B.I.G. Tips – May Employment Report Preview

Heading into Friday’s Non-Farm Payrolls (NFP) report for May, economists are expecting an increase in payrolls of 190K, which would be a big improvement from April’s reading of 164K. In the private sector, economists are also expecting a similar increase of 190K. With these increases, the unemployment rate is expected to remain low at 3.9%. The big area of focus, however, will come from average hourly earnings. With so much concern around inflation, any stronger than expected reading in wage measures will likely be viewed as a negative for the market.

Ahead of the report, we just published our eleven-page preview of the May jobs report. This report contains a ton of analysis related to how the equity market has historically reacted to the monthly jobs report, as well as how secondary employment-related indicators we track looked in May. We also include a breakdown of how the initial reading for May typically comes in relative to expectations and how that ranks versus other months.

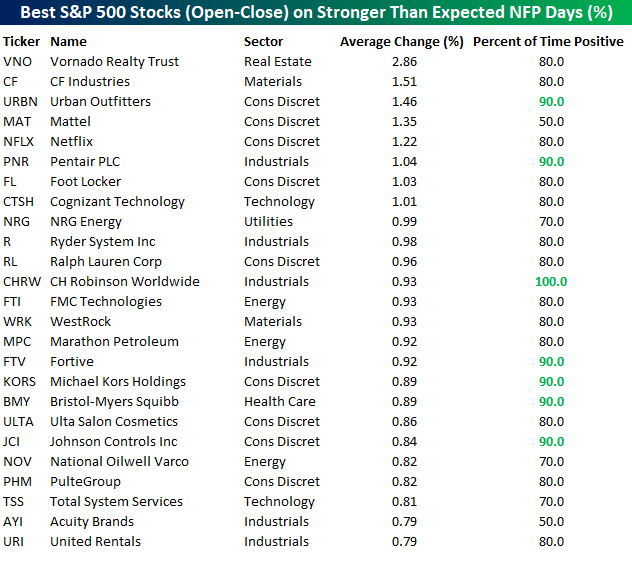

One topic we cover in each month’s report is the S&P 500 stocks that do best and worst from the open to close on the day of the employment report based on whether or not the report comes in stronger or weaker than expected. In other words, which stocks should you buy, and which should you avoid? The table below highlights the best-performing stocks in the S&P 500 from the open to close on days when the Non-Farm Payrolls report has been better than expected over the last two years.

Of the 25 top performing stocks on days when the NFP beats expectations, eight sectors are represented, and Consumer Discretionary leads the way with nine. Vornado (VNO) has been the best performing stock with an average open to close gain of 2.86%. In terms of consistency, CH Robinson (CHRW) has been up every time, while another six stocks have been positive nine out of ten times.

For anyone with more than a passing interest in how equities are impacted by economic data, this report is a must-read. To see the report, sign up for a monthly Bespoke Premium membership now!

Bespoke’s Sector Snapshot — 5/31/18

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a two-week free trial to Bespoke Premium now.

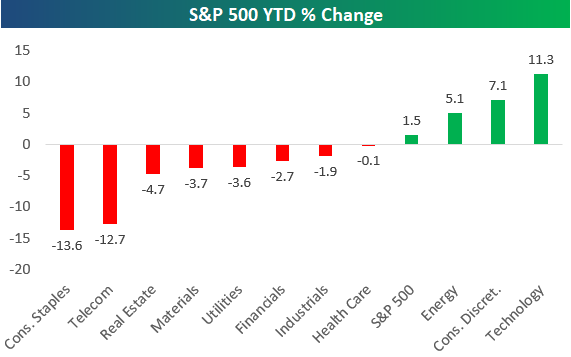

Below is one of the many charts included in this week’s Sector Snapshot, which highlights the year-to-date percentage change of the S&P 500 and its eleven sectors. As shown, just three sectors are up year-to-date, while eight are down.

