Bespoke Brunch Reads: 1/27/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Trade

Agent Orange: Trump, Soft Power, and Exports by Andrew Kenan Rose (SSRN)

Using panel data for 157 countries from 2006 – 2017 combined with Gallup data for 5 major economies, the author identifies a two-thirds percent increase in exports for every 1 point increase in other countries’ approval ratings for a leader. [Link]

China Resists U.S., EU Talks on Global Digital Trade Deal, Sources Say by Bryce Baschuk and Shawn Donnan (Bloomberg)

In the background behind bilateral trade disputes, multilateral efforts to agree on a framework for digital trade are not engaging China. [Link; soft paywall]

Retail

Inside The Strange Yet Profitable World Of Retail Arbitrage by Ian Lecklitner (Mel Magazine)

Buying goods at your local Amazon or Target then re-selling them on Amazon can net you a tidy profit; in one case, more than $2500 in a day for a board game trade. [Link]

Real Estate

Hamptons Listings Surge 82% in a Year, Pushing Home Prices Lower by Sydney Maki (Bloomberg)

In December, almost 2200 homes were for sale in the Hamptons, an 82% YoY advance that is a record. Softening demand driven by stock prices, very strong appreciation over the last decade, and tax law changes are all to blame. [Link; soft paywall]

Billionaire Ken Griffin Buys America’s Most Expensive Home for $238 Million by Katherine Clarke (WSJ)

The United States has a new record real estate transaction thanks to the purchase of a New York City penthouse by Citadel co-founder Ken Griffin. [Link; paywall]

Airport Noise NIMBYism by Eli Dourado (Mercatus Center)

Opposition to nuisance airport noise tends to be very concentrated; in one example, 78% of calls to complain about aircraft noise at Reagan International Airport came from one residence (an average of 19 per day). [Link]

Medicine

We may finally know what causes Alzheimer’s – and how to stop it by Debora MacKenzie (New Scientist)

New research suggests that the bacteria which causes common chronic gum disease is the culprit for Alzheimer’s, with the proteins thrown off by the bacteria potentially playing a key role in the evolution of the disease. [Link]

Company sells $80 used tissues, claims to help prepare people for flu season (Fox 5 WTTG)

Vaev is offering used tissues as a method for boosting your immune system, a surprising twist on the usual approach of vaccines. [Link]

CBS Rejects Super Bowl Ad for Medical Marijuana by Craig Giammona (Bloomberg)

A medical marijuana company backed by John Boehner tried to buy ad space during the Super Bowl, but was turned down. [Link; soft paywall]

Stories of the South

Lightning, Struck by Max Blau (Bitter Southerner)

The modern Mercedes-Benz stadium that will host the Super Bowl replaced the Georgia Dome, but the neighborhood that occupied the land prior to the Georgia Dome is mostly forgotten. [Link]

After a casino boom, a Mississippi county deals with a reversal of fortune by Jenny Jarvie (San Diego Tribune)

As gambling development has spread from a few concentrated meccas, traditional temples to gambling have fallen on some very hard times. [Link]

Civil Rights Unionism by Robert Korstad (Jacobin)

The recent history of the South has seen the rise of non-union manufacturing, but the longer history is fascinating, including a Communist-led union of tobacco workers fighting for Civil Rights in the wake of World War Two in the Jim Crow South. [Link]

Industry

Wind Installation Bottleneck Threatens 23% of US Projects by Mary B. Powers (Engineering News-Record)

The unique challenge of moving very large components is creating big headaches for the turbine industry, which is facing a phase-out of tax credits. [Link]

U.S. Oil Production Is 23 Years Ahead of Schedule by David Marino and Stephen Cunningham (Bloomberg)

Last year, the EIA forecasted 2042 oil production in the US would come in around 11.95mm bbl/day, but the industry is on pace to break that high water mark this year alone. [Link; soft paywall]

Vows & Vocations

As If by Design, Their Connection Was Inevitable by Vincent M. Mallozzi (NYT)

