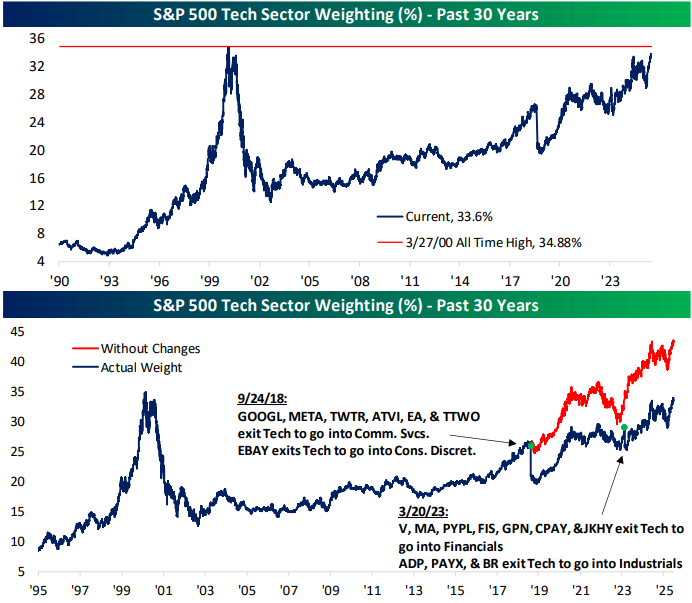

Tech Sector Now 1/3rd of S&P

Amid the AI Boom, the Technology sector’s weighting in the S&P 500 has now eclipsed 1/3rd of the index. As shown in the first chart below, the only time the sector’s weighting has been higher was during a brief window in early 2000 at the peak of the Dot Com bubble.

But the first chart only tells part of the story. Back in 2018, those in charge of sector classifications reorganized many stocks in the S&P. Already-big stocks like Alphabet (GOOGL) and Meta (META) — Facebook at the time — were shifted out of the Technology sector and into the newly classified Communication Services sector. This resulted in a big drop in the Tech sector’s weighting in September 2018 that you can see quite clearly in the chart.

In the second chart below, we’ve included a red line that shows where the Technology sector’s weighting would be right now if the pre-2018 sector classifications were still in effect. Tech would have a weighting in the S&P 500 of roughly 43% right now rather than 33.6% if pre-2018 classifications were in place. 43%!

While its sky-high weighting could be a warning sign, Tech remains the driving force for the US stock market, while every other sector plays second fiddle.

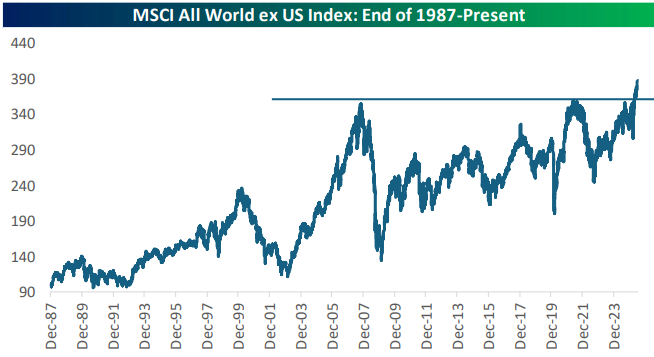

“Rest of World” Equities Finally Break Out

The plight of international equities for the last twenty years is well known to most investors, but in the last month or so, we’ve finally seen them break out to new all-time highs above two key resistance levels. Below is a chart of the MSCI All World ex US index, which basically tracks international equities as a whole. After a massive move higher in the first half of the 2000s, the Financial Crisis did a number on international stocks, and by the time COVID rolled around in early 2020, they had just barely gotten back to their pre-Financial Crisis highs. International equities recovered from the COVID Crash much more slowly than the US, and it has taken until this year for them to finally break out again. Are we now finally set for another big leg higher in international equities as the US works to make new trade deals with both friends and foes?

