The Closer – Equity Market Mess, Consumer Credit Press – 9/9/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we first take a look at the heavy rotation away from defensives and into low multiple cyclicals. We then review the technical set ups of the overall S&P 500, industrials, and the tech sector. We finish with a recap of the Federal Reserve’s monthly update on consumer credit.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Apple (AAPL) and iPhone Releases

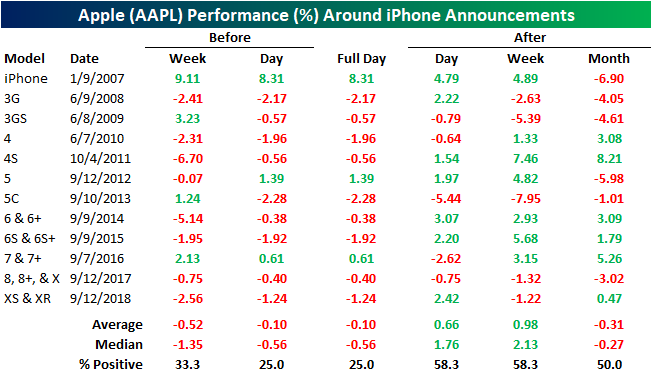

Apple (AAPL) plans to announce the newest version of their iPhone tomorrow (September 10th). Historically, the time leading up to these announcements has seen the stock down in the week and day before. With AAPL up over 2.25% over the past week and also up 0.6% today, the current situation is most similar (in terms of stock price) to 2016 when the company announced the iPhone 7. The stock is similarly weak on the day of new iPhone announcements. The only substantial gain on an iPhone announcement was in 2007 when the company unveiled the very first generation. Other than that, there were only two other times that AAPL moved higher when a new model of the iPhone was unveiled. Fortunately, over the following day and week, the stock’s performance is a little better with gains slightly more than half the time. One month later, though, a period that usually covers the entire span between the announcement and the time the phone typically hits shelves, the probability of a positive response is no better than a coinflip and AAPL is down an average 31 bps.

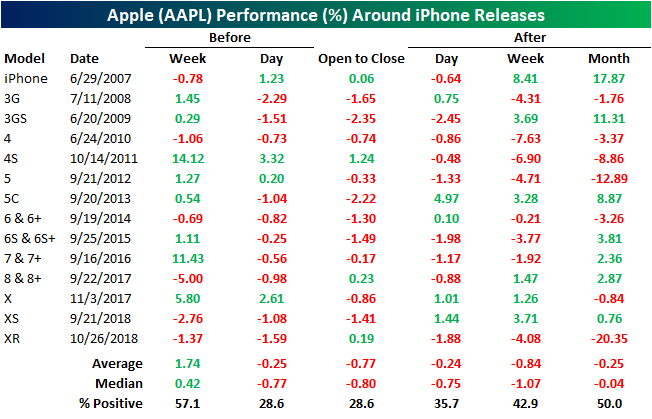

The release (when the phone is actually available for sale) of previous generations of the iPhone have typically come within the month that it gets announced. Following these releases, AAPL’s stock typically makes its way higher over 70% of the time in the week and day before. Immediately after the phone is available for sale, though, AAPL consistently falls. The first day the new version of the iPhone is for sale, AAPL stock averages a decline of a quarter percent while the median is even worse at -0.77%. AAPL also consistently is negative both that day and the following day. Performance one week and one month later is similarly weak, but it has also been positive a little more frequently. Even one month out, though, AAPL was only higher half of the time. Headed into tomorrow, AAPL is coming off of one of the worst post-release stock price responses to a new iPhone. Last October saw the release of the most recent iPhone, the iPhone XR. One month later, the stock was down over 20%. No other release has seen a subsequent decline of nearly that much.

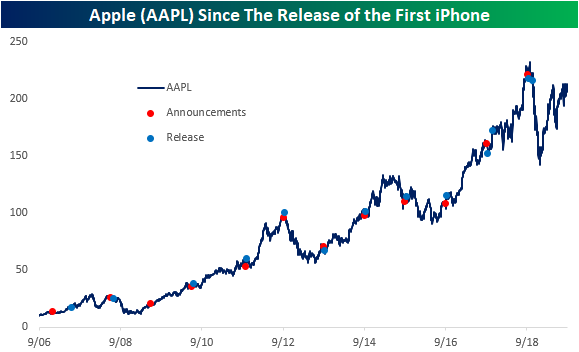

As shown in the chart below, since the company unveiled the very first iPhone back in 2007, iPhone announcements and releases for the most part, do not mark any major tops or bottoms for the stock. Only the aforementioned release of the iPhone XR and the iPhone 5 in 2012 resulted in a short to medium-term peak for the stock. Over the long run, even these poorly received products did little to completely break the stock’s long term uptrend that has been in place for many years now. Since the announcement of the first iPhone, AAPL has risen over 1500% which is more than ten times the gain in the S&P 500 over that same span. Start a two-week free trial to Bespoke Institutional to access our interactive Security Analysis tool and much more.

