Bespoke Consumer Pulse Report — July 2018

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in year two of Trump’s economy. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

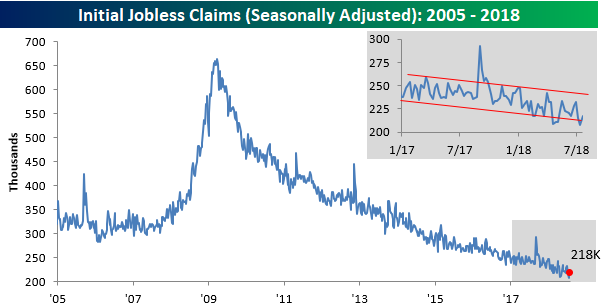

Jobless Claims Making New Records

Jobless claims came in lower than expected this week with the seasonally adjusted headline reading rising by 1K to 218K compared to consensus forecasts of 220K. While it wasn’t a big ‘beat’ relative to expectations, let’s just put the string of recent low readings into perspective. This week was the 178th straight week of sub 300K claims (a record), the 43rd straight week at or below 250K (longest streak since 1970), and the fourth straight week of readings at or below 220K (longest streak since 1969).

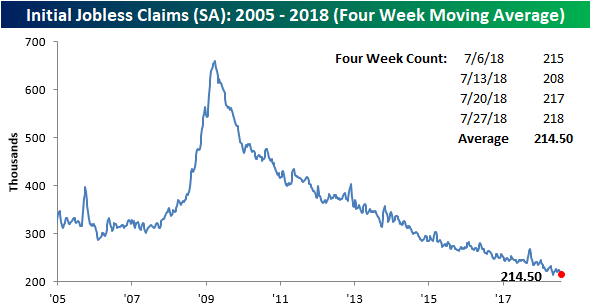

This week’s low reading in claims brought the four-week moving average close to a new cycle low this week as well. At 214.5k, the average is now within just 1K of a new cycle low. However, in order to break that prior low from May, we would need to see a reading next week below 211K (assuming no revisions). It’s possible, but it will be tough.

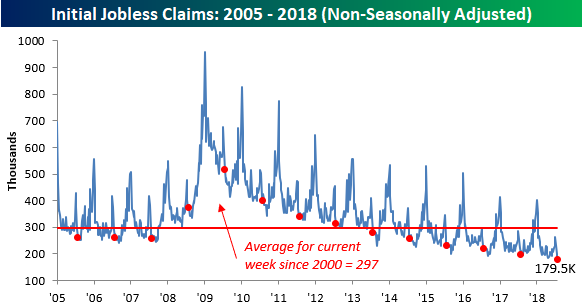

Finally, the non-seasonally adjusted (NSA) reading of claims also declined this week to its lowest level for the month of July on record. At 179.5K, it’s also over 117K below the average of 297K for the current week of the year dating back to 2000.

the Bespoke 50 — 8/2/18

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 91.5 percentage points. Through today, the “Bespoke 50” is up 196.0% since inception versus the S&P 500’s gain of 104.5%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

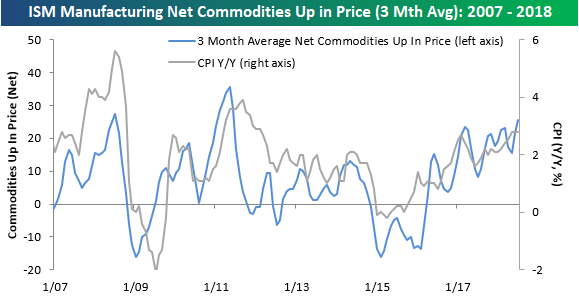

Another “Strongest Since” Inflation Indicator

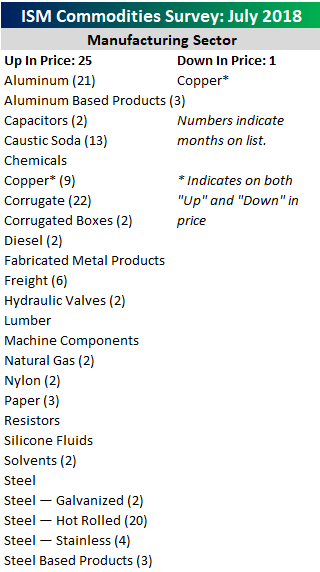

When it comes to different inflation readings, many releases have been accompanied by the phrase “strongest since” or something similar sounding. In each month’s ISM Manufacturing report, respondents are asked which commodities they have seen price increases for and which ones they have seen declines in. In this month’s report, respondents noted price increases in 25 different commodities and declines in just one (Copper- which was actually on both lists).