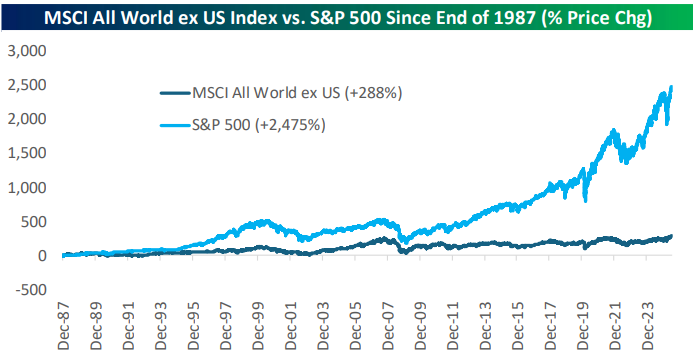

The massive underperformance of international equities versus the US can been seen in the chart below. Since the end of 1987, the US has beaten international equities by nearly 9x, with the S&P 500 gaining nearly 2,500% compared to a gain of 288% for the MSCI World ex US.

Bespoke’s Morning Lineup – 7/28/25 – Data From All Directions

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“I want to live my life, not record it.” – Jacqueline Kennedy Onassis

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

We hope you had a restful weekend, because the last four days of July and the first trading day of August are going to be jam-packed with earnings and economic data. Among the hundreds of companies reporting earnings this week, Meta (META) and Microsoft (MSFT) will report on Wednesday, followed by Amazon.com (AMZN) and Apple (AAPL) on Thursday. Regarding economic data, besides the Non-Farm Payrolls report on Friday, we’ll also receive the ISM Manufacturing report on the same day, along with the Michigan Sentiment. However, these reports will be followed by Consumer Confidence on Tuesday, ADP, GDP, and PCE on Wednesday, and jobless claims on Thursday. Don’t forget that there’s also an FOMC meeting this week that ends on Wednesday and the August 1st deadline for trade deals on Thursday. We already need a break just thinking about everything on the calendar!

This morning, equity futures are in a modestly positive position leading up to the onslaught of events and following a perfect week for the S&P 500 where it traded higher and at a record close every day last week. European stocks are also higher in the wake of the US–EU trade deal announced yesterday, and the STOXX 600 is up just over 0.5%. In Asia, it was more of a mixed session where Australia traded slightly higher, Japan was down over 1%, while China was fractionally higher.

Outside of equities, treasury yields are slightly higher, crude oil is up over 1%, while natural gas is down 1%. Gold, silver, and copper are basically unchanged to start off the week, but platinum and palladium are both up over 2%. In crypto, Bitcoin is trading just under $119K while the rally in Ethereum continues as it trades just below $3,900.

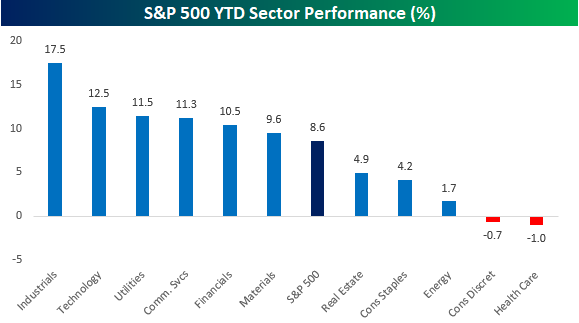

With all the talk about how market performance has been unbalanced between the mega-caps and everyone else, we wanted to look at performance within the S&P 500 on a YTD basis. At the sector level, most sectors (6) have outperformed the S&P 500 on YTD basis. Yes, Technology is one of the sectors that’s ahead of the S&P 500, but other non-tech sectors like Industrials, Utilities, Financials, and Materials have also outperformed on a YTD basis. On the other side of the performance spectrum, Health Care and Consumer Discretionary are the only two sectors in the red on a YTD basis.

