Q2 2025 Earnings Conference Call Recaps: Generac (GNRC)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Generac’s (GNRC) Q2 2025 earnings call.

![]()

Generac (GNRC) is a manufacturer of backup power generation equipment and energy technology solutions for residential, commercial, and industrial markets. Best known for its home standby generators, Generac also provides portable generators, energy storage systems, and grid services, serving everyone from homeowners in storm-prone regions to hyperscale data centers requiring megawatt-scale power resilience. Its growing presence in the data center and telecom markets, along with recurring revenue streams from smart thermostats (ecobee) and energy monitoring subscriptions, adds depth to its traditional hardware footprint. Generac’s Q2 call highlighted net sales rising 6% to $1.06B and adjusted EBITDA margins improving to 17.7%. The breakout story was Generac’s formal entry into the data center backup power market, driven by AI-related infrastructure needs, already generating a $150M backlog. Residential energy tech impressed, with ecobee turning a profit and shipments into Puerto Rico surging. Home standby sales held steady despite low outages, while portable gens gained retail market share. C&I (Commercial and Industrial) strength was offset by rental market softness. The company is recalibrating clean energy investments as solar incentives fade, aiming to eliminate losses. GNRC shares boomed 20% on 7/30 in reaction to the strong results…

Continue reading our Conference Call Recap for GNRC by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Top Quotes from Today’s Earnings Calls: 7/30/25

We sifted through earnings calls from the biggest companies that reported since last night’s (7/29) close, looking for some of the most interesting macro-related quotes from management teams that may serve as broader signals about the state of the economy, consumers, and markets. Below are twenty of the most revealing quotes that we pulled from this batch of calls, offering a window into what executives are seeing across industries and geographies right now.

- Visa (V): “The bulk of those [emerging] markets around the world are very cash-rich markets… where we haven’t been as successful digitizing cash as we have in more mature markets. And so to the extent that stablecoins get adopted in a broad-based way by both consumers and businesses, I think that could accelerate our progress digitizing consumer payments and business, small business, and commercial payments in those markets… I do think that there is real product market fit for stablecoins in remittances for certain corridors.” – Ryan McInerney, President, CEO

- Starbucks (SBUX): “Both the tariff environment and coffee prices continue to be dynamic. We continue to mitigate expected tariff exposure outside of green coffee and are pleased to see green coffee prices moderate… moving average coffee costs and coffee tariff impacts lag the market with year-over-year coffee cost increases expected to peak in the first half of fiscal 2026.” – Catherine Smith, CFO

- Mondelez Int’l (MDLZ): “The US is a little bit more of a difficult situation. There’s a lot of consumer anxiety. They look at a quite uncertain outlook as it relates to their personal finances, job expectations, inflation. So they tend to focus more on essential items. The size of the basket is getting very important, absolute price points. There’s channel shifting going on. There’s more promotions and some pack shifting, too.” – Dirk Van de Put, CEO

- Caesars Entertainment (CZR): “I don’t really see anything particularly when we look at the business as a whole, Vegas, Regional and Digital that suggests there’s anything particularly concerning about the consumer… The only thing I could point to… is the international business, particularly Canadian, is softer.” – Thomas Reeg, CEO

- Booking (BKNG): “We see generally top end of the U.S. consumer market will be a little stronger, spending more in the 5-star hotel category, spending more on international travel… At the lower end, more careful behavior… more pressure on the domestic travel, on the lower-star rated hotels.” – Ewout Steenbergen, CFO

- GE HealthCare (GEHC): “One of the things we’ve talked about [in the US] is an aging installed base, particularly in imaging, probably older than many around the world, some of that with the pauses that took place during COVID. So there is a robust replacement cycle… The other aspect is many of the new clinical products that are coming out… are driving the need for advanced cath labs… The other, which is a big obvious one, is the need for productivity. It’s difficult for U.S. hospitals to get staffed. And so equipment that moves the patient swiftly through the institution with a high-quality diagnosis is a very important asset… We haven’t seen any significant pullbacks… even from some of the most recent bills that were passed in Washington.” – Peter Arduini, President, CEO

- Republic Services (RSG): “I mean you think about manufacturing, and this is where trade policy impacts us, which is [that] manufacturers are not making capital decisions, right? Production is slow. You can see that through PMI. Now somewhat optimistic here, we see a recovery of that. But that’s what’s impacted us to date and that we’re forecasting being conservative for the rest of the year.” – Jon Vander Ark, President, CEO

