Lots of Noise, Little Headway

Despite massive volatility on a day to day basis, it may sound hard to believe, but the S&P 500 is currently trading right where it was nearly two months ago on February 13th. You read that right, in what has been the most volatile market environment in at least a couple of years, the S&P 500 has nothing to show for it – up or down! In terms of individual sectors, we’ve seen some rotation. While Technology continues to be a market leader, it has been joined by former laggards like the Energy (+5.1%) and Utilities (0.5%) sectors to the upside. On the downside, Telecom Services, Consumer Staples, and Materials are all down over 2%, while Industrials, Financials, and Consumer Discretionary are down a percent.

As far as individual stocks are concerned, 250 stocks are up and 250 stocks are down, so it couldn’t be more balanced. While a total of 43 stocks in the S&P 500 are up over 10% over the last 2 months, in the interest of space, the table below lists the twenty top performers. As you might expect given the sector’s leadership, a number of stocks from the Energy sector make up the list with Hess (HES), Noble Energy (NBL), Baker Hughes/GE (BHGE), and National Oilwell (NOV) all up over 20%. The top-performing stocks, however, have been Nektar (NKTR), XL Group (XL), and Chipotle (CMG), with each gaining close to or more than 30%. FAANG stocks had a good start to the year, but the only one that has been able to keep the momentum going is Netflix (NFLX), which is up nearly 20%.

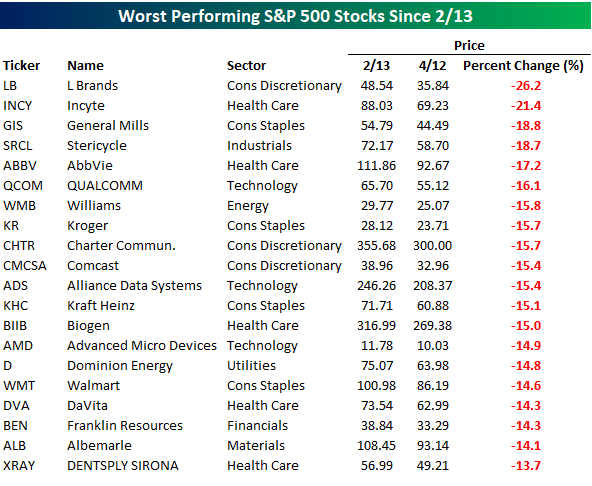

While 43 stocks in the S&P 500 are up over 10% since 2/13, 37 stocks are down 10%+, and in the table below, we list the worst 20. As shown, just two of the worst performing stocks are down over 20% since February 13th, which is actually pretty surprising to us given the volatility. Those two stocks are L Brands (LB) and Incyte (INCY). Looking through the list of losers, though, there are a number of blue-chip stocks such as General Mills (GIS), QUALCOMM (QCOM), Comcast (CMCSA), Kraft Heinz (KHC), Biogen (BIIB), and Walmart (WMT).

the Bespoke 50 — 4/12/18

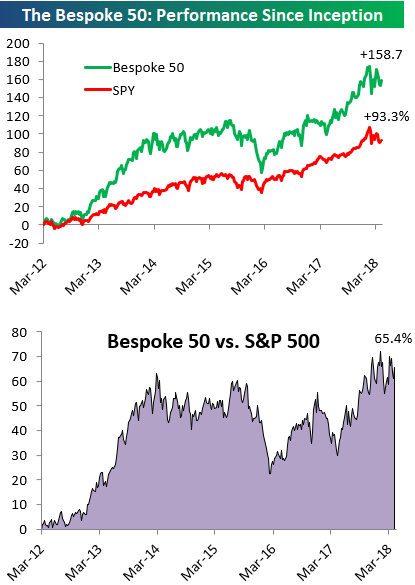

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 65.4 percentage points. Through today, the “Bespoke 50” is up 158.7% since inception versus the S&P 500’s gain of 93.3%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

