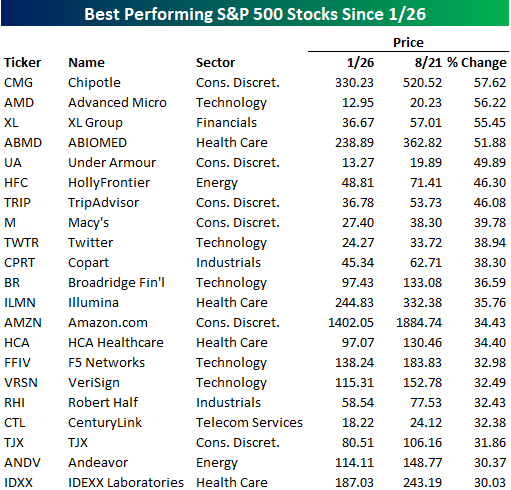

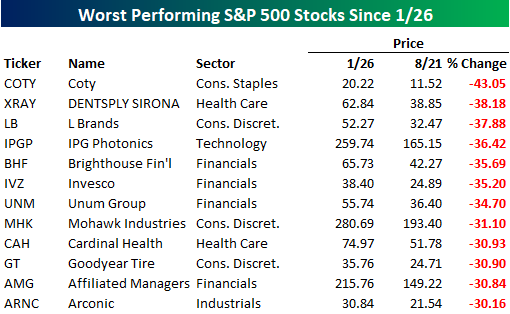

Best and Worst S&P 500 Stocks on the Road to Nowhere

Many are out making a big deal about the fact that the S&P 500 traded back to a new all-time high today, but the reality is that the S&P 500 has been ‘dead money’ for nearly seven months now. Along with the index itself being unchanged since late January, a very slight majority of stocks (256) in the S&P are lower now than they were on 1/26, and overall, the average change of the 500 individual stocks in the index since then is a decline of 0.35%. At the extremes, though, there have been some big winners and losers. We’ll start with the good news.

The table below lists the 21 stocks in the S&P 500 that have gained more than 30% since the S&P 500’s 1/26 closing high. Topping the list of biggest winners is Chipotle (CMG), which has been on quite a run, gaining more than 57% even after taking a skid last week on reports of further health issues with customers eating their food. Right behind Chipotle, although it may not want to get too close, is AMD, which is up 56%. Behind these two leaders, two other stocks (XL Group and ABIOMED) are up over 50%. Other notable names on the list of biggest winners include Under Armour (UA) and Twitter (TWTR). Also worth pointing out is that besides Amazon.com (AMZN), none of the other FAANG stocks made the list. So much for the argument that FAANG stocks are the only ones going up.

While there have been 21 S&P 500 stocks that have rallied 30% or more since 1/26, 12 stocks in the S&P 500 have lost more than 30% during that span. The biggest loser of them all has been Coty (COTY), which is down over 43%, including a drop of 7% today. L Brands (LB) is another big loser as it has seen its stock fall more than 37% since 1/26. Thankfully for most investors, there are not a lot of high-profile names on this list, but if you’re a holder of any of these names, it has definitely been a frustrating six months.

