The Closer: End of Week Charts — 7/27/18

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

Below is a snapshot from today’s Closer highlighting weekly intraday price charts for major equity indices and other asset classes. If you’d like to see more, start a free trial below.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

B.I.G. Tips – Long-Term GDP Revisions Challenge Some Narratives

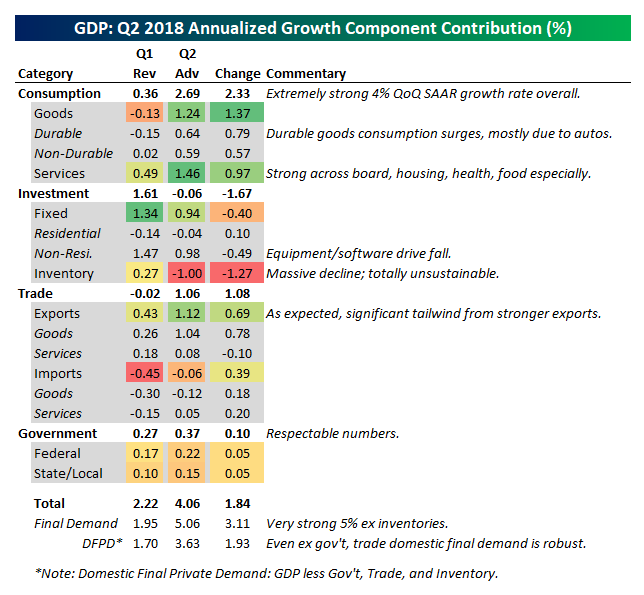

GDP Impresses, But 4% Won’t Last

Below is a breakdown of this morning’s Q2 GDP release, which came in at +4.1% — weaker than expected but still strong nonetheless. Consumption was much stronger thanks in part to lower withholding taxes in paychecks, but that one-time growth bump won’t carry forward to later quarters. Expect strong, but much less robust, consumption growth going forward. Trade was also a huge boost to overall GDP, adding 1.1% to growth in Q2. Soybeans especially, but other crops in general, helped push up exports as sellers rushed goods overseas to beat tariff deadlines. That will likely move the other direction in Q3. Government added to growth but not dramatically, a reasonable pace that may fall a bit but doesn’t look out of line. Fixed investment was notably slower in Q2 than Q1. While still contributing a very healthy 0.9% in Q2, the fall is worth keeping an eye on, especially given slowing leading indicators for capital expenditures from business. Finally, inventories plunged, dragging down growth by 1% QoQ SAAR. Inventories look ridiculously low, and can’t continue to subtract from GDP at the pace they have been over the last few years.

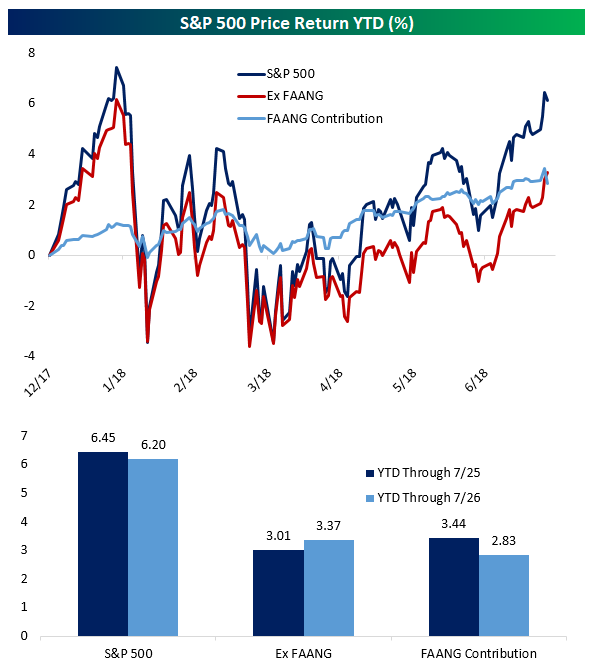

FAANG Still Helping

Below is a chart showing the S&P 500’s price return year-to-date and the impact that the five FAANG (FB, AAPL, AMZN, NFLX, GOOGL) stocks have had. While Facebook’s horrific reaction to earnings and the worst day in the stock’s history had a negative market impact, the overall performance of the market YTD has been supported by the group. While they’re only a 13.6% weight in the S&P 500’s market cap, they’re driving the market up to the tune of almost half of its YTD gains. Impressive stuff for 5 stocks on their own, even in spite of Facebook’s brutal collapse.

