Bespoke Macro Strategist George Pearkes on Bloomberg’s #WDYM

In an interview Thursday evening on Bloomberg’s What Did You Miss?, Bespoke’s Macro Strategist George Pearkes talked to Julia Chatterley, Scarlet Fu, and Joe Weisenthal about recent changes in the US fiscal outlook, the impact that will have on inflation, how the Fed is likely to react, and the way the US dollar has moved recently. To watch the full interview, please click the image below.

Inflation Expectations: Stable But Not Yet Rising

Today the University of Michigan Consumer Confidence survey was released. One of the data points the survey includes is an inflation expectation series, asking consumers what they expect as far as consumer price changes go. In recent years, economists have worried that relatively low inflation may lead consumers to expect lower inflation, leading to a downward cycle of weakening inflation. The good news is, since late 2016 the University of Michigan series have stabilized, as shown in the chart below.

We also like to compare various inflation expectations series from different surveys on a like-for-like basis. To do so, we z-score all of them by taking a given period’s reading and measuring its departure from its all-period average in standard deviations. That adjusts them all for volatility and different levels. As shown, these series have all stabilized around similar levels over the past year or so. That’s good news for members of the FOMC that are worried about inflation expectations getting too low. But at the same time, while recent inflation readings have been strong, there hasn’t been an uptick in expectations for future inflation from consumers.

The Closer — Delivery Times Rising — 2/15/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at rising delivery times, and underwhelming industrial production report, and strong producer price inflation.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

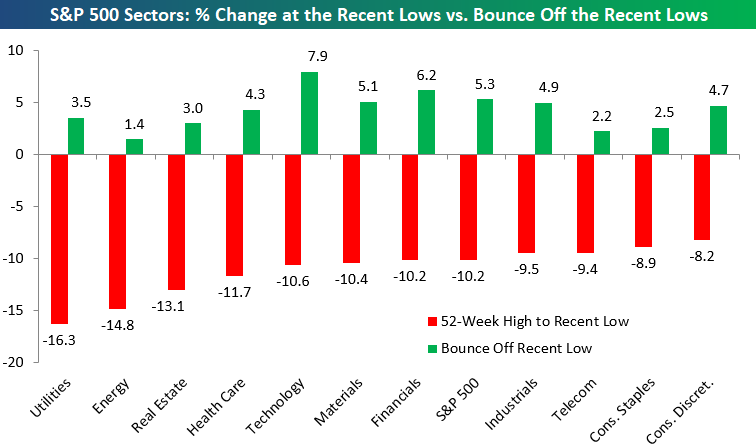

Bespoke’s Sector Snapshot — 2/15/18

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a two-week free trial to Bespoke Premium now.

Below is one of the many charts included in this week’s Sector Snapshot, which highlights how much each S&P 500 sector fell from its 52-week highs to its recent low as well as how much each sector has now rallied off of its low. As you can see, Tech has bounced the most off of its low, followed by Financials and then Materials. Energy has struggled the most. It had been down 14.8% from its 52-week high, but it’s only up 1.4% off of its low.

To see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

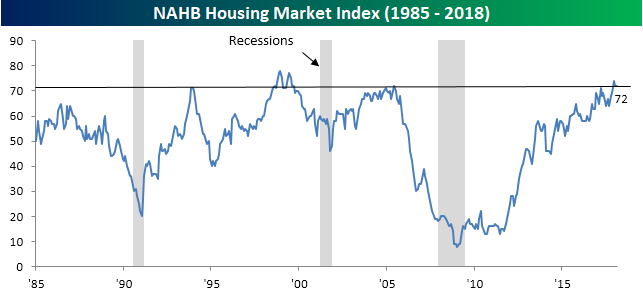

Homebuilder Sentiment Remains Optimistic

Homebuilder sentiment for the month of February came in right in line with expectations today and remains right near its highest levels of the expansion. At a current level of 72, sentiment has only been at more optimistic levels a handful of times. In fact, during the years of the housing bubble in the early 2000s, homebuilder sentiment was never higher.

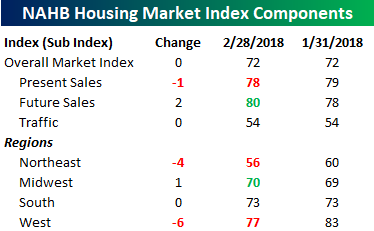

Below we show the breakdown of this month’s report by traffic, sales, and region. As far as traffic and sales is concerned, there wasn’t much in the way of big moves, although Future Sales has only been higher in one other period (the late 1990s). Regionally, sentiment in the Northeast and West saw moderate declines, while the Midwest and South (where property and local taxes are relatively low) was unchanged. This is a trend to watch going forward.

