Bespoke’s Global Macro Dashboard — 6/27/18

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

The Closer — Brent Breaks Out, Mexico Hires, Home Price Push, 4 of 5 Fed, Stoxx — 6/26/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we review a breakout in Brent and intense price action in both WTI-Brent and crack spreads. We also take a look at a variety of US data points including manufacturing activity and Case-Shiller Home Prices. Mexican labor markets are in strong shape, as today’s unemployment numbers showed. Our last set of charts reviews performance of Stoxx 600 groups and their valuations.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bespoke CNBC Appearance (6/26)

Bespoke co-founder Paul Hickey appeared on CNBC’s Squawk Box earlier today to discuss Monday’s sell-off and market prospects going forward. To view the segment, please click on the image below.

B.I.G. Tips – Diverging Confidence

Italian and Greek Yields Converge

Remember back when Greece was the laughingstock of Europe with its seemingly non-stop economic, political, and debt problems? They aren’t laughing as much anymore. Just yesterday, S&P raised its rating on Greek long-term debt, and while the current rating of B+ is still pretty far down the ladder in terms of quality, it’s moving in the right direction. As things currently stand, Greek 10-year debt sports a yield of 4.11%, which is down more than a full percentage point in the last year.

At the same time that yields on Greek debt have been falling, yields on Italian debt have been rising. In Italy, yields on 10-year debt are at 2.89%. While that’s right around the same yield as the US 10-year, relative to most other of its EU peers, Italian debt yields are up sharply over the last year as well as the last three months. As a result of the opposite moves in the yields of Greek and Italian 10-year debt, the spread between the two has narrowed considerably. Through Tuesday, yields on 10-year Greek debt offer a premium of just 122 basis points over Italian debt, which is the narrowest spread since December 2009. We’ll let you decide what this says about the relative attractiveness of either country’s debt.

Chart of the Day: Contrarian On China

Bespoke Stock Scores — 6/26/18

Trade or Rotation?

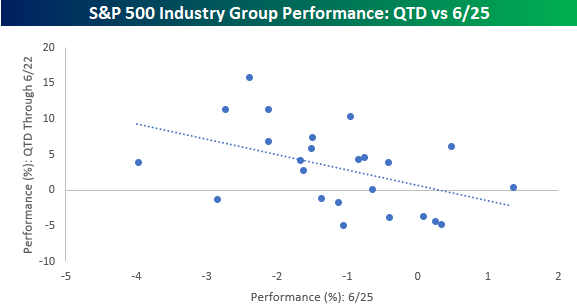

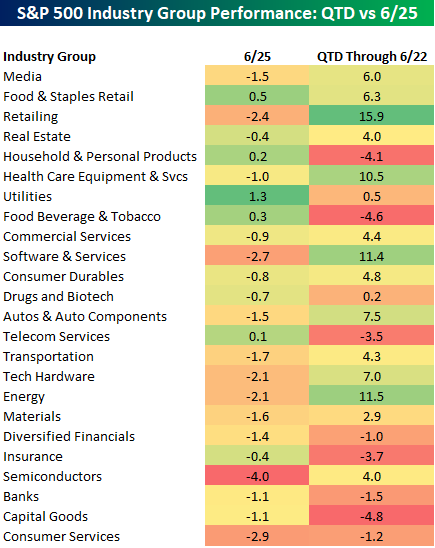

While yesterday’s decline has been largely blamed on the ongoing trade dispute between the US and China, we wouldn’t discount the impact of end of quarter rebalancing either. The chart and table below help to illustrate the point. The chart compares the performance of the 24 S&P 500 Industry Groups on Monday (x-axis) to their QTD performance through last Friday (y-axis). While there are some exceptions, the industry groups that were performing the best QTD through last Friday were down the most on Monday, while the QTD laggards performed best on Monday.

You can further see the “changing places” performance in the lower table. As shown, some of the best-performing industry groups QTD through Monday (Retailing, Software, and Energy) were down well over 2% yesterday. Conversely, many industry groups that were lagging QTD heading into Monday (Food, Beverage & Tobacco and Household & Personal Products) actually saw marginal gains on the day. Trade is definitely a factor at play in the market these days, but it’s hardly the only one.

The Closer — Deciles, New Homes, Brazil Balances, NAFTA Numbers, Global Trade — 6/25/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we analyze the factors which led to the biggest declines in stocks today using our decile analysis. We also break down economic data released today in the US, Brazil, and Mexico. Finally, we take a close look at slowing trade and a weak forecast for Canadian GDP in Canada.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

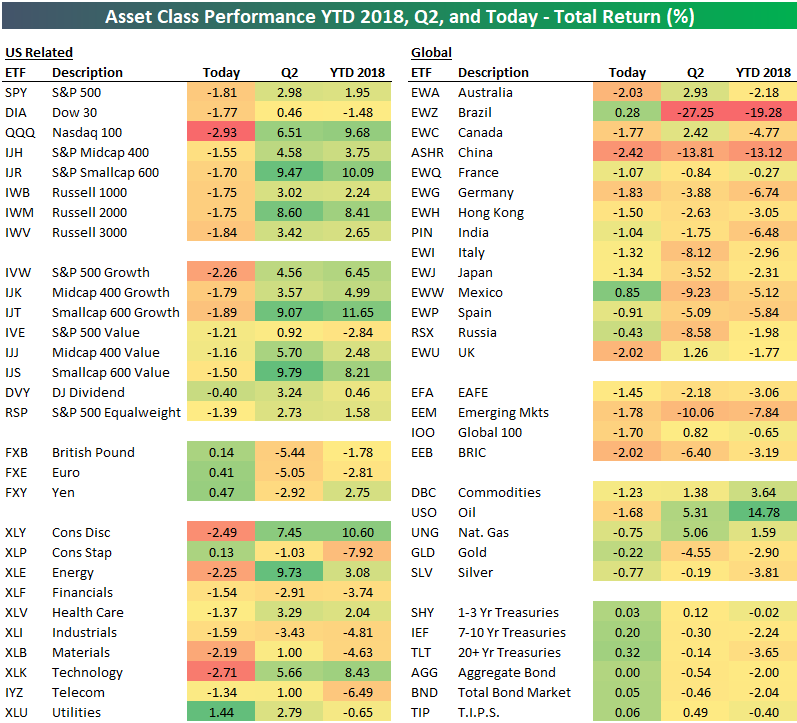

Market Leaders Getting Crushed

With the US stock market getting crushed to start the trading week, below is a quick snapshot highlighting the performance of various ETFs across asset classes. For each ETF, we show its performance today, quarter-to-date, and year-to-date.

Today’s market action is pretty simple to explain. We’re seeing extreme selling in the areas of the market that had been performing the best over the last couple of months.

As shown in our matrix below, the Nasdaq 100 (QQQ), small caps (IVW, IWM), Consumer Discretionary (XLY), Energy (XLE), and Technology (XLK) are the areas of the US market that are getting hit the hardest today. These are the areas that have rallied the most both YTD and in Q2. Defensive areas of the market like Utilities (XLU) and Consumer Staples (XLP) are actually catching a bid today as investors have decided to rotate out of recent winners and into more non-cyclical areas of the market.

Outside of the US, both Brazil (EWZ) and Mexico (EWW) are actually up on the day, while China (ASHR), the UK (EWU), and Australia (EWA) are down more than 2%.