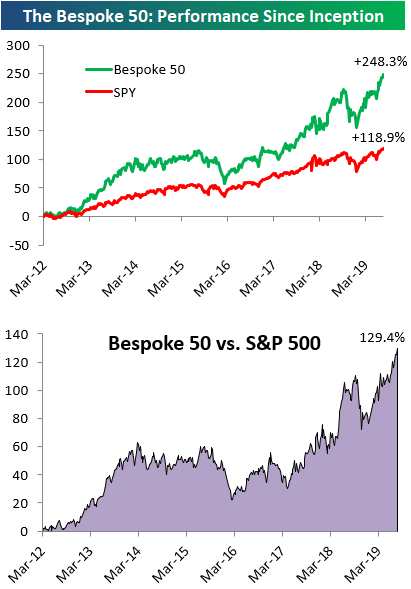

The Bespoke 50 Top Growth Stocks

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 129.4 percentage points. Through today, the “Bespoke 50” is up 248.3% since inception versus the S&P 500’s gain of 118.9%. Always remember, though, that past performance is no guarantee of future returns. To view our “Bespoke 50” list of top growth stocks, please start a two-week free trial to either Bespoke Premium or Bespoke Institutional.

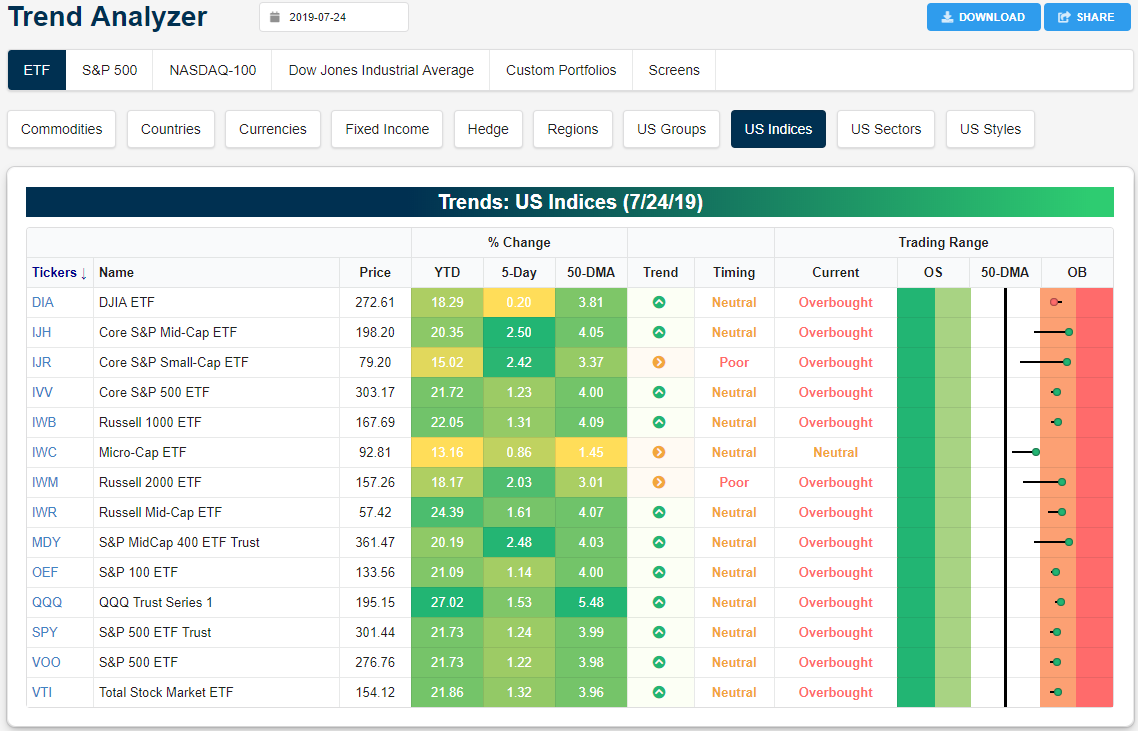

Trend Analyzer – 7/25/19 – Big Moves In Small Caps

Small and mid-caps’ recent lag has been turned on its head following strong gains in yesterday’s session. Whereas most of these have been at neutral over the past week, today only the Micro-Cap ETF (IWC) has not moved into overbought territory, although it has gotten close to doing so. Small and mid-caps have seen the largest gains over the past five days and have also seen significant moves within their trading ranges as shown through the long tails in the Trading Range section of our Trend Analyzer snapshot below.