Brunch Reads – 7/27/25

Welcome to Bespoke Brunch Reads — a linkfest of some of our favorite articles over the past week. The links are mostly market-related, but there are some other interesting subjects covered as well. We hope you enjoy the food for thought as a supplement to the research we provide you during the week.

The Inception of Insulin: On July 27, 1921, a laboratory at the University of Toronto became the birthplace of one of the most transformative medical breakthroughs of the 20th century that would go on to save millions of lives from the devastating grip of diabetes.

Before this discovery, a diagnosis of Type 1 diabetes was essentially a death sentence. The only available “treatment” was a starvation diet that could prolong life briefly but offered no real hope. Dr. Frederick Banting, a young surgeon with little research experience, believed that insulin was produced in the islets of Langerhans in the pancreas and that it could be extracted by tying off the ducts of the pancreas to preserve those cells while letting the rest degenerate.

With the reluctant support of physiology professor John Macleod and the help of Banting’s assistant Charles Best, Banting spent that summer experimenting on dogs. On July 27, their efforts paid off. They managed to isolate a substance from the pancreas that dramatically lowered blood sugar in a diabetic dog. That substance was insulin. Within a year, the team had refined the extract enough to treat a human patient, 14-year-old Leonard Thompson, who became the first person to receive insulin in early 1922. The breakthrough earned Banting and Macleod the Nobel Prize in 1923.

AI & Technology

Drones, AI and Robot Pickers: Meet the Fully Autonomous Farm (WSJ)

Autonomous farming is inching closer to reality as AI-guided tractors, drones, and robots begin to handle everything from planting to weeding without much human involvement. While the tools already exist, like Deere’s weed-targeting sprayers or berry-picking bots built with NASA-style precision, scaling them across farms is still slowed by cost, labor transition, and patchy rural internet. But with every drone flight and soil scan feeding into smarter, self-learning systems, the future of agriculture looks less like a field full of farmers and more like a network of machines. [Link]

Continue reading our weekly Brunch Reads linkfest by logging in if you’re already a member or signing up for a trial to one of our two membership levels shown below! You can cancel at any time.

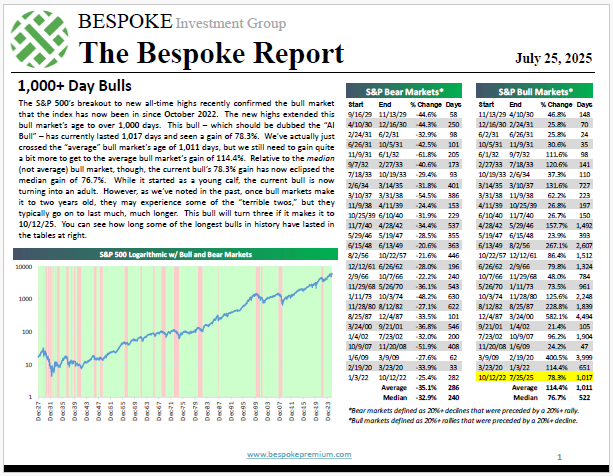

The Bespoke Report – 1,000+ Day Bulls

To read our weekly Bespoke Report newsletter and access everything else Bespoke’s research platform offers, start a two-week trial to Bespoke Premium. In this week’s report, we cover the bull market crossing the 1,000-day mark, underlying index technicals, how much the Fed should be cutting rates based on where inflation and employment stand, our unique Netscape vs. ChatGPT analysis, earnings season, longshot stocks, and more.

Q2 2025 Earnings Conference Call Recaps: HCA Healthcare (HCA)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers HCA Healthcare’s (HCA) Q2 2025 earnings call.

