Gauging the Bounce

The average S&P 500 stock fell 6.2% from 4/30 (when the index made its last all-time closing high) through last Monday (June 3rd). Since the close last Monday, the average stock in the index has bounced back 4.1%.

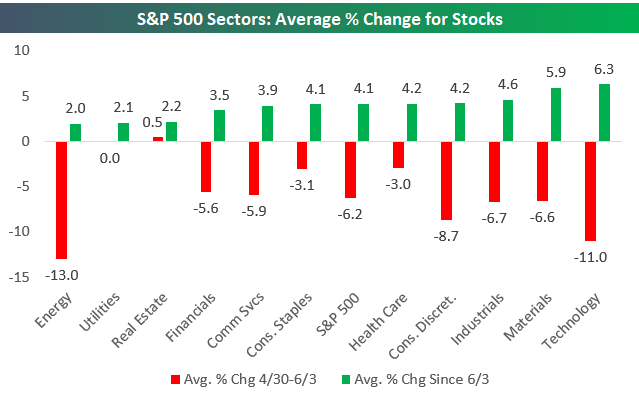

Below is a look at how stocks within sectors have performed recently. During the pullback from 4/30 to 6/3, Energy stocks fell the most of any sector at -13%. Energy stocks have also bounced back the least since 6/3 with an average gain of just 2%. Technology stocks fell the second most during the pullback with an average decline of 11%, but Tech has bounced back the most since 6/3 with an average gain of 6.3%.

Notably, some sectors have seen average gains since 6/3 that are bigger on an absolute basis than the declines they saw during the pullback. The average Utilities stock was flat from 4/30-6/3, but since then the average stock in the sector has rallied 2.1%. The average Real Estate stock actually gained from 4/30-6/3, and since then the sector has seen an average gain of 2.2%.

Consumer Staples and Health Care both saw average declines of roughly 3% during the 4/30-6/3 pullback, and they have bounced back by an average of just over 4% since 6/3.

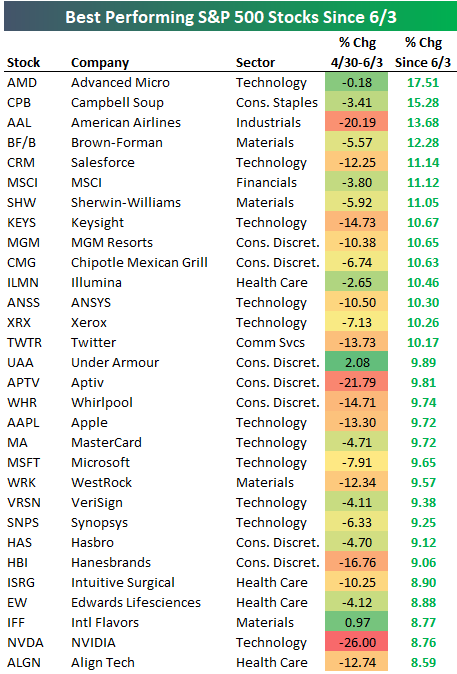

Below is a look at the best performing stocks since the S&P’s recent closing low on 6/3. Advanced Micro (AMD) is up the most of any stock in the S&P with a gain of 17.51%. Campbell Soup (CPB) — a company that couldn’t be much more different than AMD — is up the second most since 6/3 with a gain of 15.28%. American Airlines (AAL), Brown-Forman (BF/B), and Salesforce (CRM) round out the top five with gains of more than 11% each. Other notables on the list of winners include Chipotle (CMG), Twitter (TWTR), Under Armour (UAA), Apple (AAPL), MasterCard (MA), Microsoft (MSFT), and NVIDIA (NVDA). Start a two-week free trial to Bespoke Premium to unlock our premium research and investor tools!

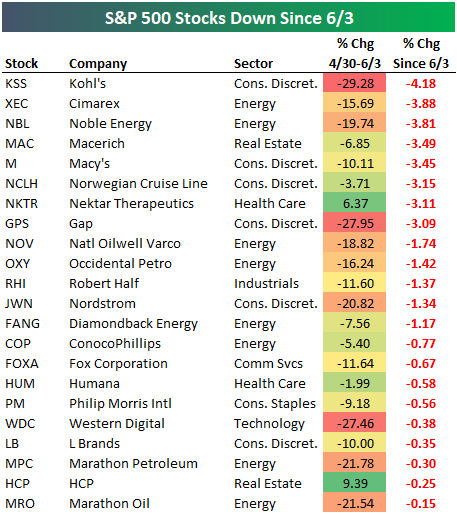

Below is a list of the 22 stocks in the S&P 500 that have the distinction of being down since last Monday. Kohl’s (KSS) is down the most with a decline of 4.18%, followed by Cimarex (XEC), Noble Energy (NBL), and Macerich (MAC). Other notables include retailers like Macy’s (M), Gap (GPS), Nordstrom (JWN), and L Brands (LB).