- Illinois Tool Works (ITW): “We saw a significant increase in the number of big orders. Semi, which is a fairly small percentage [of our total revenues], growing double-digits. If you were an optimist, you would say we’re seeing the first encouraging signs that [industrial CapEx] is really working.” – Michael Larsen, CFO

- Bunge Global (BG): “I think the one thing the last five, six years have taught us is the world’s a pretty dynamic place now… China’s very public that they’re focused on food security. So, I think it’s absolutely logical and rational that they continue to build different optionality. And I would say the importation of soy meal is a new option that they’re now developing.” – Greg Heckman, CEO

- UBS (UBS): “As we continue to see strong market performance in risk assets combined with a weak US dollar, investor sentiment remains broadly constructive, albeit tempered by ongoing uncertainties and a degree of news fatigue. Having said that, clients are ready to deploy capital as soon as conviction around the macro outlook strengthens.” – Sergio Ermotti, CEO

- Smurfit Westrock (SW): “We’ve always kind of said that the real impact on the system would be what happened to consumer demand… nothing yet to suggest that demand picture will change very quickly, and we’re certainly not baking that into any of our forecasts. Volume is okay, demand is okay, but could be a whole lot better. And I think as the tariff picture settles in, I think we’ll see where consumer confidence might come back in certain areas that’s been lacking, I think, in the last year or so.” – Ken Bowles, CFO

- Kraft Heinz (KHC): “In terms of inflation before tariffs, we have the peak of the commodities hitting in Q2. But some of that, in terms of P&L recognition, got pushed into Q3. And we should expect some sort of relief starting in Q4. So it should start to reach the inflection point. We still have pockets of high commodity inflation, particularly on coffee.” – Andre Maciel, CFO

- Trane Technologies (TT): “Transport [has] been very volatile. I think we kid ourselves and say we’re in year three of a two-year cycle, or maybe even year four of a two-year down cycle… We do see that ACT is going to come back. We’re looking forward to this coming back in 2026, and we’re going to be ready for it.” – Dave Regnery, CEO

- Automatic Data (ADP): “We are seeing meaningful productivity improvements and opportunities [from our deployment of Generative AI]. Yet, we are able to actually see some operational headcount reduction in those businesses as a result of Generative AI and some of the other like-minded tools. But again, we are still in a net investment position, likely that will continue through this fiscal year.” – Peter Hadley, CFO

- American Electric (AEP): “Texas House Bill 5247… essentially eliminates, further streamlining the regulatory process, and substantially improving the earned ROEs. This is highly supportive of increasing capital allocation [into Texas energy infrastructure]… as we participate in the massive infrastructure build-out needed to drive economic growth in the state.” – Trevor I. Mihalik, CFO

- PPG Industries (PPG): “Any stimulus, any catalyst, whether it be the impact of a tariff agreement, whether we see some progress in Ukraine, whether we see some progress in the Middle East, anything that would give a little bit of consumer confidence in Europe would be a positive… because actually the household balance sheets are pretty strong, generally speaking. So it’s much more about consumer confidence.” – Timothy M. Knavish, CEO

- Avis Budget (CAR): “Over time autonomous vehicles is touching the meatiest part of the mobility ecosystem, which is vehicle miles driven. That opens up a lot of other areas that we can play in as well in terms of expanding our horizons. So right now the core of the business is the rental car business. But as the years progress, I think we can expand our footprint.” – Brian Choi, CEO

- CGI Group (GIB): “I think we’re at the floor, right? I think we’re starting to see an end to [tariffs] or some agreement across our world. And I think when these agreements will be finalized, that will bring to the clients a certainty… and what will be the impact on the economy… I think it will take still a couple of quarters to arrive to that.” – Steve Perron, CFO

- Vertiv Holdings (VRT): “If we think about the US environment, we see a lot of attention from the administration for [data centers and AI infrastructure]… but also my comment was a little bit [intended] towards EMEA, where we see national governments, the EU, but also places like the UK, more aware of the importance and the strategic importance of AI… We believe times will soon be mature for an acceleration in Europe and EMEA.” – Giordano Albertazzi, CEO

- Altria (MO): “Inflation is still an unknown variable going forward. There’s been some green shoots, lower gas prices on a year-over-year basis, even though they remain high. Most recently, we have seen an uptick in consumer confidence. But again, the macroeconomic environment remains dynamic, and somewhat unsettled. Trade deals are still being negotiated, and what potential impact that could have on controllable spending for the consumer is something that we’ll pay close attention to.” – Sal Mancuso, CFO

Q2 2025 Earnings Conference Call Recaps: Visa (V)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Visa’s (V) Q3 2025 earnings call.

