Bespoke’s Global Macro Dashboard — 9/11/19

Bespoke’s Global Macro Dashboard is a high-level summary of 22 major economies from around the world. For each country, we provide charts of local equity market prices, relative performance versus global equities, price to earnings ratios, dividend yields, economic growth, unemployment, retail sales and industrial production growth, inflation, money supply, spot FX performance versus the dollar, policy rate, and ten year local government bond yield interest rates. The report is intended as a tool for both reference and idea generation. It’s clients’ first stop for basic background info on how a given economy is performing, and what issues are driving the narrative for that economy. The dashboard helps you get up to speed on and keep track of the basics for the most important economies around the world, informing starting points for further research and risk management. It’s published weekly every Wednesday at the Bespoke Institutional membership level.

You can access our Global Macro Dashboard by starting a 14-day free trial to Bespoke Institutional now!

The Closer – Markets Lacking Access, Retail REITs, ASEC Analysis, JOLTs Jaunt – 9/10/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, further demonstrating the mean reversion trades observed across markets this week, we begin tonight’s Closer with a bit of a case study of MarketAxess (MKTX). We then take a look at the consistent selling of bonds and the outperformance of retail-focused REITs. Turning over to economic data, we recap today’s weaker JOLTS report followed by an in depth look at the Census’ Annual Social and Economic supplementary data on income, poverty, and health care.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

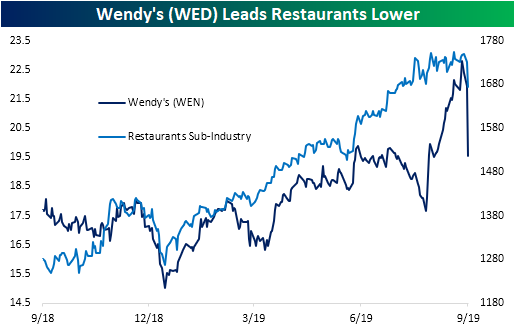

Fast Food For Finer Dining

The hype may not be over a chicken sandwich, but Wendy’s (WEN) is the latest fast-food company to make headlines after announcing a new breakfast menu. Unlike the well-received all-day McDonald’s (MCD) breakfast from a few years ago, Wendy’s announcement has been met with a frosty reaction from investors. WEN is down over 10% today, which has also dragged on the Restaurants group.

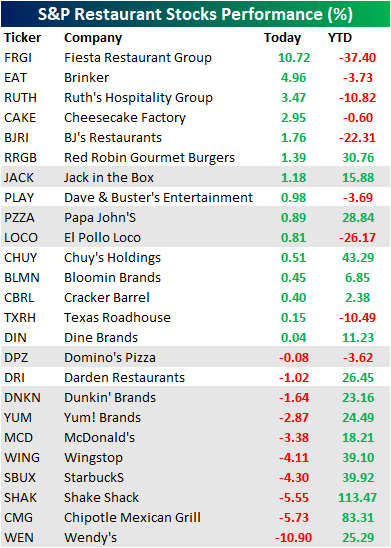

This week we’ve seen massive rotation out of this year’s winners and into the year’s losers. The trend is very apparent in the Restaurant space as we show in the table below. Fast-food stocks like Wendy’s (WEN), Shake Shack (SHAK), Chipotle (CMG), Starbuck’s (SBUX), and McDonald’s (MCD) are up huge year-to-date, but they’re getting crushed today. On the flip side, stocks like Fiesta (FRGI), Brinker (EAT), Ruth’s (RUTH), and BJ’s (BJRI) that have been beaten down YTD are up big on the day. Start a two-week free trial to one of Bespoke’s three premium membership levels.

Chart of the Day: Narrow Ranges

Bespoke Stock Scores — 9/10/19

Bespoke CNBC Appearances (9/10 and 9/6)

Below are links to two recent CNBC segments with Bespoke co-founder Paul Hickey. To view the segments, click on the links below.

