Bespoke’s Morning Lineup – 10/10/25 – Tech and Utilities Lead the Way

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“If you want a happy ending, that depends, of course, on where you stop your story.” – Orson Welles

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

US equity futures are modestly positive this morning following comments from potential Fed chair-in-waiting Christopher Waller, who said he expects the Fed to cut rates further this year, but at a ‘careful’ pace. Long-term treasury yields are notably lower as the 10-year yield trades down nearly 5 basis points to 4.10%. After dropping below $4,000 per ounce yesterday, gold is up nearly 1%, trading at $4,010. Crude oil prices are down over 1% on the prospects of peace in the Middle East, and crypto trades modestly higher at just about $121K.

With the government still shut down, the only economic data on the calendar is the University of Michigan Sentiment report, and Chicago Fed President Goolsbee will speak at a bank conference shortly after the open. Speaking of economic data, the BLS has recalled furloughed staff this morning to ensure that the September CPI report gets released by the end of the month.

Asian markets were weak overnight, with the notable exception of South Korea, which rallied 1.7%. Japan, Hong Kong, and China, however, were all down 1% or more. Japanese PPI increased 0.3% m/m, triple the rate of consensus expectations, solidified market expectations for another rate hike this year. Despite Friday’s decline, the Nikkei finished the week 5.1% higher while Hong Kong traded down 3.1% and China was up fractionally.

In Europe, equity markets have been much tamer this morning. The STOXX 600 is little changed, and no major country’s benchmark index is up or down more than 0.3%, and most are on pace to finish the week with modest gains or losses.

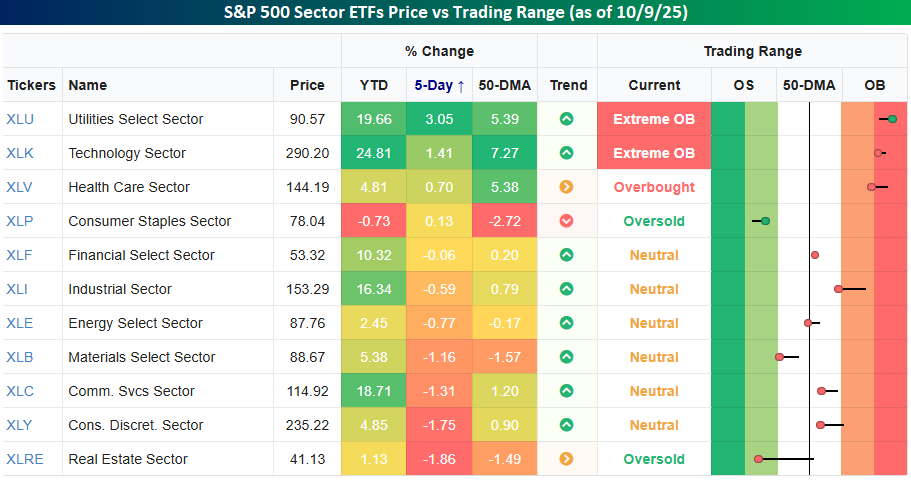

The last five trading days have been full of divergence at the sector level. The S&P 500 is fractionally higher, but seven out of eleven sectors have traded lower, including four sectors – Real Estate, Consumer Discretionary, Communication Services, and Materials – that are down over 1%. The only two sectors with gains of more than 1% are the formerly strange bedfellows of Utilities (3.05%) and Technology (1.4%). Both these sectors are also the only two trading at Extreme Overbought levels.

It wasn’t long ago that Utilities was considered the most defensive sector in the market, while Technology was considered the most risky sector. Like everything else now, it seems, AI has upended prior norms, although given the power-intensive nature of AI-related applications, the moves make sense.

