Q2 2025 Earnings Conference Call Recaps: Starbucks (SBUX)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Starbucks’ (SBUX) Q3 2025 earnings call.

![]()

Starbucks (SBUX) is the world’s largest specialty coffee chain, operating over 38,000 stores globally with a strong presence in North America, China, and other international markets. Starbucks caters to a broad customer base, including millennials, Gen Z, and urban professionals. The company is a leader in digital engagement, with nearly 34 million active rewards members and a top-rated mobile app. Its business spans in-café, drive-thru, digital, and delivery channels. This quarter focused heavily on Starbucks’ US turnaround, centered on the accelerated rollout of the Green Apron Service model, a new operating system showing early success in improving transaction comps and service speed. Despite a 2% global comp decline, China returned to comp growth (+2%) and posted strong delivery and beverage innovation gains. Management also detailed plans for loyalty program upgrades, smaller and more efficient store formats, and a shift toward protein-enhanced beverages and functional food. CEO Brian Niccol emphasized the upcoming innovation wave in 2026 and ongoing search for a strategic partner in China, noting over 20 interested parties. SBUX shares opened 5.7% higher on 7/30 on mixed results, but erased those gains intraday…

Continue reading our Conference Call Recap for SBUX by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Booking (BKNG)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Booking’s (BKNG) Q2 2025 earnings call.

![]()

Booking (BKNG) is the world’s largest online travel platform, operating global brands like Booking.com, Priceline, Agoda, KAYAK, and OpenTable. It facilitates millions of accommodations, flights, car rentals, and restaurant reservations, serving both leisure and business travelers. Its Genius loyalty program and Connected Trip vision (bundling multiple travel components into one seamless booking) position it to drive both engagement and margins. Booking delivered a standout quarter, with room nights up 8%, gross bookings up 13%, and adjusted EPS up 32% YoY. Alternative accommodations grew 10%, outpacing hotels, and the Connected Trip saw 30%+ transaction growth. Asia was the fastest-growing region, while US consumers showed caution via shorter stays and lower ADRs. AI tools like Priceline’s Penny and OpenTable’s Concierge are boosting efficiency and conversion, and direct bookings now exceed 65% of B2C volume. BKNG shares were up less than 1% on 7/30 on EPS and revenue beats…

Continue reading our Conference Call Recap for BKNG by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Polaris (PII)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Polaris’ (PII) Q2 2025 earnings call.

![]()

Polaris (PII) is a manufacturer of powersports vehicles, including off-road vehicles (ORVs), snowmobiles, motorcycles (Indian and Slingshot), and marine products, like Bennington pontoons. Polaris dominates niche markets such as utility and recreational side-by-sides, offering high-quality vehicles with strong dealer support. The company serves outdoor enthusiasts, farmers, commercial users, and lifestyle buyers, while also providing parts, gear, and accessories to enhance the ownership experience. Polaris exceeded expectations despite a 6% sales decline, driven by industry weakness and tariffs. Share gains across every segment were fueled by standout products like the XPEDITION and the newly launched RANGER 500, targeting value-focused buyers at $9,099. Tariffs remain a headwind, with an estimated $230M annualized impact, though the company has cut its China sourcing by nearly half and aims to reduce exposure by 35% by year-end. Retail demand was flat but stable, with utility vehicles showing strength, while promotions and interest rates pressured margins. PII shares were up 16.9% on 7/29 after posting stronger than expected results and launching new vehicles…

Continue reading our Conference Call Recap for PII by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: JetBlue (JBLU)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers JetBlue’s (JBLU) Q2 2025 earnings call.

