The Closer: End of Week Charts — 4/27/18

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We’ve recently added a section that helps break down momentum in developed market foreign exchange crosses as well.

Below is a snapshot from today’s Closer highlighting weekly intraday price charts for major equity indices and other asset classes. If you’d like to see more, start a free trial below.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

Traders Unload Tech, Industrials…Buy Health Care, Utes, and REITs

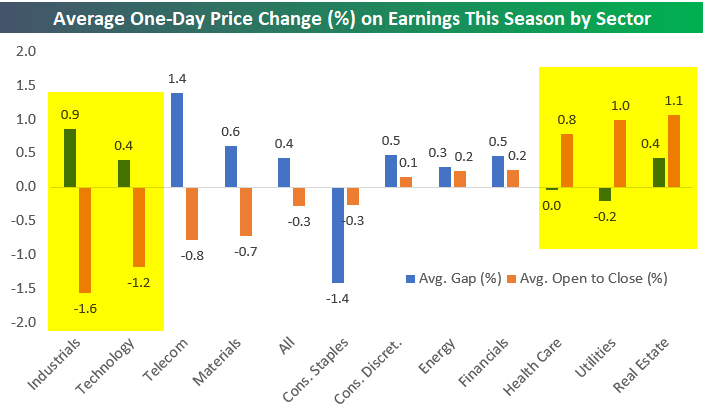

This earnings season has been very strong by almost every measure when it comes to the numbers coming out of corporate America. But as investors know, the ultimate gauge is how stock prices react to earnings reports.

In general, what we’ve seen this earnings season is an initial positive stock price reaction to the news followed by a large wave of selling throughout the trading day.

We measure the one-day stock price change in reaction to earnings for every company that reports quarterly numbers. We also break that one-day price change into two parts — the initial gap that share prices experience when they open for trading following their earnings report and the change from that gap at the open of trading through the close of trading that day (open to close % change).

Below we show how much the average stock that has reported earnings this season has gapped up or down at the open by sector. We also show how much the average stock that has reported has moved from the open to the close of trading.

For all stocks that have reported earnings this season, the average move has been a gap up of 0.40% at the open followed by decline of 0.30% from the open to the close. This means investors are initially bidding shares up on earnings before sellers come in during the trading day.

A few sectors stand out. First off, both Industrials and Technology have seen shares bid up at the open on earnings optimism, but they’ve sold off hard throughout the trading day. The average Industrial stock has gapped up 0.90% at the open following earnings only to sell off 1.60% from the open to the close. For Tech stocks that have reported, they have averaged a gap up of 0.40% and then an open to close decline of 1.20%. For these two sectors, positive earnings news appears to have already been priced in.

Other sectors have seen their stock prices do well this earnings season. Consumer Discretionary, Energy, and Financials have all seen initial gaps higher and continued buying throughout the trading day. Health Care, Utilities, and Real Estate (REITs) have seen a wave of buyers come in during regular trading hours. Utilities and Real Estate stocks that have reported have averaged gains of more than 1% from the open to the close. We don’t view shifts out of Tech and Industrials and into Utilities and Real Estate as a very bullish signal.

For more earnings season analysis, start a two-week free trial to any one of our three membership levels.

Wages Accelerate

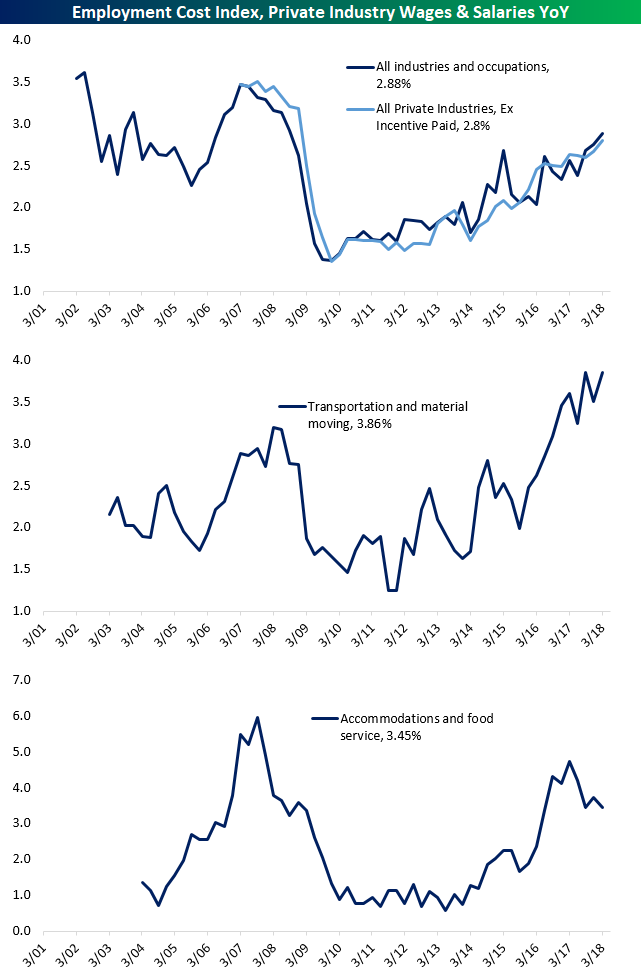

Today the BLS updated its broadest (and most useful) measure of wage growth, the quarterly employment cost index. This measure takes into account changing composition of aggregate employment and other factors that can tend to skew average hourly earnings up or down. It comes in three flavors: wages and salaries only, benefits only, and total compensation (total compensation and wages and salaries combined). Wages and salaries only are the best cash wage growth measure. The news was good. As shown in the chart below, the ECI of wages & salaries only (excluding benefits) for all private industries accelerated to the fastest YoY pace of the current economic expansion. Even after stripping out volatile incentive-paid occupations, wages keep moving higher on a YoY basis. We also chart a couple of specific industries’ ECI wages and salaries numbers. While truckers are getting huge wage bumps, a big uptick in wage growth for the hospitality sector is working itself off.

