Chart of the Day – NVDA Stalls, But Semis Keep Trucking

Past the Ides of March

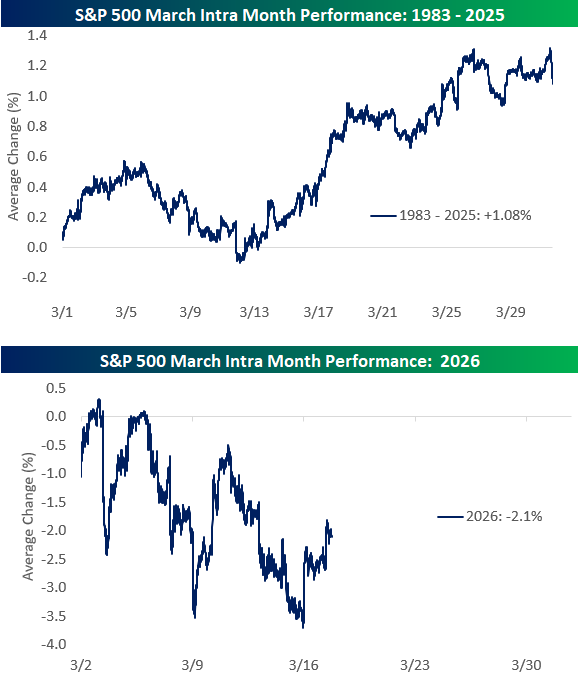

The S&P 500 fell more than 3% in the first half of March, but there’s reason to be more optimistic from a seasonal perspective. As we highlighted in this Chart of the Day for members at the start of the month, March gains have historically been back-end loaded.

The top chart below shows the S&P 500’s average path during the month of March since 1983. The second chart shows the S&P’s price action so far this March.

Historically, the market has traded relatively flat through the Ides of March and then picks up steam with gains in the back half of the month.

So far this week, we’ve seen the bulls get back to work with the S&P up more than 1% as of noon on Tuesday. We’ll see if the gains can hold and continue following the historical script with a strong finish to the month.

Sign up for Bespoke’s Think BIG mailing list to receive an interesting market stat like this in your inbox a few times per week. Click here or on the image below to sign up. An email is all we need!

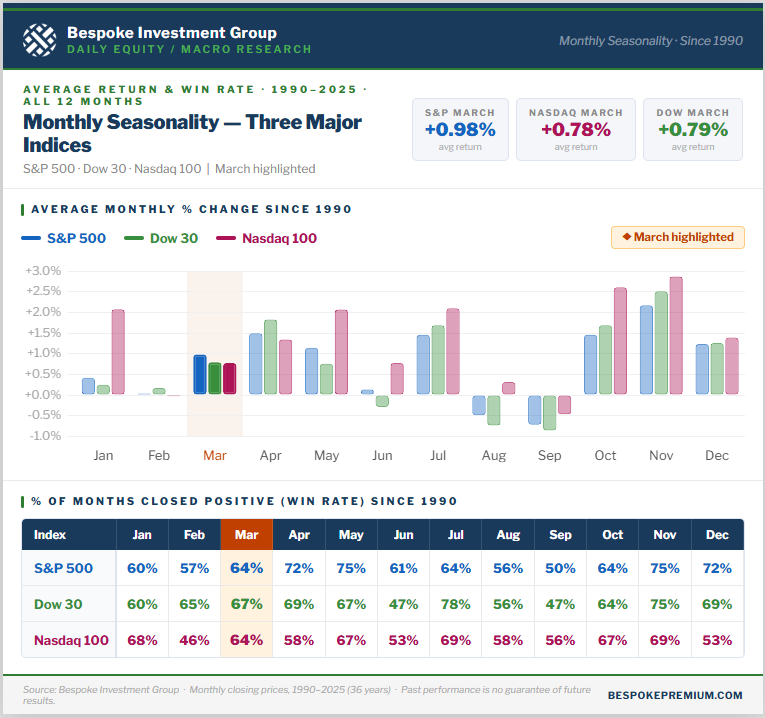

For more context on market seasonality, the graphic below was featured in our Chart of the Day for members back on March 2nd. It shows the average monthly percentage change for the S&P 500, Nasdaq 100, and Dow 30 since 1990.