Trading Nation – 9/6/19 – Special Chart Suggest the Market is Starting a Hot Streak

S&P 500 Breakout Stocks

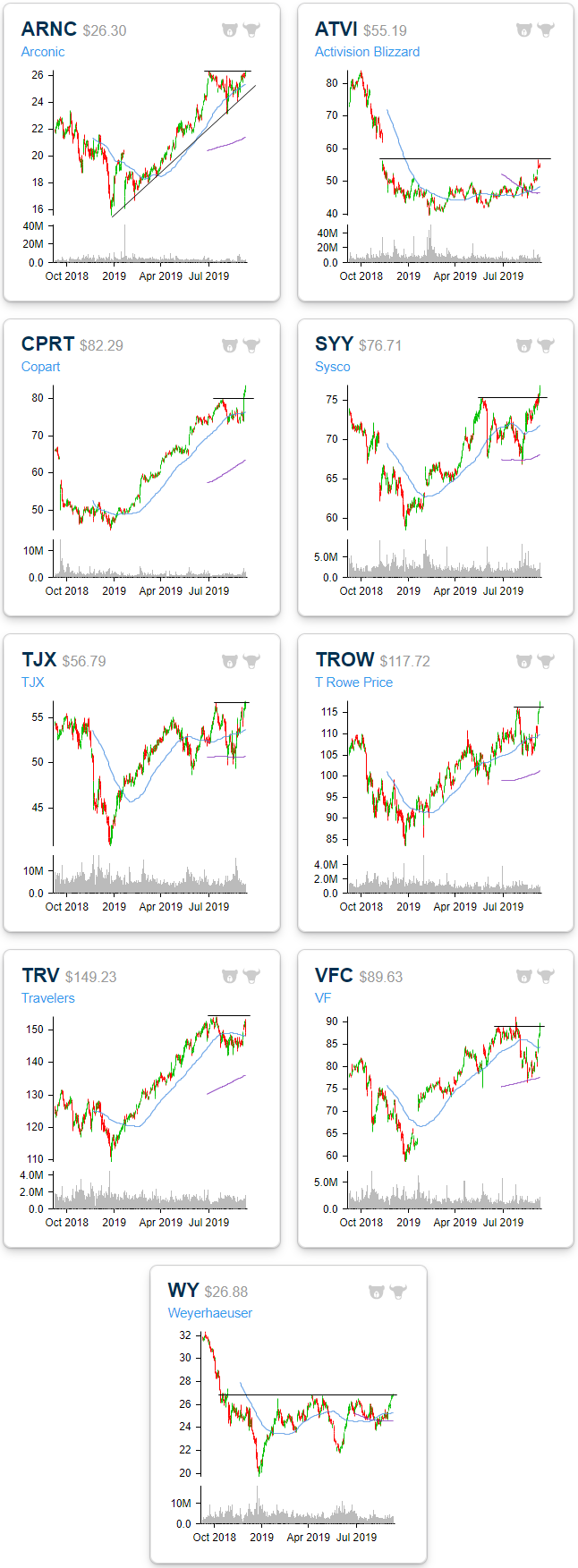

As we have previously noted, some of the stocks that have been the most beaten down this year have been experiencing distinct outperformance recently. While not necessarily the worst YTD performers in the index, below are a handful of charts taken from our Chart Scanner tool that have recently broken above the top of their downtrend channels. This does not necessarily mean that these stocks are looking to completely take a 180 in regards to their long term trends, but at least in the short term, they are showing promise. Notably, as it has been the top performing sector yesterday and today, multiple of these stocks are energy plays.

It is not just the stocks that are in downtrends that are showing signs of a breakout. Below are some more stocks that have been in healthy uptrends over the past year or have at least been sideways such as Activision Blizzard (ATVI) and Weyerhauser (WY). For ATVI and WY, both stocks have been in a range for most of the past year. More recently, these two have begun making higher lows and are now at the upper end of these ranges. For ATVI, it’s now looking to fill the large gap from earnings around one year ago. Similarly, Arconic (ARNC), Copart (CPRT), Sysco (SYY), TJX (TJX), T Rowe Price (TROW), and VF Corp (VFC) have all run up to resistance at prior highs, the only difference being these moves are in the context of long term uptrends. In the case of some like CPRT and SYY, the break out is already occurring while others like ARNC and TJX need a bit more work from the bulls. Start a two-week free trial to Bespoke Premium to access our interactive Chart Scanner and much more.

