The Closer — Construction Revised, Industrial Production Rises, Crude Flows — 5/16/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review monthly residential construction numbers including benchmark revisions to historical numbers. We also review industrial production and petroleum market data.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

General Electric (GE): Selling Low?

It’s hard to imagine a stock more out of favor these days than General Electric (GE). After a 44% decline last year, investors have been running from the stock like the plague. As a perfect example, this week marked the deadline for institutional investors to file their quarterly holdings report (13F). Based on an analysis from Bloomberg, institutional investors sold more than 126 million GE shares during the first quarter. Besides the fact that no other stock in the Industrials sector saw total sales of this magnitude during Q1, this quarter’s institutional investor outflows from GE reversed a string of three straight quarters where institutions were net buyers. In other words, while the stock was falling 44% in 2017, institutions were accumulating GE only to become net sellers after the decline. Isn’t the phrase supposed to be “buy low and sell high”?

The chart below shows the relative strength of GE versus the S&P 500 going all the way back to 1975. As with all of our relative strength charts, a rising line indicates outperformance of GE relative to the S&P 500, while a falling line indicates underperformance. From the early 1980s right on through the turn of the century, GE was a major outperformer. At its peak in 2000, it had outperformed the S&P 500 over 400%. Since that peak just a few months before famous CEO Jack Welch left the company, it has been a brutal 18 years for GE. When the stock made its recent low of $12.83 at the start of the second quarter, the 400% of outperformance had been more than erased, and the stock was now underperforming the S&P 500 by a record low of -50%.

Who knows where GE will go from here, but with the stock already up over 11% in Q2, it would be pretty ironic to see GE hit a generational bottom just as the institutional investor community started to cry uncle.

Energy: Market Leader

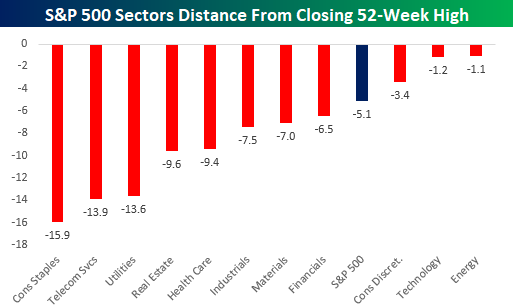

When was the last time we’ve been able to say that the Energy sector was a market leader? Well, you can say it now. While the S&P 500 is still over 5% from its 52-week closing high, the Energy sector is knocking on those levels and is currently down just 1% from its closing high. In fact, while Technology gets all the attention these days for its leadership, the sector is actually slightly further below its 52-week high than Energy. Granted, Technology has a much larger weighting and is therefore more impactful on the overall index, but strictly in terms of how far each sector is from its 52-week closing high, Energy is on top.

Behind Technology and Energy, the only other sector that is closer to its 52-week closing high than the S&P 500 is Consumer Discretionary (-3.4%). As far as the laggards are concerned, three sectors are more than 10% from their 52-week highs and they are all defensive in nature (Consumer Staples, Telecom Services, and Utilities). Given that the S&P 500 is in the middle of a correction, you would think that defensives would be holding up well. But because of rising interest rates, which make high dividend paying stocks less attractive, the defensives have struggled.

With regards to Energy specifically, the sector has had quite a run off its early April lows. At this point it’s up more than 20%.

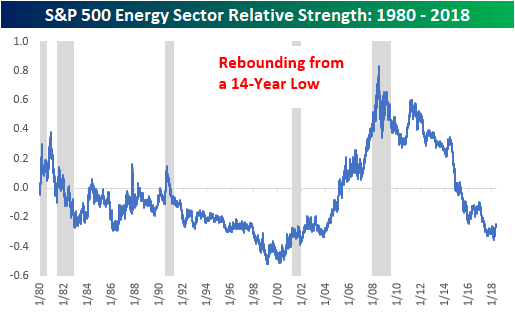

While the Energy sector is certainly overbought in the short-term, from a longer-term vantage point, you wouldn’t believe that the sector was performing well. The chart below shows the relative strength of the Energy sector versus the S&P 500 going back to 1980. When the line is rising, it indicates that the Energy sector is outperforming and vice versa. Ever since the middle of the last recession, the Energy sector has been a near constant underperformer vs the S&P 500. If you look really closely at the chart, you can see that the relative strength line for the sector has stopped going down, but it remains right near 14-year lows.

The last period of underperformance for the sector spanned a longer stretch (1980 – 2000), but the magnitude of the underperformance wasn’t nearly as deep. Given the steep underperformance, is nearly a decade of underperformance enough for the sector to finally turn things around? Rising oil prices even as the dollar has been rallying certainly doesn’t hurt the bullish argument.

Fixed Income Weekly – 5/16/18

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

This week we discuss the relationship between dividend coverage and yield, as well as identifying a series of stocks that look attractive given high yield relative to their coverage ratios.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

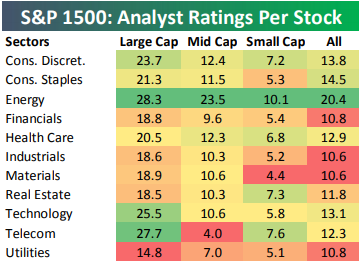

Energy Stocks Have the Most Analyst Coverage

Last week we published a post looking at the number of analyst ratings per stock by market cap. On average, a large-cap stock has 21.2 analyst ratings per stock versus just 6.2 for small-cap stocks.