A Storm Beneath the Surface

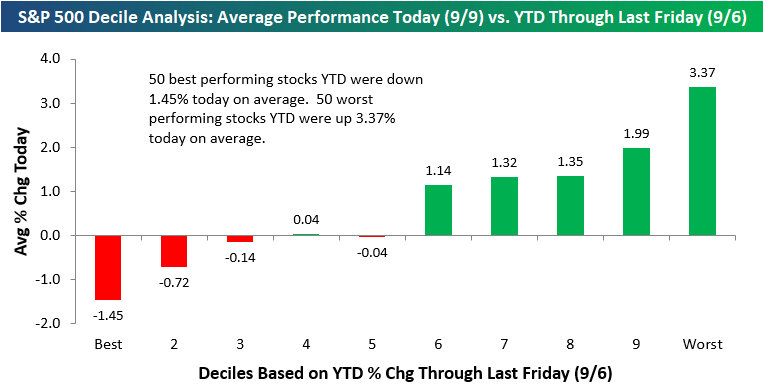

The S&P 500 traded almost exactly flat today (-0.01%), but we saw huge moves underneath the surface. Below we have broken up the S&P 500 into deciles (10 groups of 50 stocks each) based on YTD performance through last Friday. We then calculate the average performance today of the stocks in each decile.

As shown below, the 50 stocks in the S&P that were up the most YTD coming into today were down an average of 1.45% today. Decile two (the next 50 best performers YTD) saw an average decline of 0.72%, while deciles three through five were roughly flat. Once you get to deciles six through ten, though, the average performance today was greater than +1% for each decile! The 50 worst performing S&P 500 stocks of 2019 coming into today were up an average of 3.37% today.

Basically the bottom half of the S&P in terms of YTD performance exploded higher today, while the top half lagged badly. What’s the reason for the big divergence in performance? Find out by reading our Chart of the Day. You can read it with a two-week free trial to Bespoke Premium.