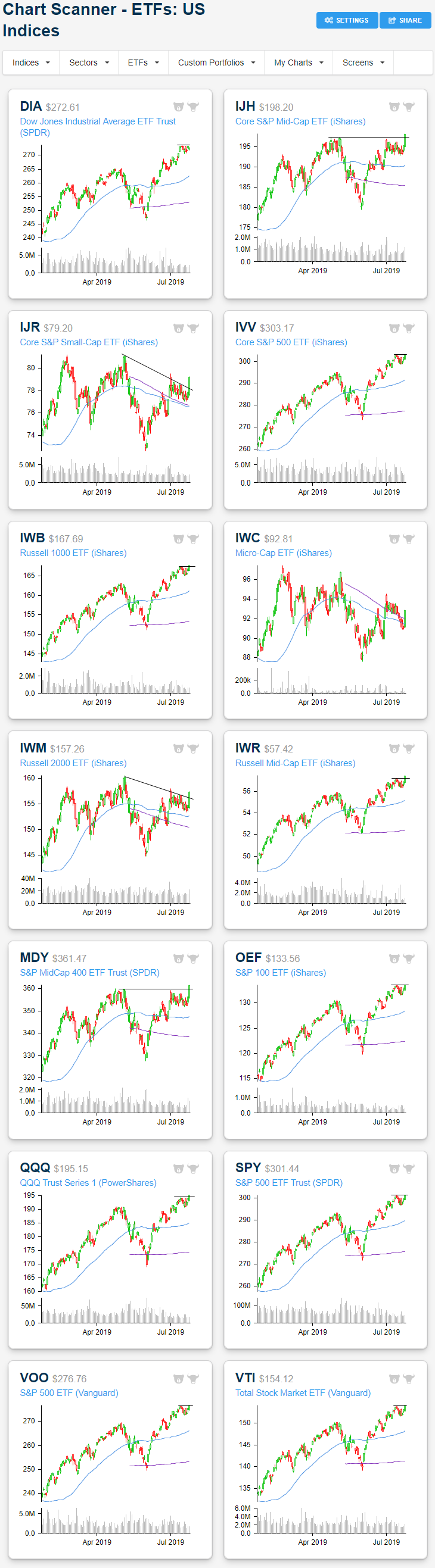

Looking at the charts, yesterday’s strong session for small and mid-caps is evident. Mid-cap ETFs like the Core S&P Mid-Cap ETF (IJH) have broken out above resistance to reach new highs. Meanwhile, small-caps like the Russell 2000 (IWM) and the Core S&P Small-Cap ETF (IJR) have broken out of their short term and a longer-term downtrends. IWC on the other hand still needs to push a bit higher to do the same. Large caps did not see as explosive of a move but the S&P 500 (SPY) and Nasdaq (QQQ) also managed to clear resistance to finish yesterday at new highs.

In the past week, it has mostly been more cyclical sectors that have led the way higher with Materials (XLB), Financials (XLF), Industrials (XLI), and Tech (XLK) all gaining well over 2%. On these moves, these ETFs have reached overbought levels. At the same time, defensives like Consumer Staples (XLP), Real Estate (XLRE), and Utilities (XLU) have fallen the most as they mean revert off of overbought levels. Start a two-week free trial to Bespoke Institutional to access our interactive Trend Analyzer, Chart Scanner, and much more.

Russell 2000 Gets in on the Act

As the S&P 500 and Nasdaq have both been rallying and testing their record highs, small-caps had been lagging behind. In yesterday’s trading, though, even the Russell 2000 got in on the act and rallied. As shown in the intraday chart for the index over the last three weeks, yesterday’s 1.6% rally broke what had been a pretty consistent short-term funk for the sector.

