Morning Lineup – Get Ready For the Circus

US equity futures are slightly higher this morning as the markets try to recover from yesterday’s post-FOMC swoon, but things are really likely to quiet down shortly after the open this morning when the Kavanaugh hearing kicks off at 10 AM.

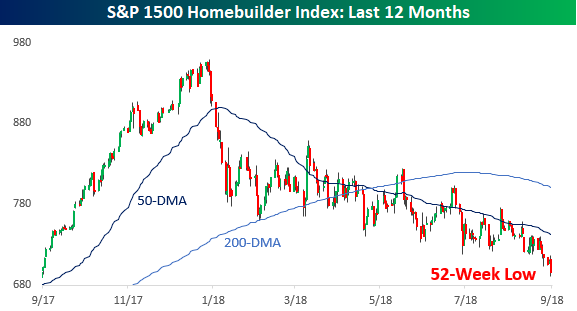

While the broader market continues to trade right near all-time highs, a number of key areas of the market are not only missing out of the party, but they’re at 52-week lows. Exhibit A is the homebuilders (chart below), but along with them, stocks like Whirlpool (WHR), and Bed, Bath, and Beyond (BBY) are also at multi-year lows, while the two ‘generals’ of General Electric (GE) and General Motors (GM) are acting more like ‘privates’.

It’s still earnings off-season, but from the few reports we have seen so far, companies aren’t exactly wowing investors. We first highlighted this in last week’s Bespoke Report, but this week we are seeing the trend continue a bit as just over half of companies reporting managed to exceed their revenue forecasts. Once earnings season comes, they are going to have to do better than that!

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Trend Analyzer – 9/27/18 – Nasdaq is the Sole Survivor

In reaction to the Fed hiking rates yesterday, equity markets fell with some areas seeing greater declines than others. Every major US Index ETF has moved below where it stood this time last week, with the exception being the Nasdaq 100 (QQQ). Up the most YTD of all these indices, it almost should not come as a surprise that it has withstood the hit of the Fed Day, still up 1.04% over the past 5 trading days. It was also the only ETF of this group to have seen any gains at all at the close. Every other major US Index ETF was down on the day. QQQ, along with the Dow (DIA), is the only remaining overbought ETF. All others have moved to neutral.

The Closer — Fed Hikes, Banks & Builders Falter — 9/26/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we recap the Fed decision today before diving into the collapse of bank stocks, new home sales data, and the decline in homebuilder stocks. We also recap EIA petroleum market data along with recent Energy price action.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

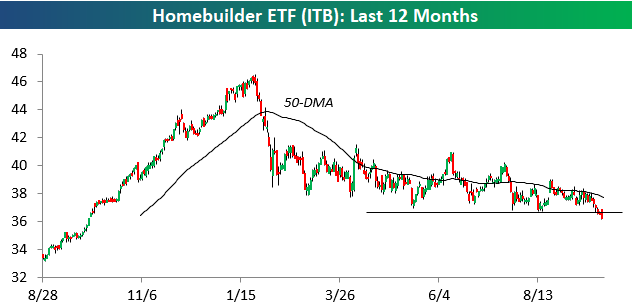

Homebuilders Continue to Break Down

While the S&P 500 didn’t go negative until the end of the trading day following the Fed’s rate hike, the homebuilder stocks were down on the day much earlier.

After initially gapping higher at the open following what appeared to be a strong earnings report, KB Homes (KBH) quickly reversed its gains to trade lower by 3% in morning trading. The reversal lower from KBH sent the entire homebuilder group into the red, and as shown below, the homebuilder ETF (ITB) went on to make a new 52-week low today.

As the broad US market and most sectors have traded to new highs lately, the homebuilders have been trading terribly. A month ago, we saw Toll Brothers (TOL) trade positively in reaction to earnings only to give nearly all of it back over the last few weeks. Today we saw KBH initially trade higher on earnings before sellers quickly started hitting bids. Investors can’t seem to get out of the group quick enough lately.

