Bespoke Stock Scores — 8/6/19

JOLTS Stronger Than Expected

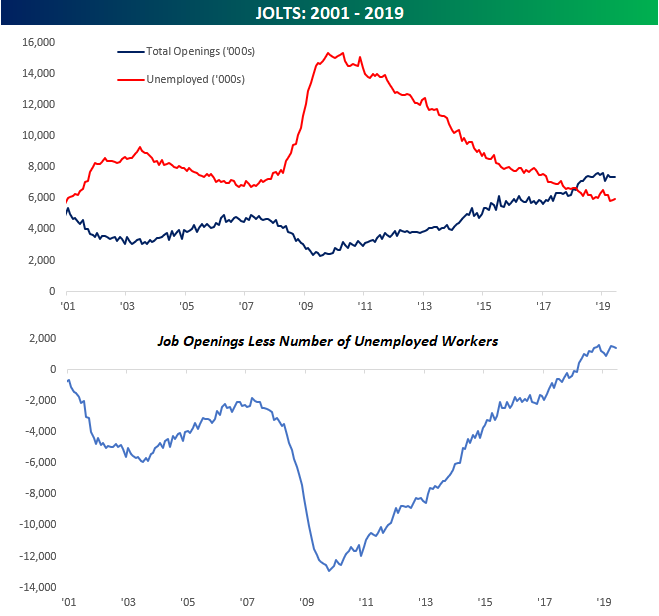

This morning’s release of the Job Openings and Labor Turnover Survey (JOLTS) for the month of June showed a stronger than expected picture in terms of the number of job openings, while last month’s was revised higher. Economists were expecting the number of job openings to come in at 7.326 million but the actual level was 22K stronger at 7.348 million. Besides the fact that the June reading was higher than expected, the most notable aspect of the JOLTS report continues to be how there are more job openings than there are available workers. The shift in the jobs vs. available workers dynamic first shifted in February 2018 but has remained that way ever since and currently stands at 1.373 million more jobs than there are workers. While the ‘shortage’ of workers raised concerns that it would accelerate upward pressure on wages, at this point we have yet to see signs that wages are beginning to spiral out of control.

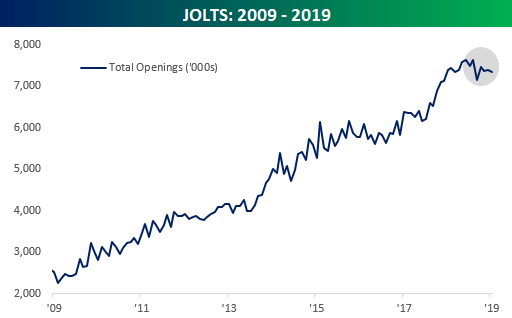

While the above picture portrays a jobs market that is red hot, we would note that there has been some slowing in recent months. As shown in the chart below, the last time the JOLTS survey made a new high was seven months ago in November. Things are far from falling off a cliff when it comes to the employment picture, but for the time being, they aren’t accelerating either. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Chart of the Day: Summer Flops for Disney (DIS)

In today’s Chart of the Day, we preview Disney’s (DIS) upcoming earnings report and also highlight a key trend that has historically impacted the performance of its stock following prior August earnings reports.

To view the report and see how Disney tends to react to its August earnings reports, start a two-week free trial to any of our research membership levels.

