ROKU Takes the Stairs Up and the Elevator Down

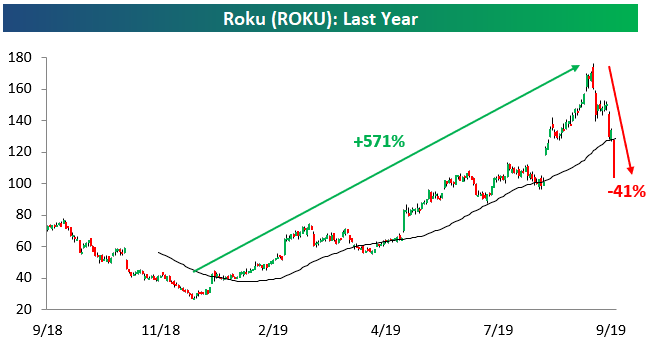

The streaming media device manufacturer Roku (ROKU) has had quite the move lately. As shown in the chart below, ROKU took the stairs up from late 2018 through early September, and it has taken the elevator down ever since. Just 11 days ago on September 9th, ROKU hit an intraday high of $176.55. At that point, the stock was up 70% since the start of August, +476% since the start of 2019, and +571% since its intraday low in Q4 2018.

Since its high on September 9th, ROKU has lost 41% of its value, and it’s down 20% today alone after Pivotal Research Group slapped a $60 price target on the stock this morning. Analyst price targets don’t normally cause 20% drops, but ROKU is a prime example of the unwind we’ve seen for a lot of high-growth, high-valuation momentum stocks that have taken it on the chin this month. Yesterday, ROKU managed to hold support right at its 50-day moving average, but today that support has completely broken down, and there are seemingly no bids in sight. Traders will now be looking for support at $100, and if that doesn’t hold, $80 is the next level. Start a two-week free trial to Bespoke Institutional to access all of our market research and interactive tools.

Bespoke’s S&P 500 Sector Weightings Report — September 2019

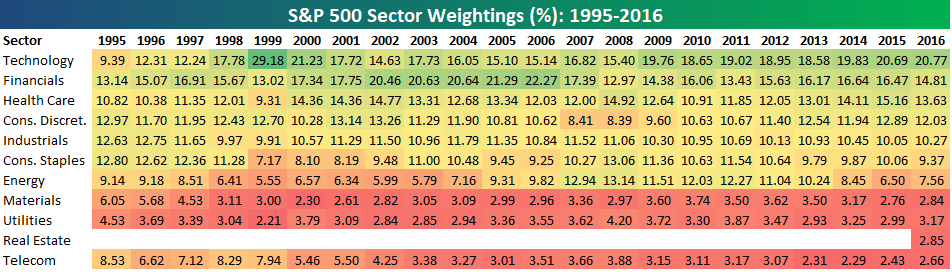

S&P 500 sector weightings are important to monitor. Over the years when weightings have gotten extremely lopsided for one or two sectors, it hasn’t ended well. Below is a table showing S&P 500 sector weightings from the mid-1990s through 2016. In the early 1990s before the Dot Com bubble, the US economy was much more evenly weighted between manufacturing sectors and service sectors. Sector weightings were bunched together between 6% and 14% across the board. In 1990, Tech was tied for the smallest sector of the market at 6.3%, while Industrials was the largest at 14.7%. The spread between the largest and smallest sectors back then was just over 8 percentage points.

The Dot Com bubble completely blew up the balanced economy, and looking back you can clearly see how lopsided things had become. Once the Tech bubble burst, it was the Financial sector that began its charge towards dominance. The Financial sector’s sole purpose is to service the economy, so in our view you never want to see the Financial sector make up the largest portion of the economy. That was the case from 2002 to 2007, though, and we all know how that ended.

Unfortunately we’ve begun to see sector weightings get extremely out of whack once again.

If you would like to see the most up-to-date numbers for S&P 500 sector weightings, simply start a two-week free trial to our Bespoke Premium or Bespoke Institutional services. Click back to this post to see the numbers once you’re signed up!

India’s SENSEX Has Biggest One-Day Gain Since May 2009

Overnight, India’s SENSEX benchmark recorded a 6.6 standard deviation move (versus the 2 year distribution of changes). The index’s 5.3% gain was its biggest one-day rally since May 2009.

Behind the move was a new set of stimulus policies from India’s government. The Finance Minister announced a corporate income tax cut from 30% to 22%, with additional levies bringing the total effective corporate income tax rate to 25.2%. Newly-formed companies will pay even less, 15% (17% effective), which is as low as a jurisdiction like Singapore. Notably, this tax cut is in large part retroactive to April of 2019, which has dubious economic value but is rocket fuel for the index. Banks and other financials led the charge on the index with other cyclicals like Tata Steel, Tata Motors, and Maruti Suzuki also surging.