Accomplished professor at the M.I.T. Media Lab, former Israeli Air Force first lieutenant, and PhD in computational design Neri Oxman wed the manager of a hedge fund in a January 19th ceremony. [Link; soft paywall]

Norman Goodman, 95, Dies; Summoned Manhattanites to Jury Duty, Like It or Not by Margalit Fox (NYT)

The man who instructed generations of Manhattan residents to appear for jury duty has passed away, leaving behind a colorful career of public service. [Link; soft paywall]

Davos

Remarks delivered at the World Economic Forum by George Soros (georgesoros.com)

Americans often hear the name George Soros as some sort of left wing puppeteer, but the investor’s speech at the World Economic Forum doesn’t read anything like that. It’s acutely focused on the dangerous authoritarianism of China under Xi Jinping, very consistent with his long-term focus on protecting free and open society. [Link]

Chilling Davos: A Bleak Warning on Global Division and Debt by Andrew Ross Sorkin (NYT)

During the World Economic Forum in Davos, Switzerland, a hedge fund manager’s bleak outlook over a global social and political divide is par for the course. [Link; soft paywall]

Polling

A big portion of Trump’s base is breaking from him and would want to end the shutdown without a border wall, new poll shows by Eliza Relmon (Business Insider)

The government shutdown ended (at least temporarily) Friday, but polling released earlier in the week suggests that the President’s base was not sticking with him as he sought wall funding in exchange for re-opening the government. [Link]

Global Warming Concerns Rise Among Americans in New Poll by John Schwartz (NYT)

73 percent of Americans polled at the end of 2018 agreed that global warming was happening, 10 percentage points higher than in 2015; 72 percent say the issue is important to them. [Link; soft paywall]

Gold

Venezuela Wants $1.2 Billion in Gold Back From Bank of England by Patricia Laya, Ethan Bronner, and Tim Ross (Bloomberg)

In order to prevent access to funds for the Venezuelan regime, the Bank of England has denied a request to repatriate the country’s gold reserves from London. [Link; soft paywall]

Crime

I’m Still Around by Samuel Kerr (Medium)

The fascinating and disturbing story of the mid-nineties gang war in Vancouver, including media mistakes, blown prosecutions, vicious murders, and more. [Link]

The Rich

Super Rich Americans Are Getting Younger and Multiplying by Ben Steverman (Bloomberg Quint)

As Baby Boomers age, the largest wealth transfer in history has started, with the average age of those with $25mm or more in assets falling to 47 from 58 in 2014. [Link; soft paywall]

Social Media

Twitter suspends account that helped ignite controversy over viral encounter by Donie O’Sullivan (CNN)

The confrontation in Washington DC last week between a teenaged supporter of Donald Trump and a native American protestor initially caught attention from an account later suspended by Twitter. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a happy New Year!

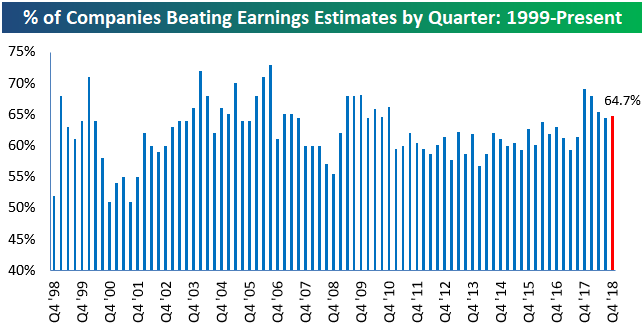

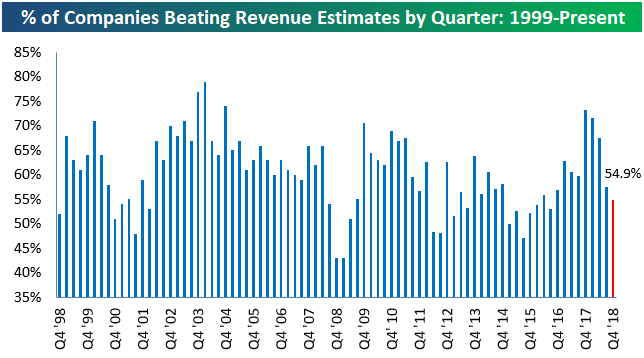

Updated Earnings and Revenue Beat Rate Numbers for Q4 2018

The Q4 2018 earnings season continued to pick up steam this week as another 100+ companies reported. Next week things kick into full gear, however, with an estimated 325+ companies set to report.