A fifteen-day high for the Russell 2000 is a start, but it still has a ways to go before getting anywhere close to catching up to the large-cap S&P 500 or Nasdaq. Not only is the index still well off its highs from earlier this year, but it’s also still more than 9% from its all-time high made back in August 2018. Start a two-week free trial to Bespoke Institutional for access to our full research suite.

Bespoke’s Morning Lineup – Peak Earnings

As noted in our earnings preview earlier this month, with 61 S&P 500 companies scheduled to report earnings, today marks the peak day for earnings among large-cap companies. With the S&P 500 up over 2.5% heading into today, so far investors apparently like what they hear.

Mario Draghi’s last ECB meeting is a dovish one, with European assets ripping in response to a new look at QE as well as the possibility of tiered deposits at the central bank. US equity index futures were pointing to a decline but now suggest a gain at the open as European credit markets rally. Earnings data last night was mixed but has been generally strong this morning. Yields are down, the dollar is up, and markets are at or near session highs.

Read today’s Morning Lineup to get caught up on news and stock-specific events ahead of the trading day.

Bespoke Morning Lineup – 7/25/19

Start a two-week free trial to Bespoke Premium to see today’s full Morning Lineup report. You’ll receive it in your inbox each morning an hour before the open to get your trading day started.

The Closer – Semis, Machinery, Banks Breaking Out, New Home Sales, EIA – 7/24/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick things off with a look at semiconductors as SMH has broken out to a new all-time high. We also look at the movements in the 3m10y yield curve while cyclical machinery and bank stocks begin to breakout. Turning to economic data, we review today’s New Home Sales release. We also show what staffing provider Robert Half’s (RHI) earnings report indicated on the labor market. We finish tonight with our weekly look at ICI fund flows—showing another week of equity outflows—and EIA data showing a massive drop in production.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Big Day for Triple Plays

Since last night’s close, there have been five triple plays. A triple play is when a company reports quarterly earnings with EPS and sales above analyst estimates and raised guidance. Typically this is a healthy sign for a company’s fundamentals with price reacting accordingly. You can use our Earnings Explorer and 100 Most Recent Triple Plays tools to keep track of recent strong earners.

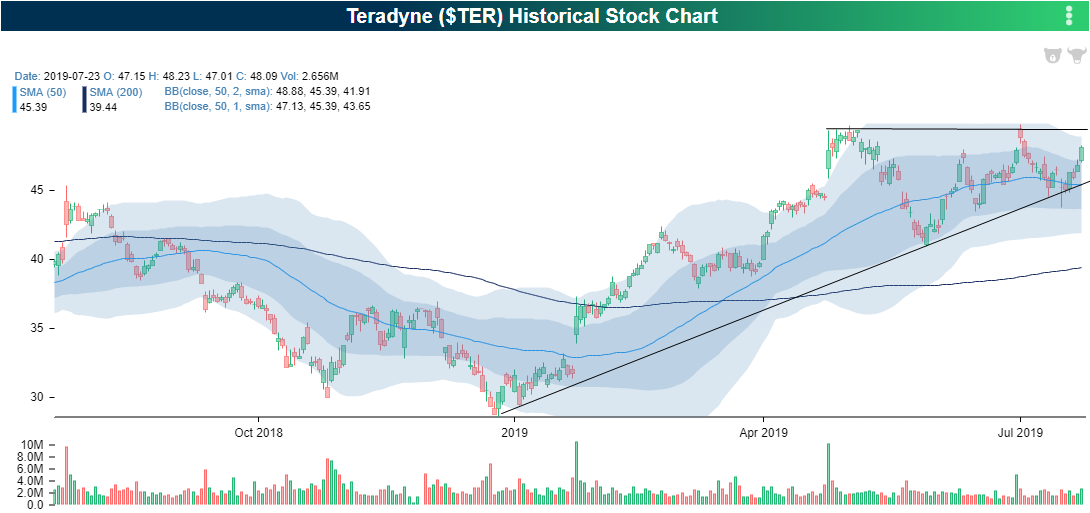

Of the five that reported in the past day, Teradyne (TER) has seen the best response, up over 20% on the day as of this writing. TER has been forming an ascending triangle with this recent move leading to a breakout. TER has also been a strong company on earnings with both EPS and sales beats for every quarter since 2013. Last night’s 4 cent EPS beat and $27.3 mm revenue beat marked the ninth triple play in that time. On average, each of these triple plays was responded to with a 2.8% gain, but today’s performance has left this average in the dust. Additionally, the company commented that the growth of 5G was a key factor in the strong quarter, similar to the first triple plays of this earnings season.