Chart of the Day: Vacation All I Ever Wanted

Individual Investors Bail

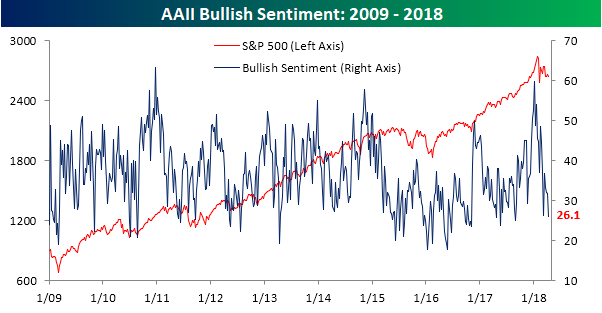

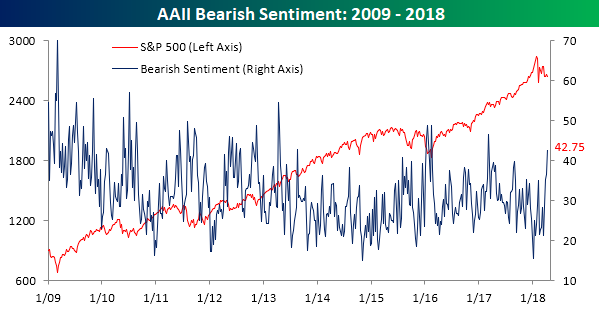

2018 hasn’t been the year for the little guy. Late last year, individual investors appeared to be finally getting comfortable with stocks as bullish sentiment in the weekly poll from AAII topped 50% for the first time in nearly three years. For a little while, they enjoyed the ride as equities surged to start the year and bullish sentiment reached just shy of 60%. Then the correction came. Since then, the bulls have been in steady retreat as increased volatility and lower prices remind these individuals why they were so apprehensive in the first place. This week provided a further confirmation of that trend as bullish sentiment in the weekly AAII poll dropped from 31.9% down to 26.09%. This marked the fourth straight week of declining bullish sentiment and took the percentage of bulls to the lowest level since last August.

The investors leaving the bullish camp recently aren’t just moving to the neutral sidelines either. They are flat out bearish. In this week’s survey, bearish sentiment surged from 36.6% up to 42.75%. Bearish sentiment has now increased by more than 20 percentage points in the last four weeks and is at its highest level since last March.

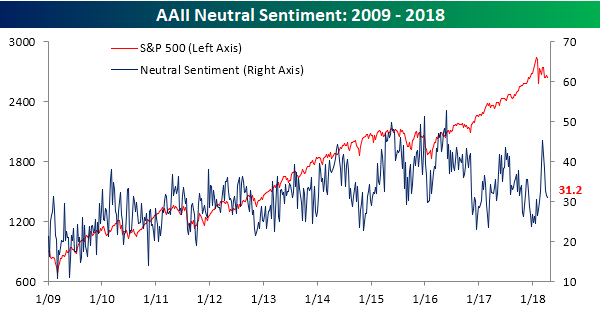

Fence sitters have plummetted in recent weeks as well, so it’s not as though investors don’t have conviction. After hitting a recent high of over 45% in early March, neutral sentiment is now down to 31.2%.

A Record Streak in Jobless Claims

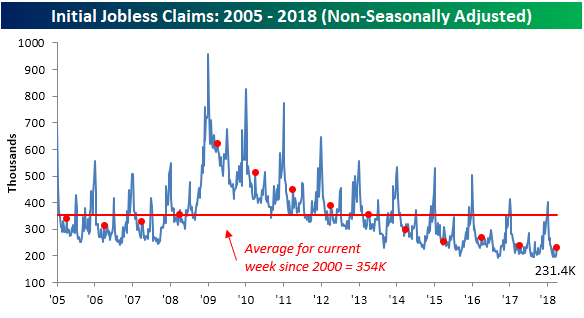

Jobless claims came in higher than expected for the second time in a row this week, but the report was still monumental from a historical perspective. While economists were forecasting first time claims to fall to 230K from last week’s higher than expected level of 242K, the actual reading came in at 233K. This week’s print now makes it 162 straight weeks where claims have come in below 300K, surpassing the previous record streak of 161 weeks that ended in April 1970. Given the fact that claims are currently still well below 300K, this could be a streak that lasts for some time.

With claims coming in at over 240K last week and above 230K this week, the four-week moving average has been drifting higher. This week’s reading came in at 230K, which is more than 7K above the multi-decade low of 222.75K that we hit five weeks ago. The way the last two prints have come in, it could be some time before we get back to those previous lows again if we get there at all.

On a non-seasonally adjusted basis, claims came in at 231.4K. While that’s up from last week’s level of 201K, it is still more than 120K below the average for the current week of the year dating back to 2000. In fact, the last time claims were lower for the current week of the year was back in 1969.

The Closer — Minute Musings, Punchy Prices, Crude Data, & Social Capital — 4/11/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we recap FOMC meeting minutes, review CPI inflation data, update tracking of monthly freight price changes, discuss weekly EIA petroleum market data and energy market price action, and analyze what social capital means for economic outcomes across states.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Short Interest Report – 4/11/18

Chart of the Day: Q1 Earnings Winners & Losers

Fixed Income Weekly – 4/11/18

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s note, we review the significant seasonality present in breakeven yields.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