![]()

JetBlue (JBLU) is a US-based low-cost carrier, offering free in-flight Wi-Fi, live TV, and extra legroom options. Serving leisure and value-conscious travelers across the US, Latin America, and transatlantic routes, JBLU operates a primarily Airbus fleet, including its efficient A220 and A320 aircraft. The company also runs a growing travel products business through its Paisly platform and has built a loyal following through its TrueBlue rewards program. JBLU delivered a modest operating profit in Q2 as it advanced its JetForward transformation, generating $180M in EBIT YTD. The standout announcement was Blue Sky, a new partnership with United Airlines that enables cross-selling, loyalty integration, and Paisly white-label expansion. It is expected to drive $50M in incremental EBIT by 2027. Close-in bookings surged mid-quarter, particularly around peak travel, though management remains cautious about calling the shift permanent. The forecast for grounded aircraft tied to Pratt & Whitney engine issues improved, clearing a path for low single-digit capacity growth in 2026. The stock was up 6.7% on 7/29 on better-than-expected results…

Continue reading our Conference Call Recap for JBLU by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day – Consistently Overbought

The Triple Play Report — 7/30/25

An earnings triple play is a stock that reports earnings and manages to 1) beat analyst EPS estimates, 2) beat analyst sales estimates, and 3) raise forward guidance. You can read more about “triple plays” at Investopedia.com where they’ve given Bespoke credit for popularizing the term. We like triple plays as an indication that a company’s business is firing on all cylinders, with better-than-expected results and an improving outlook. A triple play is indicative of positive “fundamental momentum” instead of pure fundamentals, and there are always plenty of names with both high and low valuations on our quarterly list.

Bespoke’s Triple Play Report highlights companies that have recently reported earnings triple plays, and it features commentary from management on triple-play conference calls, company descriptions and analysis, and price charts. Bespoke’s Triple Play Report is available at the Bespoke Institutional level only. You can sign up for Bespoke Institutional now and receive a 14-day trial to read this week’s Triple Play Report, which features 21 new stocks. To sign up, choose either the monthly or annual checkout link below:

Bespoke Institutional – Monthly Payment Plan

Bespoke Institutional – Annual Payment Plan

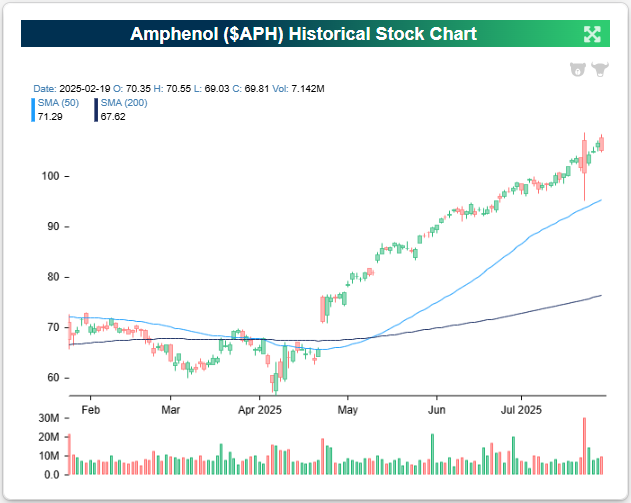

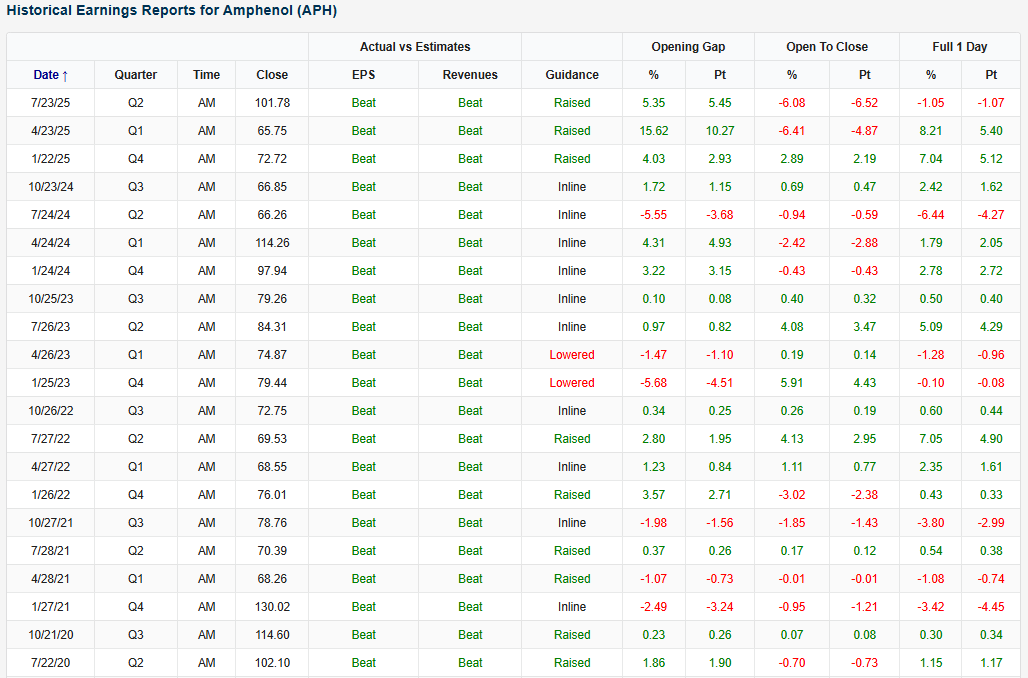

Amphenol (APH) is an example of a company that recently reported an earnings triple play before the open on 7/23. It was the company’s third straight triple play, but the stock turned negative that day after the positive moves in reaction to the two prior triple plays.

Here’s how AI describes the company: Amphenol (APH) is one of the world’s largest designers, manufacturers, and marketers of electrical, electronic, and fiber optic connectors, as well as interconnect systems, coaxial and specialty cables, and high-performance sensors. The company’s core function is to enable high-speed signal transmission and power distribution across a wide range of demanding environments, serving industries such as automotive, aerospace, defense, industrial, IT/data communications, mobile devices, and broadband. Amphenol operates through three primary business segments: Harsh Environment Solutions, Communications Solutions, and Interconnect and Sensor Systems. The Harsh Environment Solutions segment provides ruggedized connectors and interconnects used in military, commercial aerospace, automotive, and heavy industrial markets. Communications Solutions serves the mobile devices and IT/data communications markets, supplying connectors for smartphones, tablets, servers, and networking equipment. Interconnect and Sensor Systems covers a broad industrial and transportation footprint, including sensors and interconnects used in factory automation, rail, green energy, medical, and hybrid-electric vehicle applications.

Amphenol posted a blockbuster Q2 with record sales of $5.65B, up 57% YoY and 41% organically, as every end market delivered double-digit organic growth. The standout driver was AI-fueled demand in the IT datacom segment, which surged 133% organically and now makes up 36% of total sales. CEO Adam Norwitt said the company actually shipped “substantially more than expected,” including some Q3 volume, because “our team outperformed even our customers’ very high expectations.” Roughly two-thirds of both YoY and sequential IT datacom growth came from AI-related products, which Amphenol delivers across the stack, from chipmakers to hyperscalers, thanks to its critical role in high-speed, power, and fiber-optic interconnects. Even with some pull-forward, Q3 sales are only expected to dip mid-single digits, and Norwitt emphasized they’re still winning new AI programs and expanding capacity globally, supported by elevated CapEx. Outside of AI, defense sales rose 25% YoY, with global geopolitical tensions driving long-term opportunity, and European industrial sales turned positive, with broad strength in factory automation, medical, and alternative energy.

Looking at the snapshot below from our Earnings Explorer, Amphenol (APH) has been on a triple play hot streak, with very strong EPS and revenue beat rates, 91% and 94%, respectively, since 2001 when our database begins. The company’s EPS beat streak goes back to 2020 and 2016 for revenue.

You can read more about APH and the 20 other triple plays we covered in our newest report by starting a Bespoke Institutional trial today.

