Bespoke Consumer Pulse Report — May 2018

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the sustainability of economic growth in the US. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Bespoke’s Sector Snapshot — 5/3/18

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a two-week free trial to Bespoke Premium now.

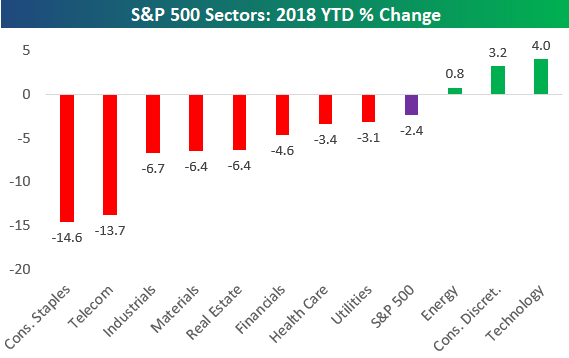

Below is one of the many charts included in this week’s Sector Snapshot, which highlights the year-to-date percentage change of the eleven S&P 500 sectors. At this point, just three sectors are still in positive territory, while eight are in the red. Consumer Staples and Telecom are down the most with declines of more than 13%.

To find out what this means and to see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

April Employment Report Preview

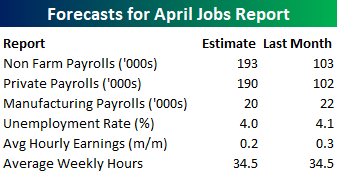

Heading into Friday’s Non Farm Payrolls (NFP) report for April, economists are expecting an increase in payrolls of 193K, which would be a big improvement from March’s dismal reading of 103K, in what was the biggest NFP miss relative to expectations since the September 2017 report. In the private sector, economists are also expecting a similar increase of 190K. With these increases, the unemployment rate is expected to fall to 4.0%. The big area of focus, however, will come from average hourly earnings. With so much concern around inflation, any stronger than expected reading in wage measures will be a negative for the market.

Ahead of the report, we just published our eleven-page preview of the April jobs report. This report contains a ton of analysis related to how the equity market has historically reacted to the monthly jobs report, as well as how secondary employment-related indicators we track looked in April. We also include a breakdown of how the initial reading for April typically comes in relative to expectations and how that ranks versus other months.

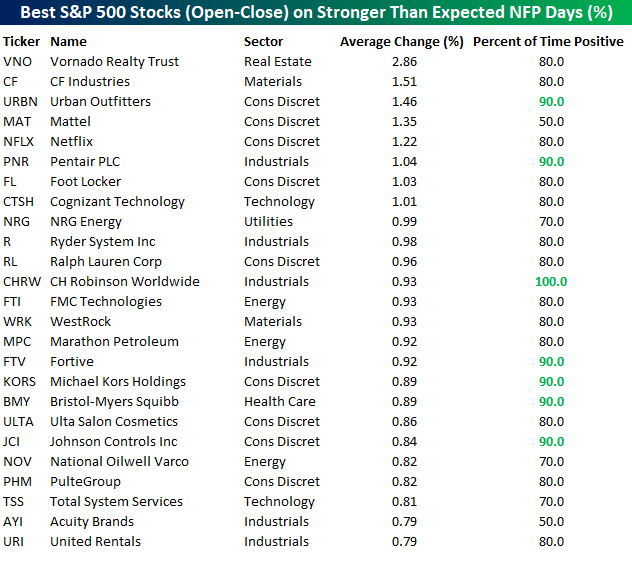

One topic we cover in each month’s report is the S&P 500 stocks that do best and worst from the open to close on the day of the employment report based on whether or not the report comes in stronger or weaker than expected. In other words, which stocks should you buy, and which should you avoid? The table below highlights the best-performing stocks in the S&P 500 from the open to close on days when the Non-Farm Payrolls report has been better than expected over the last two years.

Of the 25 top performing stocks on days when the NFP beats expectations, eight sectors are represented, and Consumer Discretionary leads the way with nine. Vornado (VNO) has been the best performing stock with an average open to close gain of 2.86%. In terms of consistency, CH Robinson (CHRW) has been up every time, while another six stocks have been positive nine out of ten times.

For anyone with more than a passing interest in how equities are impacted by economic data, this report is a must-read. To see the report, sign up for a monthly Bespoke Premium membership now!

April 2018 Headlines

ISM Services Also Disappoints

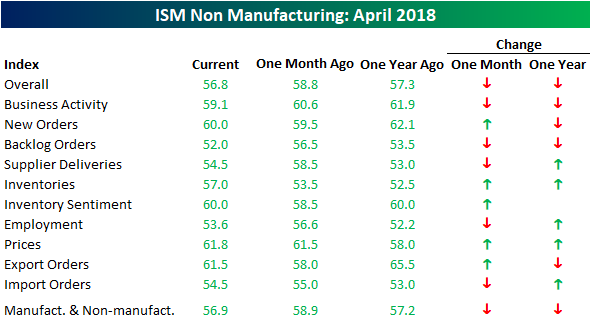

Just like its counterpart that covers the Manufacturing sector, the ISM Services report for April declined this month and came in lower than expected. While economists were expecting the headline index to come in at a level of 58.0, the actual reading was notably weaker at 56.8. While both indices have declined, the magnitude of the drop in the Services sector hasn’t been quite as large.