Trend Analyzer – 8/6/19 – What A Difference One Week Makes

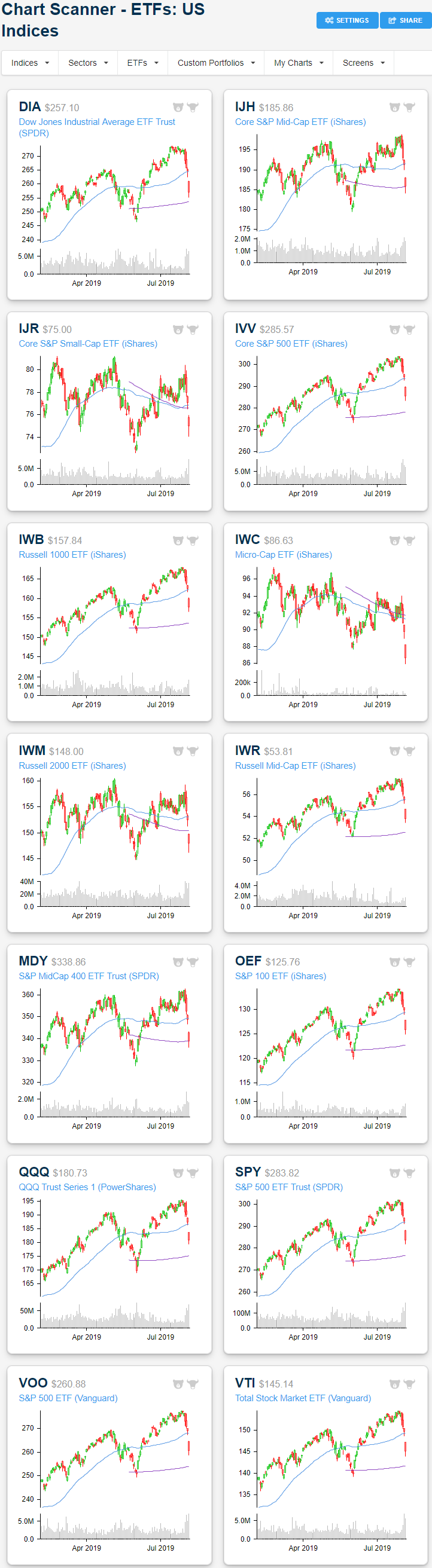

As we mentioned in a series of tweets earlier this morning, our Trend Analyzer one week ago looked a bit different than it does now. Last week, before the FOMC rate decision and the escalation of tariff tensions sent markets into a tailspin, almost all of the major US indices were overbought and had distanced themselves above their 50-DMAs. Now, in the Trend Analyzer, the reverse is true as every major index ETF has crashed through their respective 50-days, leaving ten of the fourteen oversold. Leading the way to the downside, the Micro-Cap (IWC) ETF is about as oversold as it gets as it has fallen over 3 standard deviations below the 50-DMA. With the most recent move lower, IWC is now showing a downtrend as well; the only one to show this. The four that are not oversold are just barely neutral and it would take only a little more downside for them to join the others. Ironically, one of these is the Nasdaq 100 (QQQ). While not by any significant degree, QQQ is just above oversold levels even after a 7.14% decline over the past week; the most of any major index ETF. The Nasdaq 100 has fallen more sharply than its peers as all of the others have seen declines of somewhere between 4.75% and just over 6% in that same time frame.

The past week’s steep declines have done some damage to the chart setups of these same ETFs. Across all of these ETFs, recent shorter-term uptrends have all been broken in addition to the 50-DMAs providing little to no support after yesterday’s steep gap lower at the open. For small caps like the Core S&P Small-Cap ETF (IJR) or the Micro-Cap (IWC), the 200-DMA did not provide any support either. But for mid-caps like the Core S&P Mid-Cap (IJH), buying during the day brought the ETFs off of the day’s lows and back near the 200-DMA. With equities seeing strong pre-market trading today, mid-caps could see a bounce off of this support at the open. Large caps, on the other hand, are more or less in no man’s land between the 50-DMA, 200-DMA, and prior highs and lows. While the past few days’ declines have been steep, we must also note that every major index ETF (except for IWC) is still above the lows from late May/early June. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Bespoke’s Morning Lineup – Round and Round She Goes…

Where she stops nobody knows. US futures have moved all over the place overnight but are currently pointing to a modestly higher open after Monday’s plunge. Things looked like they would be a whole lot worse shortly after the close yesterday when the US Treasury officially designated China a currency manipulator in what was basically a “surprising-not surprising move.” Surprising in that the timing wasn’t entirely anticipated but not surprising as it’s nothing the President hasn’t been saying incessantly going all the way back to his days on the campaign trail. Well, the initial response from the algos was to sell spoos lower to the tune of 2%, but after the Chinese government fixed the yuan under 7 later on in the night, futures have been grinding higher, erasing all of the initial knee-jerk reaction.

With equity futures rallying, we’re seeing the usual risk-on assets rallying while treasuries and gold ease off their overnight highs. During rudderless times like this, though, it’s important to remember that up futures are as meaningless as down futures in terms of where things will be when we close out the day or even at the open for that matter.

Continue reading in today’s Morning Lineup.

Bespoke Morning Lineup – 8/6/19

The Closer – The Few, The Proud – 8/5/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, as markets were sent reeling today in response to further escalations in the trade war, we show just how few stocks moved higher in today’s session and what performance has looked like following similar weak breadth readings. We also show how substantial the weakness has been across industry groups with a particular focus on semiconductors. We then look at some of the drivers and technicals of the yuan before finishing on some macroeconomic data including the ISM and Markit PMIs and the Sentix investor sentiment survey.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

B.I.G. Tips – Monday Meltdown Follow-up

Investors Turning to Safe Havens

As equities sell-off sharply, cyclical and trade-sensitive businesses, in particular, have fallen on hard times as investors rotate into defensives. While still down today, sectors like Utilities, Consumer Staples, and Real Estate have held up slightly better. In commodities, this same dynamic has played out. Copper, which is a bellwether for global manufacturing activity, has fallen sharply in response to trade tensions and concerns over global growth. Meanwhile, gold’s safety status has led it to rally. In Monday’s session, gold has been one of the few assets to rally, rising 1.84% from Friday’s close. Looking at the ratio between the two commodities over the past few years shows just how much gold has been outperforming. While it has been rising slowly over the past year, the ratio has really ripped higher in the past week. In fact, over the past week, the relative strength of gold versus copper has seen its largest short-term move since February 2016.

