Chart of the Day – The Worst Time of the Year

Bespoke’s Morning Lineup – 7/8/25 – Subdued

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If your only goal is to become rich, you will never achieve it.” – John D. Rockefeller

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Subdued is the tone once again this morning as equity futures are little changed on either side of the unchanged line. Nasdaq futures are showing the biggest move with a gain of 0.25%. Crude oil is fractionally lower, just below $68 per barrel, while the 10-year yield is up 2 bp,s taking the yield back above 4.4%. Gold is slightly lower, while Bitcoin and Ethereum both are trading up about 1%.

In Asia overnight, most major indices were little changed, except for China, which was up 0.70% while Hong Kong’s Hang Seng was up just over 1%. The modest gains came even as President Trump sent letters to many countries in the region, including Japan and South Korea, informing them that their exports to the US would face tariffs of at least 25%.

European stocks are little changed in the early going this morning, with the STOXX 600 up 0.10% while Germany and the UK are up fractionally, while France is lower. The EU was one region of the world not to receive a letter on tariffs, and that has raised hopes that a deal with the bloc could be near. Reports this morning suggest that the base rate will be 10% with some exceptions for aircraft and parts, medical equipment, and spirits.

Today in the US, it’s another quiet day on the calendar. NFIB Small Business Optimism came in right in line with expectations at 98.6, which was down very slightly from last month’s reading of 98.8. The only other report on the calendar is the New York Fed’s Survey of Consumer Expectations, where 1-year inflation expectations are expected to come in at 3.2%.

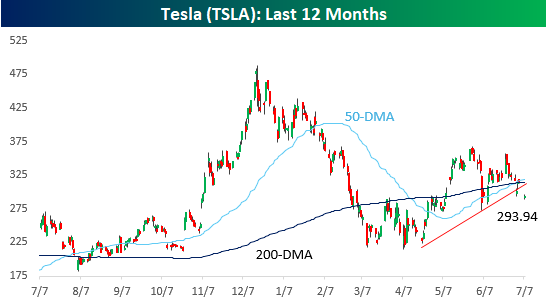

With Elon Musk announcing the creation of the America Party over the weekend and the potential of a third party to hurt Republican majorities in the mid-term elections, investors headed into the new week with concerns that potential retribution from President Trump would hurt Tesla’s business. In response, the stock opened down over 6% yesterday and basically stayed there, finishing the day with a decline of nearly 7%.

Yesterday’s decline broke TSLA’s uptrend off the April lows, and that came after making a lower high in late June. All this came after the stock made a golden cross (50-day moving average cross above the 200-day moving average as both are rising) last week, which technicians consider a positive technical formation. Fitting for a stock like TSLA, the stock’s trading pattern has been sending mixed signals.

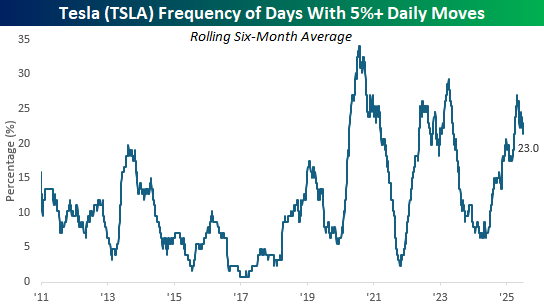

Normally, as companies become larger in terms of market cap, their share prices become less volatile, but that’s not the case with TSLA. Yesterday was the 29th daily gain or loss of 5%+ in TSLA over the last six months, which works out to 23% of all trading days. While the company went public in 2010, it wasn’t until 2020 that TSLA routinely started to see 5%+ daily moves on 20% or more of trading days over a rolling six-month period.

The Closer – Tariff Rate Tips Towards 10% – 7/7/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a checkup on where the effective tariff rate is sitting based on today’s announcement (page 1). We also provide a chart checkup of the S&P 500 at market cap and equal weight, the dollar, and the long bond (pages 2 and 3). We then finish with a look into the latest positioning data (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Chart of the Day: Tariff Talk at Overbought

Bespoke’s Matrix of Economic Indicators

Our Matrix of Economic Indicators provides a concise summary analysis of the US economy’s momentum. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!

![]()

Bespoke’s Morning Lineup – 7/7/25 – Easing Back into Things

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“History is a guide to navigation in perilous times. History is who we are and why we are the way we are.” – David McCullough

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Investors are being eased back into the market this morning, with futures showing modest losses after a more significant decline overnight. The market may be open, but with no economic or earnings reports on the calendar, things are relatively quiet to kick off the new week. That’s generally the case for the rest of the week too, with very few reports on the calendar in the next four trading days. That will leave plenty of time for investors to focus on trade, and Treasury Secretary Scott Bessent says to expect several announcements in the next two days, and for those that don’t make a deal by August 1st, tariffs on their exports to the US will go back to the levels announced on April 2nd