On a combined basis and accounting for each sector’s share of the overall economy, our composite ISM for April came in at 56.9, which is pretty much in the range of levels we have seen over the last few months. The general takeaway from these reports is the same as we have seen in much of the recent economic data — upside momentum has slowed, but from levels that were very positive to begin with.

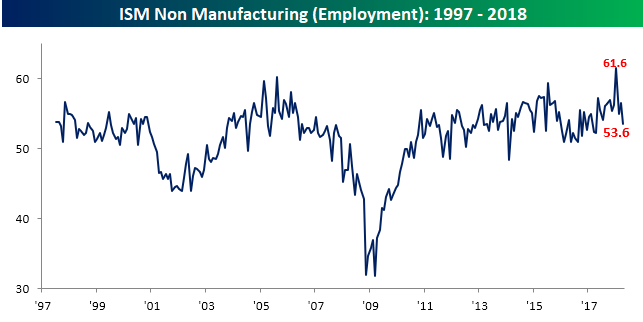

The table below breaks down this month’s report by each of its individual components. Breadth in this month’s report was pretty much neutral on both a m/m and y/y basis. The increases relative to March readings were Inventories and Export Orders, while Backlog Orders and Supplier Deliveries saw the largest declines. Given the fact that the March Non Farm Payrolls report will be released on Friday, we would also note that the Employment component saw a pretty large drop this month and is down sharply from its recent peak in January (chart below).

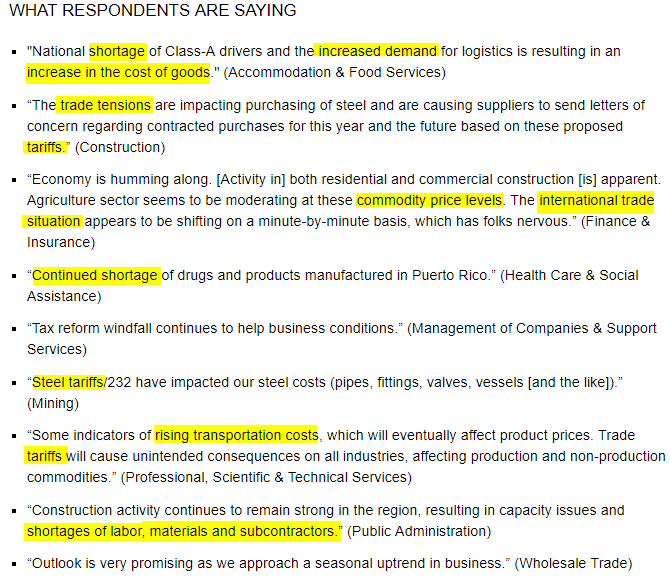

Finally, with all the concerns regarding inflation, we would note that like the commentary in the ISM Manufacturing report, the commentary in the ISM Services report also made many mentions of factors that are having upward pressure on prices. Issues like shortages, strong demand, trade tensions, and rising costs are all ultimately inflationary even if the details of this month’s report like the Prices Paid component didn’t see large increases.

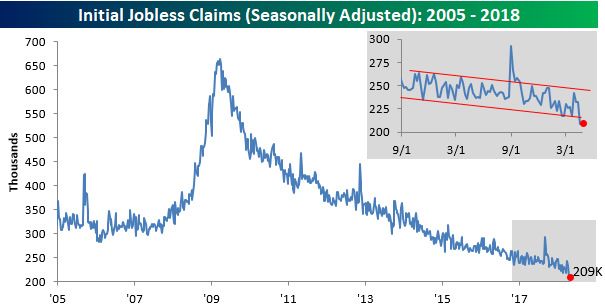

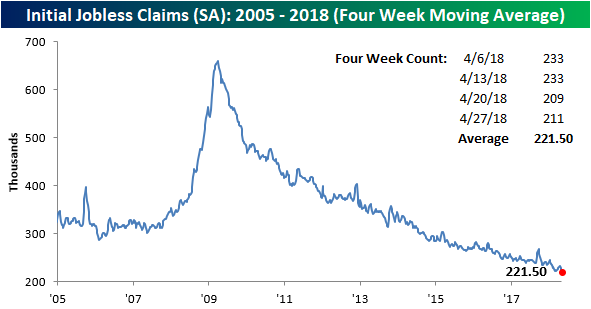

Jobless Claims: How Low Can They Go?

In last week’s update on weekly jobless claims, we described the trend in claims as “doing the limbo.” Taking the analogy one step further, this week we ask, “How low can they go?” First-time jobless claims came in at 211K this week versus estimates for a level of 225K. Last week’s print of 209K was the lowest weekly reading since 1969, and this week is the second lowest! With another week of sub-300K readings, the record streak has been extended to 165, while the streak of sub 250K readings is now up to 24, which is the longest since 1973.