Bespoke Investment Group, LLC believes all information contained in these reports to be accurate, but we do not guarantee its accuracy. None of the information in these reports or any opinions expressed constitutes a solicitation of the purchase or sale of any securities or commodities. This is not personalized advice. Investors should do their own research and/or work with an investment professional when making portfolio decisions. As always, past performance of any investment is not a guarantee of future results. Bespoke representatives or clients may have positions in securities discussed or mentioned in its published content.

Bespoke’s Morning Lineup – 7/30/25 – Should This Worry You?

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Measuring programming progress by lines of code is like measuring aircraft building progress by weight.” – Bill Gates

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are modestly higher this morning after the July ADP report came in better than expected, erasing a streak of three months of weaker-than-expected readings. Q2 advance GDP was also just released and came in stronger than expected (3.0% vs 2.6%). Personal Consumption was weaker than expected (1.4% vs 1.5%) while the inflation data was mixed (lower than expected at the headline, higher than expected on a core basis). While these would be big reports on a normal day, we still have the Fed this afternoon and earnings from Meta and Microsoft after the close.

We’re right in the thick of earnings season, and we’ll see hundreds of more reports between now and the end of the week. From the start of July through Tuesday morning, we’ve already got 461 reports, and of those, 78% exceeded EPS forecasts while 75% have topped sales estimates. Looking forward, 8% of companies reporting have raised their guidance, while just 6% have lowered their estimates. These are all better than average readings, and as you would expect, companies are reacting positively to these reports. Overall, the average opening gap of the companies reporting has been a gain of 0.94%, but from the open to close, we’ve seen selling into strength with an average decline of 0.52% for a full-day gain of 0.41%. On the one hand, the average positive reaction to earnings reports is a good signal, but the weakness from the open to close indicates that investors are taking profits.

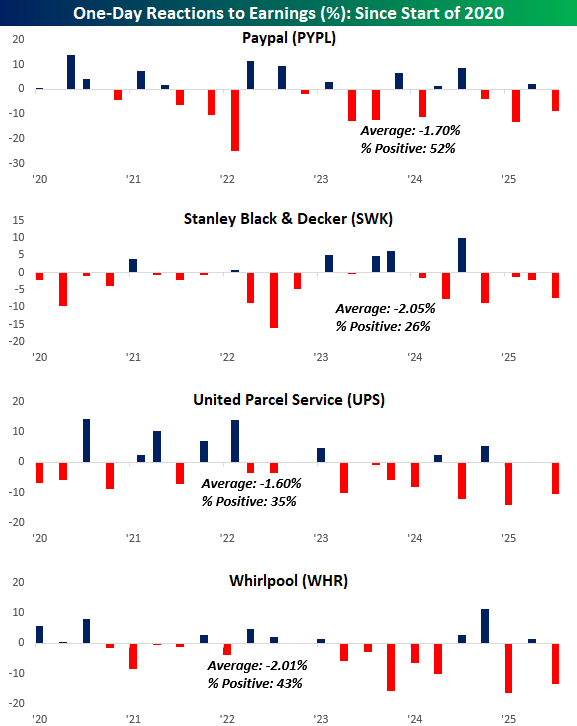

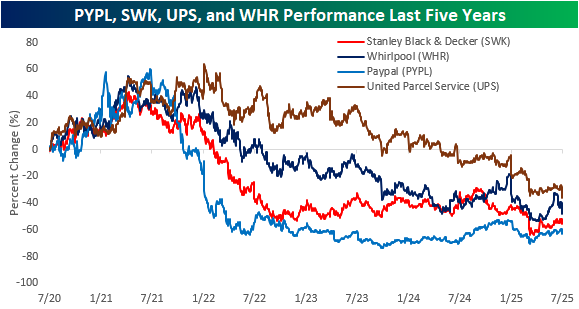

Despite the overall positive tone of reports, yesterday we saw multiple stories highlighting four stocks and their negative reaction to earnings as a potential warning sign for the economy and market. Those four stocks were PayPal (PYPL), Stanley Black & Decker (SWK), United Parcel Service (UPS), and Whirlpool (WHR), and all of them were down at least 7%.