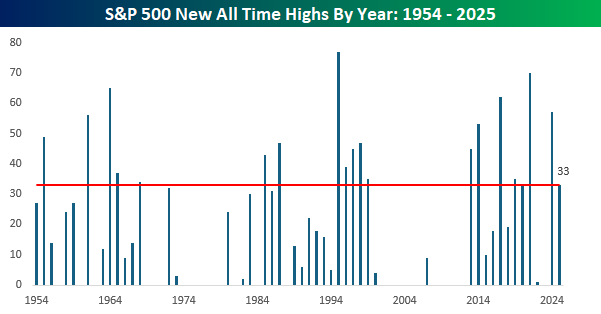

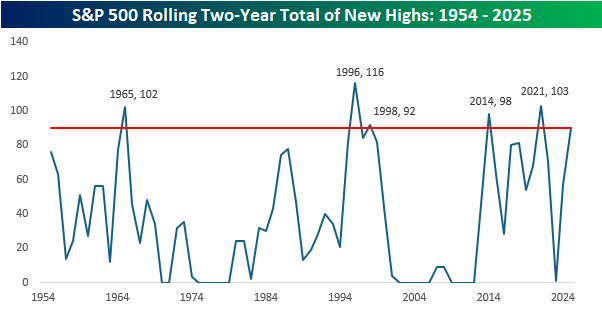

Yesterday was a down day for the S&P 500, but in the seven trading days this month, there have already been five record closes, taking the YTD total to 33. If the year were to end today, 33 record highs in a year isn’t particularly noteworthy as it ranks tied for the 19th most since 1954.

What’s been more impressive is that the 33 record closes followed last year’s total of 57. With 90 record closing highs in the last two calendar years, there have only been five other two-year stretches when the S&P 500 had more record closing highs, and not to jinx anything, but there’s a legitimate chance that by the end of the year, the last two years could end up ranking well into the top five.

Q3 2025 Earnings Conference Call Recaps: Delta Air Lines (DAL)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers Delta Air Lines’ (DAL) Q3 2025 earnings call.

![]()

Delta Air Lines (DAL) is one of the world’s largest and most profitable carriers, serving more than 275 destinations across six continents. The company’s revenue model extends beyond ticket sales to include high-margin businesses like loyalty programs, premium seating, maintenance services, and cargo. Delta’s SkyMiles ecosystem, anchored by its co-brand partnership with American Express, has become a key differentiator, blending travel, finance, and lifestyle benefits. Delta offers investors a window into broader consumer and corporate travel trends, economic confidence, and the health of affluent spending. The company reported record third-quarter revenue of $15.2 billion, up 4%. Corporate travel rebounded 9%, buoyed by resilient business confidence and rising demand for premium seats. Domestic main cabin revenue turned positive as competitors cut unprofitable capacity, while Transatlantic performance lagged but is being recalibrated with flatter seasonal flying. Premium and loyalty growth remain standouts. Amex remuneration rose 12% to $2 billion, and premium seat retention sits above 80%. Executives also noted deepening industry bifurcation, with Delta and United capturing the majority of airline profits. The stock was up more than 4% on 10/9 after posting stronger-than-expected results…

Continue reading our Conference Call Recap for DAL by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

The Closer – ETF AUM and Fee Analysis – 10/9/25

Log-in here if you’re a member with access to the Closer.

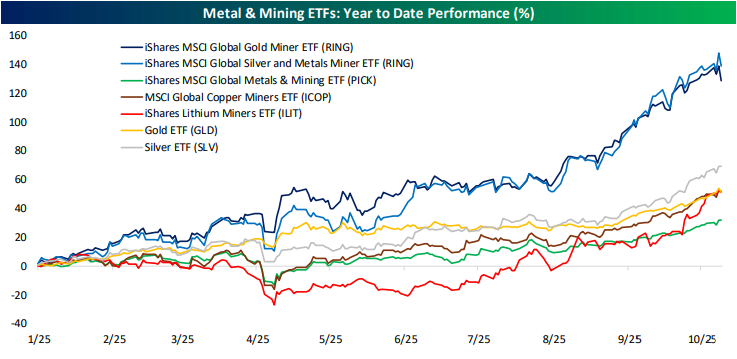

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with an overview of ETF markets including the emerging dominance of Bitcoin funds (pages 1 and 2). Next we discuss breakeven employment (page 3) before closing with a checkup on metal mining stocks’ outperformance versus gold (page 4).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

Q3 2025 Earnings Conference Call Recaps: PepsiCo (PEP)

Bespoke’s Conference Call Recaps use AI to summarize lengthy earnings calls. The commentary below is AI-generated and then edited by Bespoke for quality control. As always, none of these summaries should be construed as recommendations to buy or sell any securities, and investors should do their own research and/or consult with a financial professional before making any investment decisions.

Our latest recap available to Bespoke subscribers covers PepsiCo’s (PEP) Q3 2025 earnings call.