![]()

Visa (V) is a payments technology company that connects consumers, merchants, financial institutions, and governments across more than 200 countries and territories. It doesn’t issue cards or extend credit, but enables electronic payments via its network, VisaNet, which securely processes over 260 billion transactions annually. It serves everyone from large banks to fintech startups and small merchants, and increasingly operates in newer arenas like real-time payments, open banking, and blockchain-based stablecoins. Visa reported strong Q3 results with net revenue up 14% YoY to $10.2B and EPS up 23%. Consumer spending remained resilient across income segments, with US e-commerce growing faster than in-store. Cross-border volume (ex-Intra Europe) rose 11%, despite FX headwinds and a weak Canada–US travel corridor. Visa Direct transactions jumped 25%, driven by growing remittance use cases. The company highlighted major progress in AI-driven agentic commerce and stablecoin-based settlement, supporting both as long-term growth pillars. Value-added services revenue surged 26%, helped by risk tools, advisory, and processing partnerships. Incentives rose with elevated client renewals, but pricing power helped offset the impact. Despite better-than-expected results, V shares slipped slightly into the red on 7/30…

Continue reading our Conference Call Recap for V by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Starbucks (SBUX)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Starbucks’ (SBUX) Q3 2025 earnings call.

![]()

Starbucks (SBUX) is the world’s largest specialty coffee chain, operating over 38,000 stores globally with a strong presence in North America, China, and other international markets. Starbucks caters to a broad customer base, including millennials, Gen Z, and urban professionals. The company is a leader in digital engagement, with nearly 34 million active rewards members and a top-rated mobile app. Its business spans in-café, drive-thru, digital, and delivery channels. This quarter focused heavily on Starbucks’ US turnaround, centered on the accelerated rollout of the Green Apron Service model, a new operating system showing early success in improving transaction comps and service speed. Despite a 2% global comp decline, China returned to comp growth (+2%) and posted strong delivery and beverage innovation gains. Management also detailed plans for loyalty program upgrades, smaller and more efficient store formats, and a shift toward protein-enhanced beverages and functional food. CEO Brian Niccol emphasized the upcoming innovation wave in 2026 and ongoing search for a strategic partner in China, noting over 20 interested parties. SBUX shares opened 5.7% higher on 7/30 on mixed results, but erased those gains intraday…

Continue reading our Conference Call Recap for SBUX by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Booking (BKNG)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Booking’s (BKNG) Q2 2025 earnings call.

![]()

Booking (BKNG) is the world’s largest online travel platform, operating global brands like Booking.com, Priceline, Agoda, KAYAK, and OpenTable. It facilitates millions of accommodations, flights, car rentals, and restaurant reservations, serving both leisure and business travelers. Its Genius loyalty program and Connected Trip vision (bundling multiple travel components into one seamless booking) position it to drive both engagement and margins. Booking delivered a standout quarter, with room nights up 8%, gross bookings up 13%, and adjusted EPS up 32% YoY. Alternative accommodations grew 10%, outpacing hotels, and the Connected Trip saw 30%+ transaction growth. Asia was the fastest-growing region, while US consumers showed caution via shorter stays and lower ADRs. AI tools like Priceline’s Penny and OpenTable’s Concierge are boosting efficiency and conversion, and direct bookings now exceed 65% of B2C volume. BKNG shares were up less than 1% on 7/30 on EPS and revenue beats…

Continue reading our Conference Call Recap for BKNG by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Polaris (PII)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Polaris’ (PII) Q2 2025 earnings call.

