The Closer – AI and Appetites, Sentiment, Consumers – 10/7/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we kick off with a look at Dell’s (DELL) AI exposure (page 1) followed by a review of the performance of quantum computing, nuclear, consumer, and travel stocks (page 2). We then switch over to investor sentiment (page 3) and next look abroad with a rundown on European auto sales (page 4). Following a recap of the latest consumer credit figures (page 5), we review the New York Fed’s Survey of Consumer Expectations (pages 6 and 7) and close out with a dive into the latest LMI report (pages 8 and 9).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Q3 2025 Earnings Conference Call Recaps: Constellation Brands (STZ)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Constellation Brands’ (STZ) Q2 2026 earnings call.

![]()

Constellation Brands (STZ) is one of the largest premium alcoholic beverage companies in the US, best known for its Mexican beer portfolio led by Modelo Especial, the top-selling beer by dollar sales in America, and Corona Extra. The company also owns a range of wine and spirits brands, including Kim Crawford, The Prisoner, and Mi CAMPO. With production facilities in Mexico and distribution across North America, Constellation offers investors a lens into US consumer spending, Hispanic demographic trends, and the broader beer industry’s pricing power. On the earnings call, management attributed slower beer volumes primarily to macroeconomic strain and weakened Hispanic consumer sentiment tied to ICE activity and financial anxiety. Despite this, Modelo and Corona loyalty improved, and Constellation continued investing in marketing through MLB and NFL partnerships. CFO Garth Hankinson cited $70M in beer tariffs and $500M in cumulative cost savings since its transformation. The company reaffirmed confidence that weakness is cyclical, not structural, and highlighted affordability initiatives like smaller packs and repositioned Modelo Oro. STZ shares opened 4.2% higher on 10/7 after posting better-than-expected results, though the stock declined intraday…

Continue reading our Conference Call Recap for STZ by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Q3 2025 Earnings Conference Call Recaps: McCormick (MKC)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers McCormick’s (MKC) Q3 2025 earnings call.

![]()

McCormick (MKC) is a huge name in flavor, known for its spices, herbs, seasonings, condiments, and flavor solutions for consumers and the food industry. Its iconic retail brands, like McCormick, Frank’s RedHot, French’s, and Cholula, line home pantries worldwide, while its flavor solutions division serves quick-service restaurants, packaged food companies, and beverage producers. The company provides insight into global food trends, from home-cooking and value-seeking habits to the rise of clean-label and health-driven reformulations. McCormick’s third-quarter call centered on navigating tariff and inflation headwinds while maintaining consumer demand. The company now expects $70 million in 2025 tariff costs (up from $50M) and a $140M annualized exposure, but is mitigating through pricing and productivity savings. Commodity costs rose faster than expected, pressuring gross margins by 120 bps. In China, retail sales grew despite foodservice softness tied to austerity measures. QSR (Quick Service Restaurant) volumes strengthened globally, offsetting CPG (Consumer Packaged Goods) weakness, and reformulation projects performed well as brands reduce sugar, salt, and artificial ingredients. Management highlighted sustained household cooking and health-conscious flavor innovation as long-term tailwinds…

Continue reading our Conference Call Recap for MKC by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day – Gearing up For Fall

Bespoke’s Morning Lineup – 10/7/25 – Whipsaw Semis

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“We learn from history that we don’t learn from history!” – Desmond Tutu

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

There’s not a lot going on in the futures market this morning, and once again, it will be another day without any economic data as the government remains closed. At this point, very few people have been affected by the shutdown, but as paydays come and go, the switchboards in DC will start heating up.

While there’s no economic data on the calendar, plenty of Fed officials are likely to speak, including Fed governors Bowman and Miran as well as Atlanta Fed President Bostic and Minneapolis Fed President Kashkari. The next Fed meeting is just three weeks away, and markets currently expect a 93% chance of another 25 basis point rate cut.