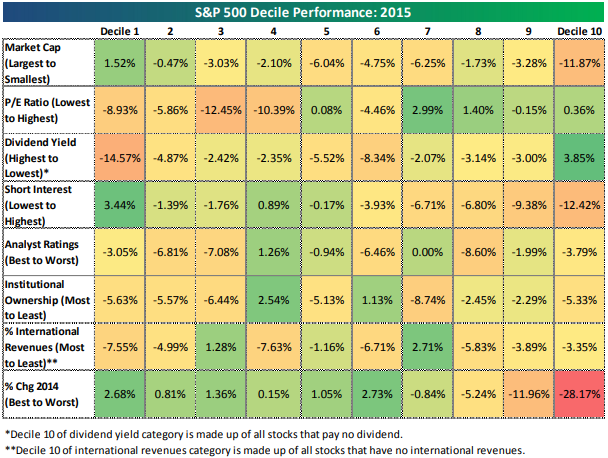

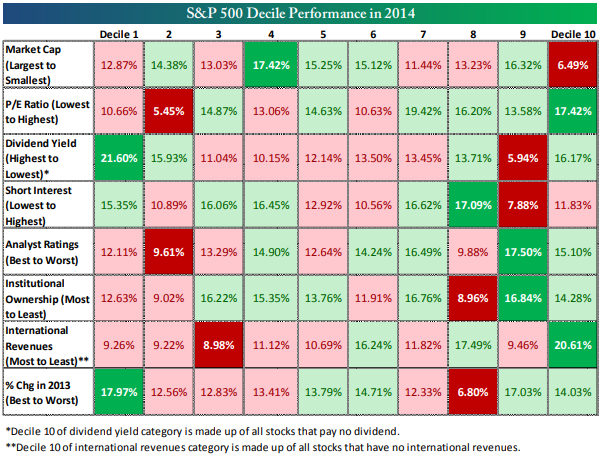

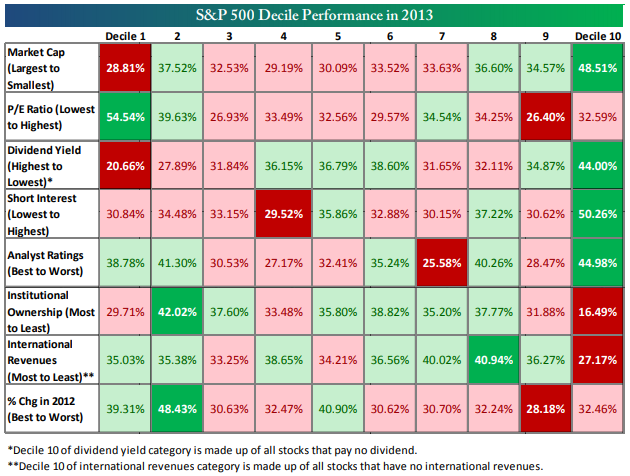

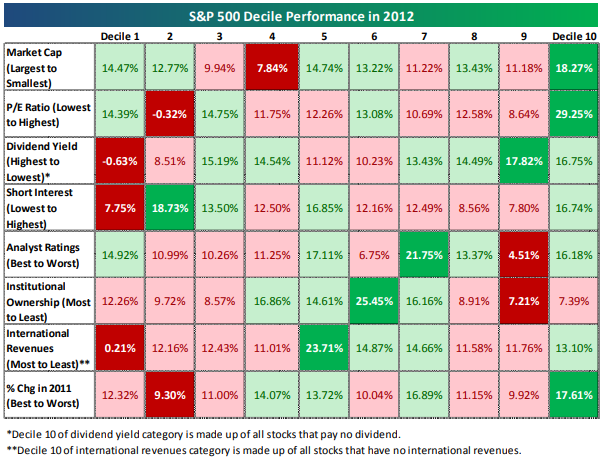

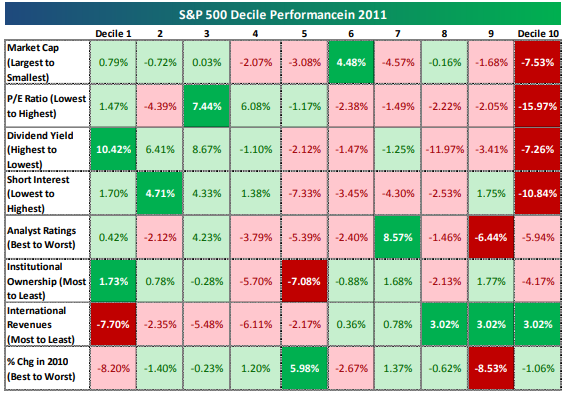

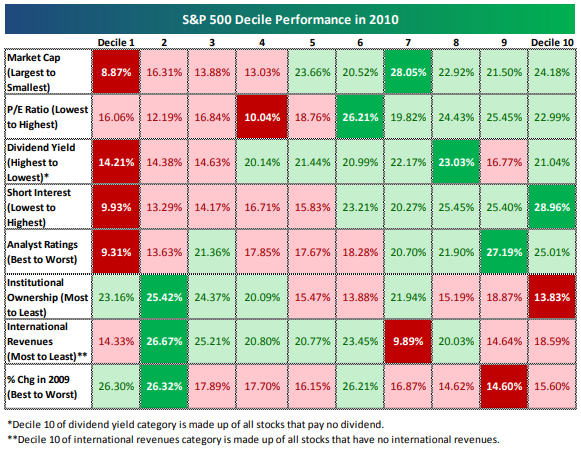

S&P 500 Annual Decile Analysis

2017

2016

2015

2014

2013

2012

2011

2010

2009

COTD: Hurricane-Force Seasonal Tailwinds

Bespoke Stock Scores — 8/21/18

The Closer — Spooz Steady Intraday, Turkish Trade Math — 8/17/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we take a look at the change in intraday trading patterns since the stock market began to rally consistently off Q1 lows. We also review Turkey’s current account and what it could take to close its enormous deficit.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Consumer Staples Leading

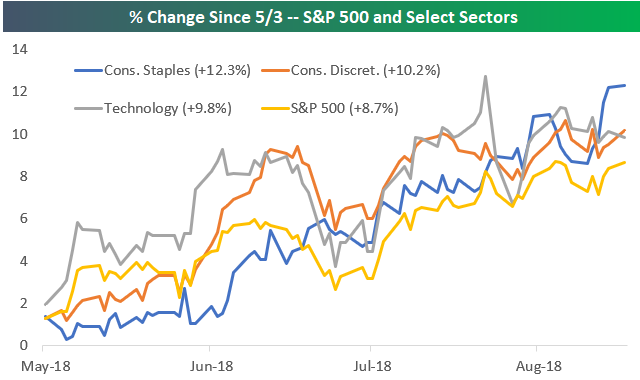

The Consumer Staples sector has been on fire lately. As shown in the snapshot from our Trend Analyzer tool below, Staples is up more than any other sector over the last week (+3.29%), and it’s now trading in extreme overbought territory at two standard deviations above its 50-day moving average.