![]()

Polaris (PII) is a manufacturer of powersports vehicles, including off-road vehicles (ORVs), snowmobiles, motorcycles (Indian and Slingshot), and marine products, like Bennington pontoons. Polaris dominates niche markets such as utility and recreational side-by-sides, offering high-quality vehicles with strong dealer support. The company serves outdoor enthusiasts, farmers, commercial users, and lifestyle buyers, while also providing parts, gear, and accessories to enhance the ownership experience. Polaris exceeded expectations despite a 6% sales decline, driven by industry weakness and tariffs. Share gains across every segment were fueled by standout products like the XPEDITION and the newly launched RANGER 500, targeting value-focused buyers at $9,099. Tariffs remain a headwind, with an estimated $230M annualized impact, though the company has cut its China sourcing by nearly half and aims to reduce exposure by 35% by year-end. Retail demand was flat but stable, with utility vehicles showing strength, while promotions and interest rates pressured margins. PII shares were up 16.9% on 7/29 after posting stronger than expected results and launching new vehicles…

Continue reading our Conference Call Recap for PII by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: JetBlue (JBLU)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers JetBlue’s (JBLU) Q2 2025 earnings call.

![]()

JetBlue (JBLU) is a US-based low-cost carrier, offering free in-flight Wi-Fi, live TV, and extra legroom options. Serving leisure and value-conscious travelers across the US, Latin America, and transatlantic routes, JBLU operates a primarily Airbus fleet, including its efficient A220 and A320 aircraft. The company also runs a growing travel products business through its Paisly platform and has built a loyal following through its TrueBlue rewards program. JBLU delivered a modest operating profit in Q2 as it advanced its JetForward transformation, generating $180M in EBIT YTD. The standout announcement was Blue Sky, a new partnership with United Airlines that enables cross-selling, loyalty integration, and Paisly white-label expansion. It is expected to drive $50M in incremental EBIT by 2027. Close-in bookings surged mid-quarter, particularly around peak travel, though management remains cautious about calling the shift permanent. The forecast for grounded aircraft tied to Pratt & Whitney engine issues improved, clearing a path for low single-digit capacity growth in 2026. The stock was up 6.7% on 7/29 on better-than-expected results…

Continue reading our Conference Call Recap for JBLU by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day – Consistently Overbought

The Triple Play Report — 7/30/25

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 21 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

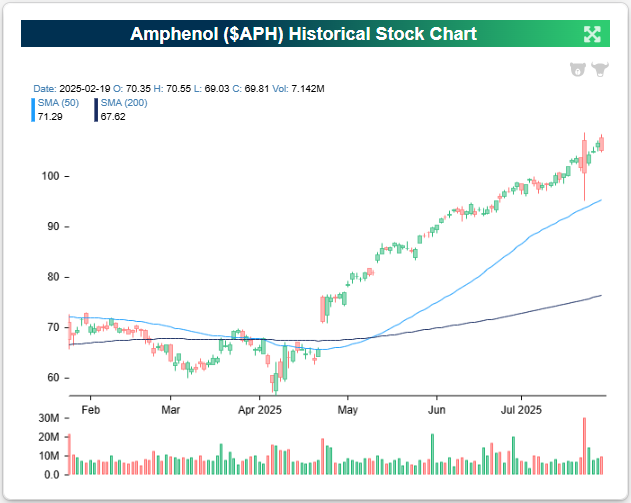

Amphenol (APH) is an example of a company that recently reported an earnings triple play before the open on 7/23. It was the company’s third straight triple play, but the stock turned negative that day after the positive moves in reaction to the two prior triple plays.

Here’s how AI describes the company: Amphenol (APH) is one of the world’s largest designers, manufacturers, and marketers of electrical, electronic, and fiber optic connectors, as well as interconnect systems, coaxial and specialty cables, and high-performance sensors. The company’s core function is to enable high-speed signal transmission and power distribution across a wide range of demanding environments, serving industries such as automotive, aerospace, defense, industrial, IT/data communications, mobile devices, and broadband. Amphenol operates through three primary business segments: Harsh Environment Solutions, Communications Solutions, and Interconnect and Sensor Systems. The Harsh Environment Solutions segment provides ruggedized connectors and interconnects used in military, commercial aerospace, automotive, and heavy industrial markets. Communications Solutions serves the mobile devices and IT/data communications markets, supplying connectors for smartphones, tablets, servers, and networking equipment. Interconnect and Sensor Systems covers a broad industrial and transportation footprint, including sensors and interconnects used in factory automation, rail, green energy, medical, and hybrid-electric vehicle applications.