With the second straight week of sub-225K readings, the four-week moving average also made a new low this week falling from 229.25K down to 221.5K. The last time the four-week moving average was this low was back in 1973. Barring a pretty big uptick in weekly claims next week, the four-week moving average should drop again, likely bringing it down to its lowest level since 1969.

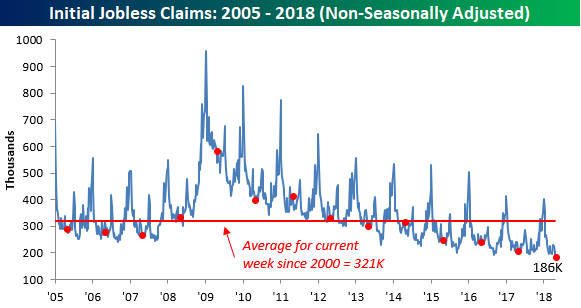

On a non-seasonally adjusted basis, jobless claims also fell back below 200K to 186K. For the current week of the year, that was the lowest print since 1969, and 135K below the average reading for the current week of the year dating back to 2000.

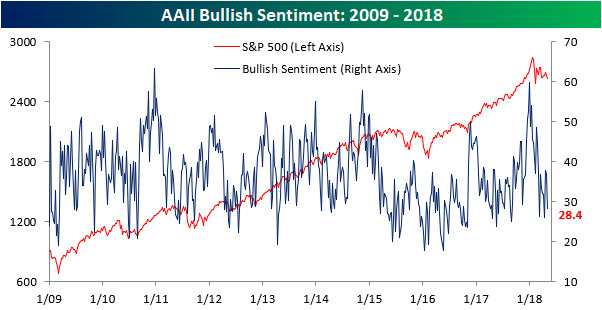

Bulls Back in Retreat Mode

With the S&P 500 down in two of the last three days, investors are once again on the defensive causing bullish sentiment to retreat. According to this week’s sentiment survey from AAII, bullish sentiment declined from 36.91% down to 28.4%. While anything sub-30% is considered low, we actually saw a lower weekly print back in the first half of April when bullish sentiment dropped down to 26.09%. One trend that is emerging in bullish sentiment, though, is just like the trend of the overall market – lower highs. Since peaking at close to 60% earlier this year, we have seen a steady downtrend emerge in sentiment where each week that has an increase is followed by another week(s) with bigger declines.

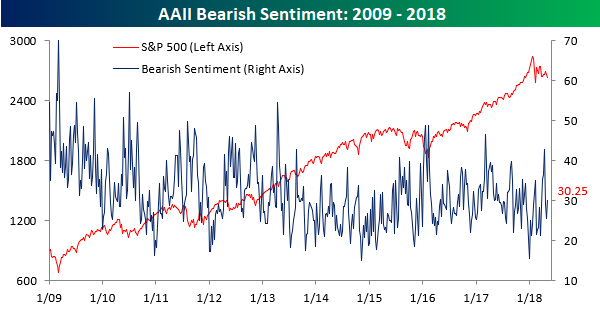

Not all the investors that left the bullish bandwagon this week went bearish. While bullish sentiment declined over 8 percentage points, bearish sentiment increased by less than 5 points. At the current level of 30.25%, it is nowhere near its recent high of over 40%.

Neutral sentiment, on the other hand, is getting back up near its highs and is back above 40%, indicating that a lot of investors simply don’t know what to make of this market.

the Bespoke 50 — 5/3/18

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 69.5 percentage points. Through today, the “Bespoke 50” is up 161.2% since inception versus the S&P 500’s gain of 91.6%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

The Closer — Fed, Energy, ARS — 5/2/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we recap the FOMC’s policy statement from this afternoon, also discussing energy markets and the nosedive the Argentinian peso has taken.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Industrials, Technology Beating Earnings at the Highest Rate

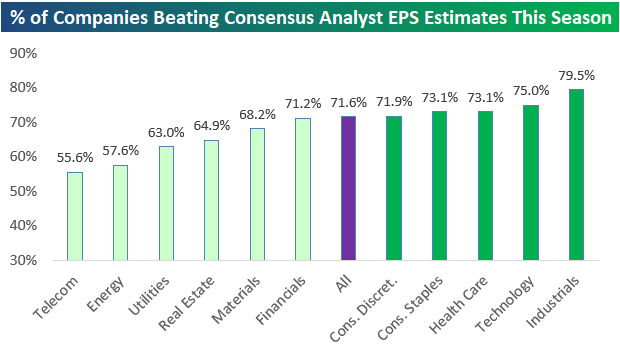

As highlighted in our prior post, the percentage of companies that have beaten consensus analyst EPS estimates this season stands at 71.6%. Any reading over 70% is very strong relative to past earnings seasons.

Below we take the beat rate analysis a step further and look at sector beat rates this season. As shown, five sectors have beat rates that are stronger than the overall market, while six sectors have weaker beat rates.

The Industrials sector is the standout with a beat rate of 79.5% this season. Technology ranks second at 75%, followed by Health Care and Consumer Staples at 73.1%.

On the weak side, Telecom and Energy both have earnings beat rates below 60%, while Utilities and Real Estate are below 65%.

We’ll be back to post an update on these readings at the end of earnings season in mid-May.