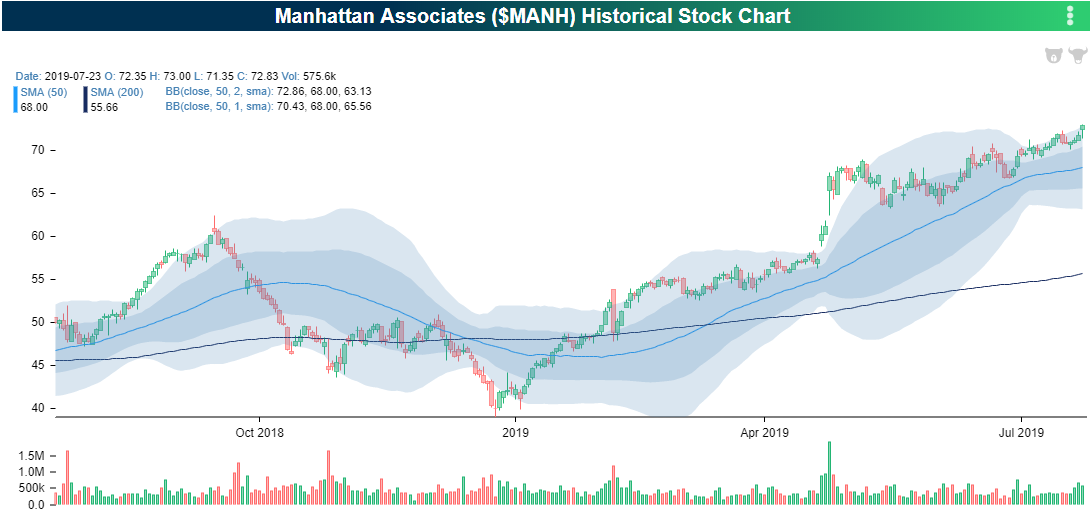

Also out last night, reporting its second straight triple play was Manhattan Associates (MANH). MANH has consistently reported strong quarters with the last EPS miss being back in 2009. Additionally, it is no stranger to triple plays with ten prior occurrences. EPS for the most recent quarter came in at $0.42 versus estimates of $0.35 while revenues were at $154.3 million, $8.3 million above estimates. Ahead of this report, the software and services company reached a 52-week high; also bringing it to extremely overbought levels. In reaction today, the stock has continued to move deeper into overbought territory with a 19% gain.

