The Closer — North America In Focus: Banxico, US Import Prices, Canada Housing — 4/12/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review the Banxico policy decision, US import and export prices, soybean export data, and Canadian home prices.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

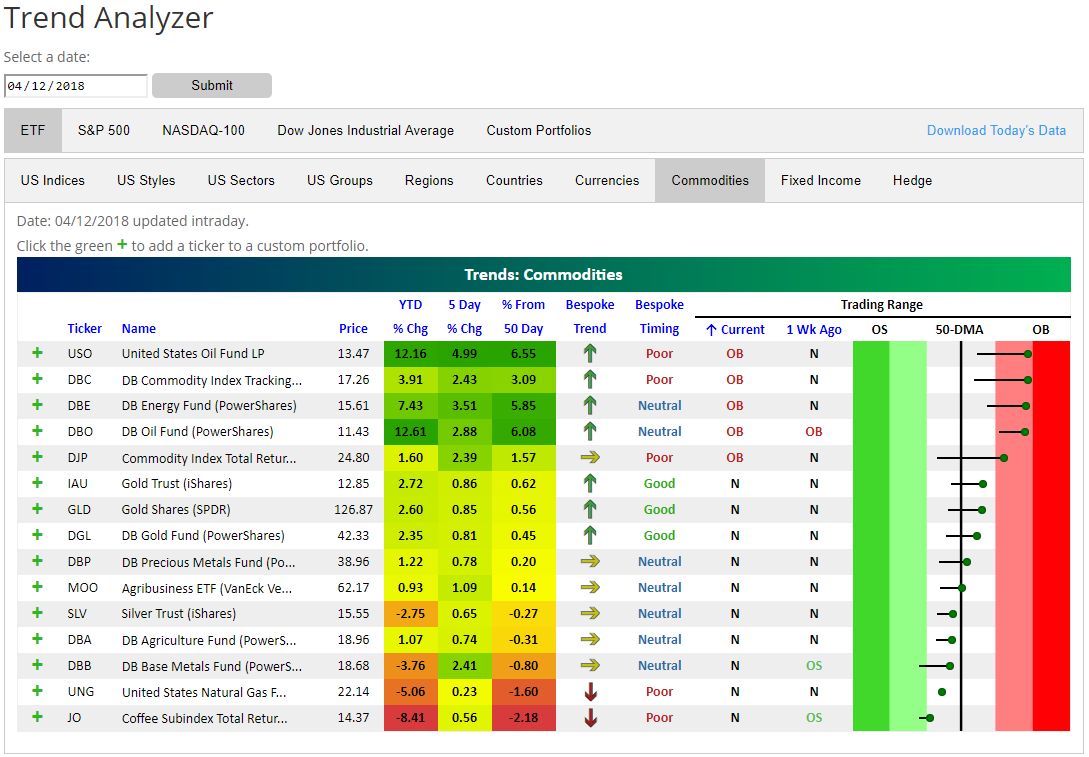

Commodities ETFs Surge

Commodities ETFs have been on a tear lately. Below is a snapshot from our Trend Analyzer tool. For each ETF, the dot in the trading range section represents where it’s currently trading within its range, while the tail end represents where it was trading one week ago. As shown, a number of commodities ETFs have now moved up into overbought territory, with USO (oil) and DBC (broad commodities) the most overbought.

While some commodities ETFs remain below their 50-day moving averages, they’re all up over the last week. Year-to-date, oil is up the most with a gain of 12%, while coffee (JO) is down the most at 8.4%.

Our Trend Analyzer tool lets you monitor trend and timing measures for all US stocks and major ETFs across asset classes. It’s accessible via a Bespoke Premium or Bespoke Institutional membership.

After viewing general trend and timing measures for commodities ETFs in our Trend Analyzer, we can dive deeper by viewing price charts of them in our popular Chart Scanner tool. Our Chart Scanner lets users browse through charts across asset classes quickly and easily. When you see a chart you like, click on it once to tag it as bullish. When you see a chart you don’t like, simply click on it twice to tag it as bearish. Below is a snapshot of nine commodities ETFs taken from our Chart Scanner. We’ve marked a few commodities ETFs as bullish because they’ve recently broken out to new one-year highs. The three that are marked are DBC, DBE, and DBO. If you had done this in our Chart Scanner, these three charts would now show up in your “Bullish” section under the “My Charts” tab.

To start tagging bullish and bearish charts in our Chart Scanner, simply sign up for a two-week free trial to Bespoke Premium. You’ll love this new feature!

Bespoke’s Sector Snapshot — 4/12/18

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a two-week free trial to Bespoke Premium now.