While March has typically seen gains of just under 1% for all three indices, April has been an even better month over the years!

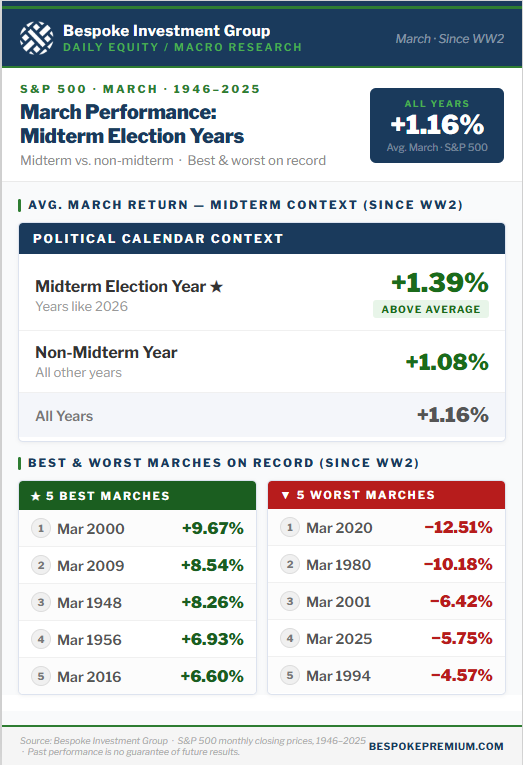

In addition to the graphic above, the one below shows how the market has performed in March during midterm election years like 2026 versus all other years. As shown, the market has historically done slightly better in March during midterm years with an average gain of 1.39% since WW2.

Like this analysis? Receive our Chart of the Day in your inbox each day by starting a Bespoke trial! Click below for details on how to sign up:

Bespoke’s Morning Lineup – 3/17/26 – Trying to Get in the Holiday Mood

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Competitive golf is played mainly on a five-and-a-half-inch course… the space between your ears.” – Bobby Jones

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

As hard as the bears have been working to push futures lower overnight and this morning, the luck of the Irish won’t quit and has pushed futures on the S&P 500 and the Dow into the green. The Nasdaq isn’t quite there, but it is well off its overnight lows. Treasuries are modestly higher, pushing yields slightly lower, while crude oil rebounds more than 2% to $95 per barrel. Gold prices are fractionally higher, and Bitcoin is basically flat.

It’s a quiet day for economic data today, with Pending Home Sales and Leading Indicators the only two reports on the calendar, and both will be released at 10 AM.

In international markets, Asian stocks were mixed overnight, while Europe is mostly higher, with the STOXX 600 up 0.5%. Those gains come despite ZEW Economic Sentiment Indices coming in significantly weaker than expected, as concerns over the war in Iran weigh on sentiment.

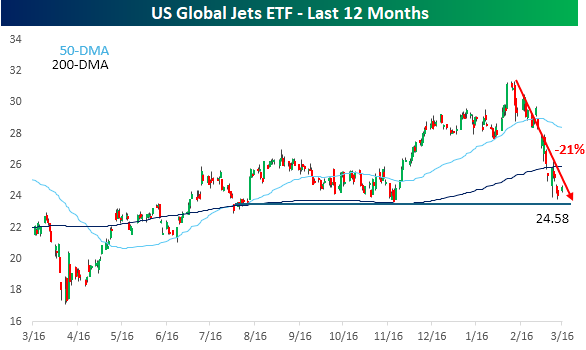

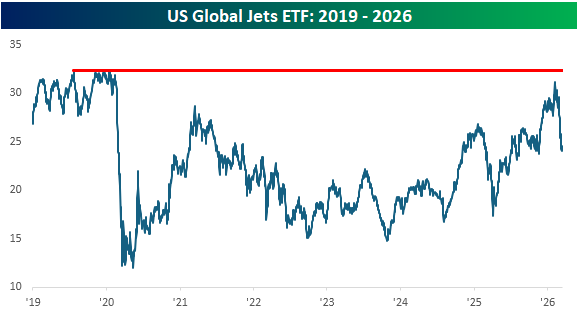

Can it get any worse for airline stocks? After already dealing with the government shutdown where TSA agents aren’t getting paid, the war with Iran has caused jet fuel prices to double and raised the threats of terrorism, which, at the margin, causes travel plans to decline. Since its peak in early February, the US Global Jets ETF (JETS) has plunged more than 20%, effectively erasing the gains from late last year after it broke out of a multi-month trading range. At $24.58, the ETF closed yesterday right near support at the low end of that prior range.