![]()

PepsiCo (PEP) is a global food and beverage leader whose portfolio includes household staples like Lay’s, Doritos, Cheetos, Quaker, Gatorade, and Pepsi. Operating in more than 200 countries, it serves consumers across retail and foodservice channels. Pepsi’s innovation pipeline, ranging from zero-sugar beverages and functional hydration to protein and fiber-enhanced snacks, puts it at the center of evolving health, affordability, and convenience trends worldwide. The company’s Q3 call focused on regaining volume growth amid affordability pressures and a slower consumer backdrop. Management highlighted a return to balanced price and volume growth, aided by sharper price-pack architecture and innovation across Lay’s, Tostitos, and Gatorade. The company is betting on “better-for-you” offerings like Muscle Milk, Propel for GLP-1 users, and avocado-oil snacks to carry 2026 momentum. Away-from-home sales grew 2–3X retail, while international demand rebounded in September after weather-related softness. Executives also outlined factory and warehouse improvements, Texas “One North America” logistics pilots, and broader AI-driven supply-chain modernization to support margin expansion next year. Shares rose more than 3% in reaction to EPS and revenue beats on 10/9…

Continue reading our Conference Call Recap for PEP by becoming a Bespoke Institutional subscriber. You can sign up for Bespoke Institutional now and receive a 14-day trial to read our newest Conference Call Recap. To sign up, choose either the monthly or annual checkout link below:

Chart of the Day: Microcap Rally Despite Results

Bespoke’s Morning Lineup – 10/9/25 – 18 Years

See what’s driving market performance around the world in today’s Morning Lineup. Bespoke’s Morning Lineup is the best way to start your trading day. Read it now by starting a two-week trial to Bespoke Premium. CLICK HERE to learn more and start your trial.

“Reality leaves a lot to the imagination.” – John Lennon

Below is a snippet of commentary from today’s Morning Lineup. Start a two-week trial to Bespoke Premium to view the full report.

Futures are flat with a negative bias this morning as the relentless rally in gold takes a pause, and oil prices see a marginal pullback. Stocks in Asia were higher overnight as China reopened for trading, and shares of Softbank surged more than 10% after announcing a deal to acquire the robotics units of ABB for $5.4 billion. In Europe, trading has been listless with the STOXX 600 down 0.04%.

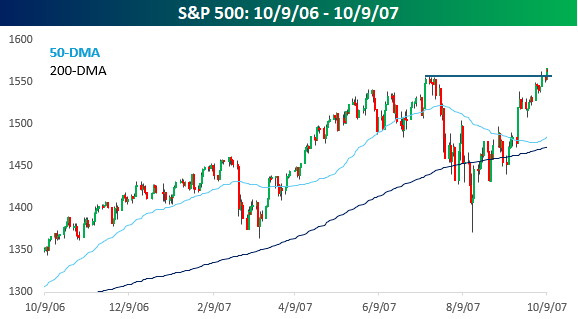

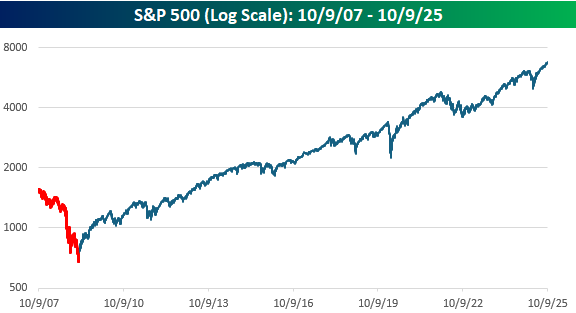

The S&P 500 closed at another all-time high yesterday, just like it did 18 years ago today on 10/9/07. That new high in 2007 followed a late-summer peak-to-trough correction of nearly 12%. It was a time of stress in the financial system as the subprime housing market was in the process of imploding, but the Fed was cutting rates, and the damage ‘appeared’ contained. From a technical perspective, the S&P 500 had traded above resistance to new highs, and the 50-DMA, which has been sloping downwards, turned higher just above its 200-DMA, which was also rising. The one caveat was that the breakout to new highs wasn’t especially convincing, as the S&P 500 had only made a marginal new high.

Investors breathed a sigh of relief on 10/9/07, but in the days that followed, the S&P 500 couldn’t follow through on its breakout, and within days, it was back below its summer 2007 highs. Shortly after that, the wheels came off, and the crash began. A year after the October 2007 high, the S&P 500 cratered more than 40%. As loud as the sighs of relief were in October 2007, they had nothing on VIX screamings towards 80 a year later as the entire banking system was on the verge of collapse.

The experience of October 2007 should serve as a reminder that even in the best times, investors should always be prepared for the possibility that the light at the end of the tunnel is a freight train steaming right at us. It’s only fitting this morning that on the anniversary of the 2007 peak, JP Morgan (JPM) CEO Jamie Dimon is in the news, warning of a correction in the market at some point in the next six months to two years. At first glance, that statement seems like something you would hear coming from Captain Obvious. Of course, there will be a correction in the next six months to two years! Stock market corrections occur on average about once a year, so there may actually be two!

