Daily Sector Snapshot — 6/10/25

CPI on Tap

Tomorrow’s report on May CPI will help to shape the inflation narrative for the rest of the summer. A stronger-than-expected report will be quickly seized upon by the anti-tariff contingency, and if there’s a weaker-than-expected report, you can bet that President Trump will be on Truth Social singing the praises of tariffs. Earlier today, we tweeted that the Fed’s CPI Nowcast was predicting headline CPI to rise 0.13% compared to a Wall Street consensus forecast of 0.2%, so if the Nowcast is right, get ready for some Truth Social posts!

Besides the Nowcast, seasonal trends suggest that a stronger-than-expected inflation print is less likely. The table and chart below show the frequency of stronger-than-expected, weaker-than-expected, and inline headline CPI prints from 1999 through 2024. Since 1999, the May CPI report (released in June) has only been stronger than expected 31% of the time. That ranks as the fifth-highest percentage of higher-than-expected readings of any month. Weaker-than-expected reports, however, are more common at 46% of the time. The only other month with a higher frequency of lower-than-expected headline CPI reports is November (released in December) at 50%.

Chart of the Day: Berkshire Struggles

Bespoke’s Morning Lineup – 6/10/25 – The Negative Nine

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Too many people miss the silver lining because they’re expecting gold.” – Maurice Sendak

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

We’re not sure if it’s the summer doldrums setting in early or that investors needed a breather after the craziness of the last several months, but for the second morning in a row, the action in futures has been quiet. This morning, S&P 500 futures have been moving on either side of the unchanged line while the Nasdaq is set to open slightly higher.

US and Chinese officials are in London again this morning for the second day of trade talks, and the economic calendar is quiet with NFIB Small Business Sentiment being today’s only report. That came in better than expected, rising from 95.8 to 98.8 in May. Overnight, in Asia, Australia and Japan were higher while Hong Kong and China declined.

When it comes to the mega-cap stocks in the S&P 500 with market caps of more than or around a trillion dollars, an increasingly evident trend is that the group no longer trades as a block, where each member’s performance is no longer in line with the others. This can be seen in the year-to-date performance of the nine stocks listed below. While the average performance of the nine stocks on a YTD basis is basically unchanged (-0.01%) and the median is a gain of 5.37%, the performance of each stock ranges from 18.5% (Meta Platforms-META) to a decline of 23.6% (Tesla–TSLA). Even over the last 12 months, while all nine stocks have experienced positive returns, the magnitude of the gains ranges from 4.3% for Apple (AAPL) to a gain of 69.6% for Broadcom (AVGO). Even with every stock trading higher, they have hardly traded in unison.

Where we have seen a group of stocks trade much more in unison is at the other end of the market cap scale. The table below shows the nine stocks in the S&P 500 with the smallest market caps and how each has performed YTD and over the last 12 months. On a YTD basis, all nine stocks are lower with an average decline of 20.7% (median: -19.35). Just as notable is that the range of returns has been much closer than the largest stocks in the S&P 500. Whereas more than 42 percentage points separates the best and worst performances of the nine largest stocks in the S&P 500, for the nine stocks with the smallest market caps, the spread is just 23 percentage points. So, while the rising tide hasn’t impacted each of the nine largest stocks equally, the nine smallest stocks have been weighed down by a more similar anchor.

In terms of performance, while there may have been some concerns over the performance of the mega-cap stocks in recent months, they’re still doing much better than the nine smallest stocks.

Even on a relative strength basis, the nine stocks with the smallest market caps in the S&P 500 have consistently underperformed. Earlier this month, they even made a new low relative to the mega caps.

The Closer – IPOs, Consumers, Allotments – 6/9/25

Log-in here if you’re a member with access to the Closer.

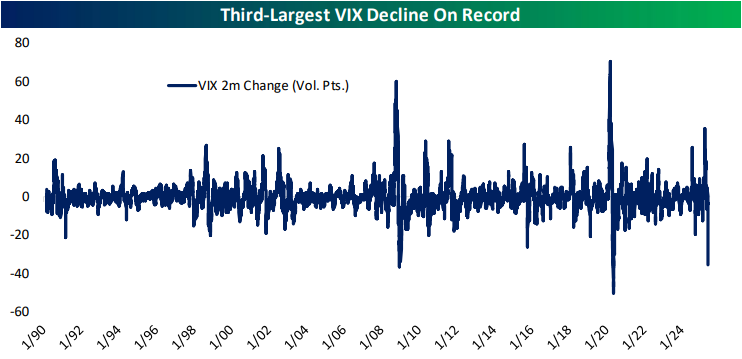

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a look at the huge drop in the VIX over the past two months (page 1). We then check in on IPO issuance (page 2) and consumer credit (page 3). Staying on the topic of the consumer, we then review their inflation expectations and other findings from the latest New York survey (pages 4 – 6). We close out with a check in on Treasury allotment figures (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 6/9/25

$1,000 in the Stock Market at Birth

There’s a real chance that newborn children in the US will begin receiving $1,000 in an investment account at birth if President Trump’s budget bill passes Congress in the months ahead. CEOs of some major public companies are actually meeting at the White House today to discuss the “$1,000 at birth” provision.