Besides the fact that these four stocks have a combined market cap of less than $160 billion, which wouldn’t even be enough to rank in the top 75 companies in the S&P 500, they have all historically had weak reactions to earnings, especially in recent years. The chart below shows each stock’s performance on its earnings reaction days over the last five years. All four have averaged declines of at least 1.6% on their earnings reaction days, and only PYPL has reacted positively more often than it has reacted negatively.

More importantly than the performance on their earnings reaction days, all four stocks have been horrendous performers over the last five years. As shown in the chart below, at one point in the last five years, all four stocks were up at least 40% from where they traded five years ago, but they have erased those gains and more over the last five years. UPS is down 36%, WHR is down 48%, while PYPL and SWK have both lost over half of their value. During this same period, the S&P 500 has rallied 96%. Far from being economic or market bellwethers, these stocks have been among the S&P 500’s worst performers over the last five years! We could highlight any number of reasons why investors should be more cautious heading into the end of summer, but the fact that four stocks that have historically performed poorly on earnings saw weakness yesterday is not one of them.

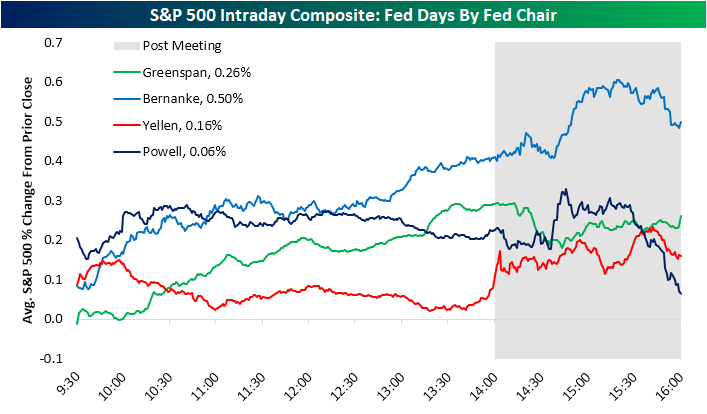

Powell Fed Days: 7 Left

With just 7 Fed Days left of his tenure including today, Chair Powell’s time as head of the Fed is coming to an end. And as shown below, the S&P 500 has gained 0.06% on average on Fed Days during Powell’s tenure dating back to February 2018, which is actually the weakest of the four chairs we’ve had since 1994 when they first began announcing policy moves on the day of their meetings. Ben Bernanke saw the best market performance on Fed Days with an average gain of 0.50%, followed by Greenspan’s 0.26% gain and Yellen’s 0.16% move.

Interestingly, the stock market has done well early in the day on Powell Fed Days, but it’s the final hour and a half of the trading day that does him in. The typical Powell Fed Day has seen solid market gains in morning trading through around 2:30 PM ET when the Fed’s press conference usually begins, and from there, the trend has been for the market to tank into the close.

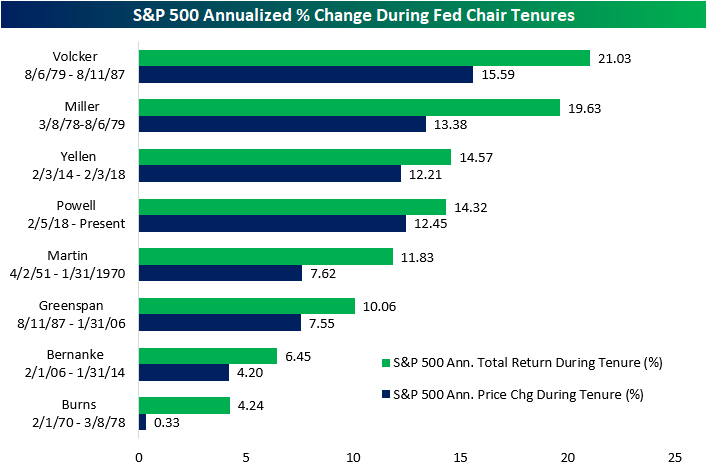

While Powell Fed Days are now known for seeing extreme market weakness into the 4 PM ET close, overall, the market has done well during Powell’s tenure. As shown below, since Powell became Fed Chair in early 2018, the S&P has posted an annualized total return of 14.3%, which ranks him fourth out of eight chairs dating back to 1950.