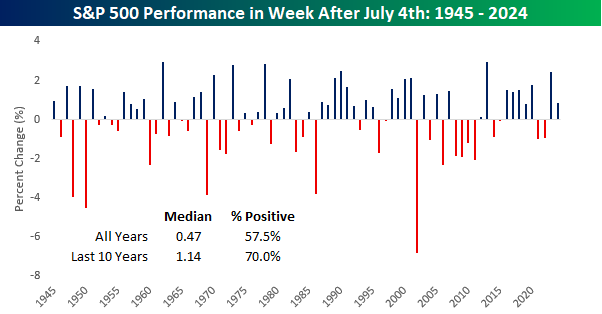

The long holiday weekend is over, and it’s time for investors to get back to business as Q2 earnings season is right around the corner, and the tariff situation is likely to become more concrete. One thing bulls have going for them heading into this week is the seasonal calendar. Since WWII, the S&P 500’s median performance during the week after the July 4th holiday week has been a gain of 0.47% with positive returns 57.5% of the time. More recently, performance has been even stronger with a median gain of 1.14% and positive returns 70% of the time.

Brunch Reads – 7/6/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

Life Is Like a Box of Chocolates: When Forrest Gump opened in theaters on July 6, 1994, no one could’ve predicted that a slow-talking Alabama man with a fondness for running would end up reshaping American pop culture. The film debuted in the middle of a blockbuster summer. The Lion King had just roared into theaters a few weeks earlier, and True Lies was waiting in the wings, but Forrest Gump carved out its own space, powered by word of mouth, critical praise, and a once-in-a-generation performance by Tom Hanks.

Audiences walked in expecting a feel-good story and left trying to unpack everything they’d just seen: Vietnam, civil rights protests, Watergate, shrimp boats, ping-pong diplomacy, and a feather that somehow made it all make sense. It struck a nerve. People laughed, cried, and immediately started quoting lines that would live on to this day: “Life is like a box of chocolates,” “Run, Forrest, run,” and even “Stupid is as stupid does.”

Forrest Gump grossed over $24 million in its opening weekend and continued to play for months. It would go on to win six Oscars, including Best Picture and Best Actor for Hanks, but on that first day, it was just another title on the marquee.

AI & Technology

Microsoft Says Its New AI System Diagnosed Patients 4 Times More Accurately Than Human Doctors (WIRED)

Microsoft built an AI system that outperformed human doctors in diagnosing complex medical cases, achieving 80% accuracy compared to their 20%, while also recommending more cost-effective tests. It works by orchestrating a group of top AI models to mimic how a panel of physicians would reason through a diagnosis, step-by-step. Experts caution that real-world clinical trials will be the true test, and that doctors in the study weren’t allowed to use any digital tools, which might’ve tilted the comparison. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

The Closer – Jobs and Wages, Claims Demographics – 7/3/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, in a recap of a busy day of economic data, we lead off with a rundown of the June payrolls report (page 1) including an update on wages (page 2). We also check in on ISM Service data and the market’s reaction to today’s releases (page 3). We close out with a look into demographic readings for jobless claims (pages 4 and 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Morning Lineup – 7/3/25 – Beating the Odds

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Governments are instituted among Men, deriving their just powers from the consent of the governed.” – Declaration of Independence

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Happy Fourth! In an outcome that most would not have predicted over the last several days and weeks, the House is likely to pass the Reconciliation Bill ahead of the July 4th holiday. Just yesterday, the odds of passage by that date were less than 50%, but the bill cleared a procedural vote overnight, and Polymarket now has the odds of passage at 91%. Whatever side of the aisle you position yourself, the ability of Speaker Johnson to pass legislation over the last six months with such a slim majority has been impressive.

That’s the biggest news event of the market day so far, but there’s a jam-packed economic calendar this morning that includes Jobless Claims, Non-Farm Payrolls, Factory Orders, and ISM Services. Besides being a busy day for data, it’s also a short session as the equity market closes at 1 PM ahead of the holiday, and the bond market closes at 2 PM.

Despite the big political news and the busy day of data ahead, futures are eerily quiet as the S&P 500, Nasdaq, and Dow are all indicated to open less than 0.10% higher. Crude oil is marginally lower, gold is unchanged, and treasury yields are lower. That last point is notable; for all the talk about how the Reconciliation Bill will be a budget buster and blow out the deficit, the 10-year yield has been going down as passage of the bill has become more likely. From a longer-term perspective, too, the 10-year yield is the same now as it was on Election Day.

Heading into the July 4th holiday, the fireworks of the second quarter have put eight of the eleven sectors into overbought territory. Over the last five sessions, every sector has traded higher, and Utilities (XLU) is the only sector ETF with a gain of less than 1%. Leading the way to the upside, Materials (XLB) have rallied over 5% pushing the sector into extreme overbought territory and a gain of nearly 9% YTD.

The Closer – Gilts, Autos, Health Care Checkup – 7/2/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin by looking at how UK Gilts are digesting the country’s fiscal concerns (page 1). We then check in on Tesla (TSLA) deliveries and collapse in shares of Centene (CNC) (page 2). We continue with a checkup on other Health Care stocks and the industry’s labor figures (page 3). We then finish with a review of brand level breakdowns of vehicle sales (page 4) and remittance data from Mexico (page 5).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!