Bespoke’s Sector Snapshot — 8/29/19

Sentiment Still Leaning Bearish

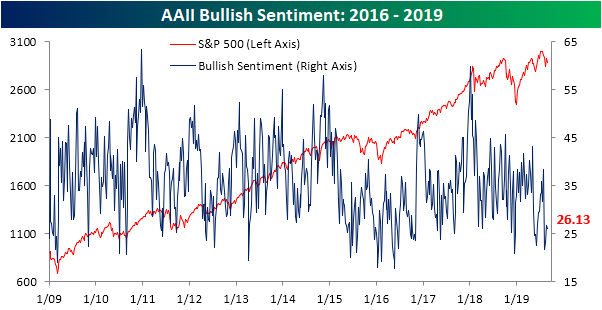

The S&P 500 is up 2.75% since last Friday, which would be the best weekly performance since early June after rebounding from consistent selling in May. Despite this, the index is still range-bound, and sentiment has yet to pick up. This week’s AAII sentiment survey saw the percentage of investors reporting as bullish fall to 26.13% from 26.64% last week. Bullish sentiment has now been more than 1 standard deviation below its historical average for four consecutive weeks. That is only the 12th such streak in the history of the data going back to 1987. The most recent similar streak was an identically long one ending on June 13th of this year.

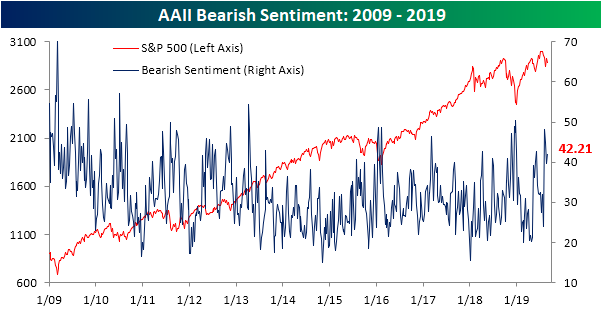

While bullish sentiment saw a fairly mild decline, bearish sentiment rose 3.5 percentage points to 42.21%. Bearish sentiment is still below where it was at the start fo the month when it peaked at 48.2%, but it also remains the predominant sentiment for four weeks running. Negative sentiment is also elevated compared to where it has been historically and has been one standard deviation above the historical average for three of the past four weeks.

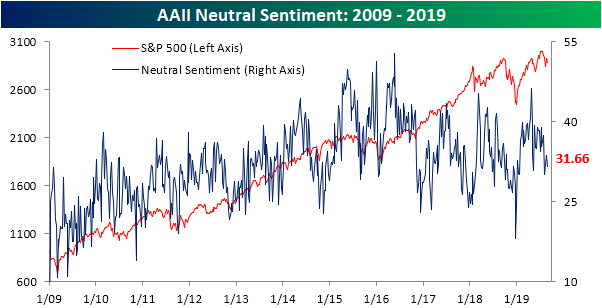

Most of the gains in bearish sentiment came out of the neutral camp. The percentage of investors reporting neutral sentiment fell around 2 percentage points to 31.66%. While this is not a new low, neutral sentiment has been trending lower over the past several weeks after spiking to its highest levels since 2016 earlier this year. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

B.I.G. Tips – Years Like 2019: August Edition

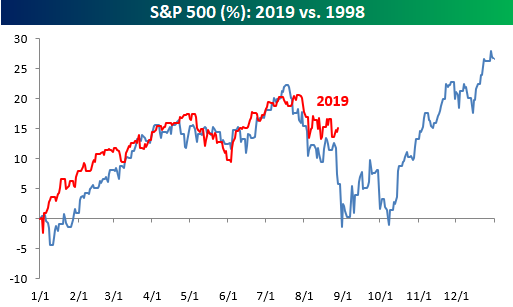

We’ve highlighted the chart below comparing 2019 to 1998 a number of times over the last several weeks, and the similarities between the performance of the S&P 500 in each year has continued right up through the end of August. While the pullback from the highs this Summer hasn’t been as severe as it was in 1998, the timing of both and the subsequent periods of backing and filling has been striking. A continuation of the similar patters certainly wouldn’t be a positive in the short term, but the silver lining is that Q4 1998 was exceptionally strong.