The Closer – Earnings Onslaught, Trade, Jobs – 7/29/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, after recapping a busy night of earnings (pages 1 and 2), we dive into the latest update of trade data (page 3). Next, we look at the changes in home prices (page 4) before pivoting to a look at job openings in the form of the JOLTS release (page 5) and Indeed data (page 6). We cap off with a dive into consumer confidence figures (page 7).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Top Quotes from Today’s Earnings Calls: 7/29/25

The Q2 2025 earnings season is well underway, and we sifted through earnings calls from the 92 companies that have reported since Monday’s (7/28) open, looking for some of the most interesting macro-related quotes from management teams that may serve as broader signals about the state of the economy, consumers, and markets. Below are twenty of the most revealing quotes that we pulled from this batch of calls, offering a window into what executives are seeing across industries and geographies right now.

- UPS (UPS): “[Small businesses] are finding that in today’s environment, credit conditions have tightened up a bit on them. So it’s not that they don’t have access to capital in the ways that they have seen in prior years. So there are a number of just challenges that this group is faced with.” – Carol Tomé, CEO

- Proctor & Gamble (PG): “The volatility the consumer is seeing isn’t necessarily grounded in their current reality, but more about what they expect in the future. So consumers are being more careful with their consumption. They’re using up pantry inventory and looking for value, either in smaller packs and promotions, or in larger pack sizes from club stores and online.” – Andre Schulten, CFO

- Merk (MRK): “The CDC’s Advisory Committee on Immunization Practices subsequently voted to recommend ENFLONSIA for use in infants younger than 8 months of age for their first RSV season and include this new option in the Vaccines for Children Program, an important step in ensuring access.” – Dean Li, President

- Enterprise Products (EPD): “This past quarter was dominated by headlines about tariffs and trade… We’ve been clear about the risk of weaponizing U.S. energy exports. These kind of actions rarely hurt the intended target and often backfire hurting our own industry more… We’re fortunate this administration understands the importance of energy and global trade even if the Commerce Department may need a little reminder.” – James Teague, Co-CEO

- CBRE Group: “There is a lot of capital out there. We have it and other people have it that wants to buy real estate, and there is a huge amount of sell-side interest on the part of owners of real estate that haven’t been able to sell it for the last few years… We expect the sales activity and the refinancing activity to both continue strong in the back half of the year. We’re not expecting interest rates to move in a way that alter that materially.” – Robert Sulentic, CEO

- Nucor (NUE): “If we think about the resiliency of [non-residential construction] on the construction market in general. That took off really post-COVID, and it has remained robust for a long period of time, and we anticipate that remaining robust… So again, the demand drivers for this segment [steel products tied to commercial, industrial, and infrastructure builds] are really robust, and we expect them to remain that way, again, throughout the rest of this year and quite frankly, beyond.” – Leon Topalian, President, CEO

- PayPal (PYPL): “Today, almost 3.5 billion people rely on digital wallets as their go-to method for shopping and transferring funds… That’s 83% of global digital payments happening through wallets… But among those billions of users, there are hundreds of regional wallets represented. This fragmented system of wallets poses tremendous challenges and immense friction in a global commerce ecosystem.” – Alex Chriss, CEO

- Hartford Financial (HIG): “Yes… I think we spoke about it equally in the past. [Litigation finance and social inflation] are still a fact of life, still a tax. It’s still a burden. It’s not fair. It’s not what our court system was intended to [support]. But I’m also equally optimistic that more and more people across the industry and businesses are getting involved and trying to take a legislative corrective action [to curb these excesses]… I think it’s getting a little bit more national attention, particularly in D.C., and I was really actually encouraged by former Attorney General Barr’s comments on the need just to put some limits on these injury claims, including noneconomic limits.” – Christopher Swift, CEO