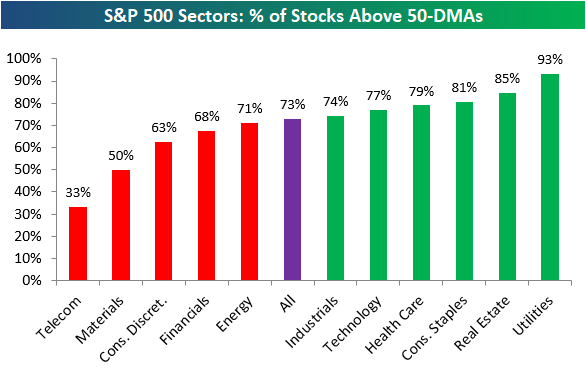

US Stock Market Breadth Strengthening

As shown below, 73% of S&P 500 companies begin the day above their 50-day moving averages, and six of eleven sectors have readings stronger than 73%. This is a sign of healthy underlying breadth for the market.

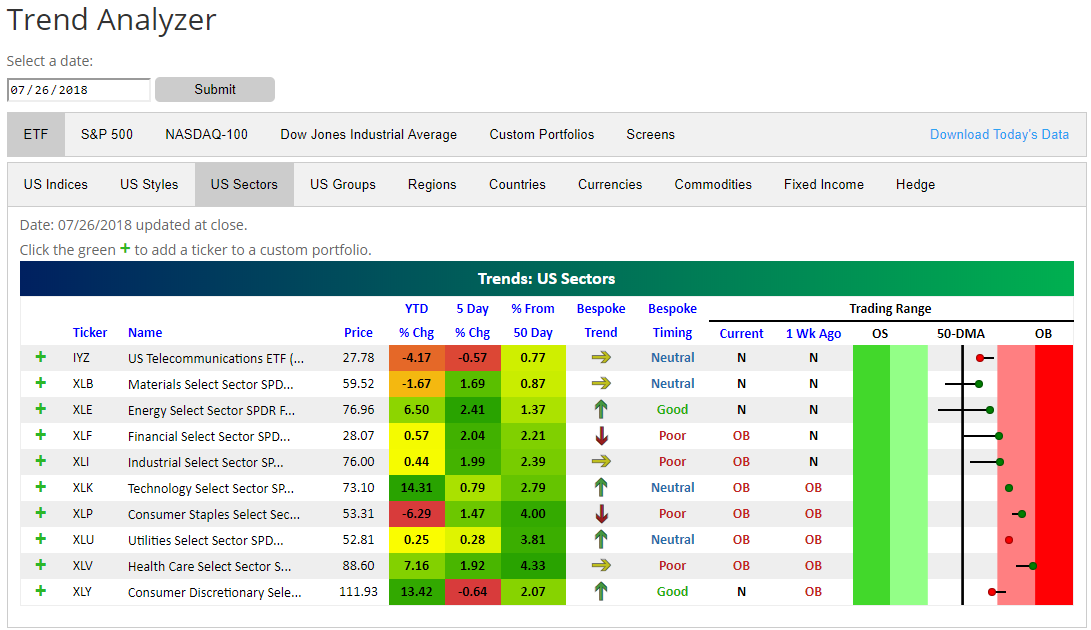

As shown in the snapshot of our Trend Analyzer tool below (available to Bespoke Premium and Bespoke Institutional members), every sector is now back above its 50-day moving average. This is a sign that the market is back to getting broad participation — something that wasn’t the case a few weeks ago when it was only Tech and Consumer Discretionary driving the gains.

The Closer — FAANG & AMZN Earnings, Economic Chart Attack — 7/26/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at the performance of the S&P 500 after stripping out the effects of the FAANG stocks. We also review Amazon earnings before moving on to a review of economic data released today: manufacturing new orders, shipments, and inventories, preliminary trade data, manufacturing activity in the KC Fed district, quarterly homeownership and household formation data, and quarterly gross job creation by type of establishment.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bespoke’s Sector Snapshot — 7/26/18

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a two-week free trial to Bespoke Premium now.

Below is one of the many charts included in this week’s Sector Snapshot, which shows the percentage of stocks in each sector trading above their 50-day moving averages. At the moment, 73% of S&P 500 stocks are above their 50-DMAs, which is a very healthy reading.

To find out what this means and to see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.

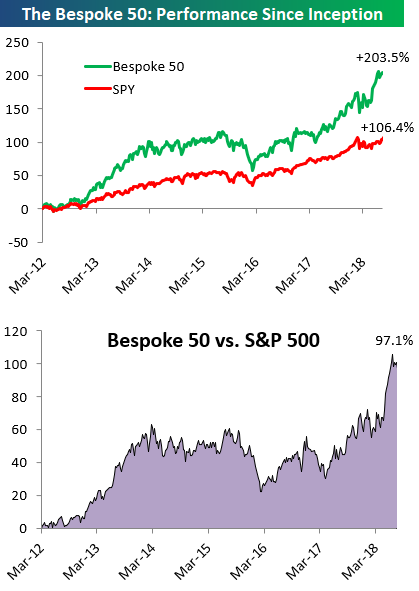

the Bespoke 50 — 7/26/18

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 97.1 percentage points. Through today, the “Bespoke 50” is up 203.5% since inception versus the S&P 500’s gain of 106.4%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