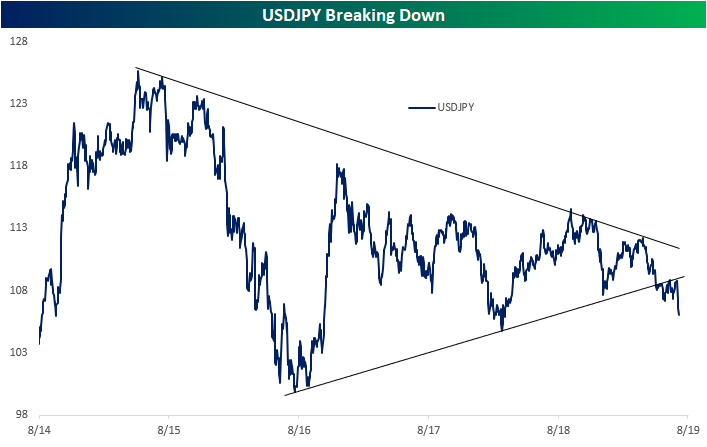

Similarly, the Japanese Yen which is commonly viewed as a safe haven currency has been surging versus the dollar. Over the past several years, USDJPY has been in consolidation. After bottoming this time of year in 2016, the cross made a series of higher lows and lower highs. Earlier this year, USDJPY failed to take out the downtrend line, continuing to move below the uptrend line. Now, over the past few sessions, the Yen has further appreciated as global trade tensions mount. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

B.I.G. Tips – S&P 500 5%+ Pullbacks

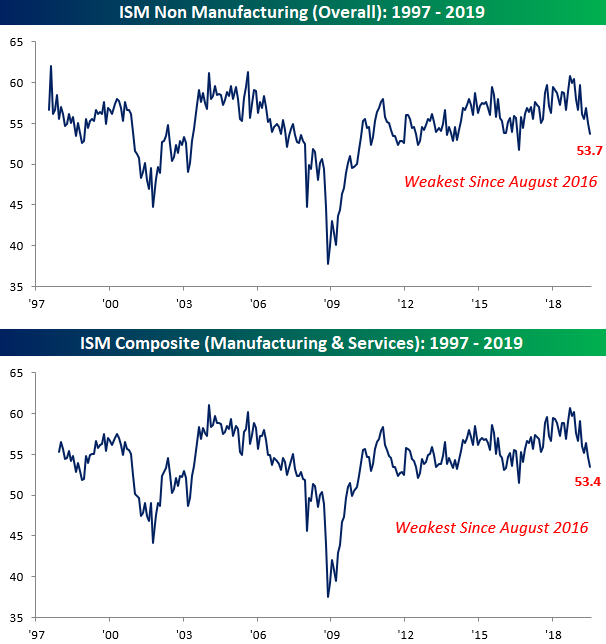

ISM Non Manufacturing Index Near a Three Year Low

Just like its manufacturing counterpart last week, the July release of the ISM Non-Manufacturing survey came in shy of consensus expectations. While economists were expecting the headline reading to increase slightly from 55.1 to 55.5, the actual reading came in at 53.7. That’s a level that is still consistent with steady growth, but it is also the weakest reading since August 2016. Similarly, on a combined basis and accounting for each sector’s share in the economy, the combined Composite PMI for July came in at 53.4, which was the lowest reading since August 2016.

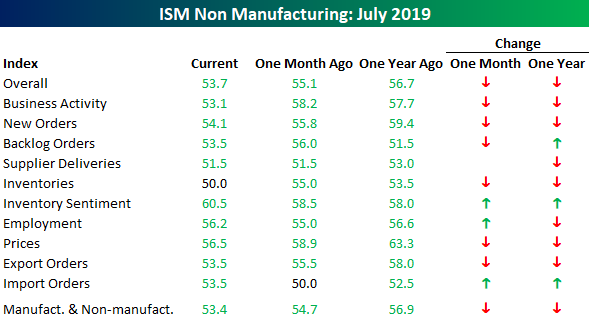

The table below breaks down the July ISM Services report by each of its sub-components and shows their m/m and y/y changes. Breadth in this month’s report was biased to the downside. Compared to June and last year, just three components showed increases.

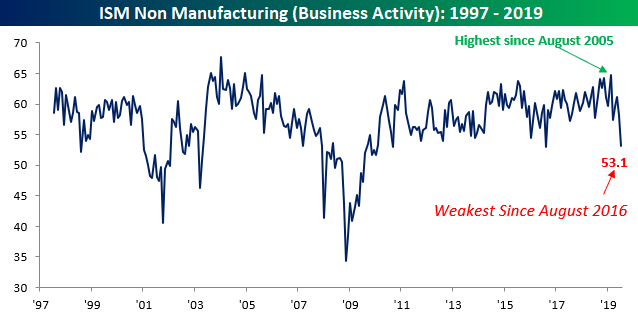

One of the biggest decliners on both a m/m and y/y basis was Business Activity. After hitting its highest level since August 2005 back in March, the index is now at its lowest level since August 2016. Overall, the July ISM Services report wasn’t a disaster, but it certainly wasn’t a picture of strength either. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.