Back in early May, the Consumer Staples sector was down more than 14% year-to-date, but it has gained back nearly all of its losses. As shown below, Staples is now down just 3.9% year-to-date. Unfortunately, Staples is still well behind its counterpart — Consumer Discretionary — which is up 14.7% on the year.

As you can see in the chart above, the first four months of the year were horrific for Consumer Staples. But since the sector hit its low for the year at the start of May, it’s been a different story.

Since May 3rd, Consumer Staples is actually outperforming the S&P 500, Consumer Discretionary, and even Technology:

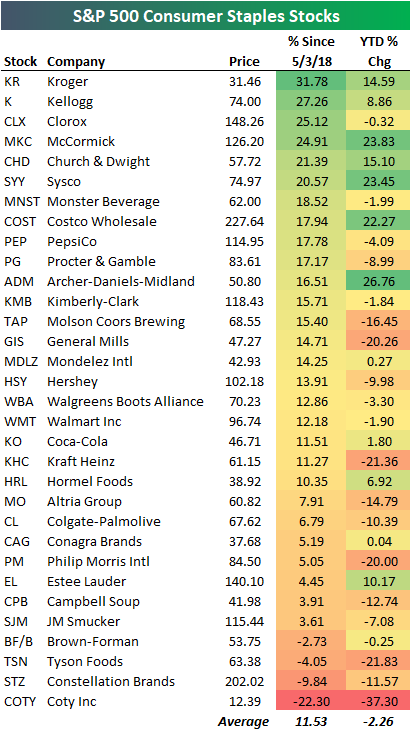

Below is a table showing the performance of S&P 500 Consumer Staples stocks on a year-to-date basis and since the sector’s May 3rd low. As shown, all but four stocks in the sector are up since May 3rd, while six are up more than 20%. Grocery store chain Kroger (KR) is up the most since May 3rd with a gain of 31.78%, followed by Kellogg (K), Clorox (CLX), and McCormick (MKC) all with gains of more than 24%.