Below we take a look at average analyst ratings per stock by sector. If we had to guess which sector had the most coverage, we would almost certainly guess Technology. That’s not the case, though. In reality, the Energy sector has the most coverage, and it’s not really close. Across the S&P 1500, which includes large caps, mid caps, and small caps, the average Energy stock has 20.4 analyst ratings per stock. The Consumer Staples sector is the next closest at 14.5.

At the large-cap level, Energy ranks first with 28.3 ratings per stock. Telecom ranks second at 27.7, followed by Technology in third at 25.5. Utilities has the lowest coverage at the large-cap level at just 14.8.

In the mid-cap space, the average Energy stock has 23.5 analyst ratings per stock, which is more than 10 ratings higher than the next sector (Consumer Discretionary) at 12.4. While Technology has 25.5 ratings per stock in the large-cap space, it only has 10.6 ratings per stock in the mid-cap space.

For small caps, Energy once again has the most coverage at 10.1 analyst ratings per stock. Energy is the only small-cap sector with an average of more than 10. Telecom, Real Estate, and Consumer Discretionary all have more than 7 analyst ratings per stock, while Technology is only at 5.8. The Materials sector has the least amount of coverage in the small-cap space with just 4.4 ratings per stock.

Chart of the Day: Housing Starts Remain Solid

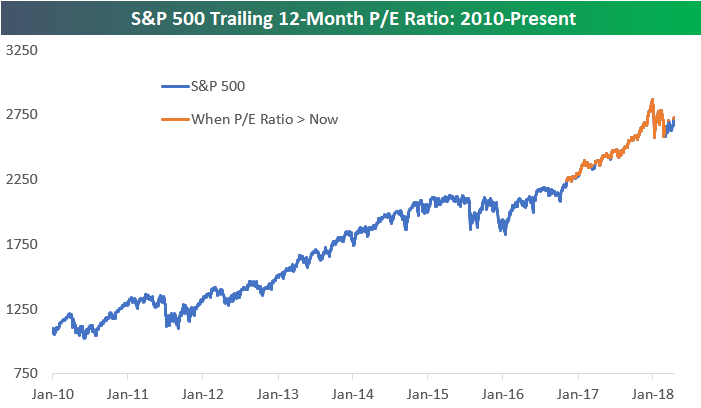

S&P 500 Trailing 12-Month P/E Ratio

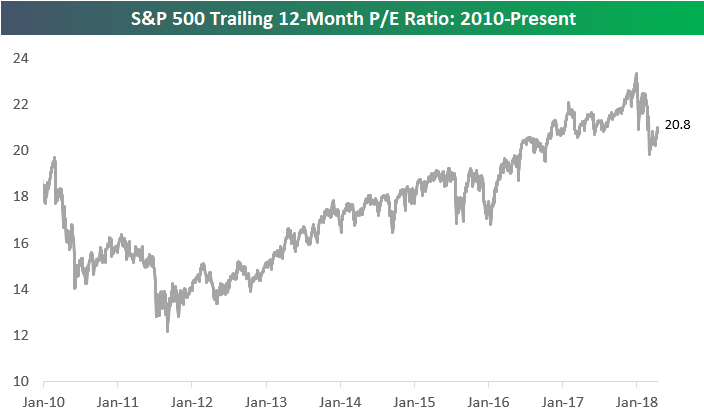

As of yesterday, the S&P 500’s trailing 12-month P/E ratio stood at 20.8. The high point for the S&P’s P/E ratio for the current bull market was 23.34 hit on January 26th, which was the same day the index made its last all-time high in price. Since those highs, the P/E has contracted by 2.54 points.

Below is a chart of the S&P 500’s price since 2010. The orange line represents periods when the S&P 500’s P/E ratio has been higher than it is now (>20.80). As shown, the index basically traded at a higher valuation than now for the entirety of 2017’s big rally.

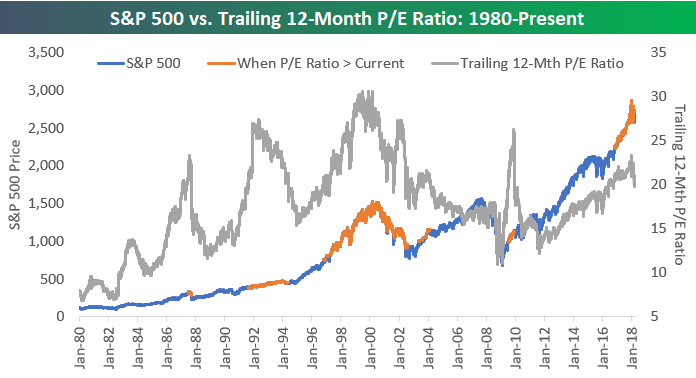

Below we show the S&P 500’s price vs. P/E ratio going back to 1980. Once again, the S&P’s price is highlighted in orange when the index’s P/E ratio has been greater than 20.8. As shown, the S&P traded at a higher valuation than now from 1992 through early 1994 and again from mid-1997 through early 2002. During the 2003-2007 bull market, we actually saw P/E contraction that kept it below 20 up until the index peaked in October 2007.

Bespoke’s Global Macro Dashboard — 5/16/18

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

The Closer — Pricing Power, TIC’d, ARS — 5/15/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we recap recent happenings in Argentina, flows into and out of the US securities markets by international investors, and data from the NY Fed with corporate profits implications.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!