With all the headwinds facing the sector, it’s not looking like the Q1 earnings season is a period that airlines are looking forward to. Despite that backdrop, it was surprising to see comments from Delta CEO Ed Bastian this morning where he said that despite the negative impact of rising energy prices on company margins, the weakness has been completely offset by exceptionally strong demand. In his interview on CNBC, Bastian noted that “We’ve seen eight of the top 10 sales days in our history this quarter, and five of those just within the last two weeks, within just the last week of March”. With demand like that, we can only imagine what the company’s quarterly results would have looked like had there not been a war!

Looking at the airline stocks from a longer-term perspective, the timing of the Iran war couldn’t have been worse. At its recent peak in February, the JETS ETF traded above $31 and was within a dollar of its pre-Covid highs. It’s been a long slog for the sector, but after more than six years, it’s almost back to even.

The Closer – $2 Per Day, Positioning, Credit – 3/16/26

Log-in here if you’re a member with access to the Closer.

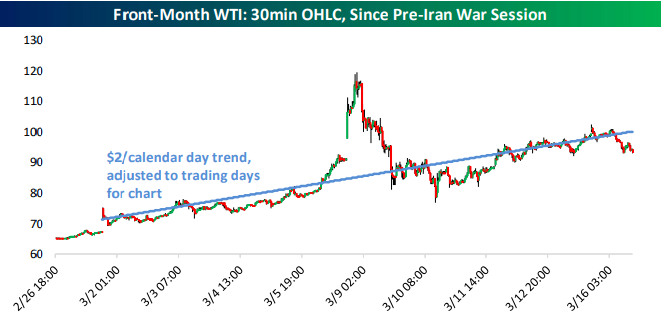

- Despite the dip today, front month WTI is rising at a $2/day pace.

- Positioning data is beginning to reflect adjustments in energy and agriculture commodity futures as a result of the closure of the Strait Hormuz.

- Consumer lending, private equity, and private credit stocks are down as IG credit spreads have soared.

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Daily Sector Snapshot — 3/16/26

Bitcoin Morning Strength

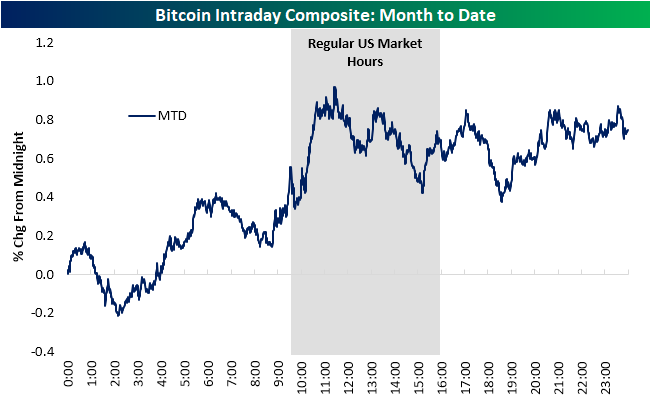

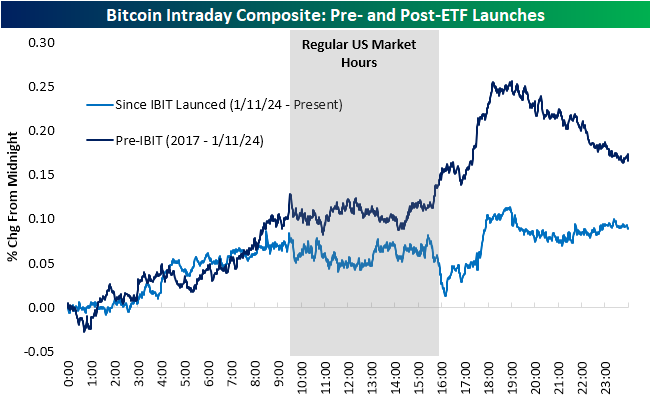

Alongside other risk assets rebounding to start the week, Bitcoin prices are approaching $74K, which is the highest price point since early February. Bitcoin and other cryptocurrencies differ from traditional assets in that they trade around the clock. In the charts below, we show an intraday composite for Bitcoin over the full course of a day over various time frames. These charts show Bitcoin’s average price movement throughout the 24-hour trading day over the time frames shown.

