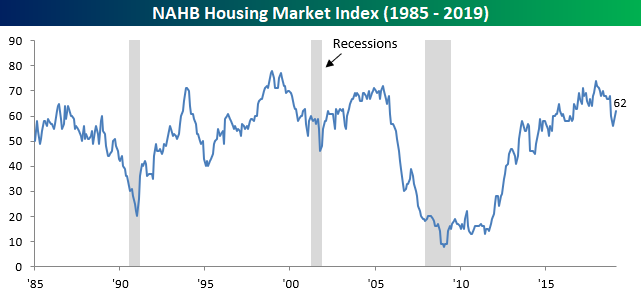

Some Good News on Housing For a Change

We’ve all grown pretty accustomed to weaker than expected housing data over the last several months, but this morning we got some positive news as homebuilder sentiment not only improved in February but also came in higher than expected. According to the NAHB, homebuilder sentiment improved from 58 up to 62 and was three points ahead of consensus expectations. For some perspective, the last time homebuilder sentiment saw a m/m increase of four points was in December 2017.

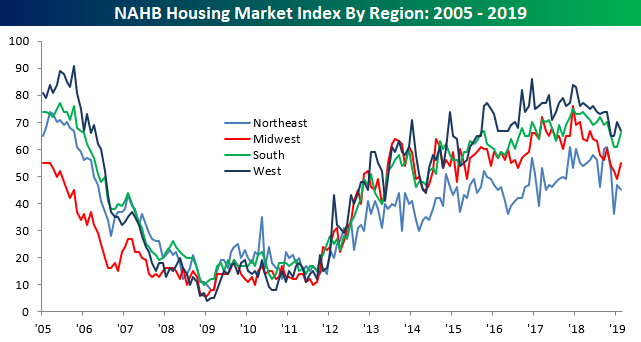

The table below breaks down this month’s report by present and future sales (both increased), traffic (increased), as well as regional sentiment (mixed). Future Sales sentiment saw the largest increase this month, followed by Traffic and Present Sales. On a regional basis, both the Midwest and South saw strong gains, while the West and Northeast saw declines.

While this month’s improvement is welcome, looking at the steep drops we saw over the course of 2018, the general downtrend in sentiment remains intact. In order to indicate a meaningful change in sentiment on the part of homebuilders, it’s going to take a couple of more months of similar reports.

Chart of the Day – 70%+ Of S&P 500 Stocks Overbought

This Week’s Economic Indicators – 2/19/19

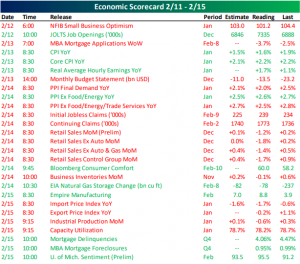

Last week was a fairly busy one for economic data with 30 releases scattered throughout the week. The majority of the reports were either weaker than expected, or in the case of indicators with no estimates, showed a decline versus their last print. There were no indicators on Monday, so the release of January Small Business Optimism from the NFIB kicked off economic data on Tuesday with a greater than expected decline. The most negative aspect of the data last week, though, was Thursday’s Retail Sales report for December, but as we mentioned last week, there are numerous reasons to be skeptical of the data. CPI came out on Wednesday and was slightly stronger on a y/y basis. PPI on Thursday missed estimates, though, and Import and Export Prices were both weaker than expected on Friday, posting y/y declines.

Turning to this week, with the holiday yesterday, the economic calendar takes a bit of a breather. At 10:00 AM today we will get February data on homebuilder sentiment, followed by Mortgage Applications tomorrow. Thursday we will get a flood of data including the Philly Fed, Jobless Claims, Durable Goods, preliminary Markit Manufacturing and Services, Leading Indicators, and Existing Home Sales. There are no scheduled releases for Friday.