Amphenol posted a blockbuster Q2 with record sales of $5.65B, up 57% YoY and 41% organically, as every end market delivered double-digit organic growth. The standout driver was AI-fueled demand in the IT datacom segment, which surged 133% organically and now makes up 36% of total sales. CEO Adam Norwitt said the company actually shipped “substantially more than expected,” including some Q3 volume, because “our team outperformed even our customers’ very high expectations.” Roughly two-thirds of both YoY and sequential IT datacom growth came from AI-related products, which Amphenol delivers across the stack, from chipmakers to hyperscalers, thanks to its critical role in high-speed, power, and fiber-optic interconnects. Even with some pull-forward, Q3 sales are only expected to dip mid-single digits, and Norwitt emphasized they’re still winning new AI programs and expanding capacity globally, supported by elevated CapEx. Outside of AI, defense sales rose 25% YoY, with global geopolitical tensions driving long-term opportunity, and European industrial sales turned positive, with broad strength in factory automation, medical, and alternative energy.

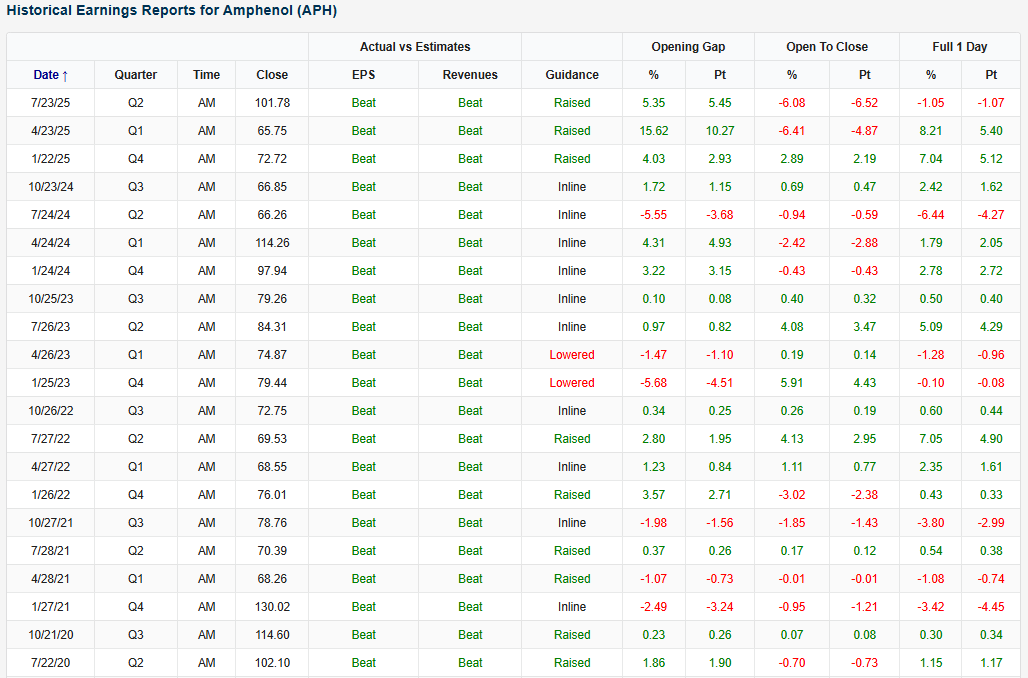

Looking at the snapshot below from our Earnings Explorer, Amphenol (APH) has been on a triple play hot streak, with very strong EPS and revenue beat rates, 91% and 94%, respectively, since 2001 when our database begins. The company’s EPS beat streak goes back to 2020 and 2016 for revenue.

You can read more about APH and the 20 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 7/30/25 – Should This Worry You?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Measuring programming progress by lines of code is like measuring aircraft building progress by weight.” – Bill Gates

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are modestly higher this morning after the July ADP report came in better than expected, erasing a streak of three months of weaker-than-expected readings. Q2 advance GDP was also just released and came in stronger than expected (3.0% vs 2.6%). Personal Consumption was weaker than expected (1.4% vs 1.5%) while the inflation data was mixed (lower than expected at the headline, higher than expected on a core basis). While these would be big reports on a normal day, we still have the Fed this afternoon and earnings from Meta and Microsoft after the close.