As shown below, Bitcoin has averaged around a 0.75% daily gain so far in March, with the bulk of that strength occurring in morning trading. In fact, Bitcoin has averaged around a 0.5% gain on the day heading into the US equity market open (9:30 AM ET) thanks to an early morning rally, and it has continued to rally towards a 1% gain by late morning. After peaking just before noon, Bitcoin has traded sideways all afternoon and night.

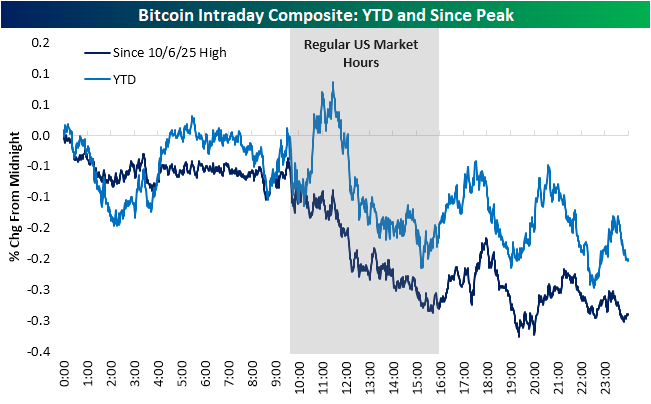

Bitcoin’s recent strength throughout the day is the opposite of what has been observed since the high in Bitcoin last fall. Generally speaking, throughout Bitcoin’s current drawdown, it has traded flat in the early morning hours and then lower throughout the US equity market trading day.

As shown below, Bitcoin has become less volatile as it has matured and especially since the latest waypoint of institutional adoption when spot ETFs garnered approval in early 2024. From 2017 up until early 2024 when the first spot Bitcoin ETFs were approved, Bitcoin generally traded higher throughout the trading day save for during regular US trading hours when price action was more flat in addition to declines late at night. Since spot ETFs like the iShares Bitcoin ETF (IBIT) were approved, though, price action has changed. Again, morning trading has been solid and even neck in neck with the intraday composite from before ETF approval. Likewise, during regular trading hours, Bitcoin price action has been largely uneventful, that is until the end of the day. Whereas previously the close of regular market hours saw Bitcoin ramping higher, since ETFs were approved, the end of the equity trading session has seen steep declines.

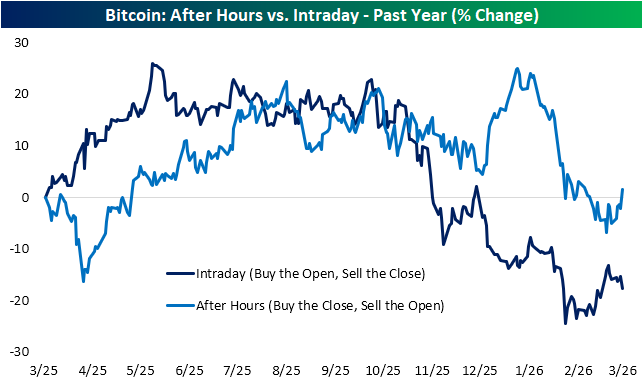

As we have done with the S&P 500 (SPY) in the past, below we show the performance of two hypothetical strategies of ownership. The first would be to buy bitcoin and only hold during regular US equity market hours (buy the open, sell the close) while the other would be the reverse of only owning outside of regular trading hours (buy the close, sell the open). As we discussed above, throughout various periods, Bitcoin performance was stable at best when stocks, bonds, and commodities are trading hands. Given this, only owning Bitcoin during regular market hours over the past year would have been the losing strategy, resulting in a 17% loss. The opposite strategy hasn’t exactly been a huge winner, but it at the moment it would still have resulted in modest gains. We would note that in the past two weeks, the two lines have begun to move in opposite directions. That dynamic was also prevalent from mid-December through the first week of the new year too.