Below we show a table summarizing ECI wages and salaries growth by occupation and industry. As shown, while wage growth is varied across the different occupations and industries, QoQ annualized growth is almost always stronger than YoY growth, itself stronger than 5 year annualized growth. While Q1 was a particularly strong quarter, and likely represents much stronger wage growth than the current trend or sustainable pace, it’s very clear that wage growth is accelerating broadly and is likely to continue doing so.

Q1 GDP Slows, But Beats Expectations

Analysts were forecasting a significant weakening of GDP in Q1 versus a solid pace in Q4, and they got it, but not to the degree they expected. Real gross domestic product rose 2.32% annualized in the first three months of 2018, the slowest pace since Q1 of 2017. That was still stronger than the 2.0% forecast by economists. Notably, that was the first beat for a Q1 GDP print in almost a decade…the last time analysts undershot the start of the year was Q1 2008.

As shown in the chart above, the deceleration in output was mostly a function of consumption. As shown in the chart, consumer spending rose over 4% in real terms in Q4 at an annual pace. That was the strongest pace since Q4 2014, when consumer outlays rose at a 5% annual rate. Nonresidential fixed investment (business capital expenditures) continues to run at a robust pace over 6% annualized. While that pace is strong, it’s interesting to note that 3 of the prior 4 quarters were stronger.

Given typical weakness in Q1 and the lumpy consumer spending numbers, this GDP report ended up pretty well all things considered. We should also emphasize that the first reading of GDP is always the least accurate, so revisions are worth keeping an eye on.

The Closer — US Data Discussion, EM Getting Cheap — 4/26/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review US data released today: homeownership & vacancy, advance goods trade data, preliminary durable goods manufacturing data, Mexican labor markets, and Brazilian loan growth. We also review high carry EM currrencies with brutal charts.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bespoke’s Sector Snapshot — 4/26/18

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a two-week free trial to Bespoke Premium now.

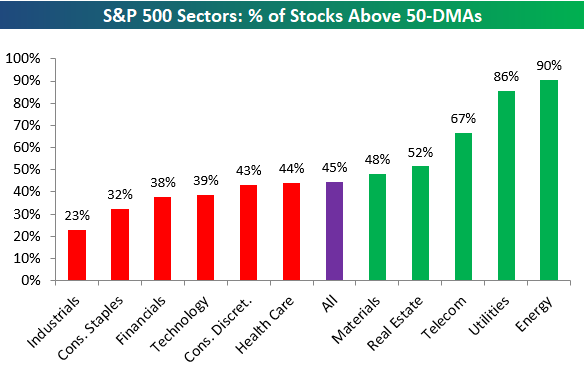

Below is one of the many charts included in this week’s Sector Snapshot, which highlights the percentage of stocks in each S&P 500 sector that are trading above their 50-day moving averages. As shown, breadth for the S&P 500 remains below 50% with 45% of stocks in the index currently above their 50-DMAs. Unfortunately, the key cyclical sectors of the market like Industrials, Consumer Discretionary, Technology, and Financials all have readings below 45%.

To find out what this means and to see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

B.I.G. Tips – Most “Dismally” Forecast Economic Report Ever?

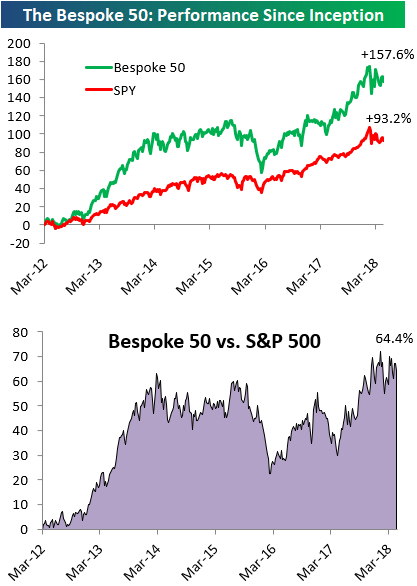

the Bespoke 50 — 4/26/18

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 64.4 percentage points. Through today, the “Bespoke 50” is up 157.6% since inception versus the S&P 500’s gain of 93.2%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

Chart of the Day: Capex Activity Likely Peaked

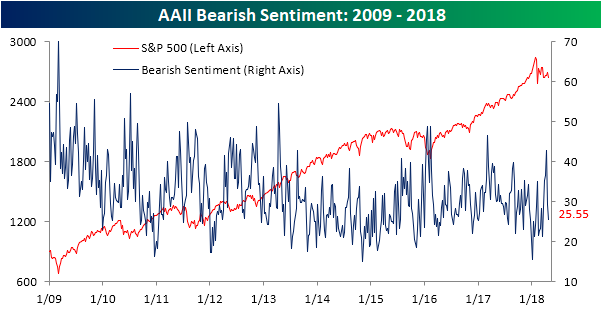

Bearish Sentiment Drops Again

Despite the weak performance for equities over the last week, individual investor sentiment didn’t show any spike in negative sentiment this week. According to the weekly sentiment survey from AAII, bullish sentiment dropped less than one percentage point falling from 37.78% down to 36.91%.

While bullish sentiment barely budged, bearish sentiment saw a relatively large decline, falling from 29.22% down to 25.55%. That decline of nearly four percentage points follows a drop of nearly 14 percentage points last week, making it the largest two-week decline in bearish sentiment since last September.