadth readings than the 46% level for the S&P 500. These include sectors like Energy, Real Estate, Consumer Staples, Consumer Discretionary, and Materials.

FAANG Trend Analyzer

Our Trend Analyzer has quickly become one of the most widely used tools by Bespoke subscribers. It lets users quickly identify trend and timing trends for key ETFs across asset classes as well as for any stock in the Russell 3,000. The Trend Analyzer also includes the year-to-date change, 5-day change, and % from 50-DMA for each stock or ETF, and it lets users easily see overbought/oversold measures using our “trading range” charts.

One of the most popular features of our Trend Analyzer is the “Custom Portfolios” tab that allows users to build up to 5 custom portfolios. We built a “FAANG” portfolio that allows us to keep tabs on Facebook (FB), Apple (AAPL), Amazon (AMZN), Netflix (NFLX), and Alphabet (GOOGL).

As shown below, all five FAANG stocks are up over the last 5 trading days, with Netflix (NFLX) up the most at +4.33% and Alphabet (GOOGL) up the least at +1.26%. Amazon (AMZN) and Netflix (NFLX) have absolutely crushed it on a year-to-date basis. Netflix is already up more than 50% in 2018, while Amazon is up nearly 30%.

Looking at current trading ranges, Apple (AAPL) and Facebook (FB) have seen the biggest moves higher within their ranges over the last week, but Facebook (FB) is still just below its 50-day moving average after yesterday’s dip. AAPL, AMZN, and NFLX are in overbought territory, while FB and GOOGL are in neutral territory. GOOGL is currently the only FAANG stock that has a “good” timing score given its long-term uptrend pattern and its neutral trading level.

Set up your own custom Trend Analyzer portfolios by starting a two-week free trial to Bespoke Premium now!

Bespoke CNBC Appearance (2/28)

Bespoke co-founder Paul Hickey appeared on CNBC’s Squawk Box on Wednesday morning (2/28) to discuss markets following Tuesday’s Congressional testimony from FOMC Chair Jerome Powell. Click on the image below to view the segment.

Bespoke’s Global Macro Dashboard — 2/28/18

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

The Closer — Powell On The Hill — 2/27/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we dissect testimony from Fed Chair Powell on Capitol Hill today. We also review a big swathe of economic data released today related to manufacturing and trade.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

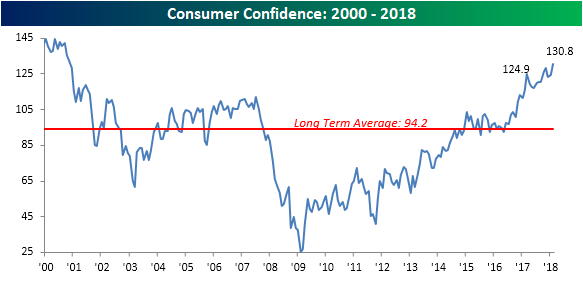

Consumer Confidence Hits a 17-Year High

Tuesday morning’s report on Consumer Confidence for February handily topped already positive expectations, as the headline index came in at 130.8 (versus expectations for 126.0), which was the highest level since November 2000. While Consumer Confidence had a hard time getting above its long-term average for much of the current expansion, it has now been above that level of 94.2 for 21 straight months.

One area of the economy where consumers are very confident is in employment. More and more lately, the percentage of consumers who consider jobs as being ‘plentiful’ has been on the rise. In February’s report, it came in just under 40%, which was the highest level since April 2001. It only makes sense that consumers who are confident also think jobs are easy to get.

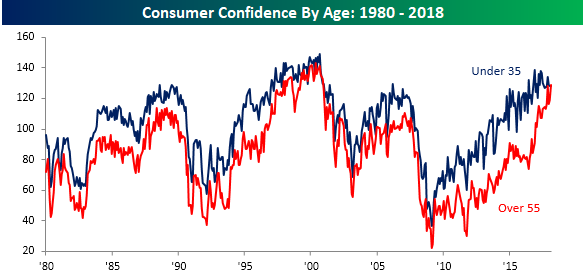

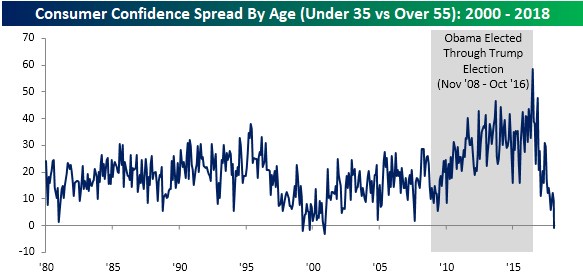

One of the more interesting trends in confidence since the November 2016 election is the shifting demographics of confidence levels. In a nutshell, younger consumers (under 35) have seen little in the way of a confidence boost since President Trump was elected, while older consumers (over 55) have seen confidence surge. After the generational divide between the two age groups widened considerably during the early to mid part of the expansion, confidence levels are now roughly equal.

Looking at how the spread between the two has changed over time, you can actually see that as of the most recent report, confidence among older consumers is now higher than it is for younger consumers. This type of confidence inversion is so rare in fact that it has only occurred three other times since 1980, and all of them came in 1999 and 2000. Another interesting trend to notice is that throughout the terms of President Obama, the confidence gap between younger and older consumers steadily rose. Right after President Trump was elected, however, that gap was quickly erased. You know where to find the President’s base!

While politics has a lot to do with the shift in confidence among different age groups, another factor is interest rates. President Obama’s tenure also coincided with a period when interest rates were generally at or very close to zero. The impact of low-interest rates has nearly the exact opposite impact on older Americans (who generally have more savings) than it does on younger Americans (who usually have more debt). When you think about it that way, it makes a lot more sense that confidence among older Americans started to improve right after interest rates bottomed.

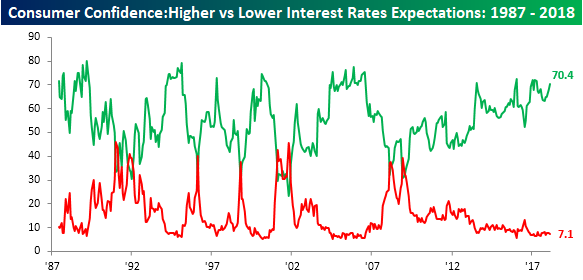

As far as sentiment towards the direction of interest rates, more than two-thirds (70.4%) of consumers expect interest rates to rise, while just 7.1% expect rates to fall. This view among consumers has generally been in place for the last several years. While it’s tempting to look at such a lopsided split between the two and want to take the other side, when rates are at or near zero, there is really nowhere to go but up!