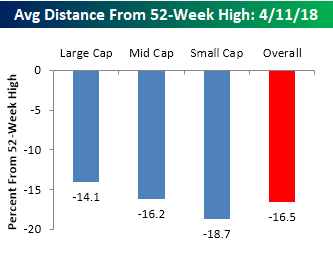

Average Stock Declines From 52-Week Highs

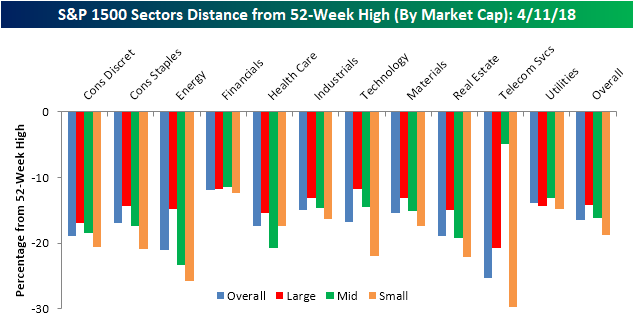

While the S&P 500 as a whole is down nearly 8% from its recent 52-week high in late January, as you might expect, the average decline of individual stocks in the index is quite a bit larger. The first chart below shows the average distance between the current price of stocks in the S&P 1500 relative to their 52-week highs by market cap. Overall, the average stock in the S&P 1500 is down just over 16.5% from its 52-week high. From a market cap perspective, the trend is pretty typical of what you would expect to see. Small caps are currently trading the furthest from their 52-week highs (-18.7%), mid caps are right in the middle (-16.2%), while large cap stocks are down an average of 14.1%.

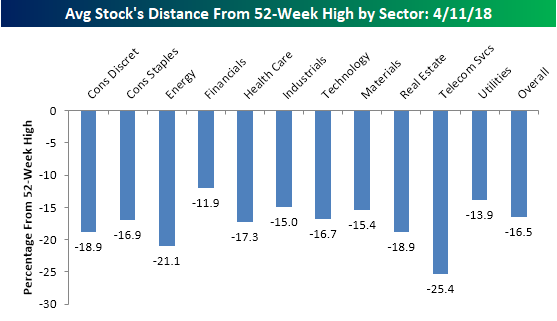

The chart below shows the average distance that stocks in the S&P 1500 are trading relative to their 52-week highs by sector. Currently, there are just two sectors where the average percentage decline is greater than 20% (Energy and Telecom Services). In the case of Energy, the current 21.1% reading is actually pretty good compared to prior readings we have seen for the sector over the last couple of years. Meanwhile, the Telecom Services sector only has a handful of stocks in it, so we don’t really place much focus on that. Financials are one sector that has held up really well in the recent market turbulence as stocks in that sector are only down an average of 11.9%. Since it’s the largest sector, no discussion would be complete without mentioning Technology, and while it had been a market leader, stocks in the sector are actually now down slightly more relative to their 52-week highs (-16.7%) than the overall market (-16.5%).

The last breakdown we wanted to look at is the average decline of stocks based on market cap and sector. The category that is down the most is small cap stocks in the Telecom Services sector (-29.66%). Keep in mind, though, that there are only seven stocks in the group. As mentioned above, stocks in the Technology sector are down slightly more than the overall average, but there is a wide disparity across different market caps. In the small cap Technology sector, the average stock is down nearly 22% compared to an average decline of less than 12% for large cap tech stocks. While there is a wide disparity between Technology sector stocks based on market cap, in the Financial sector, the spread couldn’t be narrower as less than 100 bps separates the best performing market cap range from the worst. How’s that for uniformity?

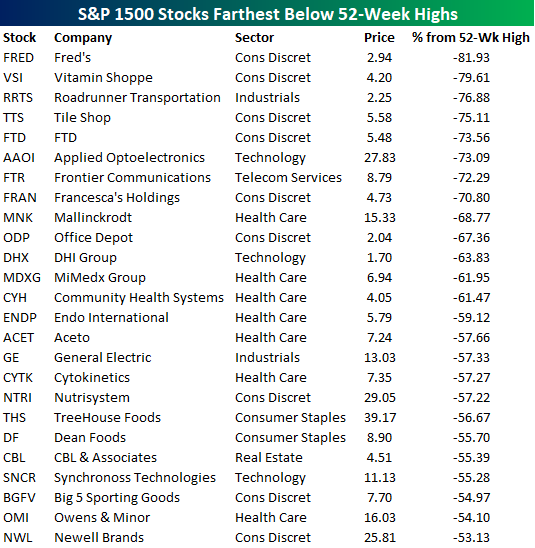

Finally, in the table below we provide a list of the 25 stocks in the S&P 1500 that are down the furthest from their respective 52-week highs. The two stocks down the most from their highs are both from the Consumer Discretionary sector and are also both brick and mortar retailers (Fred’s and Vitamin Shoppe). Outside of the brick and mortar retailers that are spread throughout the list, there are also seven stocks from the Health Care sector and three Tech stocks. The only sectors not represented on this list are Energy, Financials, Materials, and Utilities.