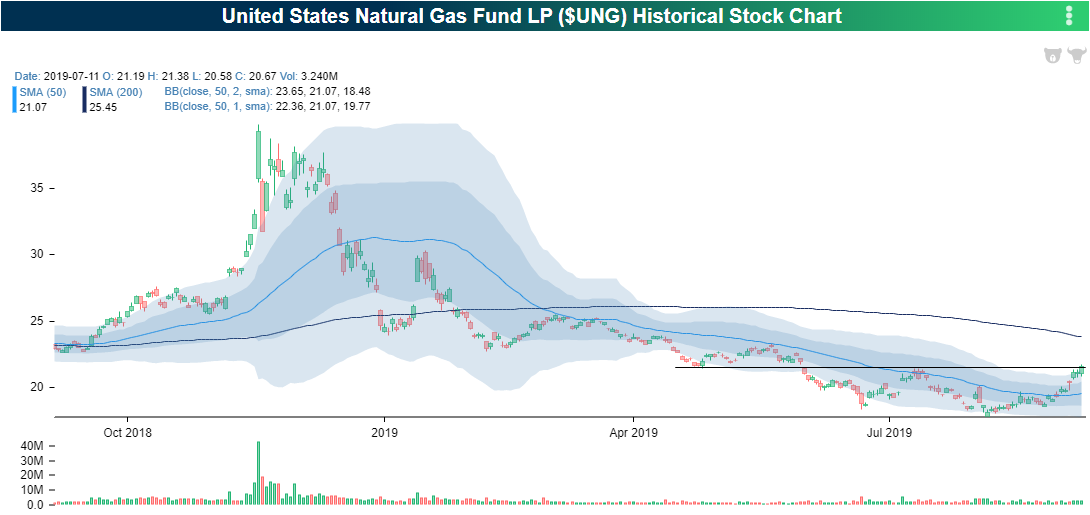

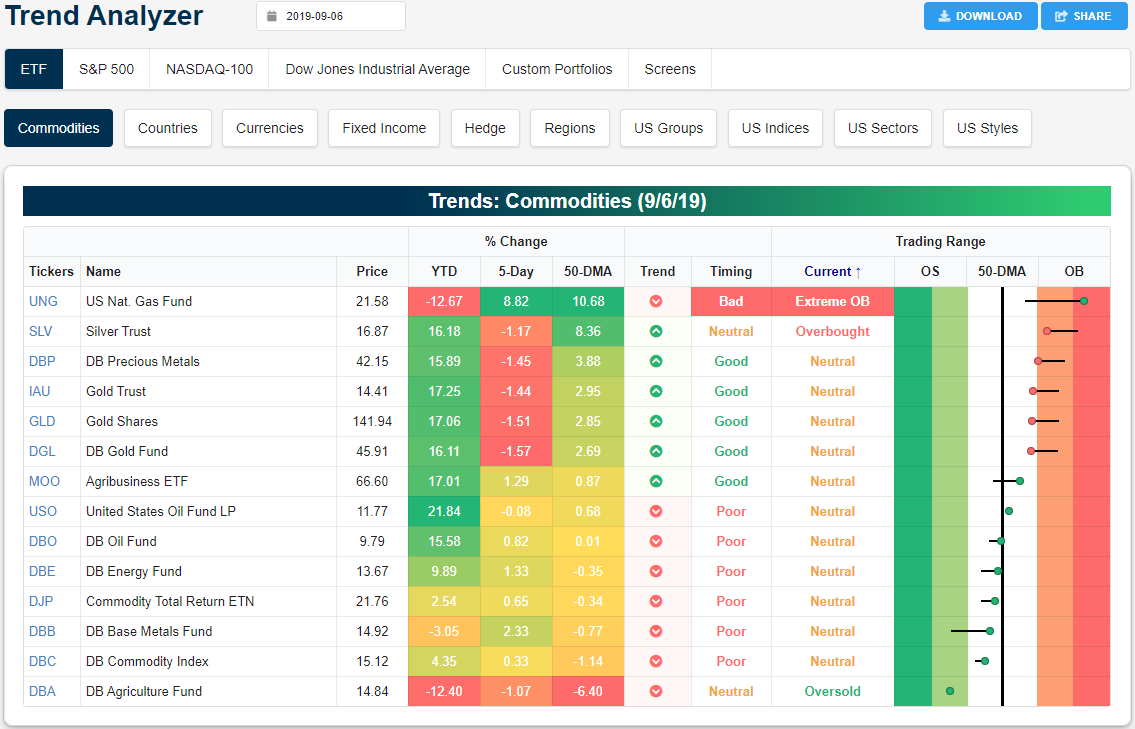

Nat. Gas (UNG) Heating Up

As we noted in Friday’s Bespoke Report, the US Natural Gas Fund (UNG) was the top-performing ETF in our asset class performance matrix last week with a 9.16% gain. That move higher is continuing today as UNG has rallied another 3.5% to its highest level since May after breaking above resistance (which also was previous support) around $21. All of this comes after the ETF made an all-time low on August 5th when it opened at $17.75. Since that open, UNG has surged 25.86%.

Following a volatile spike at the end of last year, UNG collapsed below its 50-DMA. Up until the end of August, this acted as stiff resistance for the commodity, but this most recent leg higher has sent UNG surging through these levels. UNG now sits over 10% above its 50-DMA and is moving deeper and deeper into extremely overbought territory (over 2 standard deviations above its 50-day). As precious metals have begun to experience a bit of mean reversion, UNG has become by far the most overbought commodity ETF in our Trend Analyzer. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Chart of the Day: Growth Massacre