If you read more into Dimon’s comments, though, he’s talking more about a serious bear market than a 10% correction. Even still, six months to two years isn’t really a precise forecast. While Dimon’s comments may not be of much use to investors or traders looking for any direction on where the stock market is going, they are exactly the kind of comments you want to hear from the CEO of America’s largest bank. That’s why JP Morgan Chase is just about the only major bank where the name on the CEO’s door is the same now as it was then. Dimon has earned the right to worry!

As bad as the declines were following the October 2007 high, as we always say when it comes to the market, time heals. It took several years, but eventually the market went on to make new highs, and this morning, the S&P 500 will open more than four times higher than it was when it closed at that peak 18 years ago.

The Closer – Central Banks, Gold, Micro-Cap – 10/8/25

Log-in here if you’re a member with access to the Closer.

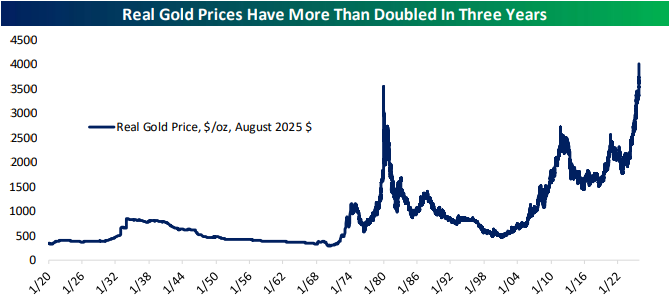

Looking for deeper insight into markets? In tonight’s Closer sent to Bespoke Institutional clients, we begin with a look into global push toward rate cuts in addition to the Fed minutes (page 1). We then show real gold prices and a handful of other insights on the yellow metal (pages 2 -4). We then finish with a check up on the surging performance in micro-cap stocks (page 5) and an update on crude inventories (page 6).

See today’s full post-market Closer and everything else Bespoke publishes by starting a 14-day trial to Bespoke Institutional today!

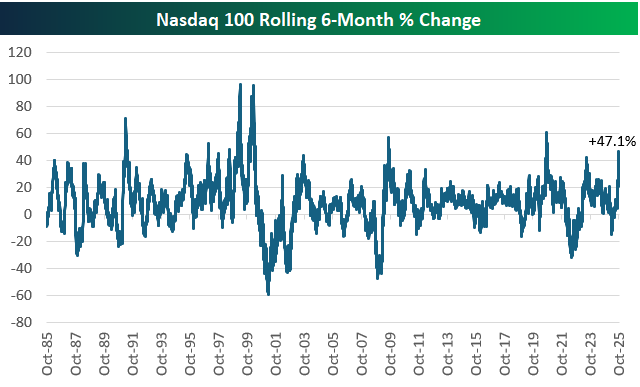

A Strong Six Months

Today marked six months since the US stock market made its “tariff crash” closing low on April 8th.

As shown below, the tech-heavy Nasdaq 100 has rallied 47.1% over the last six months. That’s definitely on the high-end for all six-month moves in the index’s history, and it’s the biggest six-month pop since the initial rally back from the COVID Crash back in early 2020.

Amazingly, in the late 1990s during the height of the Dot Com Bubble, we saw two six-month runs of nearly 100% within a year of each other in early 1999 and early 2000.

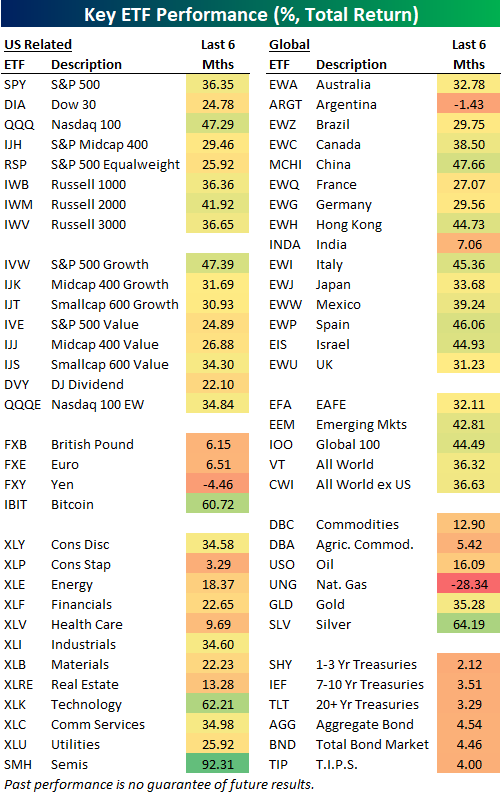

Of the major equity index ETFs in the US, the Nasdaq 100 (QQQ) has rallied the most over the last six months (+47%), while the S&P 500 (SPY) is up 36.4% and the Dow 30 (DIA) is up 24.8%. Small-caps (IWM) have rallied a solid 41.9%, while mid-caps (IJH) are up less at 29.5%.