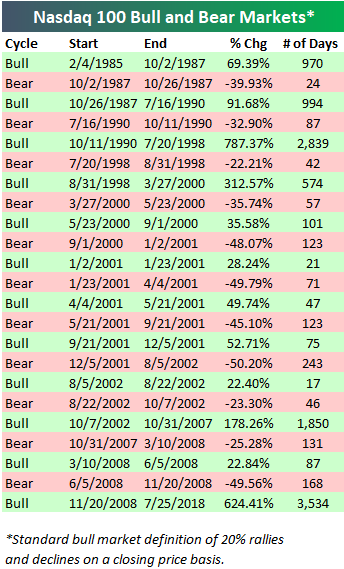

The Real Longest Bull Market Ever

We’ve read or heard a number of erroneous reports lately claiming that we’re about to set the record for the longest S&P 500 bull market on record. Since the S&P 500 made its last bull market closing high on January 26th, the bull market actually stopped aging on that date, and we’ve essentially been in limbo since. (You can read more on this topic in this post we published late last week.)

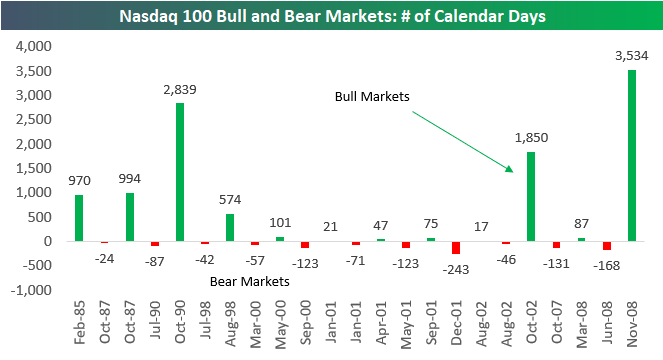

But while the bull market for the S&P 500 really isn’t the longest on record, another major US index just set the record for its longest bull market ever.

The Nasdaq 100’s current bull market has lasted 3,534 calendar days (from 11/20/08 through its most recent high on 7/25/18). As shown in the chart below, that’s easily its longest on record since the index began in 1985.

While the current Nasdaq 100 bull is easily the longest on record, it’s still not the strongest. The 1990s bull that ran from October 1990 through July 1998 saw the index gain 787.37% before it eventually fell into a short bear market in July/August ’98. The current bull for the Nasdaq has only seen a gain of 624.41%.

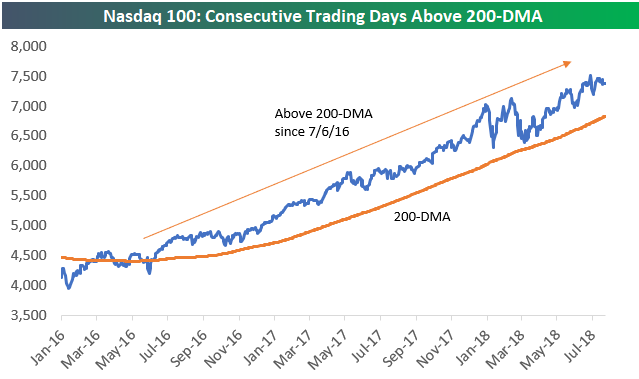

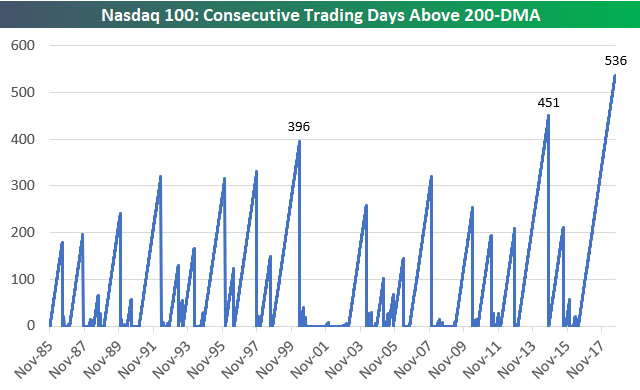

In addition to being in its longest bull market ever, the Nasdaq 100 is also in the midst of another record streak.

