Q2 2025 Earnings Conference Call Recaps: Mastercard (MA)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Mastercard’s (MA) Q2 2025 earnings call.

![]()

Mastercard (MA) is a global payments technology company that facilitates electronic payments across more than 210 countries. It operates one of the world’s largest payment networks, connecting consumers, financial institutions, merchants, governments, and businesses. While best known for credit and debit card transactions, Mastercard has expanded into cybersecurity, data analytics, open banking, and digital identity. Mastercard reported 16% revenue growth and 12% adjusted net income growth as strong consumer spending and rising FX volatility lifted results. Cross-border volumes rose 15%, with non-travel e-commerce up about 20%. The call highlighted momentum in Click to Pay, tokenization, and fleet/SME cards. Its value-added services, like AI-powered fraud prediction and Dynamic Yield personalization, continue to differentiate Mastercard and justify pricing power. Commercial payments and B2B virtual cards also gained traction through partnerships with platforms like SAP and Oracle. Management emphasized a strong US consumer, stable trends across income tiers, and an outlook buoyed by wage growth outpacing inflation. MA posted better-than-expected results on the top and bottom lines, and the stock moved about 2.5% higher on 7/31…

Continue reading our Conference Call Recap for MA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Shake Shack (SHAK)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Shake Shack’s (SHAK) Q2 2025 earnings call.

![]()

Shake Shack (SHAK) is a premium fast-casual restaurant chain known for its high-quality burgers, hand-spun shakes, and crinkle-cut fries. With roots in a single hot dog cart in NYC, it has grown into a global brand offering a more elevated alternative to traditional fast food. Shake Shack serves urban diners, travelers, and families alike, both domestically and through international licensed partners. The burger chain posted 1.8% Same-Shack Sales growth in Q2 and 23.9% restaurant-level margins, its highest in 24 quarters. Traffic turned positive in July (+3.2%), aided by a $10 Dubai Shake and new app promos. For the first time, Shake Shack launched top-of-funnel paid media, targeting 15 test markets to support LTOs and drive app adoption. The company opened 13 new company-operated Shacks and remains on track for 45–50 this year, its largest class ever. Supply chain efforts helped offset beef inflation, and cost-to-build is down about 10%. Despite EPS and revenue beats, SHAK shares took a big back step on 7/31, trading down more than 13%…

Continue reading our Conference Call Recap for SHAK by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Builders FirstSource (BLDR)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Builders FirstSource’s (BLDR) Q2 2025 earnings call.

![]()

Builders FirstSource (BLDR) is the largest supplier of structural building products, manufactured components, and value-added services to residential and multi-family homebuilders, repair and remodel contractors, and manufactured housing builders in the US. The company produces everything from roof trusses to millwork and offers integrated solutions like digital tools and off-site construction. BLDR’s operations span 43 states, with strength in fast-growing Sunbelt markets. Amid soft housing starts and affordability headwinds, BLDR delivered durable profitability with Q2 sales down 5% to $4.2B and adjusted EBITDA of $506M. Single-Family and Multi-Family revenues declined 9% and 23%, respectively, while R&R (Repair & Remodel) rose 3%. The company consolidated 8 facilities YTD, maintained a 92% on-time delivery rate, and continued ramping adoption of its BFS digital tools (>$2B in orders YTD, up 400% YoY). OSB (Oriented Strand Board) oversupply remains a drag, but lumber is stable. Management expects continued pressure in H2, but sees potential upside in 2026 if rates ease and builder destocking finishes. BLDR beat EPS estimates but came up short on the top line and revised guidance downward. The stock fell 5.3% at the open on 7/31 as a result…

Continue reading our Conference Call Recap for BLDR by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