Below is a chart comparing US Housing Starts to the homebuilder stocks going back to 2006. As you can see, prior to 2017, the two tracked each other extremely closely. Last year, though, the homebuilder stocks diverged from Starts by going on an epic run higher. Starts just couldn’t keep up.

So far in 2018, Starts have continued to trade sideways, so it appears as though the homebuilder stocks simply got ahead of themselves last year and are now mean reverting to get more in line with the historical relationship.

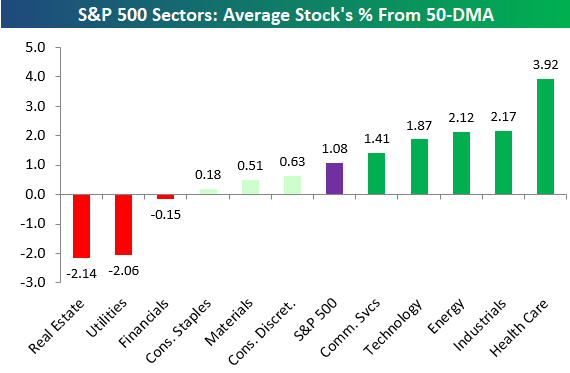

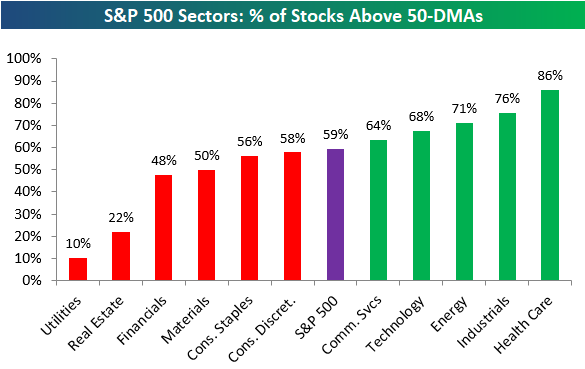

New S&P 500 Sector Breadth Levels

Below is a look at the average stock’s distance from its 50-day moving average using the new GICS sector re-classifications that were made earlier this week. As shown, the average stock in the broad S&P 500 is 1.08% above its 50-day moving average, while Health Care stocks are the most extended at +3.92%. Four other sectors have readings above the overall average — Industrials, Energy, Technology, and the new Communication Services sector.

On the downside, there are three sectors with negative readings. The average Real Estate stock is 2.14% below its 50-DMA, which is the weakest of any sector. Utilities and Financials are the two other sectors in the red.

In terms of breadth, 59% of S&P 500 stocks are above their 50-day moving averages, and five sectors have stronger readings than that — Health Care (86%), Industrials (76%), Energy (71%), Technology (68%), and Communication Services (64%).

Just 10% of Utilities stocks are above their 50-day moving averages, which is by far the weakest breadth reading of any sector. Financials and Real Estate are the only other sectors with readings below 50%.

For Bespoke’s in-depth sector analysis, start a two-week free trial to Bespoke Premium.

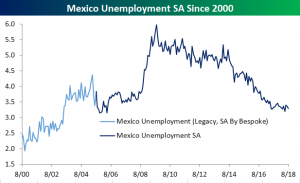

Mexico Unemployment Improves Again

This morning, Mexican Unemployment for the month of August declined to a seasonally adjusted rate of 3.29% versus estimates for a reading of 3.33%. Coming off of July’s 3.35% and a June uptick to 3.4%, we have now seen a continual downtrend in unemployment over the course of the past several years. While this month’s reported data is by no means a record low, Mexico is closing back in on the May low when unemployment sat at its lowest level since May 2006. We are currently sitting right around pre-crisis levels, but are still well above the lows of ~2% from the early 2000s. This positive data comes on the backs of Mexico and the United States working to create a trade agreement to replace NAFTA, but that development is not likely to have an impact on hard data any time soon given the fact that the US and Mexico would have to withdraw from NAFTA for the bilateral agreement to go into effect.