Going over each month’s ISM report, we have compiled an index which tracks the three month average of the net number of commodities that are up in price each month. With this month’s report, the three-month average of the net number of commodities rising in price rose from 21.7 up to 25.7. That’s a pretty big jump for a single month, and it also represents the highest reading for the index since June 2011. The chart below compares our ISM Commodity Survey index to y/y CPI going back to 2007. Over time, there has been a pretty positive correlation between the two, and in some cases, big moves in the ISM Commodities Survey even preceded a move in CPI. With that in mind, this month’s reading in the Commodities Survey index confirms the current leg higher in CPI and may even suggest further upside going forward.

Chart of the Day: Decile Analysis of Near-Term Rotation

Tariffs, Tariffs, Tariffs!

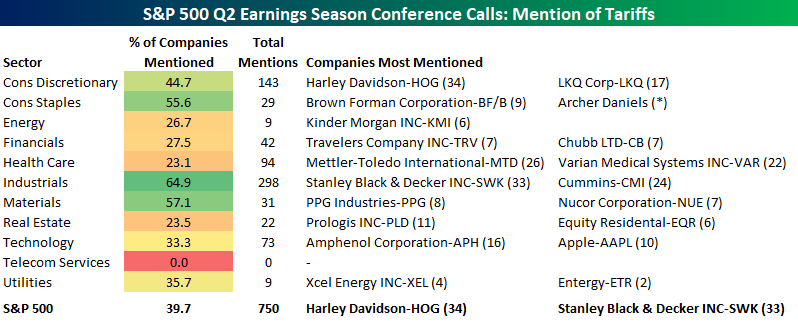

As mentioned earlier in a tweet about the ISM Manufacturing report for July, talk and concern about tariffs is just about everywhere in the manufacturing sector. In addition to the ISM Manufacturing report, we’ve also seen a major uptick in tariff conversation during the latest round of Q2 earnings conference calls. We’ve been tracking all of the conference call transcripts of companies in the S&P 500 that have reported earnings so far and with just about half of all companies reporting, the percentage of conference calls where tariffs have been brought up has more than doubled relative to Q1 (39.8% vs 16.6%). For the entire Q1 earnings season, the word “tariff” came up 290 different times in S&P 500 conference calls (in some calls, the word came up more than once), while during this earnings season, the term has already come up 609 different times. Remember, we’re only halfway through this earnings season.

The table below breaks down the percentage of companies that have mentioned tariffs in their Q2 conference calls by sector. For each sector, we have also included the conference calls where the term has come up the most frequently. Three sectors have seen “tariff” mentioned in half of the conference calls (Industrials, Materials, and Consumer Staples), and all three sectors have lagged the market considerably this year. Sectors where tariffs have been least mentioned are Telecom Services, Health Care, and Real Estate. In terms of individual companies, given all the headlines Harley Davidson (HOG) created when it was targeted by the President for saying it would move production outside of the US in response to tariffs, the fact that tariffs were mentioned the most on its conference call isn’t much of a surprise. Right behind HOG, Stanley Black & Decker (SWK), and Mettler-Toledo (MTD) round out the top three.

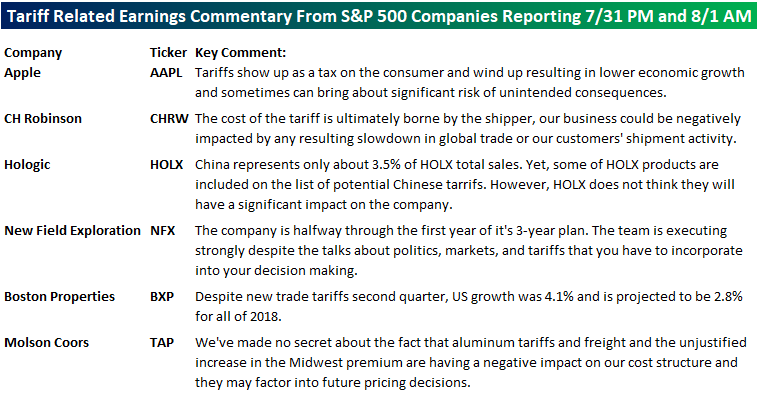

Finally, we also wanted to highlight a few excerpts from conference calls that have taken place between the close on Tuesday and the open Wednesday. Apple (AAPL) is the most notable of the six companies mentioned and gets right down to the bottom line with its statement that “Tariffs show up as a tax on the consumer…and sometimes can bring about significant risk of unintended consequences.” We couldn’t have said it better ourselves!