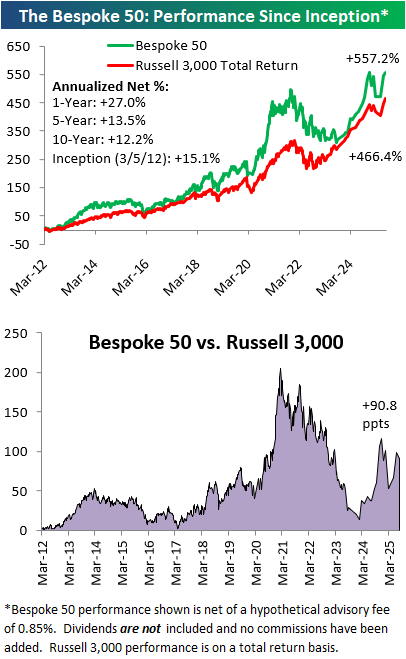

The Bespoke 50 Growth Stocks — 7/31/25

The “Bespoke 50” is a basket of noteworthy growth stocks in the Russell 3,000. To make the list, a stock must have strong earnings growth prospects along with an attractive price chart based on Bespoke’s analysis. There were 15 changes to the list this week.

The Bespoke 50 is available with a Bespoke Premium subscription or a Bespoke Institutional subscription. With Bespoke Premium, you’ll receive a number of daily market updates from us along with our weekly newsletter and a portion of our investor tools. With Bespoke Institutional, you’ll receive everything that’s included with Premium plus additional daily macro analysis and more stock-specific research.

To see all 50 stocks that currently make up the Bespoke 50, simply start a two-week trial to Bespoke Premium or Bespoke Institutional.

The Bespoke 50 performance chart shown does not represent actual investment results. The Bespoke 50 is updated monthly on Thursdays unless otherwise noted. Performance is based on equally weighting each of the 50 stocks (2% each) and is calculated using each stock’s opening price as of Friday morning after publication. Entry prices and exit prices used for stocks that are added or removed from the Bespoke 50 are based on Friday’s opening price. Any potential commissions, brokerage fees, or dividends are not included in the Bespoke 50 performance calculation, but the performance shown is net of a hypothetical annual advisory fee of 0.85%. Performance tracking for the Bespoke 50 and the Russell 3,000 total return index begins on March 5th, 2012 when the Bespoke 50 was first published. Past performance is not a guarantee of future results. The Bespoke 50 is meant to be an idea generator for investors and not a recommendation to buy or sell any specific securities. It is not personalized advice because it in no way takes into account an investor’s individual needs. As always, investors should conduct their own research when buying or selling individual securities. Click here to read our full disclosure on hypothetical performance tracking. Bespoke representatives or wealth management clients may have positions in securities discussed or mentioned in its published content.

Q2 2025 Earnings Conference Call Recaps: Carvana (CVNA)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Carvana’s (CVNA) Q2 2025 earnings call.

![]()

Carvana (CVNA) is a US e-commerce platform for buying and selling used cars entirely online. It differentiates itself through vertical integration, owning everything from inspection centers and logistics to financing, which allows it to deliver vehicles directly to consumers’ driveways, often within 24 to 48 hours. As of Q2 2025, it holds just 1.5% of the US used car market but has ambitions to reach 3 million annual units. Carvana posted a record-breaking Q2 with 41% unit growth and $4.84B in revenue. Adjusted EBITDA grew to $601M (12.4% margin), while GAAP operating income hit $511M. Tariff-related demand in April boosted retail GPU (Gross Profit per Unit) by $100. ADESA site integrations expanded to 12, cutting inbound transport miles by 20%. Marketing spend rose as the company pushes brand awareness and word-of-mouth. AI is already being deployed in customer service and documentation workflows, showing early efficiency gains. CVNA shares were up as much as 22% on 7/31 following the better-than-expected results. That pushed the stock to a new all-time high after a 99% drawback from its previous August 2021 high! That’s a 10,445% gain from the 12/27/22 low!…

Continue reading our Conference Call Recap for CVNA by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q2 2025 Earnings Conference Call Recaps: Microsoft (MSFT)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Microsoft’s (MSFT) Q4 2025 earnings call.

