The Bespoke Report — Winning and Losing Trends Entering the 2nd Half

The Closer: End of Week Charts — 6/29/18

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

Below is a snapshot from today’s Closer highlighting weekly intraday price charts for major equity indices and other asset classes. If you’d like to see more, start a free trial below.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

Bespoke Summary of Economic Indicators: 6/29/18

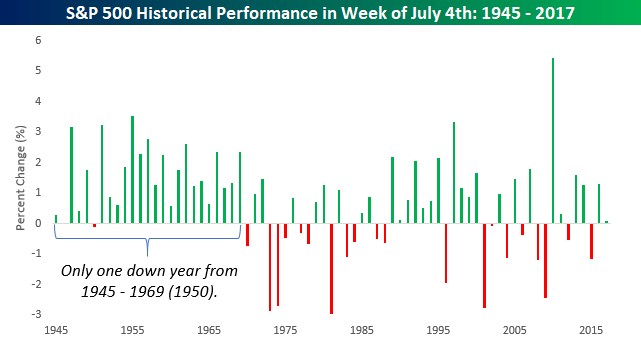

July 4th Week: Not As Bullish As it Used to Be

Next Wednesday is July 4th, and because the holiday falls right smack in the middle of the week, it is also likely to be a week where many people look to take extended weekends on either end of the holiday. That doesn’t mean it will be a quiet week in terms of economic data, though. Not only is next Friday the Non-Farm Payrolls report, but we’ll also be getting both the ISM Manufacturing (Monday) and the ISM Services (Thursday) reports, as well as FOMC Minutes (also Thursday). With fewer people at their desks and plenty of data, don’t be surprised if there is a pickup in volatility.

In terms of the US equity market’s historical performance during the week of July 4th, it has historically been positive. Since 1945, the S&P 500 has seen an average gain of 0.71% during the week of July 4th with positive returns 70% of the time. In years where the market was already up YTD heading into the holiday week, returns were even a little better at 0.78% with positive returns 75% of the time. For these calculations, we have used the S&P 500’s returns from the Friday before July 4th to the Friday after. In those cases where July 4th fell on a Friday or Saturday (in which case the markets were closed on the 3rd), performance was measured in the week before.

The chart below shows the S&P 500’s July 4th week returns since 1945. Looking at the chart, what really stands out is how consistently positive the S&P 500 was in the 25 years that followed WWII. From 1945 – 1969, the S&P 500 was up during the July 4th week in every year but one (1950), and in that one down year it only fell 0.11%. Since then, though, the bullish trend for the week has waned. While the S&P 500’s return is still positive, it has not been nearly as consistent to the upside with gains just 58% of the time.

The Closer — GDP Revised, Intangible Investment, Vols, & Consumer Comfort — 6/28/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review GDP revisions from today, discuss the rising share of non-physical investment, highlight fixed income and cross-asset volatility trends, and discuss what’s driven the recent decline in weekly Bloomberg Consumer Comfort readings.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bespoke Sector Snapshots — 6/28/18

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a two-week free trial to Bespoke Premium now.

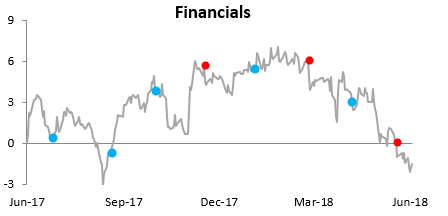

Below is one of the many charts included in this week’s Sector Snapshot, which shows the relative strength of the Financials sector versus the S&P 500. When the line is falling, the sector is underperforming the S&P, and vice versa when the line is rising. Unfortunately for anyone long the Financials, a rising line hasn’t been in the cards lately. In fact, after a record streak of 13 straight daily declines, the sector’s relative strength couldn’t be much worse.

To find out what this means and to see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

Contracting S&P 500 Trailing 12-Month P/E Ratio

While the S&P 500 is up about 1% year-to-date, earnings strength has caused its trailing 12-month P/E ratio to actually contract 1.78 points from 22.37 at the start of the year down to 20.59 as of this writing.