In Asian markets overnight, it was a quiet session. China and South Korea were closed while Japan finished marginally higher after trading up over 1% earlier in the session. The Yen weakened against the dollar again following the weekend election results as the likelihood of rate hikes declines, although a 30-year auction with a relatively high bid-to-cover ratio calmed some investor nerves.

European stocks are trading higher but by modest amounts, with the STOXX 600 trading up 0.2% with Italy (+0.6%) and France (+0.4%) leading the gains. German stocks aren’t performing as well following an unexpected decline in August Factory Orders (-0.8% vs 1.2%).

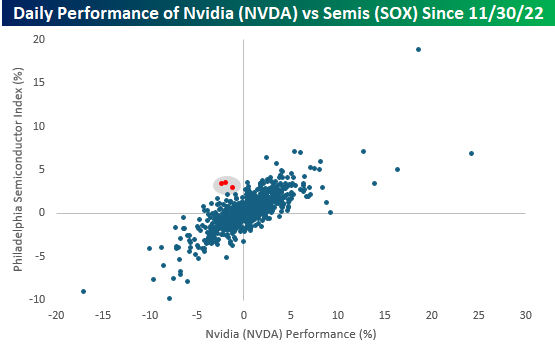

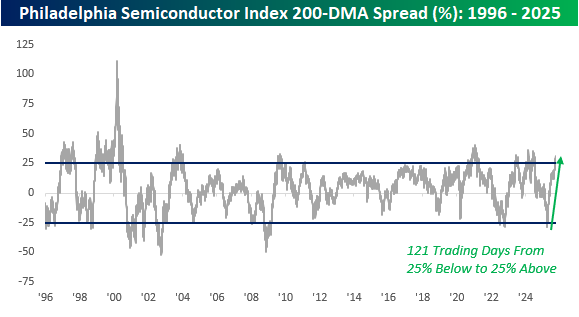

If you just looked at the performance of Nvidia (NVDA), which fell 1.1% yesterday, you probably would have thought semis had a bad day as well. You would have thought wrong. While NVDA was down, the Philadelphia Semiconductor Index (SOX) finished up 2.9%, and 24 of the index’s 30 components finished higher on the day. The scatter chart below compares the performance of NVDA (x-axis) to the SOX on every day since the launch of ChatGPT on 11/30/22, and during these 714 trading days, there have only been three where the SOX was up over 2.5% and NVDA traded down at least 1% on the day. In the post ChatGPT world, the SOX usually doesn’t rally without NVDA.

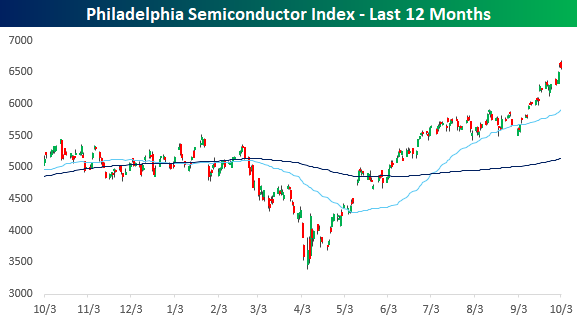

Given the broad strength in semis yesterday, the SOX continued it’s breakout from the summer consolidation and rallied to new highs yesterday. In the process, its price is now higher than the price of the S&P 500, something that only happened on a handful of other days back in 2004.

After yesterday’s rally, the SOX is now more than 31% above its 200-DMA. While that’s not unheard of for a volatile index like the SOX, the move from extreme oversold in April to extreme overbought now has been swift. In the span of 121 trading days, the SOX went from more than 25% below its 200-DMA to more than 25% above it. These kinds of reversals in the index have been uncommon.

The Closer – OpenAI-MD PCA, Bitcoin Breakout – 10/6/25

Log-in here if you’re a member with access to the Closer.