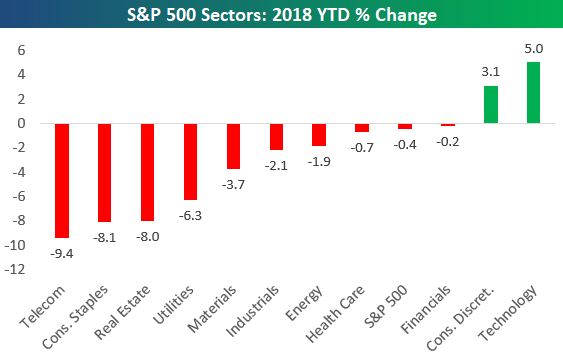

Below is one of the many charts included in this week’s Sector Snapshot, which highlights the year-to-date percentage change for the S&P 500 and its eleven sectors. As shown, the S&P is just barely in the red, but there are way more negative sectors than positive ones, which is indicative of weak breadth.

To find out what this means and to see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

Lots of Noise, Little Headway

Despite massive volatility on a day to day basis, it may sound hard to believe, but the S&P 500 is currently trading right where it was nearly two months ago on February 13th. You read that right, in what has been the most volatile market environment in at least a couple of years, the S&P 500 has nothing to show for it – up or down! In terms of individual sectors, we’ve seen some rotation. While Technology continues to be a market leader, it has been joined by former laggards like the Energy (+5.1%) and Utilities (0.5%) sectors to the upside. On the downside, Telecom Services, Consumer Staples, and Materials are all down over 2%, while Industrials, Financials, and Consumer Discretionary are down a percent.

As far as individual stocks are concerned, 250 stocks are up and 250 stocks are down, so it couldn’t be more balanced. While a total of 43 stocks in the S&P 500 are up over 10% over the last 2 months, in the interest of space, the table below lists the twenty top performers. As you might expect given the sector’s leadership, a number of stocks from the Energy sector make up the list with Hess (HES), Noble Energy (NBL), Baker Hughes/GE (BHGE), and National Oilwell (NOV) all up over 20%. The top-performing stocks, however, have been Nektar (NKTR), XL Group (XL), and Chipotle (CMG), with each gaining close to or more than 30%. FAANG stocks had a good start to the year, but the only one that has been able to keep the momentum going is Netflix (NFLX), which is up nearly 20%.

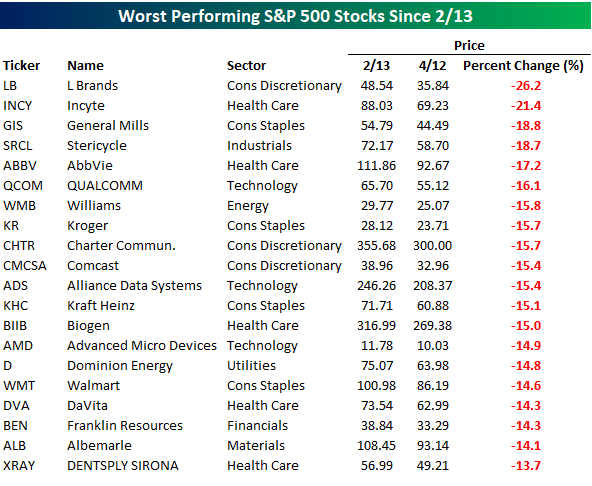

While 43 stocks in the S&P 500 are up over 10% since 2/13, 37 stocks are down 10%+, and in the table below, we list the worst 20. As shown, just two of the worst performing stocks are down over 20% since February 13th, which is actually pretty surprising to us given the volatility. Those two stocks are L Brands (LB) and Incyte (INCY). Looking through the list of losers, though, there are a number of blue-chip stocks such as General Mills (GIS), QUALCOMM (QCOM), Comcast (CMCSA), Kraft Heinz (KHC), Biogen (BIIB), and Walmart (WMT).

the Bespoke 50 — 4/12/18

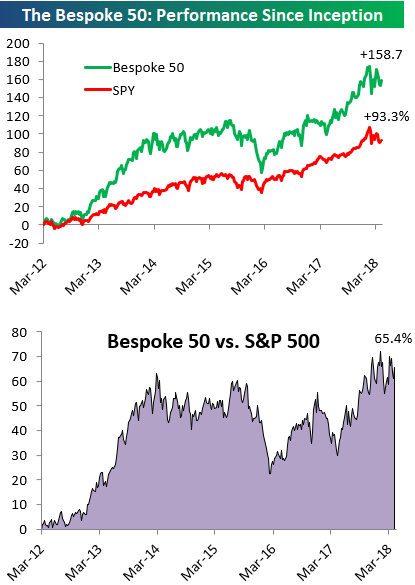

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 65.4 percentage points. Through today, the “Bespoke 50” is up 158.7% since inception versus the S&P 500’s gain of 93.3%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