![]()

HCA Healthcare (HCA) is one of the largest for-profit hospital operators in the US, with a portfolio of over 180 hospitals and 2,300+ care sites across 20 states and the UK. The company serves millions of patients annually through a diversified mix of inpatient, outpatient, and emergency services, with a strong presence in high-growth, non-Medicaid expansion states like Texas and Florida. HCA reported 6.4% YoY revenue growth and improved payer mix. Supplemental Medicaid payments and better-than-expected performance in hurricane-impacted markets added $300M to EBITDA guidance. Managed care volumes rose 4%, with exchange admissions up 15.8%, while Medicaid and self-pay volumes underperformed. HCA emphasized its cost resiliency plans in light of the One Big Beautiful Bill Act and the looming expiration of enhanced premium tax credits. Management pointed to tight labor in select regions like North Carolina and growing physician costs, but noted overall labor stability and progress on automation and digital efficiency. HCA shares fell more than 2% on 7/25 despite EPS and revenue beats…

Continue reading our Conference Call Recap for HCA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Top Quotes from Recent Earnings Calls: 7/25/25

The Q2 2025 earnings season is well underway, and we sifted through earnings calls from the hundreds of companies that have reported since Wednesday’s (7/23) close, looking for some of the most interesting macro-related quotes from management teams that may serve as broader signals about the state of the economy, consumers, and markets. Below are twenty of the most revealing quotes that we pulled from this batch of calls, offering a window into what executives are seeing across industries and geographies right now.

- “We see AI powering an expansion in how people are searching for and accessing information, unlocking completely new kinds of questions you can ask Google… Our AI features cause users to search more as they learn that search can meet more of their needs. That’s especially true for younger users.” – Sundar Pichai, CEO, GOOGL

- “If you think about Marketplace and Medicaid members, what these folks have been hearing from every major media outlet for the last 6 months is that Congress is going to take away their health insurance. And that I think does drive a certain level of behavior when compounded with macroeconomic uncertainty… Then those folks are coming into the system and colliding with a provider ecosystem that is largely still operating in a fee-for-service manner [that] is concerned about losing revenue. And that’s where we’re seeing, I think, some of the aggressive billing and coding.” – Sarah London, CEO, CNC

- “Thus far, we believe the economy has been fairly resilient. Demand for transportation fuels remains strong, and I’m feeling more optimistic overall. The next key question is whether we’ll see further refinery rationalization.” – Gary Simmons, COO, VLO

- “I think we’ll probably have autonomous ride-hailing in half the population of the U.S. by the end of the year. That’s at least our goal, subject to regulatory approvals. I think we’ll technically be able to do… [And] the service areas and the number of vehicles in operation will increase at a hyper-exponential rate.” – Elon Musk, CEO, TSLA

- “This is a great time to be in the US wireless industry, as a customer, and as a participant. In the last 3 to 4 years, [customers have seen] speeds grow 3 to 4x, and data consumption grow 3 to 4x. And at the same time, customers have paid less in real terms for the product. And as an industry, we’ve seen a 50% growth in free cash flow, which is the one metric that really matters from a value creation perspective for the industry as a whole.” – Srinivasan Gopalan, COO, TMUS

- “No, I don’t think we can make any comments yet about consumer confidence. The demand for health care largely over time appears to have been inelastic. I don’t know that anything is necessarily changing that… We had good commercial growth in a lot of categories. We had declines in areas… that were government or no payer-sponsored business… Behavioral health admissions were down… Some of that was because we shrunk supply in certain facilities… So I think… we’re still pretty confident… in the demand for health care across our markets, and we don’t see that being disrupted too much in the short run here.” – Samuel N. Hazen, CEO, HCA

- “I used the word cautious optimism at the end of the first quarter. I would now turn my way all the way to optimism around the macro environment… I think Japan is reindustrializing… South Asia is growing at north of 10%… The Middle East are trying to create now diversified economies of which technology forms a strong piece… Europe has remained remarkably resilient… We come into North America and every company is now convinced that technology forms the basis of how do you scale revenue while not spending that much on CapEx and that much on labor expenses.” – Arvind Krishna, CEO, IBM