Morning Lineup – Merger Monday Provides a Positive Encore

After the first ‘perfect’ week for the DJIA since May 2018, a slew of mergers and the deal with Mexico are helping to kick off the week on a positive note providing a nice encore to last week’s gains. In terms of economic data, the week is starting off slow but will progressively pick up as the week goes on.

Please read today’s Morning Lineup for our latest take on events from the weekend, overnight, and this morning.

Sectors have seen quite a move within their trading ranges over the last week. As shown in the chart below, at this time a week ago the S&P 500 and every sector were trading below their 50-day moving averages and most were oversold. Fast forward five days and there are now just three sectors below their 50-DMA, and Energy is the only sector that is oversold. Meanwhile, both Consumer Staples and Utilities have moved back into ‘extreme’ overbought territory.

As far as the major averages are concerned, while the S&P 500 is trading back above its 50 and 200-DMAs, the Nasdaq 100 is still below its 50-DMA, and the Russell 2000 isn’t above either of those thresholds. If the rally is going to keep on going, they have a lot of catching up to do.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

Bespoke Brunch Reads: 6/9/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Trade Wars

Trump’s Tariffs Could Nullify Tax Cut, Clouding Economic Picture by Jim Tankersley (NYT)

While tax cuts passed at the end of 2017 had a positive effect on household incomes, new tariffs rolled out over the last two years are raising costs and clawing back all the benefits of the tax cut for some households. In other words, this is the substitution of one kind of tax for another. [Link; soft paywall]

Chinese goods navigate alternate trade routes to US shores by Kyo Kitazume, Tomoya Onishi, and Yusho Cho (Nikkei Asian Review)

Companies are relocating production from China to other economies not impacted by tariffs, but trade flows are also being routed from producers in China through third-party economies that aren’t facing the same tariffs. [Link]

Fraud

The Couple Who Feds Say Scammed Berkshire Hathaway for Millions by Brian Eckhouse, Katherine Chiglinsky, and Mark Chediak (Bloomberg)

Solar financing company that got investment from Berkshire among many others was a Ponzi scheme, using a tax credit system to lure investors into plunking hundreds of millions into funds tied to the fraud. [Link; soft paywall]

Florida

Who is Florida Man? by Bob Norman (Columbia Journalism Review)

How wildly viral headlines tied to the odd crimes of Floridians cast light on the darker corners of the media landscape and the grim monetization of human pain. [Link]

Florida County School Board Approves Medical Marijuana Access in Public Schools by A. J. Herrington (High Times)

Students who have prescribed cannabis medications administered by a student’s parent or caregiver (and excluding smoking or inhalation-based treatments) will be permitted to use the treatments in Palm Beach County schools. [Link]

Homeowners

14 Millennials Got Honest About How They Afforded Homeownership by Anne Helen Petersen (Buzzfeed News)

Anecdotes from a range of 20 or 30-somethings that have bought homes. Notably, only one of the fourteen with a down payment over $10k was able to buy a home without parental contribution to down payments. [Link]

HOAs Are Popular Where Prejudice Is Strong and Government Is Weak by David Montgomery (City Lab)

More than half of single family homes are part of an HOA, but that number is greater than 80% when it comes to new homes. HOA homes tend to command higher price premiums in the South and West and tend to command higher price premiums in areas with less local land use regulation. [Link]

Data

Microsoft, Nasdaq, and Refinitiv empower everyday investors with real-time data and insights in Excel by Rob Howard (Microsoft)

In a new feature for Microsoft Excel, users will be able to stream real-time stock prices for free in updated versions of the ubiquitous spreadsheet software. [Link]

Boeing

Boeing Built Deadly Assumptions Into 737 Max, Blind to a Late Design Change by Jack Nicas, Natalie Kitroeff, David Gelles, and James Glanz (NYT)

More details on how the 737-MAX ended up with a huge design flaw that resulted in multiple fatal crashes. [Link; soft paywall]