As we do throughout the year, in our most recent B.I.G. Tips report we compared the S&P 500’s trading pattern this year to all other years in order to see which ones were the most similar. With those similar years, we then analyzed how the S&P 500 performed for the remainder of the year in order to help come up with a framework for what to expect for the rest of this year. It shouldn’t surprise anyone that 1998 made the list, but a number of other notable years also had strong similarities to the pattern of 1998 with very different outcomes as well.

For anyone with more than a passing interest in the market’s seasonal patterns, this report is a must-read. To see it, sign up for a monthly Bespoke Premium membership now!

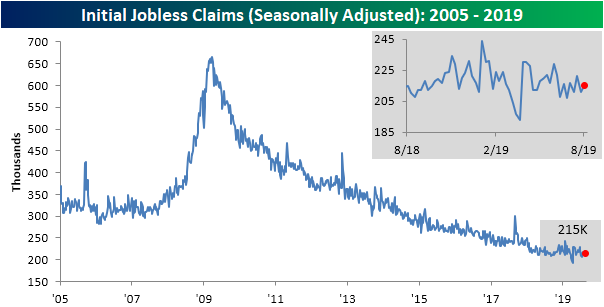

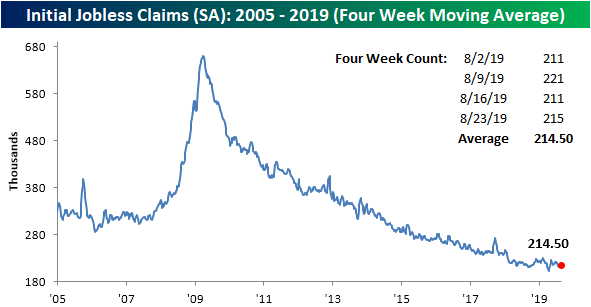

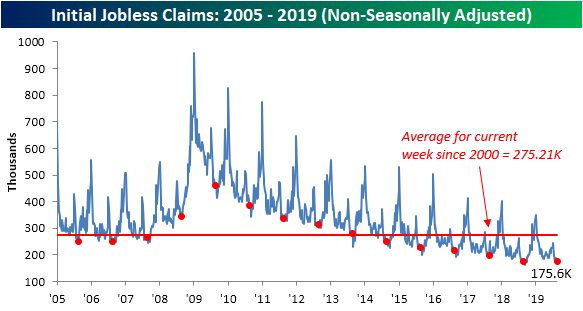

Jobless Claims Snoozefest

Initial jobless claims data were released this morning without any major new developments, largely as a result of seasonal effects. Last week saw claims come in at the lower end of their recent range at 209K. This reading was revised up to 211K and this week’s release showed another small increase to 215K, which was slightly ahead of the 214K forecast. Although claims came in weaker than expected, they remain at strong levels.

Likewise, the four-week moving average came in pretty flat once again this week only falling by 0.5K. With this modest improvement to 214.5K, through all of August, the moving average has been in a tight 2.25K range. This range is also still off of its lows set earlier this year in April.