To find out what this means and to see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

B.I.G. Tips — June 2018 Seasonality

Bespoke’s Consumer Pulse Report — May 2018

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the face of higher gas prices and a tightening Federal Reserve. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Bespoke Summary of Economic Indicators: 5/31/18

Chart of the Day: Tenet Healthcare (THC)

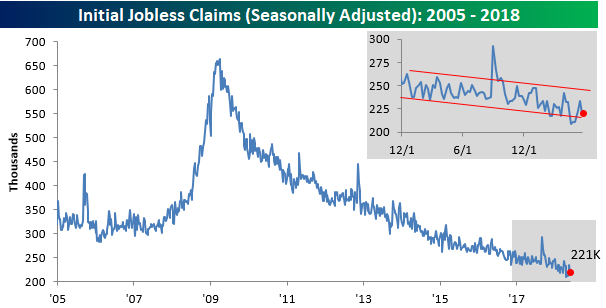

Jobless Claims Back on the Decline

After four weeks in a row of flat or rising readings, initial jobless claims declined this week falling from 234K down to 221K. That was also below consensus expectations for a reading of 228K. This week’s reading represents the record 169th straight week that claims have been at or below 300K and the 34th straight week that claims have been at or below 250K. On the latter, that’s the longest streak since 1970 when claims were at or below 250K for 89 straight weeks.

Although claims finally dropped again this week, the four-week moving average ticked up to 222.25K from last week’s reading of 219.75K. That puts the current reading 8.75K above the multi-decade low of 222.25K from two-weeks ago. Barring a big drop in claims next week, look for the four-week moving average to rise again as we will be dropping a multi-decade low of 211K from the count.

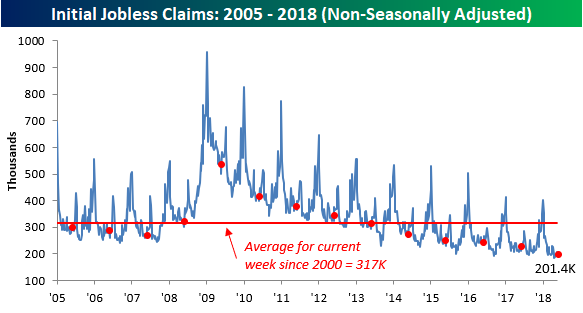

Finally, on a non-seasonally adjusted basis (NSA), claims dropped by nearly 6K down to 201.4K. For the current week of the year, this is the lowest reading since 1973, as well as more than 115K below the average of 317K for the current week of the year dating back to 2000.

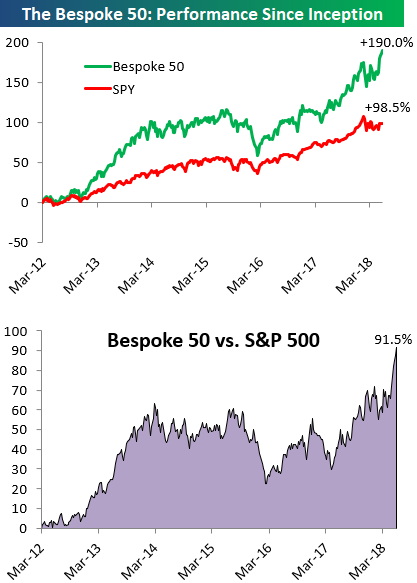

the Bespoke 50 — 5/31/18

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 91.5 percentage points. Through today, the “Bespoke 50” is up 190.0% since inception versus the S&P 500’s gain of 98.5%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

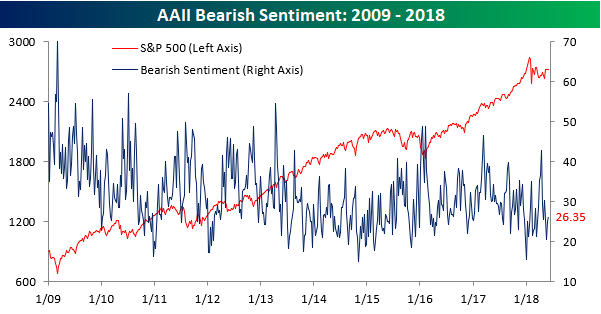

Modest Drop in Bullish Sentiment

With the markets becoming a little more volatile over the last few days, individual investors have grown slightly more cautious. According to this week’s sentiment survey from AAII, bullish sentiment dropped from 38.6% down to 35.0%, breaking a three-week streak of increases in the process. One silver lining is that in the most recent uptick in optimism, bullish sentiment made a higher high, so things are trending in the right direction at least.

Bearish sentiment saw a slight uptick this week, but at just 26.4% remains relatively low.

The Closer — Diving Into GDP — 5/30/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we take a long look at recent trends in the guts of GDP reports including corporate profits, inventories, fixed investment, and the outlook for a possible significant trade tailwind in Q2. We also review the BoC decision today and update our Bespoke Beige Book Index.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!