Below we take a look at the numbers we’ve seen so far this season. As shown in the first chart below, the bottom-line earnings per share beat rate now stands at 64.7%. This is roughly inline with the final reading seen last quarter, but it’s also low for where we are in the reporting period. Historically, the earnings beat rate drifts lower as earnings season progresses.

The top-line revenue beat rate actually ticked up a bit this week after finishing last week below 50%. As shown below, 54.9% of companies that have reported this season have beaten consensus revenue estimates. Even after the tick higher this week, top-line beats this season remain weaker than normal.

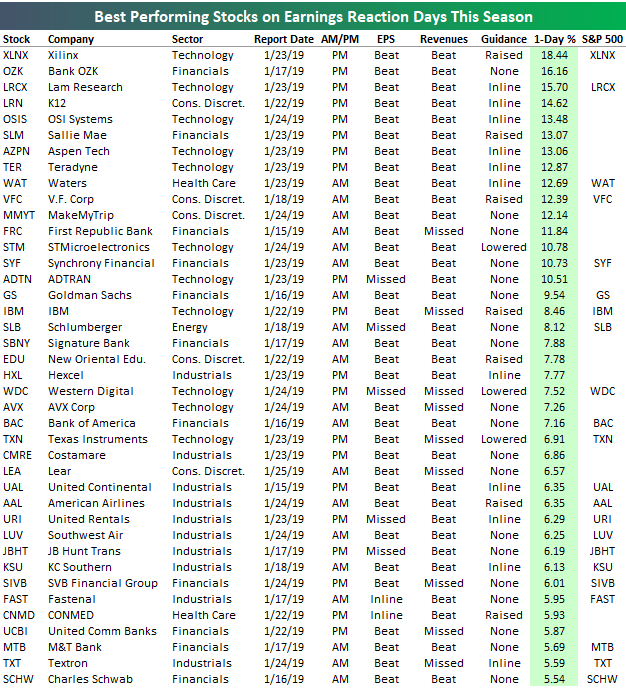

Xilinx (XLNX) Leads the List of Earnings Season Winners So Far

Roughly 200 companies have reported Q4 earnings results since the current reporting period began earlier this month. So how have stock prices been reacting to earnings reports so far this season? Very well.

The average stock that has reported Q4 numbers has gained 1.2% on its earnings reaction day. (The earnings reaction day is the first trading day following a company’s quarterly report. For companies that report before the open, its earnings reaction day is that trading day. For companies that report after the close, its earnings reaction day is the next trading day.) That’s an impressive reading suggesting investors came into the reporting period too bearish.

Below is a list of the 40 best performing stocks on earnings so far this season. Of the 40 stocks listed, 15 gained more than 10% on their earnings reaction days, with semiconductor company Xilinx (XLNX) on top at +18.44%. On January 23rd, XLNX reported an earnings triple play after the close by beating EPS estimates, beating revenue estimates, and raising guidance. Shareholders were rewarded with a one-day gain of nearly 20%.

Bank OZK (OZK) ranks second on the list with a one-day gain of 16.16% following its report on January 17th. Lam Research (LRCX) ranks 3rd at +15.7%, followed by K12 (LRN) and OSI Systems (OSIS). Other notables on the list of big winners this earnings season include Goldman Sachs (GS) with a gain of more than 9%, IBM with a gain of 8.5%, and Bank of America (BAC) with a gain of more than 7%. GS, IBM, and BAC are three blue-chip financials that had been beaten down in the months leading up to their recent reports, and they’re great examples of the newfound strength that many previously struggling financials have shown in recent weeks.

For more in-depth earnings season analysis, start a two-week free trial to Bespoke Institutional. We’ve got an amazing Earnings Explorer tool that you’ll love.

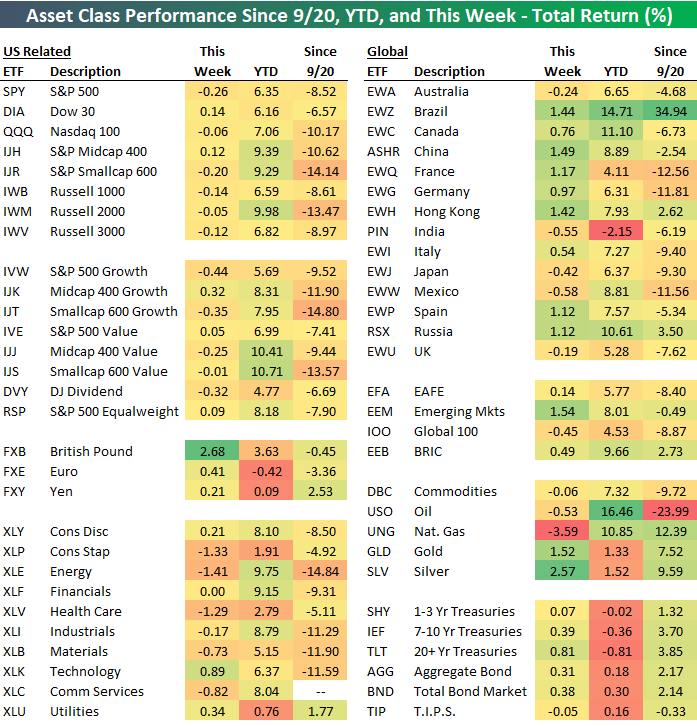

Asset Class Performance YTD Through 1/25 (ETF Matrix)

Below is a look at the recent performance (total returns) of various asset classes using our key ETF matrix. For the week, the S&P 500 (SPY) was down 26 basis points, but it’s still up 6.35% YTD. Since the 9/20/18 peak for SPY, the ETF is now down 8.52%.

While SPY is down 8.52% from its 9/20 high, the Dow 30 (DIA) is down just 6.57%, while the Nasdaq 100 (QQQ) is down 10.17%. Small-caps are down the most from their highs at -14.14% (IJR).

Looking at sectors, it really wasn’t a great week outside of strength in Tech (XLK). Health Care (XLV), Energy (XLE), and Consumer Staples (XLP) were all down more than 1% on the week, while Materials (XLB) and Communication Services (XLC) were down more than 70 basis points. For the year, Energy (XLE) is still up the most, but it’s also down the most of any sector since the 9/20 peak.

International equity markets performed much better than the US this week, and most countries are outperforming the US on a year-to-date basis as well. Brazil (EWZ) continues to post massive gains, returning 1.44% on the week at +14.71% on the year. While SPY is down 8.52% from its 9/20 high, EWZ is up 34.94% over the same time period. The only country struggling this year is India (PIN) with a decline of 2.15%.

Commodities are performing well in 2019, with DBC up 7.32% on the year. Oil (USO) and natural gas (UNG) took a breather this week, but they’re still both up 10%+ on the year. And while gold (GLD) and silver (SLV) are lagging energy commodities so far in 2019, these two precious metals posted nice gains this week. Here’s a closer look at gold’s price chart if you’re interested.

Be sure to read our newest Bespoke Report newsletter, which covers everything you need to know about equities, the economy, and more. You can read it by starting a two-week free trial to any of our three membership levels.

The Bespoke Report – And Then There Was One

US equities took a bit of a breather this week from their torrid rally off the Christmas Eve lows. While anyone long equities would like to see the market trade consistently higher, nothing moves in a straight line. At this point, the sideways trading this week can still be considered nothing more than a pause as the market looks to catch its breath. Next week, though, we should get a lot more clarity on which way this market wants to move as the FOMC will announce its latest views on monetary policy Wednesday, followed by a Jerome Powell Press conference. Just as important, the pace of earnings reports for Q4 will pick up even more steam as nearly a quarter of the S&P 500 (122 companies) will report numbers.

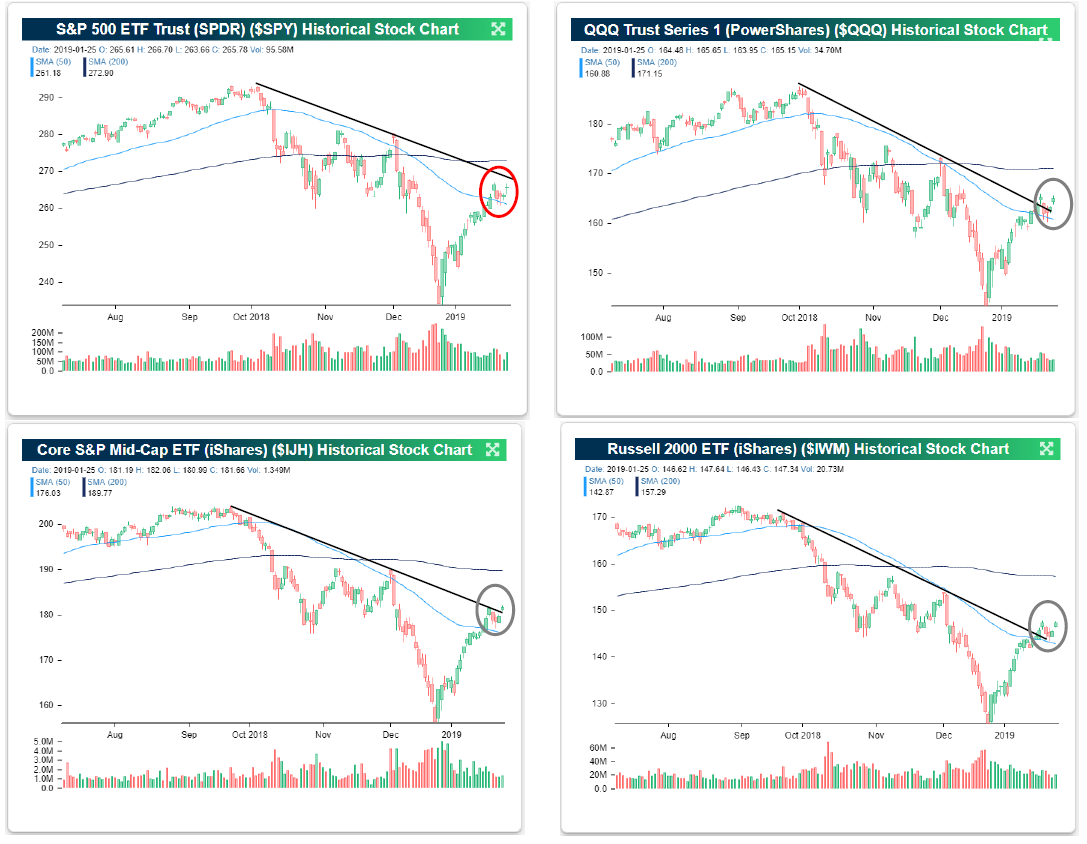

Looking at where some of the major US averages closed out the week, one of these pictures doesn’t look like the others. As shown in the four charts below, in this week’s trading, the Nasdaq 100, the S&P 400 Mid Cap Index, and the Russell 2000 all appear to have broken their downtrends from the October highs. The lone holdout at this point is the S&P 500, which finished the week just shy. Breadth for the S&P 500 has been very strong lately (page 30), so now all we need is price to confirm it. Something tells us that next week we’ll have a good idea either way!

For in-depth analysis of recent price action, sector technicals, earnings season, the economy, and more, start a two-week free trial to one of our three membership levels and read this week’s Bespoke Report newsletter. You won’t be disappointed!

A Golden Day for Gold

Gold had a rough first half of 2018, but the precious metal has been rallying nicely since equity market volatility picked up in Q4. After making a bottom in mid-August last year, gold has taken a number of bullish technical steps to put it in a new multi-month uptrend channel.

As shown below, gold first made a series of higher lows and higher highs to end 2018, breaking two key resistance levels in the process. It has made another big leg higher over the last month or so, and after a slight dip over the last two weeks, today it has popped once again. As of early afternoon trading, gold was testing another resistance level and trying to make a new rally high. If this resistance can be taken out today or early next week, gold bulls will be looking for yet another leg higher.

Emerging Markets ETF (EEM) Makes Strides

The Emerging Markets ETF (EEM) continues to trend higher in 2019 after a horrible 2018 in which it trended lower for basically the entire year. Below is a snapshot of EEM’s chart over the last year. As you can see, every time EEM got near or just above resistance at its 50-day moving average in 2018, it was stopped dead in its tracks. So far this year, the ETF has managed to break and hold solidly above resistance at its 50-day, and in the process it has broken out of the long-term downtrend channel that was in place. Also, the ETF experienced its first “higher low” at the turn of the year, and this week it has made a “higher high” by trading above prior highs seen in December.

After a very rough stretch of bearish trading, there appears to be light at the end of the tunnel for EEM bulls.

Start using Bespoke’s chart tools like the one below with a two-week free trial to Bespoke Institutional!

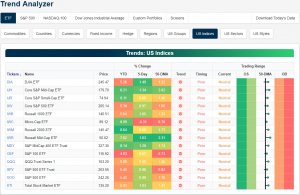

Trend Analyzer – 1/25/19 – Still Neutral

Major US index ETFs in our Trend Analyzer are still in a neutral trading range as they have been for much of the past few weeks. These ETFs have moved slightly closer to overbought territory in the past week but have a ways to go until they get there. Of these names, the Russell Mid-cap (IWR) is the closest to becoming overbought as it is 2.31% above its 50-DMA. IWR is also up the most on the week gaining 1.63%. Other Mid-Cap ETFs like IJH and MDY are some of the others that have seen the largest gains this week. On the other hand, the Micro-Cap (IWC) ETF is the only member of this group that’s down over the last week. Granted, these losses have not pressed it below its 50-DMA.

Morning Lineup – A Positive Close to the Week

Despite a 6% decline from Intel (INTC) in reaction to its Q4 earnings report, US equity futures are looking to close out the week on a positive note. These gains follow strong showings in both Asia overnight and Europe this morning. Read today’s Bespoke Morning Lineup below for major macro and stock-specific news events, updated market internals, and commentary.

Bespoke Morning Lineup – 1/25/19

Breaking downtrends. That seems to be the theme of this week as a number of charts we go through show similar patterns of breaking the short-term downtrends of the fourth quarter. Granted, longer-term downtrends remain in place, but you have to start somewhere! The example we wanted to highlight this morning is Europe’s STOXX 600. As shown in the chart below, after a brief consolidation following the upside break of the 50-DMA, today’s rally has pushed the STOXX 600 above the short-term downtrend that has been in place since last Fall.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bespoke’s Sector Snapshot — 1/24/19

We’ve just released our weekly Sector Snapshot report (see a sample here) for Bespoke Premium and Bespoke Institutional members. Please log-in here to view the report if you’re already a member. If you’re not yet a subscriber and would like to see the report, please start a two-week free trial to Bespoke Premium now.

Below is one of the many charts included in this week’s Sector Snapshot, which shows where each sector is trading relative to its 50-day moving average (the black vertical “N” line). After a period of extreme volatility that saw sectors move deeply oversold and overbought, things have settled down quite a bit over the last two weeks. Not one sector is currently overbought or oversold, which is just how things stood last week at this time as well.

To find out what this means and to see our full Sector Snapshot with additional commentary plus six pages of charts that include analysis of valuations, breadth, technicals, and relative strength, start a two-week free trial to our Bespoke Premium package now. Here’s a breakdown of the products you’ll receive.