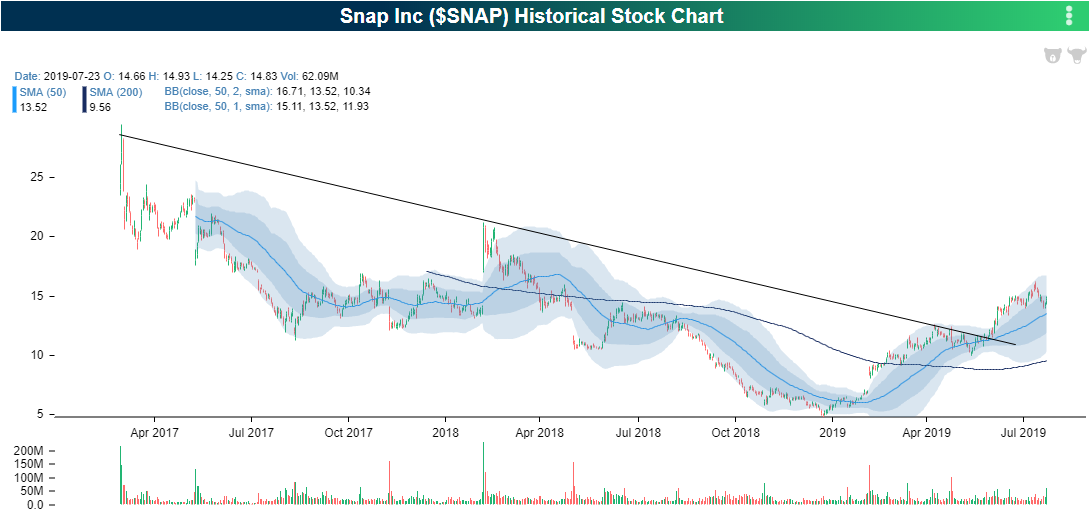

Ahead of Facebook’s (FB) quarter out later today, another social media giant, Snapchat (SNAP), reported last night. Though EPS was still negative (-$0.06), it was also the second smallest loss to date and the second largest revenue per quarter at $388.02 million. SNAP has been in a downtrend since its IPO but earlier this year the stock managed to break out of this downtrend. The 16% gain today has brought the stock further away from this downtrend. Of the ten quarterly reports for SNAP, today is only the third time that the stock has experienced a positive full-day change.

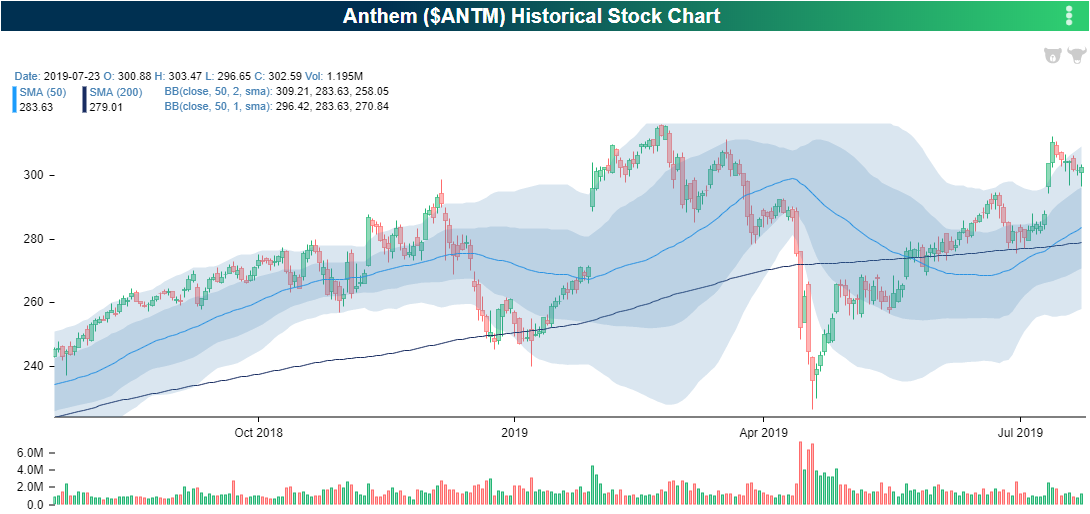

This morning, Anthem (ANTM) also reported a triple play. Its third triple play in a row, ANTM also has not missed EPS since 2016. Perhaps the most impressive streak for ANTM in regards to earnings is in the past seven quarters, the stock has seen a full day gain each time. Despite the triple play today, this streak is looking like it will come to an end. As of this writing, the stock is down 4.18% in today’s trading. Granted, it is also well off of the day’s lows that stopped just short of the 200-DMA. But if the stock was to have seen a positive reaction today, it could have run back up to resistance around the $315 level.

Finally, Teledyne (TDY) saw a solid EPS beat and revenues slightly above estimates. TDY has never missed EPS estimates in its 59 quarter history, although it has only beaten sales 59% of the time. The last two times the stock reported a triple play it saw a full day decline of 1.19% and 0.6%. Today it has bucked this trend with a 5.61% gain. Like MANH, this move higher has brought the stock to elevated levels as it has sat in a steady uptrend this year. Access all of the day’s earnings triple plays with a Bespoke Premium membership. Click here to start a two-week free trial.

