Bespoke’s Global Macro Dashboard — 3/14/18

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

The Closer — Inflation, Poloz — 3/13/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review today’s CPI report from the BLS. We also discuss the dovish Poloz speech today and the outlook for USDCAD.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

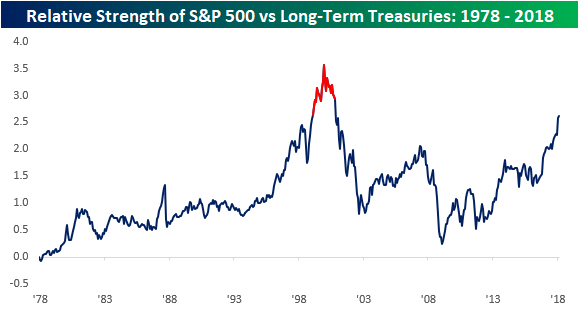

Stocks Leave Bonds in the Dust

With investors celebrating the nine-year anniversary of the financial crisis low last week, it should surprise no one that equities have been outperforming long-term treasuries over the last several years. What will likely surprise a lot of people is by just how much equities have been outperforming. The chart below shows the relative strength on a total return basis of stocks (S&P 500) vs bonds (Merrill Lynch 10+ Year US Treasury Index) going back to the start of 1978. In the chart, a rising line indicates that equities are outperforming bonds and vice versa.

Since the middle of 2016, the relative strength of the S&P 500 has gone practically parabolic as equities have surged and interest rates have risen. Equities are outperforming by such a wide margin right now that there have only been 21 other months going back to 1978 where the performance disparity was wider than it is now, and all of those months were in the period from February 1999 through October 2000. Back in 2000, once that period of equity outperformance came to an end, Treasuries consistently outperformed equities for ten years right through to February 2009. Since then, it’s been a nine year run for equities, with little in the way of looking back.

B.I.G. Tips – CAT Nap

Bespoke Stock Scores — 3/13/18

Chart of the Day: No IPO Flow

Whiskey Wanters Win

This morning’s CPI report for the month of February from the BLS was altogether unexciting, with core CPI rising 0.2% MoM as expected. While the report was pretty boring generally speaking, it contained some excellent news for whiskey drinkers.

As shown below, from 2002 to 2015 the price of whiskey rose ever higher relative to other spirits. Unfortunately for the curious, there are no separate series for other liquor cabinet staples like vodka, gin, or rum. Instead, we have to see their aggregate price under the “other distilled spirits” category. But recently, increased supply from new US distillers has driven much stronger competition. The result? Whiskey has cheapened up relative to other spirits. With long lead times for aging, fickle consumer tastes, and high relative prices to consider, US whiskey drinkers are likely to get further reprieves in the year ahead.

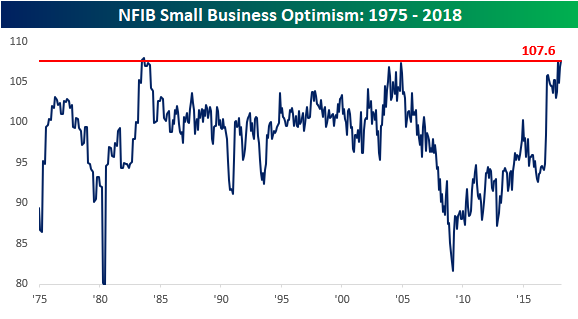

NFIB Small Business Optimism Hits a 34 Year High

Say what you want about the pace of economic growth, but most small business owners are downright giddy and the most confident they have been in their careers. The latest evidence is the monthly sentiment survey of small businesses from the NFIB. In this month’s report, the headline index came in higher than expected, rising from 106.9 to 107.6 versus expectations for an increase to 107.1. The last time the index was this high was in September 1983, and in the history of the survey, the index has only been higher twice. Check out the long-term chart below. In 1983, there were two months where the index exceeded this month’s reading, and in 2004 it got close to current levels but came up just short.

From a shorter-term perspective, this month’s increase to new multi-decade highs continues the surge that began in November 2016 and puts the current reading a full ten percentage points above its historical average dating back to 2000.

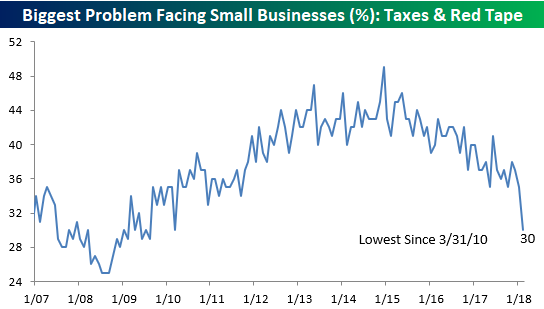

When President Trump campaigned, he ran on a platform of reducing the regulatory and tax burden for American businesses. Based on the trends we have seen from the monthly Small Business Optimism report since he was elected, his actions have certainly had an impact. Take the “most important problem” question in each month’s report. Back in October 2016, before President Trump was elected, a combined 42% of small businesses cited either Taxes or Government Regulation as their biggest problem, and the two were tied for the lead as being cited by the largest percentage of businesses. In the most recent report, the combined reading of these two problems is just 30%, which is the lowest in eight years!

The table below lists the percentage of small businesses that cited each of the problems below as their most important problem. This month, Quality of Labor leads the list at 22%, while Taxes and Red Tape are tied at 15%. The labor quality issue has been a concern for the market since it might have an inflationary impact as employers are forced to pay up for higher quality workers. This month, though, both “Quality of Labor” and “Cost of Labor” were flat month-over-month, which should soothe the market a bit.

The Closer — Rates Positioning, Flatter Labor Markets, Inflation Expectations — 3/12/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we dive deep into rates futures positioning. We also take a look at inflation expectations and some very long-term trends in the labor market.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!