Trend Analyzer – 2/19/19 – Not Extreme Yet

Equities rounded out last week with another push higher continuing its impressive run of several consecutive weeks of gains. With markets closed yesterday in observance of President’s Day, today equities are kicking off this week entirely overbought. Of the 14 index ETFs in our Trend Analyzer, all of them are extended well into overbought territory. While not quite at extreme levels (the darker red area of the tool) yet, the indices have inched increasingly closer to there. They have also pushed higher essentially in tandem; none of the indices are drastically more or less overbought than the others. Though as they have been the better performing indices so far this year, small and mid caps are in fact all the furthest above their 50-DMAs. Small caps specifically have seen solid upward movement in the past week (gaining over 4% each) leading them to be the group that is the furthest above the 50-day. Conversely, large caps are still underperforming, but by a smaller margin than they had been.

Morning Lineup – Walmart Ends Earnings Season on a Positive Note

We’ve always considered Walmart’s (WMT) earnings report to mark to unofficial end to earnings season. While there are still plenty of other reports left to get through, the vast majority of companies have already reported their performance metrics for the prior quarter. This morning WMT reported and ended earnings season on a positive note. The company handily exceeded EPS forecasts, revenues were inline with forecasts, and the company reaffirmed guidance. In reaction to the news, shares rallied over 3.5%, and after closing at $99.99 on Friday jumped back above the triple-digit mark this morning. Read all about overnight events around the world and this morning’s news in today’s Morning Lineup.

Bespoke Morning Lineup – 2/19/19

Today’s rally in WMT will mark the fourth straight quarter that the company has had a positive reaction to earnings, but one thing to keep in mind is that following each of those three prior reports it didn’t pay to chase the strength. As our Earnings Explorer tool illustrates, following each of those three prior positive opens, the stock gave up at least some of those initial gains during the trading day.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bespoke Brunch Reads: 2/17/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Recessions

The Financial Crisis at 10: Will We Ever Recover? by Regis Barnichon, Christian Matthes, and Alexander Ziegenbein (FRB SF)

A blog post fleshing out the argument that the drop in the trend of GDP growth following the global financial crisis was a permanent effect of the recession. [Link]

Beware of a Recessionary Bias Among Analysts by Tim Duy (Fed Watch)

Following some notably extreme data points this week, economist Tim Duy cautions against cherry-picking data, and instead advocates a more comprehensive analysis which yields very different conclusions. [Link]

Distress Dynamics

Distressed Mergers And Acquisitions (Wachtell, Lipton, Rosen & Katz)

A very useful background on the area of distressed M&A, which investors may find useful as a piece of reference material or as an initial foray into the special situations space. [Link; 241 page PDF]

Why Banks Can’t Be a Bridge Over Troubled Markets by Paul J. Davies (WSJ)

Linking capital requirements to VaR calculations which raise the capital cost of inventorying securities during periods of high volatility could have negative side-effects down the line. [Link; paywall]

Criminal “Justice”

The NYPD’s new DNA dragnet: The department is collecting and storing genetic information, with virtually no rules to curb their use by Allison Lewis (NY Daily News)

DNA sampling by police is broadening, and the wide nets being cast by police is generally falling in areas least able to defend themselves from attacks on civil liberties. [Link]

Domineque Ray Died So the Death Penalty Could Live by Matt Ford (The New Republic)

In a shocking move this week condemned from across the political spectrum, the Supreme Court denied an Alabama death row inmate the right to have his imam present during his execution, disregarding basic questions about the state’s motivations and constitutional protections against state sanctioned religion. [Link]

California

California Governor Proposes Digital Dividend Aimed at Big Tech by Kartikay Mehrotra (Bloomberg)

In a major recent policy rollout, California Governor Gavin Newsom announced a new tax on large tech companies based in Silicon Valley. [Link; soft paywall, auto-playing video]

America’s Signature Mode of Transportation Is High-Cost Rail by Jacob Bacharach (Hmm Daily)