Small Business Sentiment — “Pessimism is Contagious”

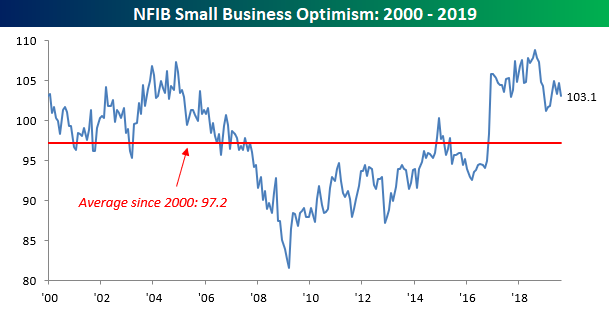

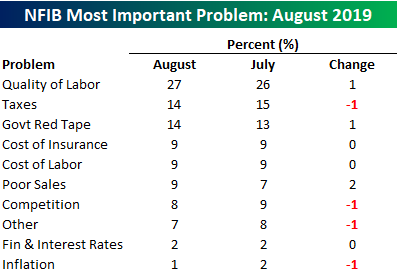

Sentiment on the part of small business owners declined in August and based on the steep drop in interest rates and escalation of the trade war with China, you can’t really blame business owners for becoming more cautious. Overall, the main index of sentiment dropped from 104.7 down to 103.1, which was 0.4 points lower than the 103.5 consensus expectation. In the commentary of the report, the NFIB noted that “in terms of real economic activity, August was a very good month,” and went on to say that “the decline in the index was driven by weakened expectations for the future.” One line that stood out from this month’s report was the statement that “Pessimism is contagious, even when the real economy is doing well, expectations can be infected and turn sour. Those rooting for a recession are having a psychological impact in spite of a strong Main Street economy.” While the statement isn’t entirely inaccurate, we would note that the escalation of tariffs and rhetoric from the President certainly hasn’t helped either.

Looking at the chart below, it has now been a full year since the NFIB Small Business Index made its peak for the cycle. While it isn’t far from that level now, it has shown signs of rolling over in the last few months. If the lows from January are breached, depending on your political perspective, that would suggest that either it’s more than just news headlines driving down sentiment or that the headlines actually won out.

In terms of the biggest problems facing small business owners, Labor Quality remains at the top of the list, rising from 26% to 27%. Behind Labor Quality, Taxes and Red Tape are tied for second at 14% each. It wasn’t that long ago that these two problems topped the list and together totaled over 40%. Today, on a combined basis the two would barely top Labor Quality as the biggest problem. In last week’s ISM reports, we noted that the ISM Commodities surveys were increasingly showing fewer and fewer commodities rising in price. Today, that sentiment of benign inflation was further illustrated by the fact that only 1% of small business owners see Inflation as their most important problem.

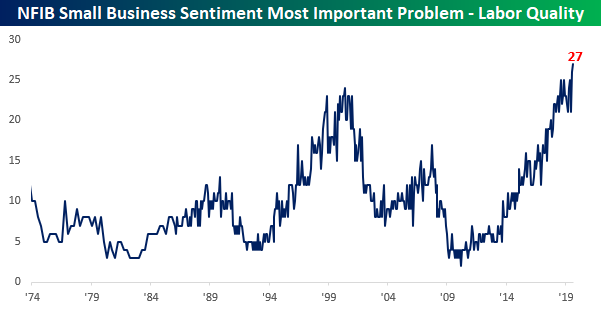

As mentioned above, Labor Quality remains the most important problem for small business owners these days, and in the entire history of the survey, it has never been a bigger problem. At 27%, the level is now comfortably above the 24% peak reached in 2000. While it only seems logical that labor costs would rise as Labor Quality becomes a bigger problem, to this point we have yet to see that play out as only 9% of small business owners noted wage costs as their most important problem. Start a two-week free trial to Bespoke Institutional to access our unparalleled research and interactive tools.

Momentum Massacre

Yesterday saw a nearly unprecedented collapse for stocks with high price momentum relative to stocks with value characteristics. These two baskets of stocks are most easily tracked using the iShares Momentum (MTUM) and Value (VLUE) factor ETFs.

Momentum stocks are those that have been going up; momentum refers to the upward trajectory of price. Value stocks are generally low multiple, and often have the opposite price attributes of momentum stocks. As shown in the chart below, yesterday was an absolutely catastrophic day for Momentum (MTUM) relative to Value (VLUE). Part of this was a function of rates, with recent upticks in short and long term interest rates driving utilities and other defensive stocks with strong trailing momentum lower, while banks rallied. But it was broader than that too: software got smashed while oil & gas stocks surged, automakers ripped while stable consumer staples names took a hit, and the market generally reversed all of the trends it has been operating on so far this year in a massive stop-out of successful (up to now) trading strategies. Start a two-week free trial to Bespoke Institutional to see more details on the blow up of growth-oriented momentum stocks versus value stocks in reports published yesterday.

Bespoke’s Morning Lineup – Quiet Tuesday

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.