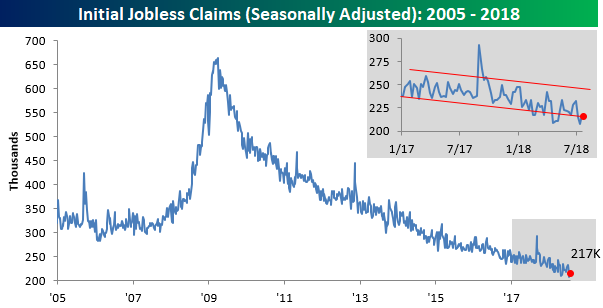

No Cracks in the Jobs Market

While recent residential housing data has been showing some cracks, the employment picture continues to look robust. This week’s latest read on initial jobless claims provides the latest example. Although the report came in slightly higher than expected (217K vs 215K), by just about any measure it’s an extraordinarily low reading. As we update readers every week, this week’s reading marks the 42nd straight week where claims have been at or below 250K and the record 177th straight week where claims have been under 300K.

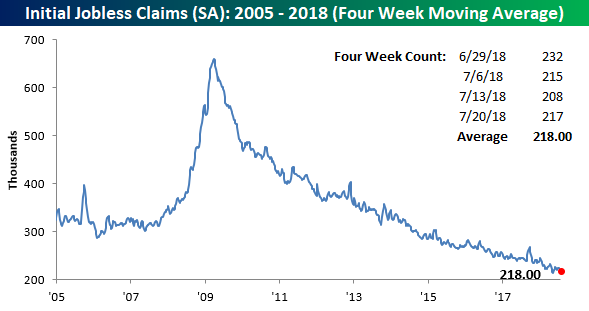

With another sub 220K reading, the four-week moving average also started to move meaningfully lower this week, falling from 220.75K down to 218K. This reading is now within 5K of its multi-decade low of 213.5K from early May, and if next week’s reading comes in below 214K, we’ll see a new low.

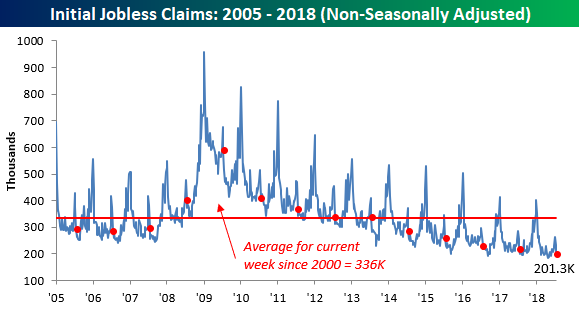

On a non-seasonally adjusted (NSA) basis, jobless claims fell from 232.2K down to 201.3K. For the current week of the year, this is the lowest reading on record, and going back to 2000, it is more than 134K below the average for the current week.

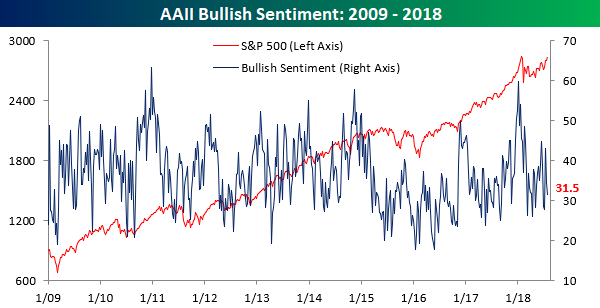

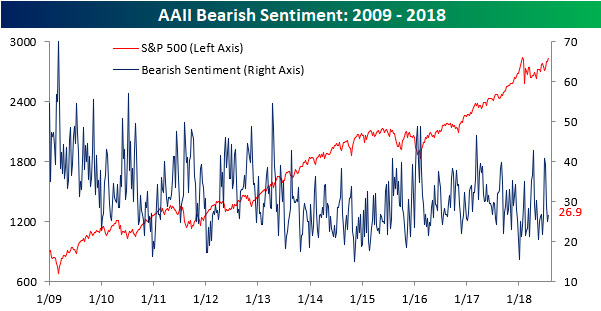

Bullish Sentiment Declines For the Second Straight Week

In the last two weeks, the S&P 500 has rallied 1.5% and broken out above significant resistance at the 2,800 level. With that kind of move, you would expect to see an uptick in optimism from individual investors. Based on the latest AAII survey data, though, we have seen the opposite. According to this week’s report, bullish sentiment declined for the second week in a row, falling from 34.66% down to 31.52%.

As bullish sentiment declined, bearish sentiment ticked up from just under 25% to just under 27%.

The plurality of investors, however, are still on the fence. As shown in the chart below, neutral sentiment in this week’s survey increased from 40.4% up to 41.58%. That’s the highest level since mid-May. Sentiment is a major driver of stock prices and is a topic we cover regularly in reports for clients. To stay on top of the latest sentiment trends, you can start a two-week free trial to Bespoke Institutional.