![]()

Microsoft (MSFT) is currently the second-largest company in the world by market cap, behind NVIDIA, selling software, cloud services, hardware, and AI-powered solutions across consumer and enterprise markets. Best known for products like Windows, Office, Azure, and LinkedIn, the company serves businesses of all sizes, government agencies, and billions of consumers worldwide. It’s at the forefront of the AI revolution, uniquely positioned with massive cloud scale, proprietary models via OpenAI, and an expansive product ecosystem from developer tools to business applications. Microsoft delivered a blockbuster quarter, with revenue up 18% to $76.4B and EPS rising 24% to $3.65. Azure grew 39% as demand for AI workloads, cloud-native apps, and major migrations (e.g., Nestlé moving 200 SAP instances) accelerated. The Copilot suite now boasts 100M+ monthly users, with major clients like Barclays and UBS scaling adoption. Foundry processed 500T tokens and is now used by 80% of the Fortune 500. CapEx will top $30B next quarter, yet the company remains supply-constrained despite standing up 2+ gigawatts of new data center capacity. Management struck a confident tone, calling the current AI wave a “generational tech shift.” MSFT shares popped more than 9% after hours on 7/30 in reaction to the strong results…

Continue reading our Conference Call Recap for MSFT by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

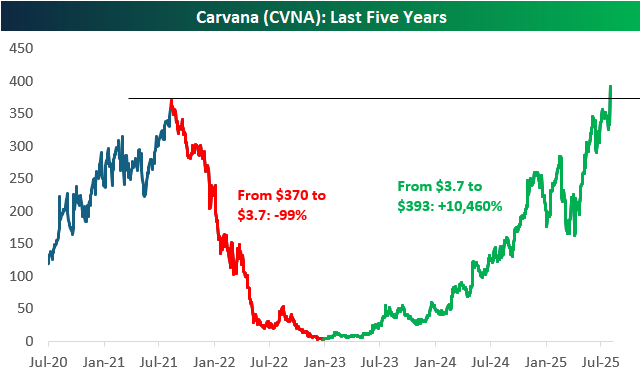

The Carvana (CVNA) Comeback

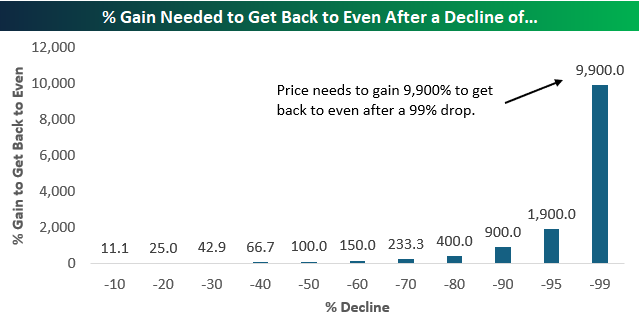

Even if you’ve been following markets for decades, you’ve likely never seen anything as crazy as the comeback that online used-car company Carvana (CVNA) has experienced in the last couple of years. Big stocks like Netflix (NFLX) and Meta (META) saw massive drawdowns of 75%+ during the bear market of 2021 and 2022, but Carvana (CVNA) was on another level with a decline of 99% from a peak of $370/share to its closing low of $3.72 made on 12/27/22.

As shown below, a stock that falls 70% needs to gain 233% to get back to even. That’s a tall task, but it at least seems do-able. A stock that falls 99%, however, needs to gain 9,900% to get back to even. That seems downright impossible!

Below is a price chart of Carvana (CVNA) over the last five years. As of today, with the stock currently up 17% on earnings to $393/share, CVNA has not only fully recovered its 99% drawdown, but it has also eclipsed its prior highs. In less than three years, the stock has gained 10,460%! Maybe you have, but we’ve never seen any recovery quite this remarkable.

Bespoke’s Matrix of Economic Indicators – 7/31/25

Our Matrix of Economic Indicators provides a concise summary analysis of the US economy’s momentum. We combine trends across the dozens and dozens of economic indicators in various categories like manufacturing, employment, housing, the consumer, and inflation to provide a directional overview of the economy.