Science

Laser flight path caught on camera for the first time by Jacob Aron (New Scientist)

This isn’t new news, but it’s still pretty cool: extremely high framerates allowed scientists to capture the path of laser beams through the air. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — Negative Void Coefficient

This week’s Bespoke Report newsletter is now available for members. Equity markets surged despite short term interest rate markets pricing near-certainty of multiple Fed rate cuts this year. How can an economy so bad that the Fed needs to cut mean stocks go up? We take a look around for some answers. We also review just how dovish the Fed has been relative to what markets have been pricing of late. While the domestic economy has definitely slowed down from the torrid pace of 2018, even the disappointing nonfarm payrolls number today paints a different picture than assumptions of multiple cuts from the front end. The global economy is less constructive, but there’s a difference between weakness and a recession panic, as we show. Finally, we present an argument for why Fed rate cuts may not be necessary for the economy to stabilize and start to pick up again thanks to negative feedback loops.

We cover everything you need to know as an investor in this week’s Bespoke Report newsletter. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!

The Closer: End of Week Charts — 6/7/19

Looking for deeper insight on global markets and economics? In tonight’s Closer sent to Bespoke clients, we recap weekly price action in major asset classes, update economic surprise index data for major economies, chart the weekly Commitment of Traders report from the CFTC, and provide our normal nightly update on ETF performance, volume and price movers, and the Bespoke Market Timing Model. We also take a look at the trend in various developed market FX markets.

The Closer is one of our most popular reports, and you can sign up for a free trial below to see it!

See tonight’s Closer by starting a two-week free trial to Bespoke Institutional now!

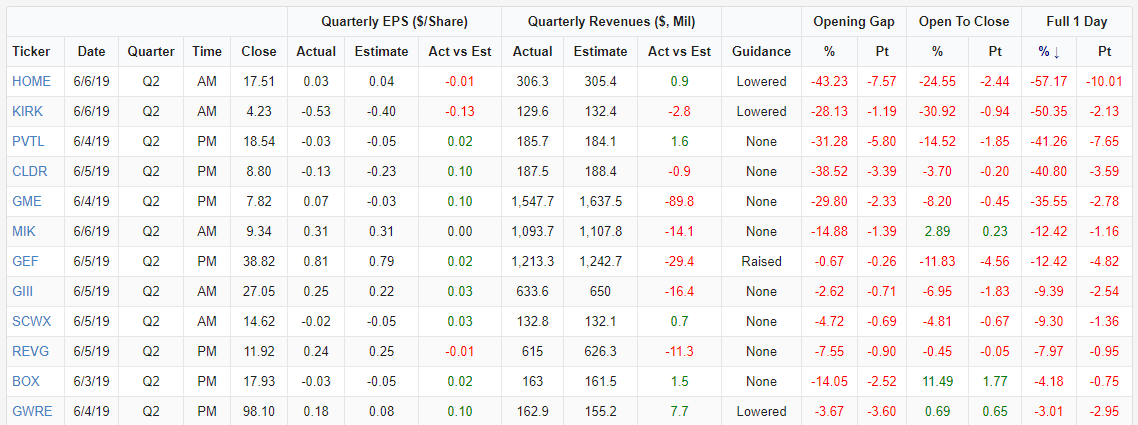

Earnings Disasters

While the broad stock market had a banner week, companies that reported earnings this week generally did not. A total of 42 companies reported earnings this week, and the price reactions certainly left something to be desired. The average stock that reported this week opened down 2.44%, then traded down another 1.75% from the open to the close. The average full-day change for the 42 stocks that reported this week was a decline of 3.63%.

Below is a snapshot of the stocks that had the most negative price reactions to earnings this week:

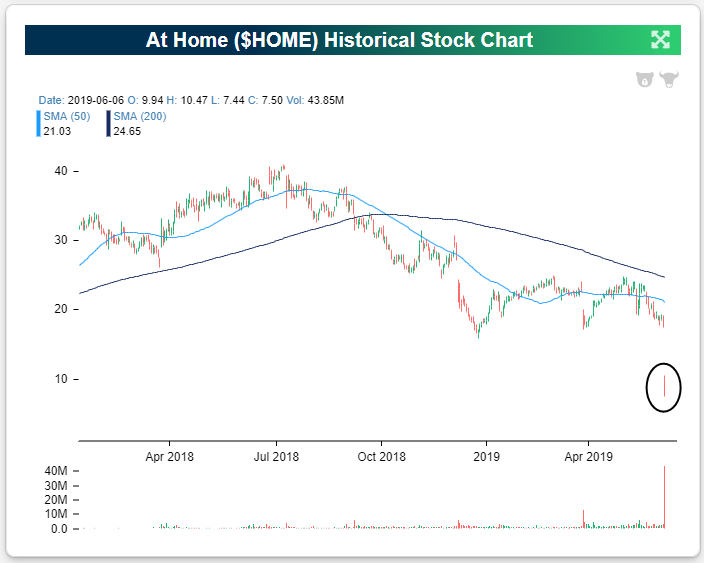

Home furnishing retailer At Home (HOME) tops the list of losers after the stock lost more than half of its value after its most recent earnings report Thursday morning. On top of lowering guidance, the company was expected to see EPS fall to $0.04, a massive decline versus the previous quarter’s $0.47 and last year’s Q2 $0.34, but the company reported an even worse EPS of $0.03. This profitability drop overshadowed YoY revenue growth of just over 6%. The stock’s complete collapse yesterday accelerated what was already a long-term downtrend, bringing the stock to an all-time low.

Another specialty home decor retailer, Kirkland’s (KIRK), reported its second abysmal quarter in a row with lowered guidance, lower and negative EPS, and a miss in revenues. Last quarter saw a similarly poor report and the stock slid 23.38% in response. The punishment kept coming this time around as the stock was cut in half, falling from $4.23 at Wednesday’s close to $2.10 by the end of the day Thursday; the stock’s lowest level in over a decade.

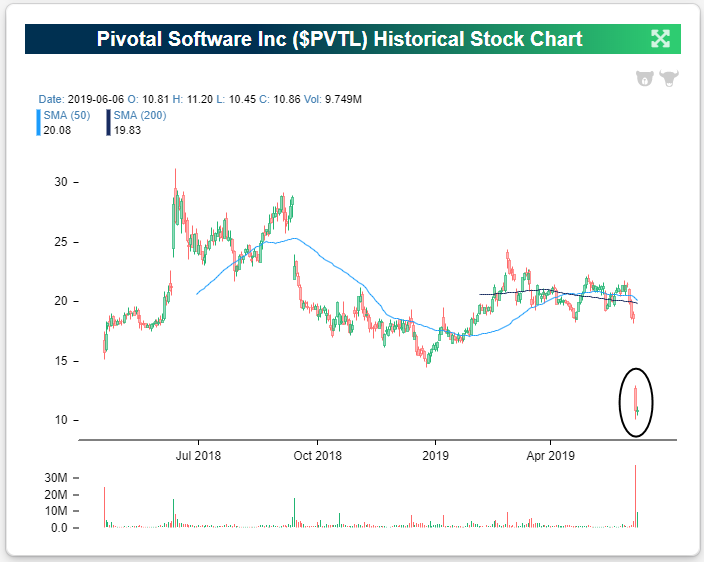

At first glance, cloud services provider Pivotal Software’s (PVTL) most recent quarter may not have looked too bad, especially given its solid earnings history headed into the report. Even after Tuesday’s report, the company has never missed an EPS estimate in its history, and it has only missed revenue estimates once (the prior quarter). Despite maintaining this pretty strong track record, PVTL fell 41.26% in response in Wednesday’s trading. These declines were a result of weakness under the hood of this report. PVTL claimed several deals had fallen through and competition had become more of a headwind. In turn, the stock received multiple analyst downgrades. This perfect storm leaves the stock near all-time lows and 36.12% below its price when the stock first hit the market just over one year ago. Start a two-week free trial to Bespoke Premium to use our Earnings Calendar and other tools!

Beginner’s Luck?

Since its IPO on May 2nd, plant-based meat alternative brand, Beyond Meat (BYND), has been one of the hottest stocks in the market. Last night, the company had its first earnings report as a public company. The results seemed to justify the run-up in price since the IPO as it saw an earnings triple play (beat EPS, beat revenues, raised guidance). EPS came in negative but 1 cent above analyst estimates. Revenues were $40.2 million versus estimates of $38.93 million. The major highlight of these revenue numbers was a year-over-year growth rate of an astounding 214.1%. The company also raised guidance. This has rocketed the stock higher as it now sits up 25.92% today, and that is off of the day’s highs and below the opening price!