As shown below, the 5%+ gain for the SENSEX came at a time when the index was further breaking down within a multi-month downtrend. Instead of being oversold at new lows and well below its 50-day and 200-day moving averages, the SENSEX heads into the weekend in overbought territory and back above its major moving averages. When surprise fiscal policy moves hit the tape, you can throw technicals out the window! Start a two-week free trial to Bespoke Institutional to stay up-to-date on all the latest developments in global financial markets and economics.

Bespoke’s Morning Lineup — 9/20/19

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week free trial to Bespoke Premium. CLICK HERE to learn more and start your free trial.

The Closer – Stocks At Resistance, Thursday Data Deluge – 9/19/19

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight on markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin by evaluating the resistance that both US and European stocks find themselves at. We also show what the credit market is suggesting the next move may be. Next, we review today’s large slate of economic data including the Leading and Coincident indices, first of the September inputs of our Five Fed Manufacturing Composite, Existing Home Sales, and Current Account balance.

See today’s post-market Closer and everything else Bespoke publishes by starting a 14-day free trial to Bespoke Institutional today!

Bespoke’s Sector Snapshot — 9/19/19

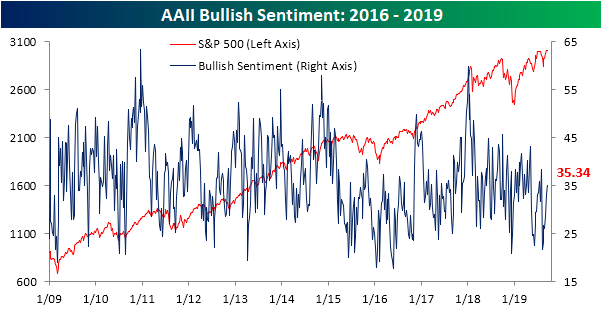

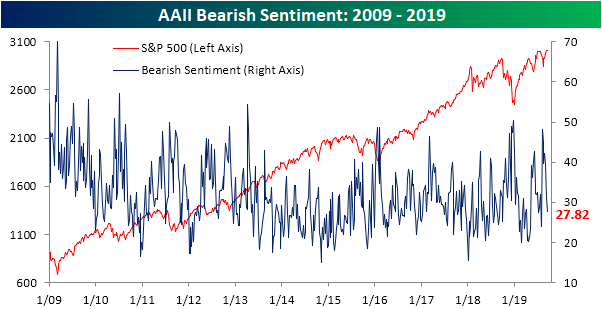

Bears Back Off

As the S&P 500 has come within half a percent of its all-time highs today, sentiment has continued to lean more positive. AAII’s weekly investor sentiment survey for the past week showed 35.34% of respondents reporting as bullish. That is up from 33.13% last week and is the third straight week with an increase. Despite these consistent increases in the past month, bullish sentiment is still below its historical average of 38.11% as it has been for the past seven and 18 of the last 19 weeks. If the S&P 500 manages to take out previous highs, it would be reasonable to expect bullish sentiment to make a larger move higher.

The biggest move in sentiment this week was actually in bearish sentiment. In the past month, bearish sentiment has fallen considerably. In fact, the 14.39 percentage point drop over the past four weeks is the largest such move since January 10th when negative sentiment was working off even higher levels in the wake of the Q4 2018 downturn. Now at 27.82%, bearish sentiment is back below its historical average for the first time since August 1st.

Still, the largest percentage of investors don’t know what to make of the market as neutral sentiment checked in at 36.84% which represents a 1.2 percentage point increase from the prior week. Granted, relative to its historical average, neutral sentiment is still elevated as it has been for most of this year. In fact, 32 of the 37 total weeks so far this year have seen above-average neutral sentiment readings. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.

Chart of the Day: Delving Into Diode (DIOD)

Dividend Stock Spotlight: Target (TGT)

Earlier today, Target (TGT) announced that its board approved a new $5 billion buyback program which is expected to begin in 2020. In addition to the buybacks, which are equivalent to over 9% of the company’s market cap, TGT also declared its quarterly dividend of $0.66 per share. While the stock is down today, after a big beat in its last earnings report in August, TGT skyrocketed over 20% with further gains in the following days. Although it has pulled back a bit recently, the stock remains elevated, but also still yields 2.47%. That yield is larger than the 2.07% average for other S&P 500 retailers and the broader S&P 500 which yields only 1 bp less than retail.