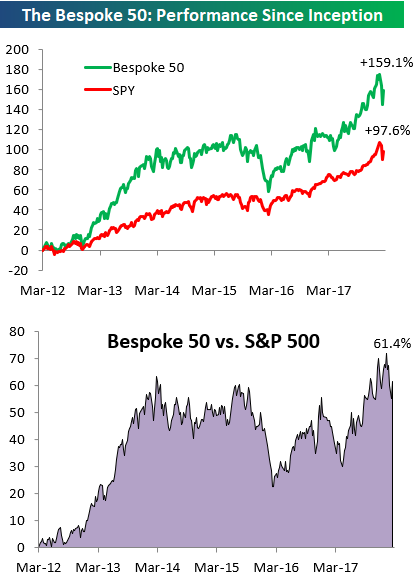

the Bespoke 50 — 2/15/18

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 61.4 percentage points. Through today, the “Bespoke 50” is up 159.1% since inception versus the S&P 500’s gain of 97.6%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

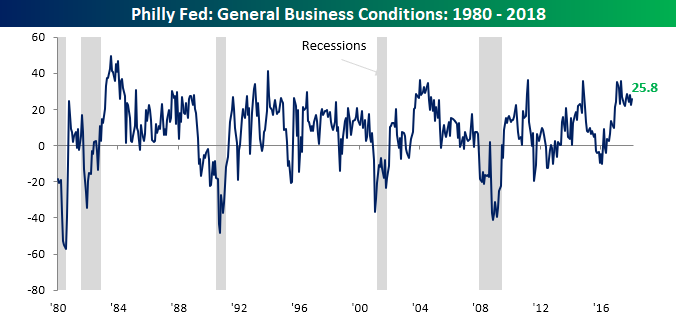

Philly Fed Surpasses Expectations

While the Empire Manufacturing report (released earlier) disappointed relative to consensus forecasts, the February Philly Fed report beat expectations, coming in at a level of 25.8 compared to January’s reading of 22.8. At 21 months and counting, the Philly Fed is currently in its longest streak of positive readings since August 2015. More impressively, though, the last 15 months have seen readings in excess of 20. The only other period in the history of the report (since 1980) that saw as many or more monthly readings above 20 was in the 17-month stretch ending in June 1984!

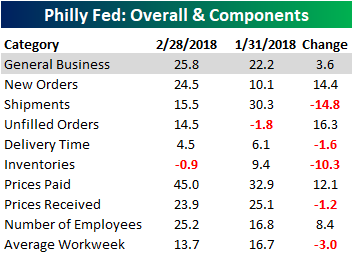

The table below shows the internals of this month’s report, which were mixed. While New Orders surged, Shipments dropped sharply. On the inflation front, Prices Paid saw the third largest increase of any component and is now at its highest levels since 2011 (chart below).

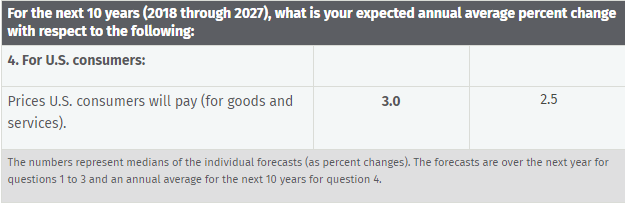

Finally, with respect to prices, one special question asked of respondents in this month’s report had to do with what the expected annual average percent change in prices will be for US consumers over the next ten years. As shown in the graphic below, respondents expect prices to rise by an average of 3% per year for the next ten years, which is up from 2.5% in November. Here again, we have another sign of inflation creeping into the picture.

Chart of the Day: Not The Same Old USD

Empire Manufacturing Report Disappoints

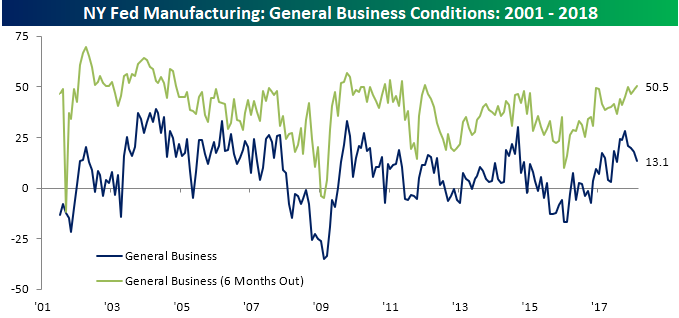

This morning’s report on manufacturing activity in the New York area provides one of the first reads on how business activity is trending for the month of February, and the results were a bit weaker than expected. While economists were expecting the headline General Business Conditions index for the month of February to increase slightly from last month’s reading of 17.7, the actual reading missed to the downside coming in at 13.1. While the current conditions index (dark blue line) declined for the fourth straight month, the index for expected conditions six-months out rose for the fourth time in five months, hitting its highest level since January 2012. Eventually, this divergence has to resolve itself; the only question is in which direction that happens.