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we lead off with a commentary on the deal between OpenAI and AMD (AMD) and what that could mean for the broader AI space (page 1). We then preview this week’s earnings (page 2) before switching over to some principal component analysis (page 3). We wrap up tonight’s note with a check-in on Bitcoin’s breakout (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Bespoke’s Consumer Pulse Report – October 2025

Bespoke’s Consumer Pulse Report is an analysis of a huge consumer survey that we run each month. Our goal with this survey is to track trends across the economic and financial landscape in the US. Using the results from our proprietary monthly survey, we dissect and analyze all of the data and publish the Consumer Pulse Report, which we sell access to on a subscription basis. Sign up for a 30-day free trial to our Bespoke Consumer Pulse subscription service. With a trial, you’ll get coverage of consumer electronics, social media, streaming media, retail, autos, and much more. The report also has numerous proprietary US economic data points that are extremely timely and useful for investors.

We’ve just released our most recent monthly report to Pulse subscribers, and it’s definitely worth the read if you’re curious about the health of the consumer in the current market environment. Start a 30-day free trial for a full breakdown of all of our proprietary Pulse economic indicators.

Bespoke Stock Profile: Cloudflare (NET)

Chart of the Day: 30 in 6, 80 in 3

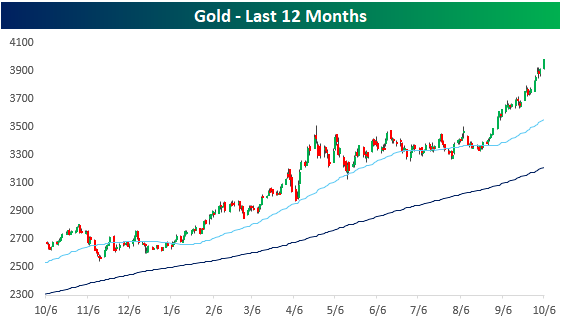

BNPL Fiscal Policy Drives Gold to New Highs

Japanese stocks surged over 4% to start the week after Sanae Takaichi was elected to lead Japan’s ruling party, positioning her to become the country’s first female prime minister. Last night’s rally propelled the Nikkei above 46,000 for the first time and extended the rally from the April lows to more than 56%!

The 4% gain in the Nikkei, however, is somewhat misleading, particularly for US investors. This is because Takaichi is seen as a fiscal dove; she once called recent Bank of Japan (BoJ) rate hikes “stupid,” and one of her advisers has publicly stated the BoJ shouldn’t raise rates this fall. Given her preference for expansionist monetary policy, the Yen plunged nearly 2% against the dollar immediately following the news. As a result, the Nikkei’s 4% gain in nominal terms is nearly cut in half on a dollar-adjusted basis. Still, even a 2% rally is impressive!

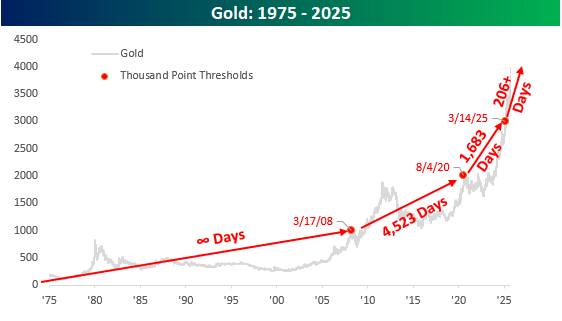

With one of the world’s five largest economies now being led by a noted fiscal dove who favors easy monetary policy and expanded government spending, investors concerned about profligacy are flocking to gold, continuing the massive breakout from its period of summer consolidation. As of early Monday afternoon trading, gold was less than 1% from crossing $4,000 for the first time.

The chart below shows gold’s long-term performance, noting the first time it closed above each thousand-point threshold. While every thousand points represents a smaller percentage gain relative to gold’s overall price, it’s still worth highlighting how each one has been crossed in closer proximity to the last. It took infinity days for gold to first close above $1,000. The next thousand took 4,523 days, and then it took less than half that time to first cross $3,000. Now, less than seven months later, here comes $4,000. Simple math says that each subsequent thousand-point threshold will be crossed more quickly, and the more that governments around the world take a “buy now, pay later” approach to governing, the faster each domino will fall by the wayside.