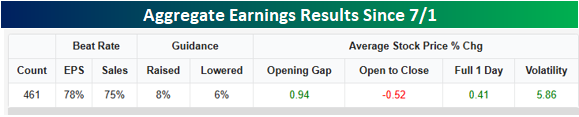

We’re right in the thick of earnings season, and we’ll see hundreds of more reports between now and the end of the week. From the start of July through Tuesday morning, we’ve already got 461 reports, and of those, 78% exceeded EPS forecasts while 75% have topped sales estimates. Looking forward, 8% of companies reporting have raised their guidance, while just 6% have lowered their estimates. These are all better than average readings, and as you would expect, companies are reacting positively to these reports. Overall, the average opening gap of the companies reporting has been a gain of 0.94%, but from the open to close, we’ve seen selling into strength with an average decline of 0.52% for a full-day gain of 0.41%. On the one hand, the average positive reaction to earnings reports is a good signal, but the weakness from the open to close indicates that investors are taking profits.

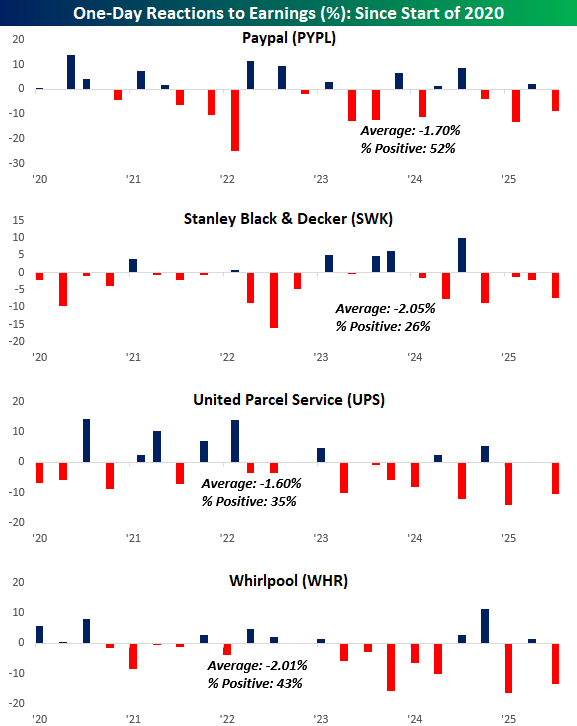

Despite the overall positive tone of reports, yesterday we saw multiple stories highlighting four stocks and their negative reaction to earnings as a potential warning sign for the economy and market. Those four stocks were PayPal (PYPL), Stanley Black & Decker (SWK), United Parcel Service (UPS), and Whirlpool (WHR), and all of them were down at least 7%.

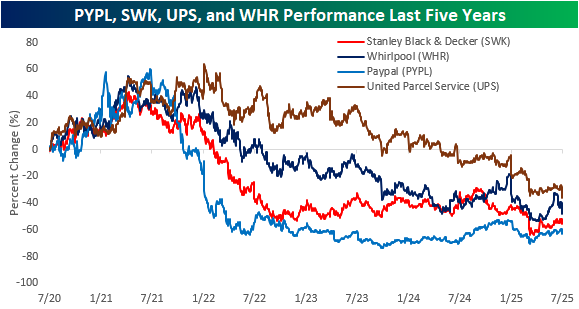

Besides the fact that these four stocks have a combined market cap of less than $160 billion, which wouldn’t even be enough to rank in the top 75 companies in the S&P 500, they have all historically had weak reactions to earnings, especially in recent years. The chart below shows each stock’s performance on its earnings reaction days over the last five years. All four have averaged declines of at least 1.6% on their earnings reaction days, and only PYPL has reacted positively more often than it has reacted negatively.

More importantly than the performance on their earnings reaction days, all four stocks have been horrendous performers over the last five years. As shown in the chart below, at one point in the last five years, all four stocks were up at least 40% from where they traded five years ago, but they have erased those gains and more over the last five years. UPS is down 36%, WHR is down 48%, while PYPL and SWK have both lost over half of their value. During this same period, the S&P 500 has rallied 96%. Far from being economic or market bellwethers, these stocks have been among the S&P 500’s worst performers over the last five years! We could highlight any number of reasons why investors should be more cautious heading into the end of summer, but the fact that four stocks that have historically performed poorly on earnings saw weakness yesterday is not one of them.