Looking at the eleven major sector ETFs, Technology (XLK) is the only one that has done better than SPY since the 4/8 low with a gain of 62.2%. Consumer Staples (XLP) and Health Care (XLV) are both up less than 10%. Within the Tech sector, the semis (SMH) are up a remarkable 92.3%; the best performing ETF in our matrix over the last six months.

Outside of the US, plenty of country ETFs have gained 40%+ like China (MCHI), Hong Kong (EWH), Italy (EWI), Spain (EWP), and Israel (EIS). India (INDA) is up just 7.1%, while Argentina (ARGT) has actually fallen 1.4%.

Gold (GLD) has kept right up with equities since 4/8 with a gain of 35.3%. Silver (SLV) is up nearly twice as much with a gain of 64.2%, while the Bitcoin ETF (IBIT) is up 60.7%.

Across Treasury and fixed income ETFs, we’ve seen gains from 2-4.5%.

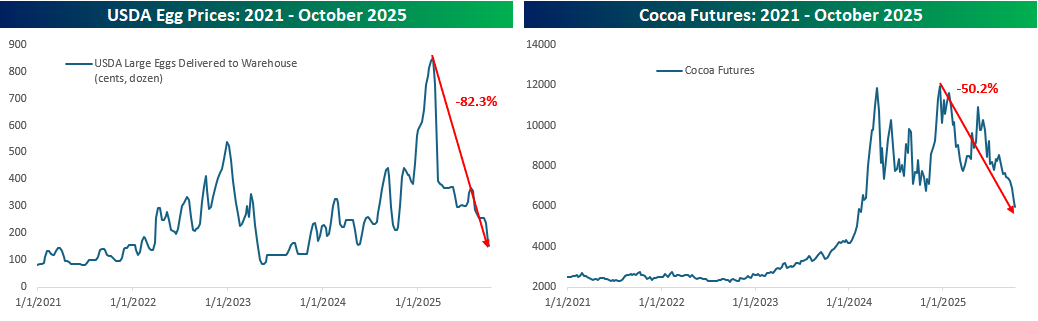

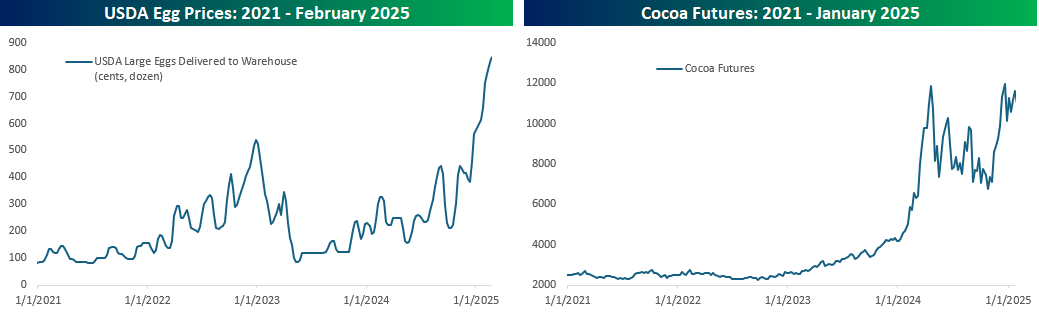

What Ever Happened to Egg and Cocoa Prices?

Remember earlier in the year when rising egg and chocolate prices threatened to cancel breakfast and Valentine’s Day? In the case of eggs, retailers, who could get their hands on them, even limited the number of eggs customers could purchase. Regarding chocolate, there were stories about manufacturers reducing the number of chocolate pieces or chips they included in their various products, like ice cream and cookies. The charts below illustrate the spikes in both commodities through their highs earlier in the year, and the media ran with it, extrapolating these events to warn of impending inflation spirals in the global food chain.

While the stories were all over business and even mainstream news earlier in the year, when was the last time you heard about egg or cocoa prices? Probably not recently, right? Have you wondered why? Maybe the updated charts below explain why. From their highs earlier in the year, egg prices have declined by 82% and cocoa prices are down by half. Given the frenzy over higher prices back then, why aren’t there as many warnings of a deflationary spiral in food prices now? When it comes to commodities, the cure for higher prices has always been higher prices.