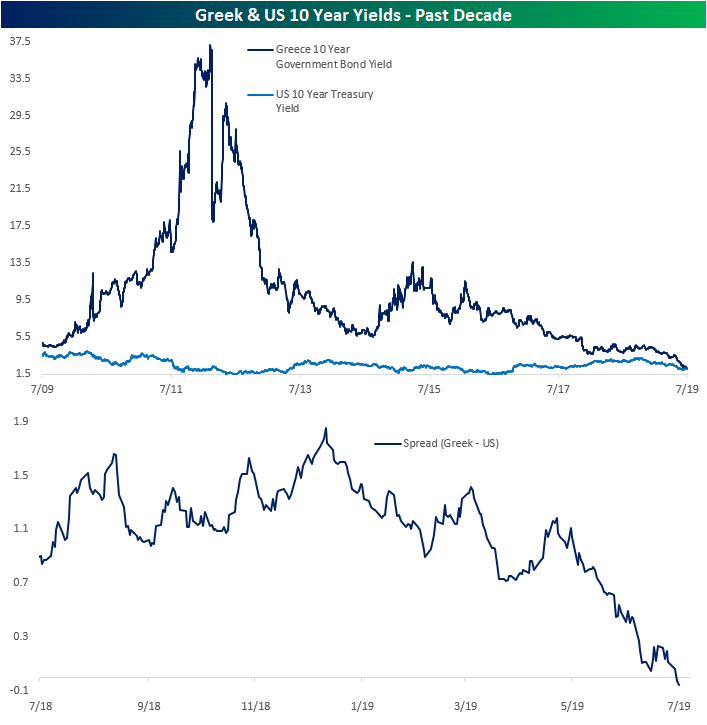

Greece 10 Year Yields Fall Below 10 Year UST

Earlier this month, some headlines noted that Greece’s 10-year government bond yields fell below that of US Treasuries of the same maturity. This came on hopes of ECB easing as well as a victory of the New Democracy party in the most recent election. Today, Greek government bond yields have fallen further to fresh lows with the 10-year yield now a hair under 2% while the US 10 year yields 2.05%. This is the first time since Q4 of 2007 that Greek 10-year debt has had a lower yield than the same maturity in the US. Where they currently stand is a far cry from earlier in the decade when Greek yields surged when the country was dealing with bankruptcy.

But there is one caveat to this comparison. These yields are in local currency. Even though the yields may appear to be relatively similar, controlling for currency differences, Greece’s bond would yield more. If the Greek 10 year (EUR denominated) was swapped to USD it would actually have a much higher yield than the US treasury yield (USD denominated). To be specific, swapping cashflows from EUR to USD shows the Greek 10 year currently yields 4.75% in USD equivalent, more than 250 bps over the 10y UST yield.

The biggest reason for the difference in yields across the two currencies is that the benchmark/policy rates are different. The ECB’s current policy rate is set at -0.4% whereas in the US that rate is significantly higher at 2.4%. Relative to their respective benchmarks, the Greek yield is actually higher, especially compared to other Eurozone countries; some of which even have negative yields at the ten-year maturity. In the table below, we show these rates for the 23 countries in our Global Macro Dashboard also adding in Greece. In other words, while the fact that the lower yield on Greek 10-year debt doesn’t seem to make sense at face value, the comparison in yields is not necessarily like-for-like. Start a two-week free trial to Bespoke Institutional to access our Global Macro Dashboard and much more.

Chart of the Day: Higher Opens, Flat Intraday

In today’s Chart of the Day, we update a chart we have referenced often over the years. It shows the performance of the S&P 500 ETF (SPY) since it began trading in 1993 broken up by after-hours trading and intraday trading. The after-hours strategy measures the performance of SPY had you brought the ETF at its closing price every day and sold it at the next trading day’s open. The intraday strategy measures the performance of SPY had you bought the ETF at the open every day and sold it at the close that same day.

See whether the after-hours or intraday strategy has performed better by continuing this Chart of the Day by logging in (if you’re already a member) or starting a two-week free trial to any of our research membership levels.

Fixed Income Weekly – 7/24/19

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we review front end inversions around the world that haven’t led to a widening in credit spreads.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!