TGT has also consistently raised its dividend each year going all the way back to 1980. In the past five years alone, the dividend has grown over 7%. While that is a somewhat slower pace than the average for S&P 500 retailers in that time (11.27%), Target’s dividend payout ratio is also low meaning that the company has room to not only keep paying out this dividend but also to raise it further. Taking into account the buyback program and recent strong quarter only adds to the case that the company has the ability to increase the dividend in the future. Additionally, looking at the company’s valuation, it also has a lower price-to-earnings, price-to-book, and EV/EBITDA than comparable companies in its group. Again, that is even though price has seen a massive run higher in the past month. Start a two-week free trial to Bespoke Premium for Bespoke’s most actionable equity market ideas.

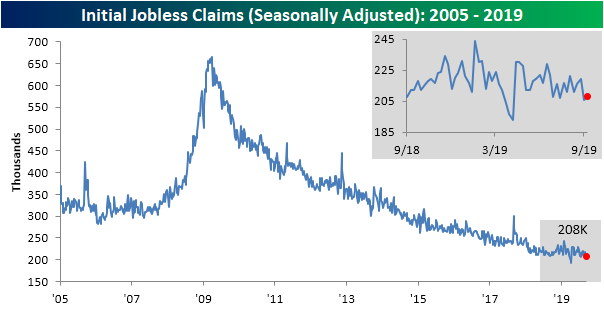

Claims Still Low

Last week, seasonally adjusted jobless claims saw a large move back below the past several months’ range when the headline reading fell to 204K. This was the lowest print since April when it was at a 50 year low. This week, although still near the lows of the past few months, there was a small uptick to 208K on top of an upward revision of last week’s print (revised to 206K). Despite this increase, this week’s data was still better than expectations as forecasts were calling for a much larger increase to 213K. Also on the bright side, claims have now been at or below 250K and 300K for record streaks of 102 and 237 consecutive weeks, respectively.

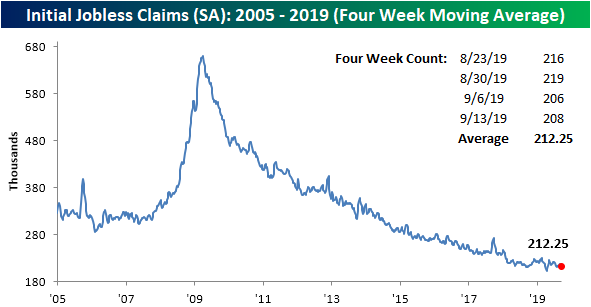

Despite last week’s revision and this week’s higher claims number, the four-week moving average actually ticked down to 212.25K. But it was a tiny decrease of just 0.75K from last week which brings the average to its lowest level since the final week of July when it was at 212K. Given these small fluctuations, the average continues to show minimal improvements as it has been flat in the past year.

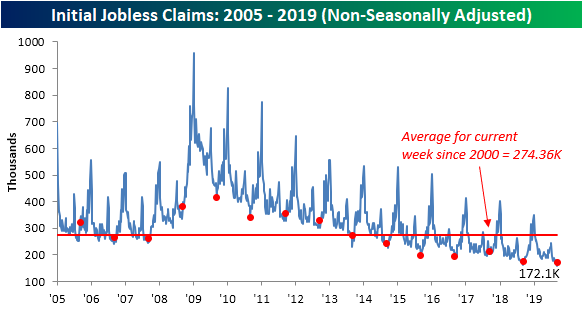

Last week, non-seasonally claims came in at their lowest level since the 1960’s. This week, claims rose from that 160.3K reading up to 172.1K. As a result of seasonal factors, last week likely marked this year’s low for NSA claims. It can be taken as a positive sign, though, that this week’s reading of 172.1K, although higher week-over-week, was down versus the same week last year.

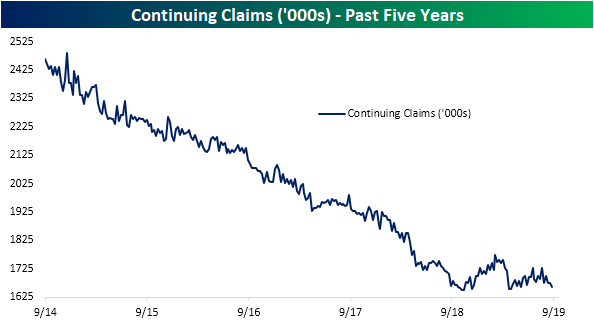

In addition to initial jobless claims showing improvements over the past couple of weeks, so has continuing claims. Falling to 1661K this week, continuing claims are at their lowest levels since April. Much like seasonally adjusted initial jobless claims, continuing claims have finally begun to grind lower after remaining relatively flat, if not sloping upwards, over the past year. Start a two-week free trial to Bespoke Institutional to access our interactive economic indicators monitor and much more.