Below we show how trailing 12-month valuations have changed both year-to-date and over the last 12 months.

Year-to-date, every sector with the exception of Consumer Discretionary and Utilities has seen contraction in its P/E ratio. The Energy sector has seen the biggest contraction, but it also started the year with the second highest valuation. Along with Energy, there are five other sectors that have seen contraction of 2.5 points or more in their P/E ratios — Materials, Industrials, Consumer Staples, Telecom, and Financials.

The Technology sector is up 10% year-to-date, and even it has seen contraction in its P/E ratio due to earnings strength. As shown in the table, Tech’s P/E started the year at 23.63, and it’s now down to 22.55.

The one sector that has seen an expansion in its trailing 12-month P/E ratio is Consumer Discretionary, which has jumped 1.62 points YTD from 23.49 up to 25.12.

For more in-depth sector analysis, check out our Sector Snapshot report every Thursday as part of our Bespoke Premium service. You can join Bespoke Premium today with this 14-day free trial offer.

Chart of the Day: European Credit Cautionary

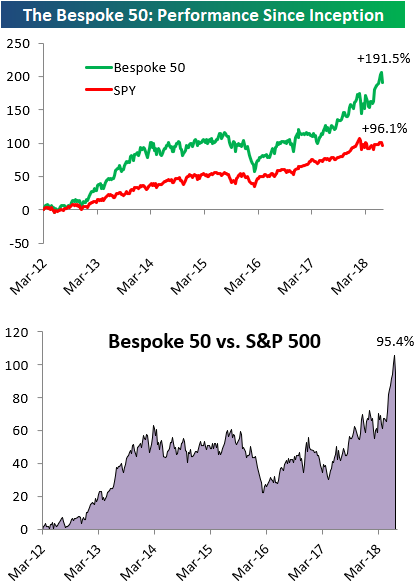

the Bespoke 50 — 6/28/18

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 95.4 percentage points. Through today, the “Bespoke 50” is up 191.5% since inception versus the S&P 500’s gain of 96.1%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

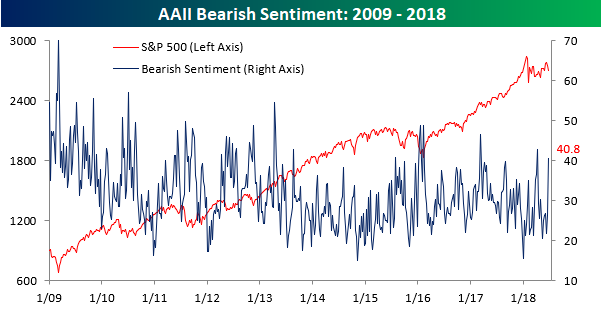

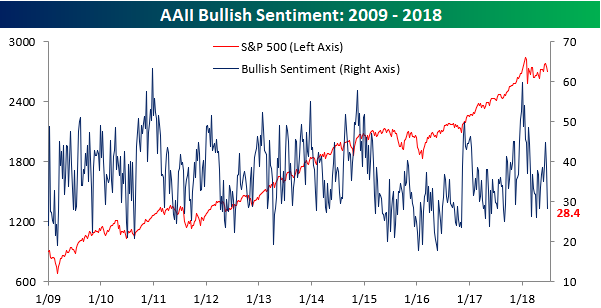

Bearish Sentiment Surges

After a few very weak days for the stock market’s leaders, individual investor sentiment really headed south this week. According to the weekly sentiment survey from AAII, bullish sentiment dropped more than ten percentage points, falling from 38.7% down to 28.4% in what was the largest one week decline since early March.

As bullish sentiment declined, bearish sentiment surged, rising from 26.2% up to 40.8% in what is only the second week in the last year where bearish sentiment has been above 40%. More importantly, though, it was the largest one week increase in negative sentiment since January 2016, which also happens to be another time when a plunging Chinese stock market was in the headlines.