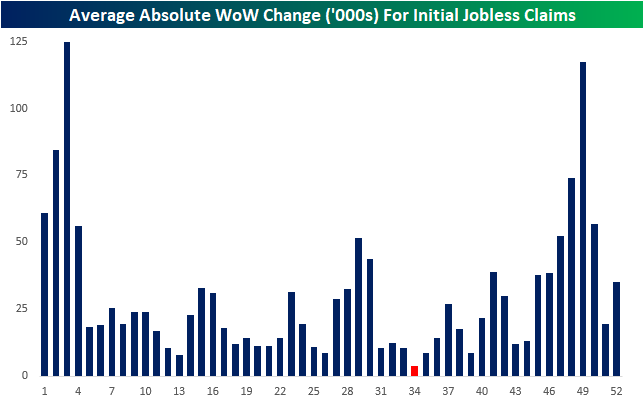

Most of the reason for the lack of movement this week in initial jobless claims data is due to seasonal effects. Looking back at the current week of the year (34th week) over the past ten years, non-seasonally adjusted claims has only seen an average week-over-week change, in absolute terms, of just 3.4K. As shown in the second chart below, that is the smallest change for any given week of the year. That also actually makes this week’s 4.2K increase to 175.6K larger than normal. But still sticking to the script of little changes as well as the broader trend of slowing improvements in labor data, this week’s NSA data was only 0.1K lower year over year. One important thing to consider with this minor improvement from last year, over the next couple of weeks, non-seasonally adjusted claims typically make their yearly low. In other words, in the coming weeks, we should be able to get a pretty good idea on how this year’s low stacks up to prior years of the cycle. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

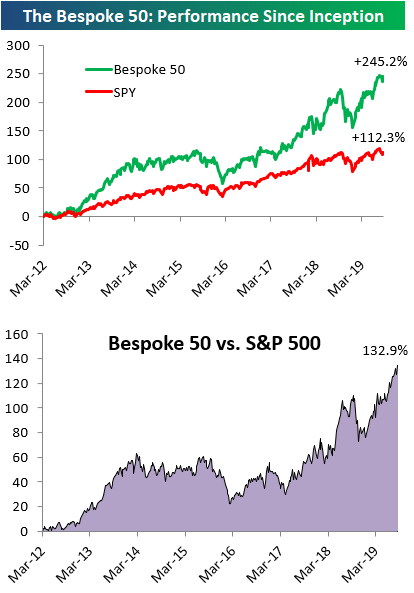

The Bespoke 50 Top Growth Stocks — 8/29/19

Every Thursday, Bespoke publishes its “Bespoke 50” list of top growth stocks in the Russell 3,000. Our “Bespoke 50” portfolio is made up of the 50 stocks that fit a proprietary growth screen that we created a number of years ago. Since inception in early 2012, the “Bespoke 50” has beaten the S&P 500 by 132.9 percentage points. Through today, the “Bespoke 50” is up 245.2% since inception versus the S&P 500’s gain of 112.3%. Always remember, though, that past performance is no guarantee of future returns. To view our “Bespoke 50” list of top growth stocks, please start a two-week free trial to either Bespoke Premium or Bespoke Institutional.

Chart of the Day: SLB Below Financial Crisis Lows, HAL Close

Bespoke’s Morning Lineup — Bulls Step In

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Home On The Range, Mexican Macro, ETF Flow, EIA Inventory Crash – 8/28/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, as the S&P 500 remains rangebound in August, we take a look at the recently lower correlation between stocks and rates. Ahead of tomorrow’s GDP release, we also give an updated look at the Atlanta Fed’s GDPNow growth tracker. Next, we review weekly fund flow data, including data on mutual funds and ETFs. We then recap recent Mexican macro data before looking at the impressive results in this week’s EIA data.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Chart of the Day: Silver Soars But For How Long?

Fixed Income Weekly – 8/28/19

Searching for ways to better understand the fixed income space or looking for actionable ideas in this asset class? Bespoke’s Fixed Income Weekly provides an update on rates and credit every Wednesday. We start off with a fresh piece of analysis driven by what’s in the headlines or driving the market in a given week. We then provide charts of how US Treasury futures and rates are trading, before moving on to a summary of recent fixed income ETF performance, short-term interest rates including money market funds, and a trade idea. We summarize changes and recent developments for a variety of yield curves (UST, bund, Eurodollar, US breakeven inflation and Bespoke’s Global Yield Curve) before finishing with a review of recent UST yield curve changes, spread changes for major credit products and international bonds, and 1 year return profiles for a cross section of the fixed income world.

In this week’s report we show what is different this time about yield curve inversion, even if the outcome may not be different.

Our Fixed Income Weekly helps investors stay on top of fixed income markets and gain new perspective on the developments in interest rates. You can sign up for a Bespoke research trial below to see this week’s report and everything else Bespoke publishes free for the next two weeks!

Click here and start a 14-day free trial to Bespoke Institutional to see our newest Fixed Income Weekly now!