To access our newest Matrix of Economic Indicators, start a two-week free trial to either Bespoke Premium or Bespoke Institutional now!

Q2 2025 Earnings Conference Call Recaps: Meta Platforms (META)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Meta Platforms’ (META) Q2 2025 earnings call.

![]()

Meta Platforms (META) is a powerhouse in social networking, digital advertising, and immersive technology. It owns Facebook, Instagram, WhatsApp, and Threads, serving over 3.4 billion daily users with communication, content discovery, and commerce tools. It also operates Reality Labs, developing AR/VR devices like Meta Quest and AI-powered smart glasses in partnership with Ray-Ban and Oakley, pushing toward a future of AI-integrated wearables and spatial computing. Meta’s Q2 2025 call highlighted growing AI ambition, strong ad performance, and aggressive infrastructure expansion. The company formed Meta Superintelligence Labs and plans to scale Llama models, with Prometheus (its gigawatt-scale AI cluster) coming online next year. Ad conversions rose 5% on Instagram and 3% on Facebook, driven by new models like GEM and Lattice. Threads now uses LLMs for content ranking, while Meta AI exceeded 1 billion monthly users, with WhatsApp leading usage. CapEx for 2025 was raised to $66–$72B, and 2026 CapEx is set to surge again. Glasses and messaging saw growing traction, but Meta warned of possible “significant” European ad revenue hits due to regulatory changes. The triple play earnings pushed the stock $12 higher on 7/31…

Continue reading our Conference Call Recap for META by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

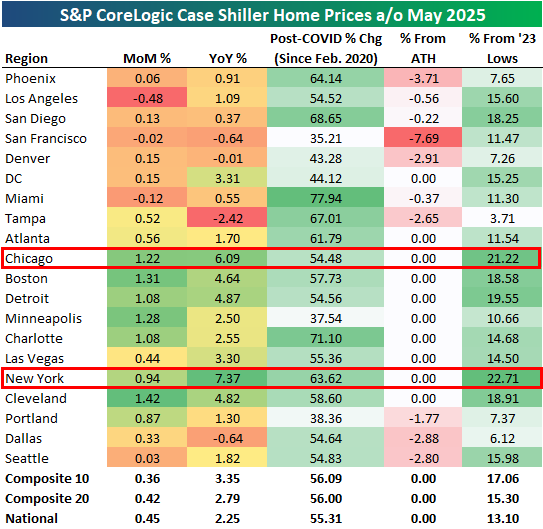

New York and Chicago On Top

The latest monthly data on home prices was published earlier this week from S&P CoreLogic’s Case Shiller indices. Case Shiller indices are published on a two-month lag, but they break down price levels across twenty major cities around the country.

Below is a look at the latest data. Seventeen of twenty cities were up month-over-month, with many cities up more than 1%: Chicago, Boston, Detroit, Minneapolis, Charlotte, and Cleveland. The three cities that were down m/m were Los Angeles, San Francisco, and Miami.

On a year-over-year basis, the national reading came in at +2.25%, but there’s quite a bit of disparity across cities. Tampa, Dallas, San Francisco, and Denver are actually down year-over-year, while New York and Chicago are up 6%+. New York is actually up the most of any city tracked over the last year with home price gains of 7.4%.

Exactly half of the twenty cities tracked hit new all-time highs in May. San Francisco is the city where prices are down the most from their highs at -7.7%.

Back in 2022 and early 2023, we saw a dip in home prices after seeing a huge post-COVID surge in 2020 and 2021. Since that dip, though, prices nationally have rallied roughly 13%. The two cities that have seen the biggest rallies since their 2023 lows are Chicago and New York, which are both up more than 20%.

In terms of prices, given their y/y readings and their gains since early 2023, New York and Chicago have been the hottest markets in the last couple of years. Conversely, the West Coast and Southeast have seen the most weakness.