- “Joblessness is trending in the right direction. While GDP has been pulled down a little bit, it’s still positive for the back half of the year. And I think that all lends to a customer that’s more willing to get out there and spend and travel and do some things that they want to do.” – Robert D. Isom, CEO, AAL

- “The competitive environment is stable, not improving, but not deteriorating. So we have steady fiber overlap. That’s not new. Cell phone Internet continues at its pace for now. But just as big when you think about the overall market and funnel is the overall market is challenged because there’s an incredibly low amount of moves and new build… and then in addition to that, you have a reversion to mobile-only customers and [the Affordable Connectivity Program] accelerated that… reverting mobile-only back to the pre-pandemic level.” – Christopher Winfrey, CEO, CHTR

- “We’ve seen three quarters of revenue growth above our expectations, which we attribute at least in part to customers hedging against tariff uncertainty.”- David Zinsner, CFO, INTC

- “We have our arms around the what. I think the industry generally doesn’t have their arms around the why… The prevalence of behavioral conditions is up… People did not go for services during the pandemic, and now they are. There’s some pent-up demand. The supply side is finding interesting ways to code, to bundle codes… using AI… It’s happening nationally… not just Medicaid, not just Medicare… it’s across the board.” – Joseph Zubretsky, CEO, MOH

- “We’re seeing some pressure as energy project spending shifts to the right, partly due to economic uncertainty and regulatory issues. [Liquified Natural Gas] demand remains strong, but sustainable fuel projects have been the most impacted. Fortunately, things have cleared up over the last 10 days, and we expect positive momentum to return. Long term, the outlook for our energy segment remains extremely bullish, we’re simply in a normal part of the cycle.” – Vimal Kapur, CEO, HON

- “Many of the companies driving AI and data center growth don’t have strong infrastructure or utility capabilities, and some aren’t interested in building behind-the-meter power systems—our specialty. While we don’t have a specific project to announce right now, we’re positioning ourselves to capture growth as it emerges.” – James R. Fitterling, CEO, DOW

- “What I think feels different is it was just tough to get volume back even with promotions, [but] we’re starting to see the volume return. And I think that’s a strong sign that it’s a broad-based recovery… But to me, that’s very encouraging.” – Robert Jordan, CEO, LUV

- “There’s still pent-up demand. I have 0 doubt about that. How that gets released is going to… be the economic environment and how new vehicle affordability plays out in the coming months and years. If it doesn’t manifest itself in new vehicles, some of it tends to move into used vehicles. So you have to be agile in terms of how you move between the segments… But there is no doubt that there is and will remain our opportunity in the After-Sales side of the business.” – Michael M. Manley, CEO, AN

- “Tariffs are going to have — will not have a material impact on our growth rate when you look at our revenue growth year-on-year. They do have an impact on margin performance… because you’re passing it through. They’re largely a pass-through for us. So you see that in this updated guide as well.” – Kevin S. Krumm, CFO, FLEX

- “I met with the customer a couple of months ago that said that they were shifting some of their production from Asia into Mexico [because of tariffs], and we’ve got a strong service product coming out of Mexico… Over the long term, we think that, that will be a positive for us even if it doesn’t happen today or next week.” – Kenyatta Rocker, EVP of Marketing & Sales, UNP

- “We’ve had, I think, some very productive conversations with the administration with commerce over the last several weeks, and they’re listening to us. And I think they understand and share the same objective we do, which is to have U.S. manufactured vehicles be competitive in the U.S. and on the global stage… If logic prevails here, that seems to make a lot of sense to protect the competitiveness of U.S. manufactured vehicles.” – Jason Cardew, CFO, LEA

- “We recognize our consumers are under pressure from car prices and other costs, which have outpaced wage growth and higher interest, virtually double the rates we saw just a few years back.” – Daryl Kenningham, CEO, GPI

- “NATO members are now targeting defense spending increases to 5% of GDP… We recently secured software-defined radio awards from the German and Czech armed forces… replacing indigenous providers, a direct result of our resilient interoperable, battlefield proven technology and expanding global footprint.” – Christopher Kubasik, CEO, LHX

- “While enthusiasm for the boating lifestyle remains high, the uncertainty is prompting buyers to delay purchases until the economic outlook is clearer.” – Brett McGill, CEO, HZO

Q2 2025 Earnings Conference Call Recaps: Centene (CNC)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Centene’s (CNC) Q2 2025 earnings call.