Like this analysis? Join our premium members by starting a trial today! Click below for details on how to sign up:

Chart of the Day: Mag 7 Entry Points

Bespoke’s Morning Lineup – 3/16/26 – Crude Gives Equities a Break

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Philosophy is common sense with big words.” – James Madison

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

It’s been a tough few weeks for equities. After months of trading in a sideways range, the war in Iran has put an added weight on the bearish side of the scale, pushing stocks lower. All of the major US indices are below their 50-DMAs, and the 200-DMAs are now starting to come into play as well. The short-term key has been and will continue to be oil prices. With no spike this morning, equities are taking the opportunity to rally, and we’ve been picking up steam as the morning drags on. The S&P 500 is on pace to gap up 0.75% as the open, while the Nasdaq is up closer to 1%. Now, let’s see if the gains can hold!

Outside of equities, treasury yields are falling with the 10-year yield down 5 bps to 4.24%, and crude oil falls almost 2% to just under $97 per barrel. Gold prices are down just over 1% and barely hanging on to $5,000, while bitcoin is up nearly 3% and above $73K.

Asian stocks were flat to higher to start the week on the optimism that oil prices didn’t spike more after the weekend. Japanese stocks traded down 0.1% while China was down 0.8%. Hong Kong, India, and South Korea, however, all rallied more than 1%. The declines in China came despite better-than-expected February data for Industrial Production, Retail Sales, and Fixed Investment.

European stocks have taken a more muted start to the week. The STOXX 600 is down 0.1% while Germany is up 0.3% and Italy drops 0.3%. It will be a busy week for central banks on the continent as the ECB, BoE, and SNB all have meetings.

It’s a relatively busy day for economic data this morning, with the Empire Manufacturing report for March hitting the tape at 8:30, followed by Industrial Production and Capacity Utilization at 9:15. Homebuilder sentiment will come out at 10 AM. Another area of focus today will be on Nvidia (NVDA) as CEO Jensen Huang will give the keynote speech at his company’s GTC conference at 2 PM Eastern. Looking ahead, the Fed will announce its latest policy decision on Wednesday.