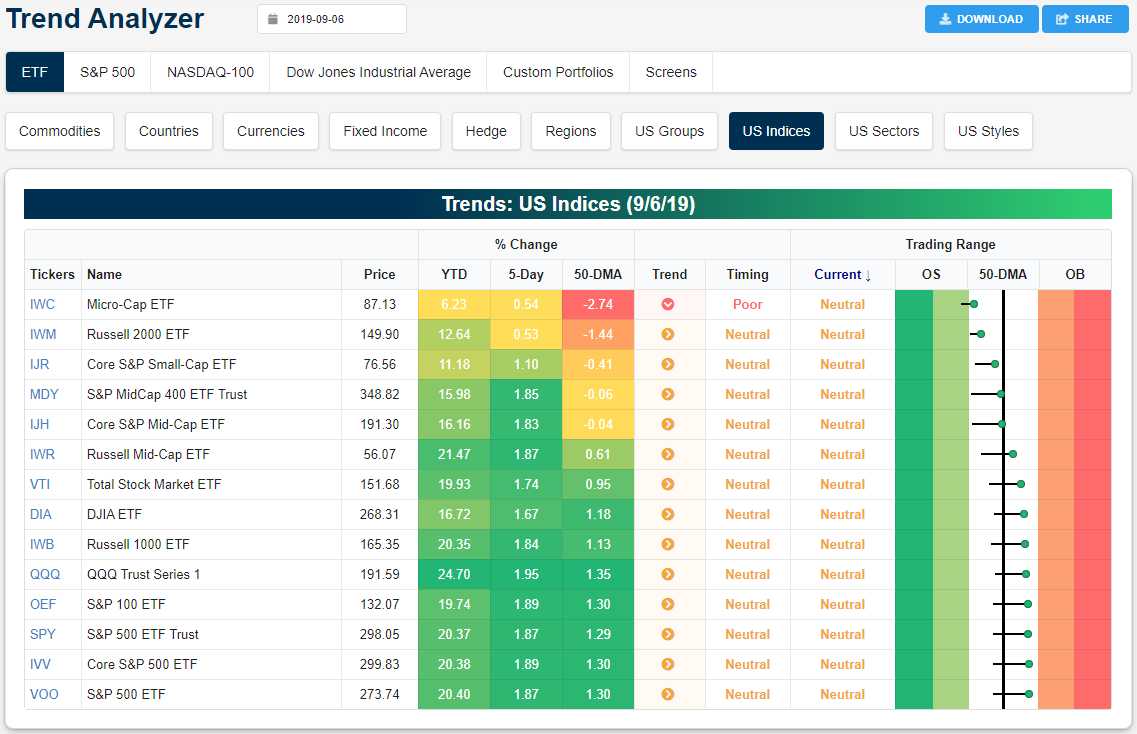

Trend Analyzer – 9/9/19 – Neutral and Sideways

Despite positive price action last week with most major index ETFs (other than small caps) up over 1.5% from five days ago, the longer-term trends have worsened in our Trend Analyzer. Over the past few months, fewer and fewer major index ETFs have held onto their long term uptrends. Headed into Friday, ETFs tracking the S&P 500 (SPY, VOO, IVV) had been the only ones left in uptrends, but today they have joined their peers and are trending sideways. Fortunately, only the Micro-Caps ETF (IWC) is in a downtrend. More near term, each of the major index ETFs has experienced mean reversion over the past couple of weeks as each one has now exited oversold territory. Large caps have also retaken their 50-DMAs and are now approaching overbought territory in the process.

Last week, stocks finally managed to break out of the range that they had been in since the first days of August. Large caps like the Dow (DIA) saw the most distinct breakout above this range in addition to a move back above their 50-DMAs. On the other hand, although mid-caps like the Core S&P Mid-Cap ETF (IJH) and the S&P MidCap400 ETF (MDY) also managed to breakout above the short term downtrends that were established in August and their 50-DMAs, they did not hold above their 50-DMAs on Friday. The small-cap Russell 2000 (IWM) looks more or less the same, but rather than the 50-DMA, IWM failed to hold above its longer term 200-DMA. Start a two-week free trial to Bespoke Institutional to access our interactive Trend Analyzer, Chart Scanner, and much more.

Small Changes, Big Moves

After a relentless downward move for much of August, long-term interest rates have started to stabilize in the last week or so and have even started to show small upward moves. Take the 30-year US Treasury yield, for example. After hitting a low of 1.90% on August 28th, the 30-year yield has moved up to 2.09%.

While a small increase in yields may not seem like a lot, the further out into the future the maturity of that asset is, the bigger the impact the move in interest rates will be on its price. Let’s take an extreme example using the Austrian 100-year bond that was issued in late 2017 and matures in September 2117. As the frenzy for yield has eased since late August, the price of the Austrian 100-year bond has dropped over 15%. That’s a pretty big move given that the interest rate on the bond has only increased 23 basis points! To be fair, it works both ways. When yields were falling, the price of the Austrian 100-year was one of the top-performing assets in the entire financial universe, and even after the recent decline, it is still up 57% YTD. If rates keep rising, those big gains investors have seen in their long-term fixed-income holdings this year will reverse sharply. Start a two-week free trial to Bespoke Institutional to access our unparalleled research and interactive tools.