Chart of the Day: Vacation All I Ever Wanted

Individual Investors Bail

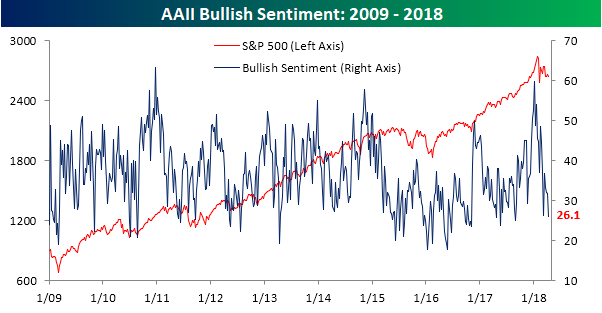

2018 hasn’t been the year for the little guy. Late last year, individual investors appeared to be finally getting comfortable with stocks as bullish sentiment in the weekly poll from AAII topped 50% for the first time in nearly three years. For a little while, they enjoyed the ride as equities surged to start the year and bullish sentiment reached just shy of 60%. Then the correction came. Since then, the bulls have been in steady retreat as increased volatility and lower prices remind these individuals why they were so apprehensive in the first place. This week provided a further confirmation of that trend as bullish sentiment in the weekly AAII poll dropped from 31.9% down to 26.09%. This marked the fourth straight week of declining bullish sentiment and took the percentage of bulls to the lowest level since last August.

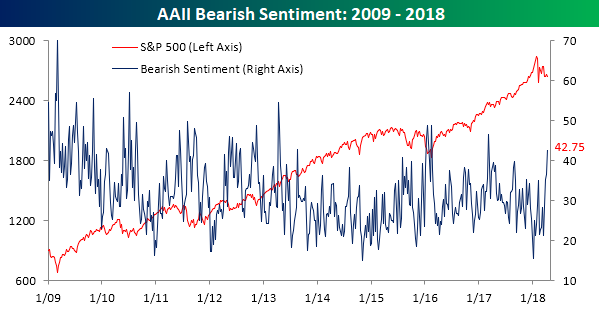

The investors leaving the bullish camp recently aren’t just moving to the neutral sidelines either. They are flat out bearish. In this week’s survey, bearish sentiment surged from 36.6% up to 42.75%. Bearish sentiment has now increased by more than 20 percentage points in the last four weeks and is at its highest level since last March.

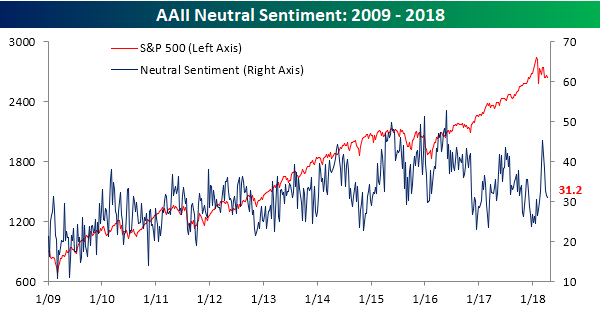

Fence sitters have plummetted in recent weeks as well, so it’s not as though investors don’t have conviction. After hitting a recent high of over 45% in early March, neutral sentiment is now down to 31.2%.

A Record Streak in Jobless Claims

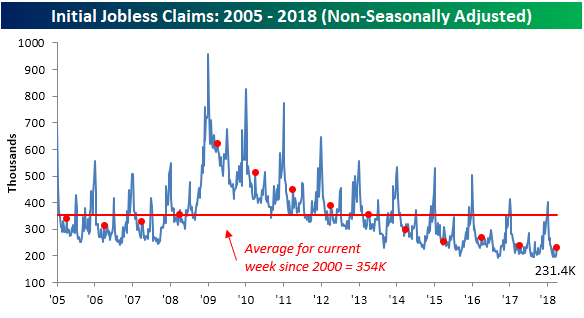

Jobless claims came in higher than expected for the second time in a row this week, but the report was still monumental from a historical perspective. While economists were forecasting first time claims to fall to 230K from last week’s higher than expected level of 242K, the actual reading came in at 233K. This week’s print now makes it 162 straight weeks where claims have come in below 300K, surpassing the previous record streak of 161 weeks that ended in April 1970. Given the fact that claims are currently still well below 300K, this could be a streak that lasts for some time.

With claims coming in at over 240K last week and above 230K this week, the four-week moving average has been drifting higher. This week’s reading came in at 230K, which is more than 7K above the multi-decade low of 222.75K that we hit five weeks ago. The way the last two prints have come in, it could be some time before we get back to those previous lows again if we get there at all.

On a non-seasonally adjusted basis, claims came in at 231.4K. While that’s up from last week’s level of 201K, it is still more than 120K below the average for the current week of the year dating back to 2000. In fact, the last time claims were lower for the current week of the year was back in 1969.

The Closer — Minute Musings, Punchy Prices, Crude Data, & Social Capital — 4/11/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we recap FOMC meeting minutes, review CPI inflation data, update tracking of monthly freight price changes, discuss weekly EIA petroleum market data and energy market price action, and analyze what social capital means for economic outcomes across states.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!