![]()

Centene (CNC) is a government-focused managed care company that provides health insurance through Medicaid, Medicare Advantage, and Affordable Care Act (ACA) marketplaces. Serving over 28 million members across all 50 states, Centene specializes in delivering healthcare services to low-income, vulnerable, and medically complex populations. Its Ambetter brand makes it the largest player in the ACA exchanges, while its scale in Medicaid gives it deep insight into US healthcare policy shifts, cost trends, and regulatory impacts. Q2 2025 was defined by a $2.4B earnings hit tied to a sharp deterioration in ACA marketplace risk pools, as healthy members left and high-utilizing members surged, exacerbated by program integrity enforcement. Medicaid margins were also pressured by rising costs in behavioral health, home care, and high-cost drugs, especially in Florida and New York. Medicare Advantage showed stable improvement, and Part D exceeded expectations with margins above 1%. The EPS miss on better-than-expected revenue resulted in a 4.5% gain for the stock on 7/25…

Continue reading our Conference Call Recap for CNC by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Intel (INTC)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Intel’s (INTC) Q2 2025 earnings call.

![]()

Intel (INTC) is one of the world’s largest semiconductor manufacturers, known for designing and producing CPUs, GPUs, and other chips that power PCs, servers, data centers, and edge devices. The company serves a broad customer base, from global cloud providers and enterprises to governments and OEMs. Intel is a key bellwether for both the technology supply chain and global manufacturing policy, particularly as a US-based chipmaker amid rising geopolitical tension and AI-fueled demand for compute. On the Q2 2025 call, Intel reported $12.9B in revenue (above estimates), but posted a GAAP EPS loss due to $800M in tool impairments and $1.9B in restructuring charges. CEO Lip-Bu Tan emphasized discipline across the board: right-sizing the organization (cutting 50% of management layers), cutting $5B in CapEx YTD, and pausing unprofitable fab expansions. AI was a major focus, with Intel repositioning around inference and “agentic AI,” while acknowledging its historic software gaps. Panther Lake (18A) and Granite Rapids are ramping, but Tan noted rebuilding trust in both x86 and foundry will take time and results. On mixed results, INTC shares were down 9% on 7/25…

Continue reading our Conference Call Recap for INTC by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Boston Beer (SAM)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Boston Beer’s (SAM) Q2 2025 earnings call.

![]()

Boston Beer (SAM) is one of the largest craft brewers in the US, best known for its Samuel Adams beer, Twisted Tea, Truly Hard Seltzer, Angry Orchard cider, Dogfish Head ales, and most recently, Sun Cruiser RTD (Ready To Drink) spirits. The company serves a wide range of consumers across beer, cider, and spirits alternatives, especially younger and flavor-seeking drinkers, while offering investors a window into evolving alcohol trends and consumer behavior. Its outsized focus on “beyond beer” categories (over 85% of volume) positions it uniquely within a declining beer industry. Despite a tough environment marked by weak summer demand and pressure on Hispanic consumers, Boston Beer posted 1.5% YoY revenue growth, a 380 bps YoY improvement in gross margin to 49.8%, and EPS growth of 24% to $5.45. Sun Cruiser saw strong distribution growth and is already a 4-share brand in RTD spirits. Twisted Tea lost floor space and may be overpriced in some packs, while Truly saw traction in its high-ABV “Unruly” line. Productivity gains and procurement savings helped offset $15–20M in expected tariff costs. Better-than-expected results lifted the stock as much as 12.9% on 7/25…

Continue reading our Conference Call Recap for SAM by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below: