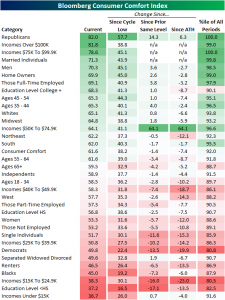

Consumer Comfort Makes Another High

The Bloomberg Consumer Comfort Index has once again made another new high for the current cycle rising to 61.6 from last week’s 61.2. Not only is it an impressive release for the current cycle, but it is also at the highest level since the final days of 2000— one year after the index had hit its all-time highs. This data echoes a jump in bullish sentiment among individual investors that was also released earlier today. Optimism seems to be growing across the board.

Breaking the report down further into demographics, politics has had a strong impact on comfort readings. As you can see in the chart below, the party in power typically boosts comfort among its members and vice versa. Republicans currently top the chart with the highest comfort of all groups. The most recent release actually posted the highest comfort in the history of the survey (since 1990) for Republicans. Meanwhile, Democrats’ comfort is unsurprisingly significantly lower. Despite this, this group’s comfort has actually been climbing for several weeks now to its highest level since June. Drama over Supreme Court justices amid the wider trend of political polarization has not necessarily slowed consumer comfort on either side of the aisle.

Looking at income levels, there is a clear split at $50k. Income earners between $75K to $99.9K are sitting at their all-time high in terms of confidence, while the $100K and over group is not far behind. On the other hand, those making under $50K understandably have a much lower comfort level, but they are not at historically low readings. Incomes between $15K and $24.9K are currently in the lowest percentile of all demographics, while the lowest income demographic of under $15k actually sits in the 91st percentile only 0.7 points from its all-time high.

Some other honorable mentions are the homeowners, who despite weak housing market data claimed comfort in the 99th percentile. Conversely, renters are sitting relatively low on the list. Married individuals are within one point of their all-time high alongside college-educated individuals. There is also a discrepancy between comfort levels among men (70.3) and women (53.3).

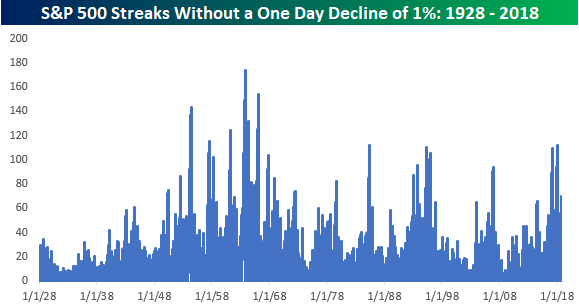

First 1% Decline Since June?

The S&P 500 is currently trading down just over 1%, and if these declines hold through the closing bell, it would be the first decline of 1% or more for the index since late June. At 70 trading days, the current streak ranks as the third longest of the bull market behind the 109 trading day streak that ended in March 2017 and the 112 trading day streak that ended earlier this year. Besides those two streaks, the only other streak that was nearly as long was the one that ended in July 2014 at 66 trading days.

While the current streak of days without a 1% decline is long relative to recent history, from a wider lens, there have been a number of streaks that lasted longer. The chart below shows all S&P 500 streaks without a 1% decline in the S&P’s history. In the post-WWII period, there have actually been 24 streaks that lasted longer with the bulk of those coming in the 1950s/1960s. The longest streak ended in November 1963 at 174 trading days. Considering how painful the decline feels today, can you imagine how bad it felt in 1963 when the S&P 500 finally declined more than 1% after going eight months without one?

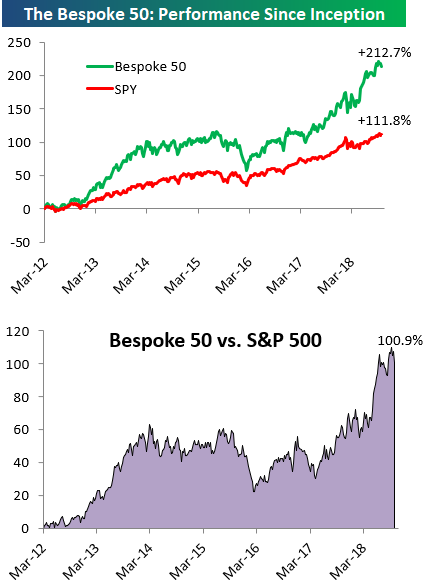

the Bespoke 50 — 10/4/18

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 100.9 percentage points. Through today, the “Bespoke 50” is up 212.7% since inception versus the S&P 500’s gain of 111.8%. Always remember, though, that past performance is no guarantee of future returns.

To view our “Bespoke 50” list of top growth stocks, click the button below and start a trial to either Bespoke Premium or Bespoke Institutional.

Chart of the Day: Albemarle Acting Awesome

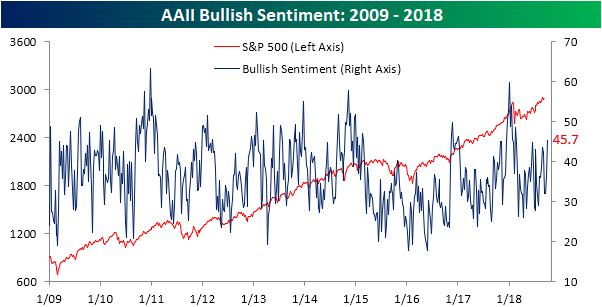

Individual Investor Sentiment – Uh Oh

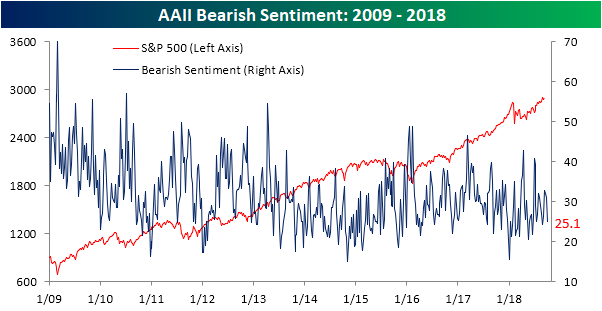

With the Dow suddenly hitting record highs on what seems like a daily basis, you would expect to see individual investor sentiment improve, and that’s exactly what we saw this week. According to the weekly sentiment survey from AAII, bullish sentiment surged 9.4 percentage points to 45.66% from last week’s reading of 36.22%. That move represents the largest one week increase since early July and the highest weekly reading since mid-February. While we’re not quite at the 50% reading yet, we would note that the last time optimism in this survey neared the 50% level was in late December. That wasn’t the exact top of the market right before the correction, but it was close to it.

While bullish sentiment starts to rise, bearish sentiment is back down in the mid-20 percent range, which is a level it has seen repeatedly throughout the year.

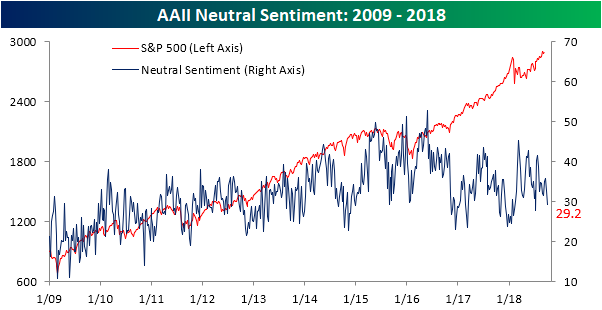

So if all the new bulls didn’t come out of the bearish camp, where did they come from? As shown in the chart below, the pool of undecideds continues to shrink as it fell from just under 33% last week to 29.22% this week. That’s the lowest level since mid-July.

Jobless Claims Move Back Down

After a week where jobless claims ‘surged’ to 215K, this week they resumed their downward trend falling to 207K versus expectations for a reading of 215K. This now makes it a record 187 straight weeks that claims have been at or below 300K, 52 straight weeks that they have been at or below 250K (longest streak since 1970), and 13 straight weeks where they have been at or below 225K (longest streak since 1969).

Despite the decline in claims this week, the four-week moving average moved slightly higher rising from 206.5 up to 207K. Even with the increase, though, claims are now just 1K above their multi-decade low of 206K from two weeks ago.

On a non-seasonally adjusted (NSA) basis, claims ticked down to 165.2K. For the current week of the year, that’s the lowest reading since 1969, and it’s also more than 117K below the average for the current week of the year dating back to 2000.

Morning Lineup – Yields Busting Out

Global bond yields have been on the rise all night and all morning continuing the trend that started in US Treasuries yesterday. Equity futures are trading lower in reaction, and semis will be an area to watch again as Deutsche Bank is the latest in the chorus of sell-side firms to cut numbers on the group. Despite the uptick in negative analyst commentary, the Philadelphia Semiconductor index has traded up for five straight days. If the sector can squeeze out a sixth straight day of gains in spite of the negative commentary, that could signal a turn for the group.

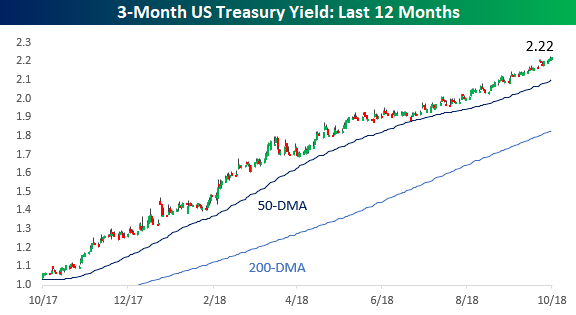

As mentioned above, interest rates are the main focus today. At the short end of the curve, the 3-month Treasury yield continues to move steadily higher hitting a level of 2.22% this morning.

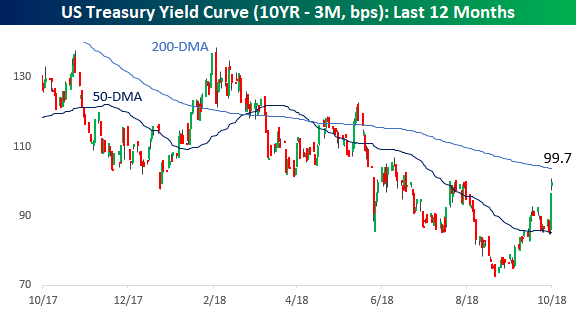

There’s been nothing ‘steady’ about yields at the longer end of the curve, though, as the 10-year yield broke out to 3.22%- its highest yield since 2011!

With that breakout in the long end of the curve, the yield curve has spiked from its recent lows in the 70-bps range to just under 100 bps today.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

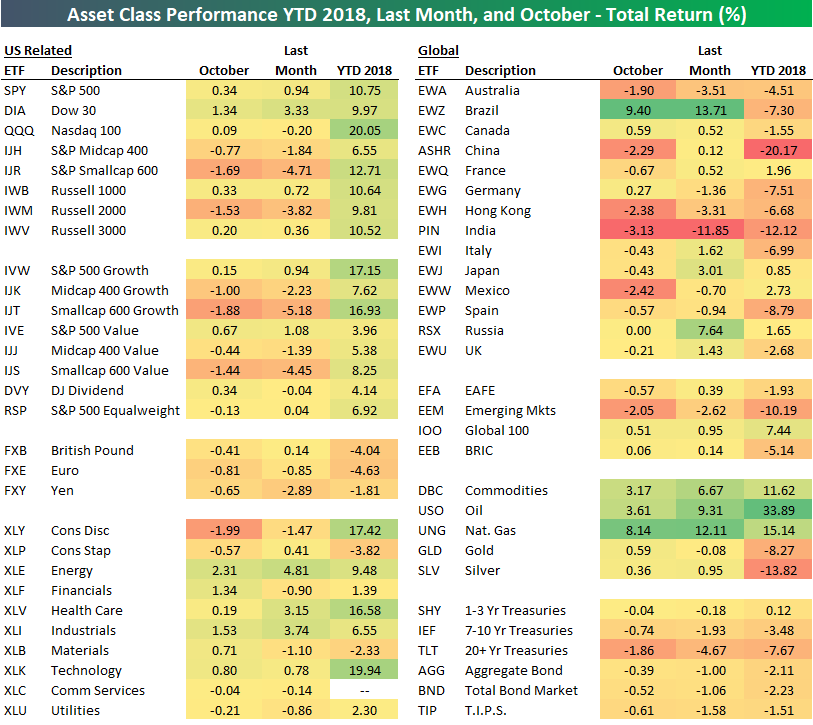

Divergent Start to October

Below is a snapshot of asset class performance to start the month of October. We also include performance over the last month and year-to-date.

The month has gotten off to a pretty strange start, with equity ETFs going in different directions. Small-cap ETFs have gotten hit very hard, while large-caps are in the green. Both consumer sectors are in the red, with Consumer Discretionary (XLY) off by 2% already. On the upside, Energy (XLE), Financials (XLF), and Industrials (XLI) have seen a wave of buying.

Outside of the US, Brazil (EWZ) is already up 9% in October, while India (PIN) is down more than 3%. Prior to September, India had been performing relatively well this year, but an 11.85% drop over the last month has sunk the country’s equity market deep into the red. China (ASHR), Hong Kong (EWH), and Mexico (EWW) are all down more than 2% this month already as well.

Commodities ETFs are on fire, especially energy-related ones. Oil (USO) is up 3.6% month-to-date, while natural gas (UNG) is up 8%. Finally, Treasury ETFs have fallen quite a bit so far in October as interest rates have broken out higher.

The Closer — Bonds Breaking, Hawkish Talk, Brazilian Polls Firming — 10/3/18

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we discuss the rip higher in bond yields today. While investors may focus on the outright levels of yields, more impressive was the steepening of the curve as yields moved up. We also review hawkish Fed speakers that helped precipitate the move as well as a discussion of weekly EIA petroleum market data. Finally, we chart the consolidation of Brazilian polling behind two specific candidates ahead of Sunday’s election.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bespoke Consumer Pulse Report — September 2018

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in year two of Trump’s economy. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.