As shown below, the index has now closed above its 200-day moving average for a record 536 trading days dating back to July 6th, 2016. That’s well above the 396-trading day streak that ended in May 2000 and the 451-trading day streak that ended in October 2014.

See Bespoke’s most actionable stock market research with a Bespoke Premium free trial.

Chart of the Day: 2000 vs 2018 – Similar But Very Different

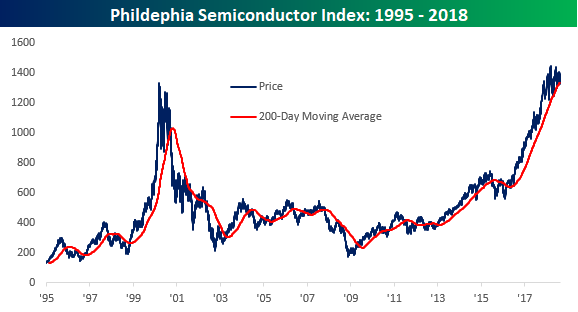

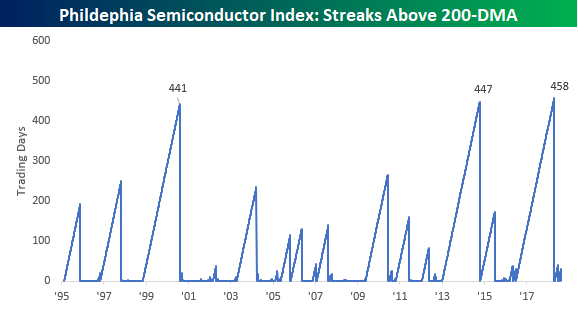

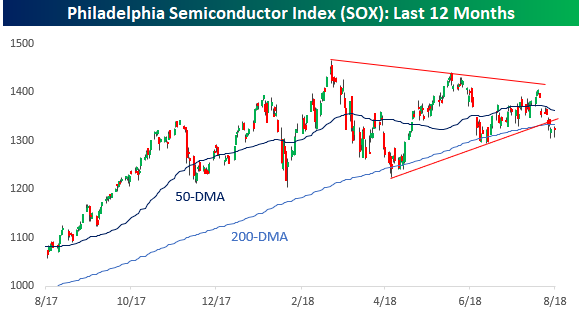

This Sox

For much of the two-plus years since the Brexit vote in June 2016, semiconductors were one of, if not, the market’s biggest leaders. From the time it broke out in mid-2016 through its highs earlier this year, the Philadelphia Semiconductor Index (SOX) more than doubled, taking out its dot-com highs in the process.

Another notable aspect of the rally in semis during that span is that the group saw a record run of 458 consecutive daily closes above its 200-day moving average. Going back to 1995, this was just the third such streak of more than 400 consecutive closes above the 200-DMA, only eking out the two other streaks from 1999/2000 and 2013/2014 by a number of days.

For much of the last 20+ years, semiconductors have been considered a leading indicator for the Technology sector, if not the market as a whole. While trends tend to change over time as certain sectors of the economy lose their relevance and are overtaken by others, recent price action in the semis has been a bit concerning. When the SOX first broke its streak of consecutive closes above the 200-DMA back in April, it quickly bounced back more than 15%. While the snapback was impressive, the rally stalled out short of a new high and pulled back down to its 200-DMA. On the second test of its 200-DMA in early July, the SOX bounced again, but that rally not only failed short of a new high, it also came up short of the prior lower high.