Newsom was in the news this week, radically scaling back plans for high speed rail in California. That raises a variety of questions related to the utterly ridiculous cost of any large infrastructure project in the United States. [Link]

APNewsBreak: Teach for America slammed over Oakland strike by Sally Ho (AP)

Successful NGO Teach for America suggested that corps members who do not cross picket lines during an Oakland teachers strike would be punished financially. [Link]

International Matters

China’s Demographic Danger Grows as Births Fall Far Below Forecast by Liyan Qi and Fanfan Wang (WSJ)

Recent demographic data has shown that China is aging – and failing to reproduce – a t a drastically worse rate than had been previously estimated. [Link; paywall]

Taiwan insurers skirt restrictions to load up on dollar bonds by Edward White and Robin Wigglesworth (FT)

An explanation of the absolutely ludicrous Taiwanese insurance market, which depends on massive overseas bond holdings which are vulnerable to an appreciation of the Taiwan dollar. [Link; paywall]

The Case for a Significant German Stimulus Is Now Overwhelming by Brad W. Setser (Council on Foreign Relations)

With fiscal surpluses dating back to 2014, slowing growth, a surging household savings rate, and low debt levels, Germany is the poster-child for the sort of economy that ought to be engaging in fiscal stimulus. [Link]

Investing

For Boeing, juggling cash flow often means ‘another “Houdini moment”‘ by Dominic Gates (Chicago Tribune)

With contracts that give it enormous leeway to pull forward or push back cashflow, Boeing (BA) is able to play a delicate financial game and make its operations look healthier – or at the very least, more consistent – than they actually are. [Link]

How a Nasdaq Loophole Fueled One Stock’s Rise of 3,750% by Dave Michaels and Alexander Osipovich (WSJ)

A Nasdaq-listed firm with a massive stock of restricted shares is listed on the large market despite its dubious ability to meet listing requirements. [Link]

Malfeasance

Exclusive: FBI investigating top Vitol executives in Americas – sources by Brad Brooks and Gary McWilliams (Reuters)

One of the largest players in the physical oil trading market has executives under investigation in connection to the massive bribery scandal still unfolding in Brazil. [Link]

The former Apple lawyer who was supposed to keep employees from insider trading has been charged with insider trading by Sara Salinas (CNBC)

Three different times during 2015 and 2016, the Apple employee responsible for keeping Apple compliant with securities law traded ahead of earnings. [Link]

Wealth

Wealth concentration near ‘levels last seen during the Roaring Twenties,’ study finds by Christopher Ingraham (Seattle Times)

New research from UC Berkeley economist Gabriel Zucman suggests that the 400 richest Americans control more wealth than the bottom 60 percent of the distribution (150mm people), with that massive swathe of the population holding only 2.1% of total wealth. [Link]

Americans’ Confidence in Their Finances Keeps Growing by Jim Norman (Gallup)

The highest percentage of American population expects to be better off over the next year since 1998, with 69% of those Gallup surveyed optimistic. [Link]

Social Media

Writer Sues Twitter Over Ban for Criticizing Transgender People by Georgia Wells (WSJ)

In a novel legal strategy, a Canadian writer is suing Twitter on competition grounds after being banned under the Twitter hateful conduct policy. [Link; paywall]

Money Ball

Machado and Harper haven’t signed because baseball teams are now run like Wall Street ‘quant funds’ by Michael Santoli (CNBC)

A very slow free agent signing season has led analysts to compare the behavior of MLB teams to quants that underweight high-flying and glamorous stocks that garner all the headlines. [Link]

Migration

Americans continue their march to low-tax states by Jonathan Williams (The Hill)

Williams argues that tax rates and low budget deficits are driving the movement of Americans from large population states to booming Sunbelt locales. [Link]

EVs

Electric truck start-up Rivian announces $700 million investment round led by Amazon by Robert Ferris and Paul A. Eisenstein (CNBC)

A small company aiming to fill a high-performance niche in the EV markets with a pickup truck and SUV got a big funding boost from Amazon this week. [Link]