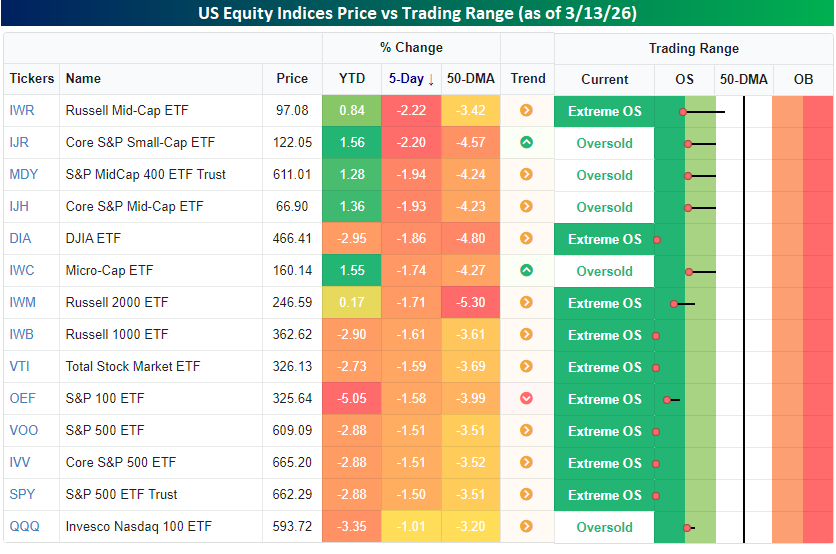

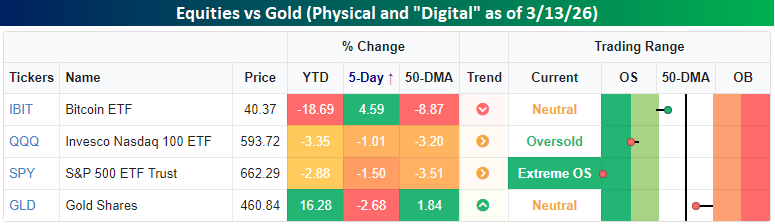

The S&P 500 has declined for four straight weeks now, but still hasn’t even declined 5% from its closing high in late January, so while it’s been a slump, it could be worse. Even with the relatively modest declines, as we discussed in Friday’s Bespoke Report, it still finds itself in what we consider ‘extreme’ oversold levels as it closed more than two standard deviations below its 50-DMA. Along with the S&P 500, the majority of other US index ETFs also finished off last week in extreme oversold territory, and the ones that aren’t are still in oversold territory.

Last week, there was a little bit of rotation in the market where the indices that had been performing the best YTD (small and mid-caps) experienced the largest declines, while large caps, which had been the weakest, were down less. It’s all relative, though, as even the best-performing US indices last week were still down over 1%.

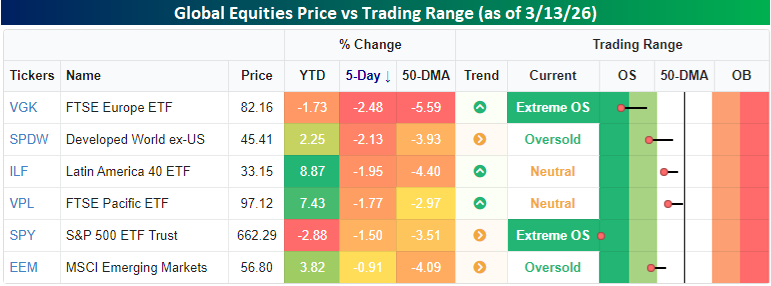

Similar to the relative outperformance of large caps versus small caps last week, US stocks outperformed their global peers once again last week, further digging out of their relative hole on a YTD basis. While the S&P 500 was down 1.5%, European stocks traded down by 2.5% last week, putting them into ‘extreme’ oversold territory with the US. The only areas of the world not oversold heading into the new week are Latin America (ILF) and Asia Pacific (VPL).

With equities under pressure, investors must be taking shelter in the safety of gold, right? Not really. Physical gold hit a speed bump last week, falling more than 2.5%. Despite the decline, though, it’s still up over 16% YTD and above its 50-DMA, so don’t shed too many tears for the gold bugs. One area of surprising strength last week was in Bitcoin (IBIT). While it’s still down close to 20% this year, it managed to rally more than 4.5% last week. As they say, even a broken clock is right twice a day.

Brunch Reads – 3/15/26

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Beware the Ides of March: On March 15, 44 BC, known in the Roman calendar as the Ides of March, Roman dictator Julius Caesar was assassinated by a group of senators inside the Theatre of Pompey in Rome. Caesar had risen to unmatched power after years of civil war and had recently been named dictator for life, alarming members of the Roman elite who feared the Republic was giving way to monarchy. Led by conspirators including Marcus Junius Brutus and Gaius Cassius Longinus, roughly 60 senators surrounded Caesar during a Senate meeting and stabbed him more than twenty times in one of history’s most famous political assassinations.

The conspirators believed Caesar’s death would restore the Roman Republic, but the opposite happened. His assassination plunged Rome into another round of civil wars that ultimately ended the Republic altogether. Within a few years, Caesar’s adopted heir, Augustus, consolidated power and established the Roman Empire. The betrayal on the Ides of March later became legendary through William Shakespeare’s play Julius Caesar.

Markets & Investing

Inside one of the wildest days the oil market has ever seen (Financial Times)

Oil traders faced one of the most chaotic sessions in the market’s history as Brent crude swung from about $119 to $84 in a single day amid escalating Middle East tensions and changing political signals. The extreme volatility forced market makers to widen spreads dramatically and left some traders scrambling to hedge or exit positions, with reports of massive losses and even entire trading teams being fired after getting caught on the wrong side of the moves. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

Bespoke’s Consumer Pulse Report – March 2026

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.