- Waste Management (WM): “I think you actually are seeing a little bit of strength in the economy that we haven’t had. We’ve talked about kind of an industrial recession over the last probably 5 or 6 quarters. And I think that’s largely kind of dissipated and we’re seeing it in roll-off and in [construction and demolition].” – James Fish, CEO

- Carrier Global (CARR): “We have not seen a big switch from repair over replace. We are watching the consumer. Movement was slower in 2Q than we had expected. Movement was a bit light in July, but it started to pick up towards the end of July, a bit more because of some of the heat in the country… Interest rates have continued to be high, which has put a damper on residential new construction and also people moving to buy new homes.” – David Gitlin, CEO

- Johnson Controls (JCI): “China is maybe a longer discussion, but I was there recently and maybe the one tidbit is that, that market is gradually turning into a more mature market in the sense of that the retrofit part of the market continues to steadily increase, which is different than a number of years ago when it was sort of a new construction new build market. So it’s starting to look a little bit more like some of our Western markets.” – Joakim Weidemanis, CEO

- Asbury Automotive (ABG): “The average age of a passenger car on the road is 14.5 years old, and the average truck is nearly 12 years old… recent and upcoming models have more technology and innovative powertrains, which should create opportunity for our service departments for years to come.” – Daniel Clara, COO

- Koninklijke Philips (PHG): “We continue to see strong demand in North America, with patient volumes remaining high and procedures still on the rise. Health systems are increasingly focused on productivity… finding ways to serve more patients at lower cost. At the same time, there’s growing interest in ambulatory solutions to extend care beyond hospital walls. Most importantly, we see this demand trend holding steady into next year. – Roy Jakobs, CEO

- Universal Health (UHS): “We continue in certain markets to be hampered by our inability to hire all the staff that we need. It’s still a tight labor market. And again, while it is not the pervasive issue that it was at the height of the pandemic, staffing scarcity continues to be an issue in some markets.” – Steve Filton, CFO

- UnitedHealth (UNH): “The American health system’s long-standing cost problem is accelerating. We are embracing our responsibility to continue to drive better health outcomes while trying to keep healthcare affordable for all Americans.” – Tim Noel, CEO

- Sysco (SYY): “Traffic to restaurants [was] down approximately 1% in the quarter, certainly better than Q3. We believe Q3 was a bit of an anomaly… external news was quite negative, consumer confidence dropped, the conversations about tariffs and the impact on consumer confidence [lowered traffic to restaurants] … We’re expecting the current conditions to continue for 2026.” – Kevin Hourican, CEO

- Lithia Motors (LAD): “I believe that manufacturers have already begun to either decontent cars or not charge for other upgrades… Consumers can save other dollars… So a finite 15% increase when we think about the tariff… is just another thing in our daily lives… As the world moves on and as [tariffs] start to change the industry, those with more cash and more ability to code solutions for customers [to] make it easier are those that are going to be able to grow market share and be less impacted by whatever changes do come from tariffs, franchise laws, or whatever else.” – Bryan DeBoer, CEO

- Royal Caribbean (RCL): “We see a very healthy customer. When we dig into that customer, they have great jobs, they have strong balance sheets, and they’re confident in spending and making sure that they’re receiving the vacation experience that they’re looking for. So again, I think all turns are green on the customer at this point in time, and they’re traveling all over the world. We’re seeing that not just in North American, but we’re also seeing that in European travel activity.” – Jason Liberty, CEO

- Boeing (BA): “[Supply chain] constraints tomorrow get resolved and then there’s new constraints, and you just constantly are working each one of those down… We’re in a perpetual rate increase kind of environment.” – Robert Kelly Ortberg, CEO