Trade

Measuring Trump’s 2018 Trade Protection: Five Takeaways by Chad P. Bown and Eva (Yiwen) Zhang (PIIE)

In addition to the sheer size and scale of tariffs introduced by the Trump Administration, some products are being hit multiple times. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Closer: End of Week Charts — 2/15/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. Below is a chart of the US Global Citi Economic Surprise Index which saw the largest one-day decline in the Citi Economic Surprise Index in over 13 years yesterday.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

The Bespoke Report — Market Doesn’t Fold

The big headline around financial circles this week was the fact that after facing resistance from a minority of politicians and public figures, Amazon decided to pull the plug on its planned expansion into New York City. Whatever your individual views towards the deal, the fact is that most people in the New York City area and Long Island City, where the project was to be based, were in favor of the expansion plan. In that regard, Amazon’s decision to pull out was viewed as a negative for the city and sets a bad precedent for the future when other firms weigh expansions in the region.

It’s always disheartening when a project runs into resistance and fails to clear the finish line, so thankfully for bulls, the market didn’t pull an Amazon and pack up and quit when it too faced resistance heading into the week. While Small and Mid Caps were finally able to take out one of the prior highs from before the December swoon (red arrows), the S&P 500 and Nasdaq haven’t quite been able to clear that hurdle. In the case of the S&P 500, though, the 200-DMA is now in the rearview mirror, so it’s a start.

We had lots to talk about in this week’s Bespoke report, so if you don’t have access yet, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

Trend Analyzer – 2/15/19 – Overbought to End the Week

Despite stocks finishing lower yesterday, all of the major US index ETFs have held onto their overbought levels and are looking to finish the week there. The greatest strength continues to come from small to mid-caps. Whereas recently mid-caps have done slightly better, this week’s price action has led small-caps to take the throne. The Micro-Cap ETF (IWC) has been the best of these ETFs headed into the end of the week rallying 2.86%. Other small-caps, the Core S&P Small Cap (IJR) and Russell 2000 (IWM) are not far behind these kinds of gains at 2.77% and 2.73% WoW, respectively. As we have repeatedly highlighted, large caps have continued to lag. In the last week, the Dow (DIA) and S&P 100 (OEF) have both ‘only’ gained 1.29% and 1.26%, respectively. Still, these are not losses so things are not that bad.

Granted, despite an impressive rally this year with each ETF hovering around a 10% or greater gain year-to-date, not a single member of this group has broken out of their downtrends (on a six-month time frame). While progress has been made in changing that, it will likely take a bit more time and work on the part of the bulls to see trends begin to change through our Trend Analyzer. These trends are evident in the charts. Shown below is a snapshot of the above ETFs in our Chart Scanner tool. Obviously, prices are trending down and to the right still, but price action has also more than broken out from the downtrend lines so these trends have very much had some positive developments. At the current overbought levels, there is likely to be some type of pullback that could restest these downtrend lines.

Morning Lineup – Optimism on Chinese Trade Talks

Let the record show that we are getting just as tired about typing subject lines related to Chinese trade talks as you are reading about them, but that’s the story once again this morning as trade officials from both China and the US have agreed to resume trade talks in DC next week. That has turned what was a modestly negative tone to a modestly positive one as we close out the week and head into the long holiday weekend. In economic data for the US, Import and Export Prices were both weaker than expected, but the Empire Manufacturing report slightly exceeded expectations. Read all about overnight events around the world and this morning’s news in today’s Morning Lineup.

Bespoke Morning Lineup – 2/15/19

Along with the strong gains so far in 2019, we have also seen very strong breadth. The chart below shows the 10-day A/D line for the S&P 500 over the last year, and while it has typically oscillated between gains and losses, it has been consistently positive now since early January. In fact, for 28 straight days now the 10-Day A/D line has been above +500, which is the longest streak in nearly three years (March 2016).

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.