Bespoke’s Morning Lineup – Keeping Up the Momentum

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

Bespoke Brunch Reads: 9/8/19

Welcome to Bespoke Brunch Reads — a linkfest of the favorite things we read over the past week. The links are mostly market related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

While you’re here, join Bespoke Premium for 3 months for just $95 with our 2019 Annual Outlook special offer.

Indexing

The Big Short’s Michael Burry Explains Why Index Funds Are Like Subprime CDOs by Reed Stevenson (Bloomberg)

One of the most well-known benefactors of housing short trades sees index funds as the next big problem for markets, citing liquidity mismatches and structuring as the key problems for investors. [Link; soft paywall, auto-playing video]

Debunking the Silly “Passive is a Bubble” Myth by Ben Carlson (A Wealth Of Common Sense)

The prior story about indexing gets a forensic treatment from Carlson, who does a great job pointing out the absurd hyperbole surrounding index funds. [Link]

Tech

The Time Netflix Considered Selling Itself to Amazon for Peanuts by Marc Randolph (WSJ)

Back in 1998, the now-giant streaming service was on the ropes as an order-by-mail DVD rental business, and it briefly considered a sale of its business to the nascent Amazon empire. [Link; paywall]

Waze Hijacked L.A. in the Name of Convenience. Can Anyone Put the Genie Back in the Bottle? by Jonathan Littman (LA Mag)

How the traffic app started off giving Los Angelenos a god-like power over their commute, but has since led to dead-ends by snarling streets with traffic and prompting pushback from the neighborhoods turned throughfares that Waze pushes traffic through. [Link]

Investing

Quality Stocks Are an Overcrowded Trade by John Authers (Bloomberg)

Stocks which have attributes broadly grouped into the basket of “quality” have been outperforming, but are their gains sustainable? [Link; soft paywall]

The Collector: 1977 WSJ Article on Buffett Strikes Familiar Themes (The Rational Walk)

A blast from the past with quotes from Warren Buffett much earlier in his career, offering a remarkable degree of consistency in his views about companies over the years. [Link]

Tech Dystopia

A Breakthrough for A.I. Technology: Passing an 8th-Grade Science Test by Cade Metz (NYT)

In Seattle, a lab has developed an AI capable of scoring 90% on an 8th-grade math test and more than 80% on a 12th-grade exam; that’s a remarkable breakthrough in natural language processing that clobbers efforts made by hundreds of teams as recently as four years ago. [Link; soft paywall]

Fraudsters Used AI to Mimic CEO’s Voice in Unusual Cybercrime Case by Catherine Stupp (WSJ)

Using software that allowed them to duplicate a CEO’s voice, scammers were able to direct one of his subordinates to transfer a six figure payment to a fictitious supplier. [Link; paywall]

Higher Ed

All the Greedy Young Abigail Fishers and Me by Jia Tolentino (Jezebel)

A fascinating look at the industry of tutors who work to get their higher income peers into high status colleges with that perfect essay or personal statement. [Link]

Food

Meet The Man Who Guards America’s Ketchup by Dan Charles (WFAE)

Assuring a consistent taste and quality in America’s ketchup supply is an important job, and it falls to a man Kraft Heinz refers to as their “Ketchup Master”. [Link]

Real Estate

The ridiculous reasons rich New Yorkers no longer buy penthouses by Christopher Cameron (NY Post)

With super-thin buildings pushing dozens upon dozens of stories high, the ultra-lux penthouse is no longer as attractive to buyers who don’t like the excessive height of the tallest floors. [Link]

Read Bespoke’s most actionable market research by joining Bespoke Premium today! Get started here.

Have a great weekend!

The Bespoke Report — 9/6/19

This week’s Bespoke Report newsletter is now available for members.

In this week’s newsletter, we highlight the S&P 500’s breakout above a key resistance level this week and try to identify if the rally has any staying power. We provide a run-down of major economic releases and what they mean for global financial markets, and we also take a look at the recent action in mega-cap stocks at the top of the food chain. To read the Bespoke Report and access everything else Bespoke’s research platform has to offer, start a two-week free trial to one of our three membership levels. You won’t be disappointed!