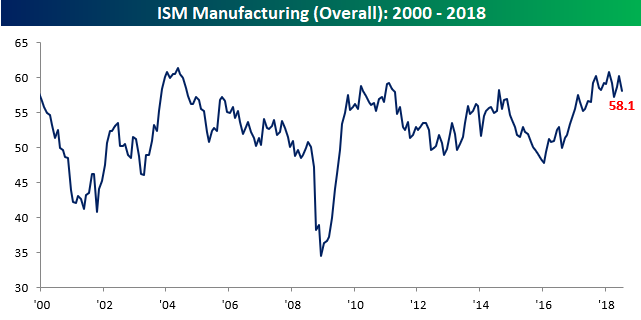

ISM Manufacturing Drifts Lower

Activity in the Manufacturing sector was slightly weaker than expected in July but still remained at strong levels. According to ISM, the Manufacturing PMI index fell from 60.2 down to 58.1 compared to expectations for a reading of 59.4. Putting this level into perspective, the Manufacturing PMI index is less than three points from its multi-year high of 60.8 from February.

Breadth in this month’s report wasn’t particularly strong as the vast majority of components showed declines relative to June with the biggest drops coming in Supplier Deliveries, Backlog Orders, and Imports, while Business Inventories and Employment were the only two categories that increased on a m/m basis. On a y/y basis, breadth was better as the number of components rising and falling was equally split at five.

One component we wanted to highlight specifically is New Orders. Looking at the chart below, this category is definitely trending lower from its high of 67.4 in December. At the same time, though, this component has been at or above 60 for 15 straight months now, so it can’t stay there forever. Going back to 1948, there have only been two other periods where this component was at 60 or above for 15 or more months. The first spanned the period from September 1954 through January 1956 (17 months), while the second period spanned 19 months from December 1971 through June 1973.

Fixed Income Weekly – 8/1/18

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

The Eurodollar futures curve (linked to LIBOR) is pancake flat and even partially inverted in some out-years. We review the even more skeptical views of the Eurodollar options market.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!

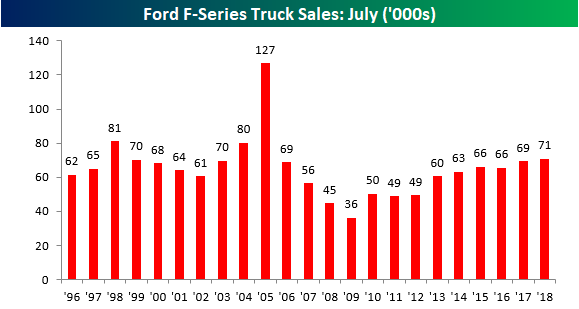

Best Year in Over a Decade For Ford F-Series Trucks

Ford released July sales figures earlier today and while the overall results were a bit weaker than expected, sales trends for its F-Series trucks remained healthy. Sales of pickup trucks (specifically at Ford) are often a sign of strength or weakness in the small business and construction sectors, and based on these numbers from Ford, the small business sector still looks strong. Ford reported sales of 70,949 F-Series trucks, which marks the strongest July sales total since 2005 and the fourth strongest July since 1996. Another thing to keep in mind regarding July’s sales totals is that the company mentioned in its call that a fire at one of its supplier plants actually hampered sales.

Keep in mind that the above sales totals are unadjusted so they don’t take the number of selling days, which are generally auto industry parlance for days in a month that aren’t Sundays or a national holiday, into account. So while selling days can vary from month to month (in July 2017 there were 25 compared to 24 this year), looking at YTD sales totals provides a more apples to apples comparison. To that end, the chart below shows YTD sales totals for F-Series trucks through July for every year since 1996. Through 7/31 of this year, total sales of F-Series trucks were 522,087. That’s the highest YTD sales total since 2005 (535K) and the third highest sales total since 1996.

Bespoke’s Global Macro Dashboard — 8/1/18

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!