Note: in the graph above, data predating September 2005 is NSA legacy data that Bespoke has seasonally adjusted.

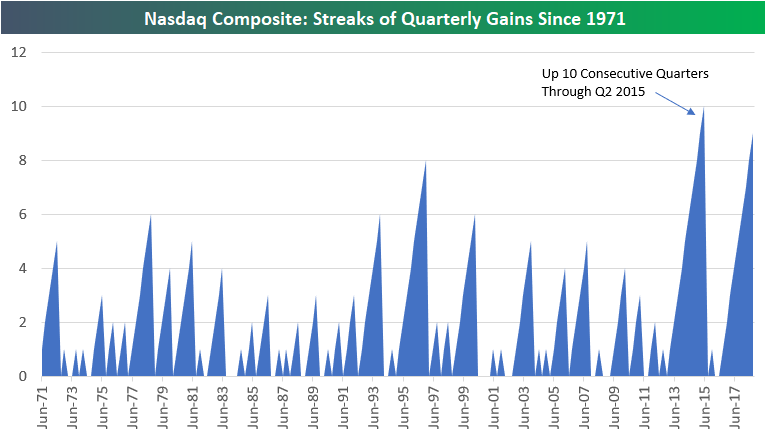

Nasdaq Up 9 Quarters in a Row…Again

The Nasdaq Composite is set to finish higher for the 9th consecutive quarter when exchanges close this Friday, September 28th. (With a QTD gain of more than 6%, it would take a dramatic plunge over the next two trading days for the quarter to end in the red.)

Below is a chart showing streaks of quarterly gains for the Nasdaq Composite since its inception in 1971.

Nine quarters of gains is not quite the longest streak on record, and it’s not even the longest streak of the last six years! The longest stretch of quarterly gains made it to ten from Q1 2013 through Q2 2015. Prior to that, the record was 8 quarters back in the mid-1990s (Q1 1995 through Q4 1996). Not even during the Dot Com boom of the late 1990s did we see such consistency of gains for the Nasdaq.

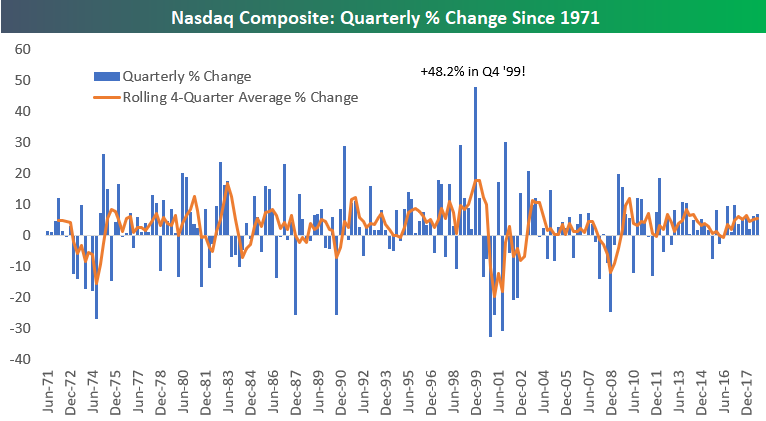

While the Nasdaq has been more consistent to the upside during this bull market than it was during its epic late-1990s rally, the size of the quarterly gains seen this time around don’t come close to matching the rallies seen back then. In the chart below, we show the quarterly price change for the Nasdaq going back to 1971. Yes, we’ve seen very nice quarterly gains of 5-10% many times during the current bull, but from 1997 through Q1 2000, the Nasdaq posted seven double-digit quarterly percentage gains, including a gain of 29.5% in Q4 1998 and a ridiculous 48.2% gain in Q4 1999. This period is nothing like the 1990s.

Chart of the Day: Nasdaq at 100 Again

Fixed Income Weekly – 9/26/18

Searching for ways to better understand the fixed income space or looking for actionable ideals in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

This week we take a look at the basis swap market.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!