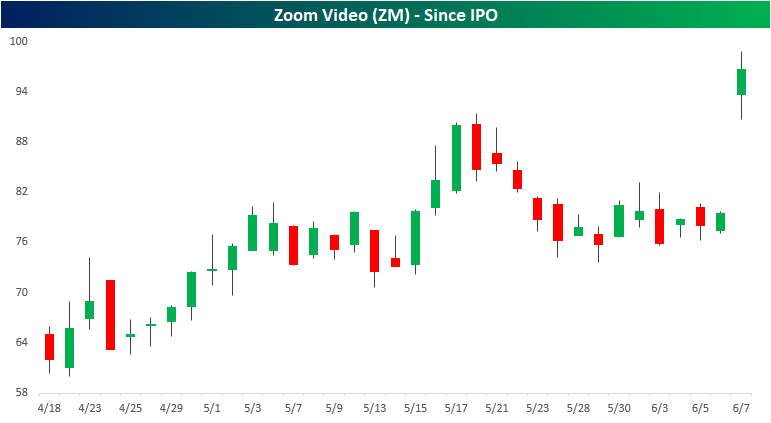

Another recent IPO, Zoom Video (ZM), is also up over 20% on an earnings triple play reported last night. This provider of video communication services reported EPS of $0.03 compared to estimates of $0.01. Revenues also came at $122 million, well above estimates. Similar to BYND, revenues also saw substantial year-over-year growth of 103.1%.

Perspecta (PRSP) was the third triple play reported last night after the close. While not as green as ZM or BYND, Perspecta is still fairly new as it first hit the market just over a year ago. PRSP beat EPS by 7 cents and revenues by $16 million. Not as high of a growth rate as the others, PRSP still boasts high YoY growth of 53%. Relative to the other triple plays today, PRSP hasn’t been nearly as volatile but it has made a solid push higher. The stock gapped up 2.18% at the open, rising further from the open now sitting 5.85% above last night’s close. It now sits just 2.28% below its highs from the first week of May. Start a two-week free trial to Bespoke Premium to track all earnings triple plays on a daily basis!

F For Forecasting

One would think that with all the technological improvement in the last few years and the ability to gather more data related to the employment landscape of the US economy, that forecasting of the monthly Non-Farm Payrolls report would be improving. For several years that was the case, but lately not so much. Take the last six months, for example. In the six Non-Farm Payrolls reports that have been released so far in 2019, the actual reported readings versus expectations have been +128K, +139K, -160K, +19k, +73k, and -100K, respectively. There was a time when it was pretty uncommon for Non-Farm Payrolls to be more than 100K above or below the consensus reading. Recently, though, that has been the norm, and over the last six months, the actual reported reading has been above or below consensus expectations by an average of 103K!

Using our Economic Indicators tool, we created the chart below which shows the six-month average spread between the actual and reported reading in Non-Farm Payrolls going back to the late 1990s. From 1999 through the early 2000s, there were multiple periods where the average spread topped 100K. Beginning in early 2005, though, the spread dropped below 100K and remained that way for a number of years, averaging just 50K from the start of 2005 through the end of last year. Economists were really on a roll in their forecasting! This year, though, the pattern has shifted in a big way, and through this morning’s report, the six-month average now stands at 103K – the highest reading since December 2004. We realize that there have been a number of macro-headwinds (government shutdown in late 2018 and tariffs this year) that have made the forecasting process more difficult, but it has been a bad few months for forecasting. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Morning Lineup – Will Jobs Keep the Rally Going?

The last day of the week is looking like it will be off to a positive start, but who is anybody kidding thinking that these moves will mean anything when we have one of the most anticipated jobs reports in months on the horizon?

Please click the link below to read today’s Bespoke Morning Lineup for our take on this morning’s encouraging pattern in European Industrial Goods sector as well as a closer look at what’s driving the weakness in German exports.

Ahead of this morning’s jobs report, we just wanted to take a quick look at market breadth to see where the S&P 500’s cumulative A/D line stands. By this measure at least, we still don’t see a whole lot of weakness underneath the service as the cumulative A/D line held up pretty well throughout the recent bout of selling and currently isn’t far off its highs from earlier in the year.

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer – New Small Cap Lows, Real Yield Impact, Factory USD, Flow of Funds – 6/6/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look the underperformance of small caps as the relative performance of the Russell 2000 versus the S&P 500 has hit a 52-week low. We also look into the decline in real yields and how this can impact markets and industrial production in the future. Next, we dig into today’s Federal Reserve’s Z.1 report to get a read on debt levels in the US economy.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!