Since that most recent lower high, the SOX has once again broken below its 200-DMA and still has yet to bounce. Not only that, but if it doesn’t find its footing soon, it will become increasingly likely that the SOX will fall below levels seen in early July, resulting in a lower low. Two lower highs followed by a lower low? From a technical perspective, that wouldn’t be an especially promising pattern.

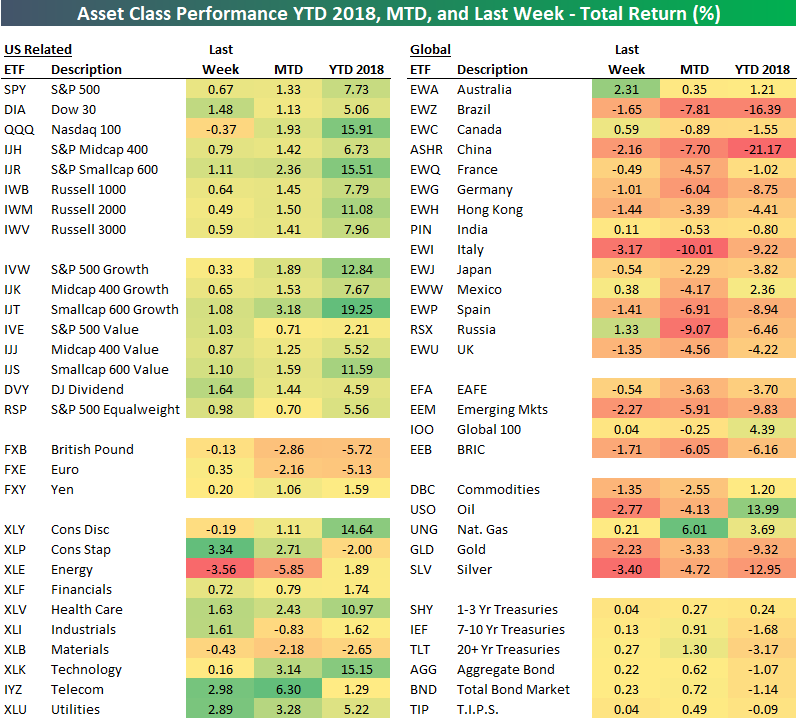

Bespoke Asset Class Performance Matrix

Below is our total return ETF matrix highlighting the performance of various asset classes from the perspective of a US investor.

With a solid end to the week on Friday, US equities finished the week with across the board gains as all of the major averages with the exception of the tech-heavy Nasdaq 100 (QQQ) finished in the green. Don’t feel too bad for the Nasdaq, though, as it is still up nearly 2% MTD and over 15% on the year. The biggest laggard of the major US index ETFs on a YTD basis has been the Dow (DIA) with its YTD gain of 5.06%, and that’s after taking into account its leading 1.48% gain last week.

On a sector by sector basis, defensive stocks led the way higher as Consumer Staples (XLP), Telecom Services (IYZ), and Utilities (XLU) all had gains of close to 3% or more. On the downside, commodities related stocks took it on the chin with Energy (XLE) falling over 3.5% and Materials (XLB) dropping 0.43%.

Outside of the US, it was a rough week for global equities. Italy (EWI) was the biggest decliner with a drop of 3%, which brings its MTD decline to more than 10%. Not far behind Italy, though, Russia (RSX) is down over 9% even after rising more than 1% last week, while Brazil (EWZ) and China (ASHR) are both down more than 7%. On the year, China is down over 21% and Brazil is down more than 16%. Just to illustrate how bad a year it has been for international equities from the perspective of a US investor, the only two countries we track in the matrix that are up on the year are Australia (EWA), which was actually down heading into the week, and Mexico (EWW).

In the commodities sector, outside of Natural Gas (UNG), all of the commodities ETFs we track were down on the week (hence the weakness in Energy and Materials sectors).

Finally, we saw marginal gains in fixed income, with slightly more strength at the longer end of the curve as 20+ year Treasuries were up 0.27%.