The table below breaks down this month’s report by each of its sub-sectors. In terms of current conditions, despite the decline in the headline index, most of the components actually increased this month. Conversely, while the index of General Business conditions for six months out increased, most of the subcomponents declined.

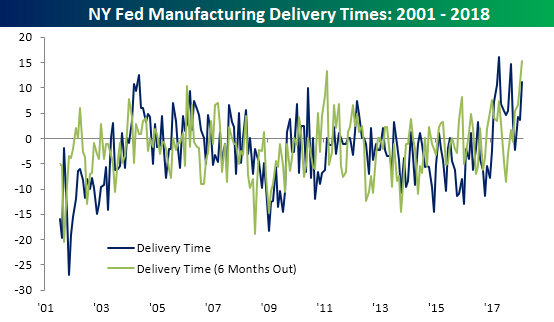

With all the focus on inflation recently, we wanted to highlight a few of the components in this month’s report that could impact prices. The first is Delivery Times. While the current conditions index is well off its recent highs, the index for six months out rose to its highest level in the history of the survey. Extended delivery times can often be a sign of supply problems which can have inflationary implications down the line.

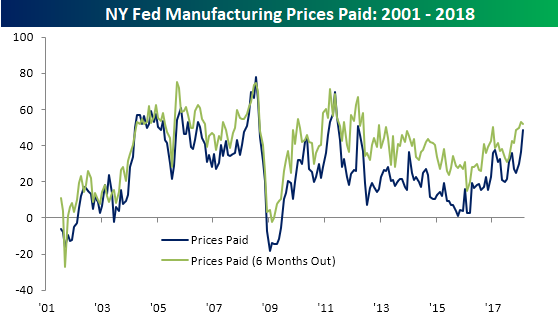

The Prices Paid components of this month’s report also remain elevated with the current conditions index at its highest level since mid-2012.

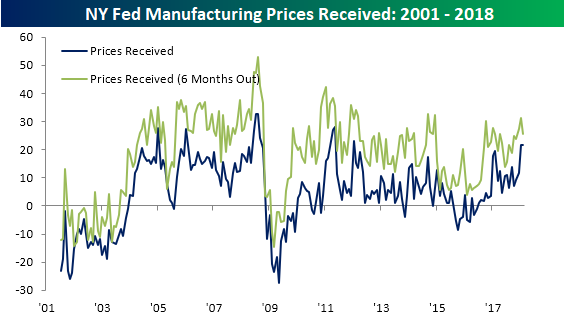

Similarly, Prices Received is also elevated as the current conditions component remains right near its highest level since mid-2012 as well. Based on trends in Prices Received as well as the indicators above, it doesn’t appear as though any upward pressure in prices is going to abate any time soon.

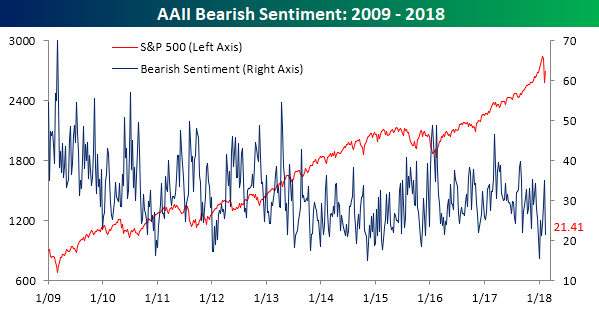

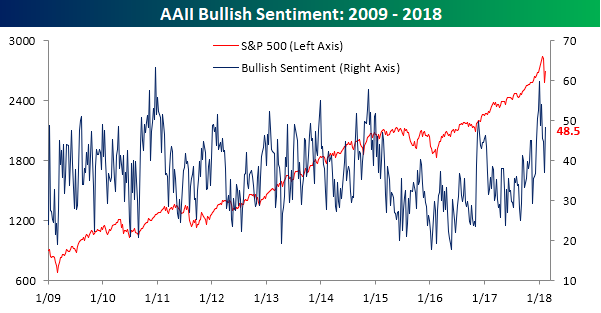

Bulls Back on the Charge

For years we’ve seen a trend where anytime the S&P 500 saw a pullback, any bulls in the weekly AAII sentiment poll would run for the exits and stay there until all signs pointed to an all clear. Earlier this year, we saw bullish sentiment surge to some of the highest levels of the bull market right before the market peaked. Then, when stocks pulled back, so too did bullish sentiment. Heading into this week’s poll results, we expected that bullish sentiment would remain subdued given the volatility in equities. What we saw, though, is that bulls have come charging back! In this week’s survey, bullish sentiment increased from 37.0% up to 48.5% for a gain of 11.5 percentage points. That’s the largest weekly increase since last September. It’s nice to see that investors are finally starting to get comfortable with equities. The time to worry, though, is when that comfort turns into complacency.

As you might expect given the surge in bullish sentiment, bearish sentiment plunged from 35.0% down to 21.4%. That’s the largest weekly decline in two years!