Below is a chart we created showing how much $1,000 at birth would be worth today if it were invested in the S&P 500 at the end of each month going back 50 years (with dividends re-invested).

As shown above, $1,000 invested in the S&P fifty years ago and not touched would be worth nearly $350,000 today. That number drops to roughly $127,000 if the $1,000 were invested at the end of November 1980 and $40,000 if the start date is August 1987. Even still, there are a lot of 37-year olds out there born just before the 1987 crash that wouldn’t mind having $40k in an investment account right now!

The second chart above shows the same data over just the last 25 years for better scale. Because of the Dot Com bubble and burst of the late 1990s and early 2000s and the Financial Crisis of the late 2000s, people born in various months during this period would have quite different account values right now. $1,000 invested in August 2000 just after the Dot Com peak would be worth roughly $6,200 today, while $1,000 invested nearly ten years later in February 2009 would be worth nearly $5k more at $11,000. If this provision comes to pass, we may see birth rates go up during lengthy bear markets!

Q1 2025 Earnings Conference Call Recaps: Lululemon (LULU)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Lululemon’s (LULU) Q1 2025 earnings call.

![]()

Lululemon Athletica (LULU) is a premium athletic apparel company known for blending high-performance functionality with sleek, lifestyle-focused design. Originally built on yoga wear, the brand now serves fitness enthusiasts, casual wearers, and trend-driven consumers with women’s and men’s apparel, accessories, and footwear. In Q1, LULU reported 7% revenue growth, with US comps up just 2%, but China up 22%. Cautious US consumer behavior and lower store traffic weighed on performance, though new product innovations like Align No Line and Daydrift were successful. Gross margin rose 60 bps to 58.3%, but new tariffs from China are expected to pressure margins in Q2 before mitigation efforts take effect. The company reaffirmed full-year revenue guidance, expecting 7–8% growth, with stronger international expansion and pricing adjustments planned to offset FX and tariff impacts. LULU beat revenue and EPS estimates, but the stock plummeted 19.8% on 6/6…

Continue reading our Conference Call Recap for LULU by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q1 2025 Earnings Conference Call Recaps: ServiceTitan (TTAN)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers ServiceTitan’s (TTAN) Q1 2026 earnings call.

![]()

ServiceTitan (TTAN) is a software platform built to power the home and commercial services industries, providing end-to-end business management tools for contractors in trades like HVAC, plumbing, electrical, garage doors, roofing, and more. Its cloud-based solution takes care of everything from dispatching and customer relationship management to marketing, payments, and field technician support. TTAN serves thousands of technicians and businesses, from small shops to private equity-backed consolidators, offering insight into digitization trends across the skilled trades economy. In Q1, TTAN posted 27% YoY total revenue growth to $215.7M, with subscription revenue up 29% and usage revenue up 22%. The company saw traction with large enterprise go-lives and cited record ARR activation in commercial accounts, with more ARR in 28 hours than a typical month. AI-native products like Contact Center Pro began booking jobs autonomously, while the roofing segment advanced via new tech and partnerships (like EagleView). Leadership remained cautious on macro headwinds, especially weather-driven Q2 seasonality and tariff risks. TTAN shares were down 6.9% on 6/6 despite the triple play results…

Continue reading our Conference Call Recap for TTAN by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q1 2025 Earnings Conference Call Recaps: DocuSign (DOCU)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers DocuSign’s (DOCU) Q1 2026 earnings call.

![]()

DocuSign (DOCU) provides cloud-based software for automating the agreement process, best known for its eSignature product but now expanding into a broader platform called Intelligent Agreement Management (IAM). The IAM platform integrates AI to streamline how organizations create, execute, and manage contracts, offering features like biometric ID verification, automated risk review, and obligation tracking. With more than 1.7 million customers globally, DOCU serves a wide range of industries from financial services to healthcare to government. DOCU’s Q1 call centered on the rapid adoption of IAM, which now has over 10,000 customers and is contributing to stronger product usage and upsell potential. IAM self-serve launched in April and added nearly 1,000 customers within three weeks, while international IAM deals grew over 50% sequentially. Although billings growth came in at 4%, slightly below guidance due to earlier-than-expected drops in early renewals, usage trends hit multi-year highs and net dollar retention improved to 101%. DocuSign also unveiled a slate of new AI-powered tools and reaffirmed its commitment to building a long-term, efficient growth engine. DOCU added another triple play under its belt, its seventh in the last nine quarters, but the stock fell 19% on 6/6 on AI growing pains that are impacting billings growth…

Continue reading our Conference Call Recap for DOCU by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below: